医療用エラストマー:市場シェア分析、産業動向と統計、成長予測(2025~2030年)

Medical Elastomers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1641888

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

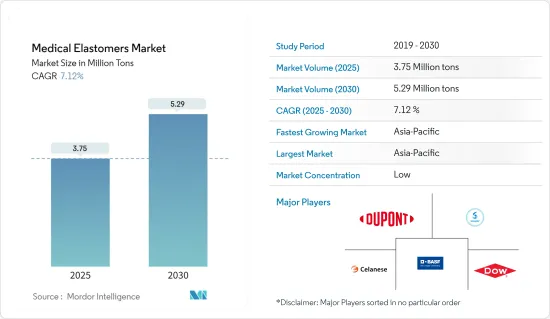

医療用エラストマー市場規模は2025年に375万トンと推定され、予測期間(2025~2030年)のCAGRは7.12%で、2030年には529万トンに達すると予測されます。

市場は2020年のCOVID-19によってマイナスの影響を受けました。全国的な封鎖と厳しい社会的距離の義務化により、市場のさまざまなセグメントでサプライチェーンが混乱しました。しかし、医療への投資の増加により、市場は安定的に成長すると予想されます。

主要ハイライト

- 安全なハロゲンフリーポリマーへの需要と、ウェアラブル医療機器や外部から相互通信可能な医療機器への医療産業のシフトが市場を牽引しています。

- シングルユース機器の使用減少やシリコーンの価格上昇が、市場の成長を鈍らせる要因となっています。医療用エラストマー産業は、環境意識の高まりとともに、持続可能で環境に優しいプロジェクトへと移行しています。

- バイオベースの熱可塑性エラストマーの開発は主要な市場機会です。

アジア太平洋が世界市場を席巻しており、中国、インドなどでの消費が最も多いです。

医療用エラストマー市場動向

熱可塑性エラストマー(TPE)セグメントが急成長

- 医療用エラストマー市場では、熱可塑性エラストマー(TPE)セグメントが最大のシェアを占めています。

- 医療産業では、スチレン系ブロック共重合体(SBC)が主に医療用チューブやフィルム用途に使用されています。また、手術用ドレープ、針シールド、歯科用ダム、点滴室、運動用バンド、注射器プランジャーチップ、呼吸器用機器、整形外科用部品、医療用パッチなどの医療用バッグ、創傷ケア、機器、包装、診断用製品の製造にも使用されています。

- 熱可塑性ポリウレタン(TPU)は長鎖の直鎖ポリマーで、ポリウレタンを溶かして部品を形成し、その後部品を固化させることができます。TPUの高性能特性、化学品や油に対する耐性、機械的特性の向上、耐久性の強化により、医療用途での使用は一貫して増加しています。

- ポリ塩化ビニル(PVC)は線状の熱可塑性ポリマーで、ほとんどが非晶性です。可塑化ポリ塩化ビニル(PVC-P)または軟質PVCは、可塑化することで柔軟性、強度、透明性、耐キンク性、耐スクラッチ性、ガス透過性、生体適合性、一般的な溶剤や接着剤での接着のしやすさ、ガンマ線滅菌、エチレンオキサイド滅菌、電子線滅菌時の安定性など、さまざまな特性を発揮するため、医療用途に使用されています。

- 医療産業では、TPVはOリング、ソフトタッチグリップ、蠕動ポンプチューブ、シリンジチップ、ボトルドロッパー、ストップシール、ガスケット、バルブ、ダイヤフラム、各種医療機器用チューブの製造に使用されています。また、医療産業では注射器のプランジャーのガスケットとしても使用されています。

以上のような要因から、世界の医療産業における熱可塑性エラストマーの需要は、市場に影響を与える可能性が高いです。

アジア太平洋が市場を独占

- アジア太平洋では、中国とインドが市場を独占すると予想される2大経済大国です。

- 中国は過去5年間に公立病院への投入額を2倍の380億米ドルに増やしました。2030年までに医療産業の価値を現在の2倍以上の2兆3,000億米ドルに引き上げることを目指しています。

- さらに、中国政府は国内の医療機器イノベーションを支援・奨励する施策を開始し、市場調査の機会を提供しています。「メイド・イン・チャイナ2025」イニシアティブは、産業の効率、製品の品質、ブランドの評判を向上させ、国内医療機器メーカーの開発に拍車をかけ、競合を高めています。

- 中国は世界第2位の医療市場です。しかし、同国は先進国から技術的にハイエンドのインプラントを輸入しています。国内の医療機器の主要消費者は公立病院です。2021年、医療への公的支出は1兆9,200億元でした。

- インドでは2021年末、連邦保健相が国内の医療施設を改善するためのインド政府のさまざまな計画を発表しました。政府は今後6年間で医療セグメントに6,418億インドルピーを投資する計画です。政府は、一次、二次、三次医療システムと新・新興疾患の発見と治療のための機関の能力を開発することにより、既存の「国民健康ミッション」を強化する計画です。

- COVID-19の発生による様々な医療用途からの需要の増加は、予測期間中、医療用エラストマー市場を牽引すると推定されます。

医療用エラストマー産業概要

世界の医療用エラストマー市場は、少数の大手企業が優位を占め、多くのローカル企業が存在する断片的な性質を持っています。市場の主要企業には、BASF SE、Celanese Corporation、DOW、Solvay、DuPontなどがあります(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 安全でハロゲンフリーのポリマーに対する需要の高まり

- その他の促進要因

- 抑制要因

- 単回使用機器の減少

- シリコーン価格の上昇

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- タイプ

- 熱可塑性エラストマー

- スチレン系ブロック共重合体(SBC)

- 熱可塑性ポリウレタン(TPU)

- 可塑化ポリ塩化ビニル(PVC)

- 熱可塑性バルカニゼット(TPV)

- その他の熱可塑性エラストマー

- 熱硬化性エラストマー

- シリコーン

- 液状シリコーンゴム(LSR)

- 高コンシステンシーゴム(HCR)

- その他のシリコーン

- 天然ゴム(ラテックス)

- ブチルゴム

- その他熱硬化性エラストマー

- 熱可塑性エラストマー

- 用途

- 医療用チューブ

- カテーテル

- 注射器

- 不織布・フィルム

- 手袋

- 医療用バッグ

- インプラント

- その他

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Arkema Group

- AVANTOR Inc.

- Avient

- BASF SE

- Biomerics

- Celanese Corporation

- Covestro AG

- DOW

- DSM

- DuPont de Nemours inc.

- Eastman Chemical Company

- ExxonMobil Corporation

- Foster Corporation

- Hexpol AB

- Kraton Corporation

- Kuraray Co.Ltd.

- Momentive

- Romar

- RTP Company

- Solvay

- Sumitomo Rubber Industries Ltd.

- Tekni-Plex

- Teknor Apex

- The Rubber Group

第7章 市場機会と今後の動向

- バイオベース熱可塑性エラストマーの採用

目次

The Medical Elastomers Market size is estimated at 3.75 million tons in 2025, and is expected to reach 5.29 million tons by 2030, at a CAGR of 7.12% during the forecast period (2025-2030).

The market was negatively impacted by COVID-19 in 2020. The nationwide lockdowns and stringent social distancing mandates led to supply chain disruptions across different segments of the market. However, the market is expected to grow steadily owing to increasing investments in healthcare.

Key Highlights

- The demand for safe, halogen-free polymers and the shift in the medical industry toward wearable health devices and medical tools that can talk to each other from the outside are the main things driving the market.

- Decreasing usage of single-use devices and the increasing prices of silicone are the factors that may slow down the market's growth. The medical elastomer industry is moving toward sustainable and green projects as environmental awareness grows.

- The development of bio-based thermoplastic elastomers is the key market opportunity.

Asia-Pacific dominated the market across the globe, with the largest consumption in countries such as China, India, etc.

Medical Elastomers Market Trends

Thermoplastic Elastomers (TPE) Segment to Register Fastest Growth

- Among the types, the thermoplastic elastomers (TPE) segment is the largest market shareholder in the medical elastomers market.

- In the medical industry, Styrenic Block Copolymers (SBCs) are mainly used in medical tubing and film applications. They are also used in the manufacturing of medical bags, wound care, equipment, packaging, and diagnostic products, including surgical drapery, needle shields, dental dams, drip chambers, exercise bands, syringe plunger tips, respiratory equipment, orthopedic parts, medical patches, and others.

- Thermoplastic polyurethanes (TPU) are long-chain linear polymers, which allow the polyurethane to be melted to form parts, and then the parts are solidified. The usage of TPU in medical applications is consistently increasing, owing to its high-performance characteristics, resistance to chemicals and oils, improved mechanical properties, and enhanced durability.

- Polyvinyl chloride (PVC) is a linear, thermoplastic, mostly amorphous polymer. Plasticized Polyvinyl Chloride (PVC-P) or flexible PVC is used for medical applications as it offers various properties when plasticized, including flexibility, strength, transparency, kink resistance, scratch resistance, gas permeability, biocompatibility, ease of bonding with common solvents or adhesives, and stability during gamma, ethylene oxide, or E-beam sterilization, among others.

- In the medical industry, TPVs are used in the manufacturing of O-rings, soft touch grips, peristaltic pump tubes, syringe tips, bottle droppers, stop seals and gaskets, valves, diaphragms, and tubing for various medical devices. They are also used in the medical industry as a gasket on syringe plungers.

Due to the aforementioned factors, the demand for thermoplastic elastomers in the global medical industry is likely to affect the market.

Asia-Pacific Region to Dominate the Market

- In the Asia-Pacific region, China and India are two major economies that are expected to dominate the market.

- China has doubled the amount, it had been pouring into public hospitals in the last five years, to USD 38 billion. It aims to raise the healthcare industry's value to USD 2.3 trillion by 2030, more than twice its size now.

- Furthermore, the Chinese government has started policies to support and encourage domestic medical device innovation providing opportunities for the market studied. The 'Made in China 2025' initiative improves industry efficiency, product quality, and brand reputation, which will spur the development of domestic medical device manufactures and will increase competitiveness.

- China is the second-largest healthcare market in the world. However, the country imports technologically high-end implants from advanced economies. The public hospitals in the country are leading consumers of medical devices in the country. In 2021, the public expenditure done on healthcare was 1.92 trillion yuan.

- In India, in late 2021, the Union Health Minister announced various plans of the Indian government to improve healthcare facilities in the country. The government plans to invest INR 64,180 crore in healthcare sector over the next six years in the country. The government plans to strengthen the existing 'National Health Mission' by developing capacities of primary, secondary, and tertiary healthcare systems and institutions for detection and cure of new and emerging diseases.

- The increasing demand from various medical applications due to the COVID-19 outbreak is estimated to drive the market for medical elastomers during the forecast period.

Medical Elastomers Industry Overview

The global medical elastomer market is fragmented in nature with the dominance of a few large players and the existence of many local players. Some of the major players in the market include (not in any particular order) BASF SE, Celanese Corporation, DOW, Solvay, and DuPont, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rise in Demand for Safe and Halogen-free Polymers

- 4.1.2 Other Drivers

- 4.2 Restraints

- 4.2.1 Decreasing Usage of Single-Use Devices

- 4.2.2 Increases Prices of SIlicone

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Thermoplastic Elastomer

- 5.1.1.1 Styrenic Block Copolymers (SBC)

- 5.1.1.2 Thermoplastic Polyurethane (TPU)

- 5.1.1.3 Plasticized Polyvinyl Chloride (PVC)

- 5.1.1.4 Thermoplastic Vulcanizate (TPV)

- 5.1.1.5 Other Thermoplastic Elastomers

- 5.1.2 Thermoset Elastomer

- 5.1.2.1 Silicones

- 5.1.2.1.1 Liquid silicone rubber (LSR)

- 5.1.2.1.2 High consistency rubber (HCR)

- 5.1.2.1.3 Other Silicones

- 5.1.2.2 Natural Rubber (Latex)

- 5.1.2.3 Butyl Rubber

- 5.1.2.4 Other Thermoset Elastomers

- 5.1.1 Thermoplastic Elastomer

- 5.2 Application

- 5.2.1 Medical Tubes

- 5.2.2 Catheters

- 5.2.3 Syringes

- 5.2.4 Non-wovens and Films

- 5.2.5 Gloves

- 5.2.6 Medical Bags

- 5.2.7 Implants

- 5.2.8 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Arkema Group

- 6.4.2 AVANTOR Inc.

- 6.4.3 Avient

- 6.4.4 BASF SE

- 6.4.5 Biomerics

- 6.4.6 Celanese Corporation

- 6.4.7 Covestro AG

- 6.4.8 DOW

- 6.4.9 DSM

- 6.4.10 DuPont de Nemours inc.

- 6.4.11 Eastman Chemical Company

- 6.4.12 ExxonMobil Corporation

- 6.4.13 Foster Corporation

- 6.4.14 Hexpol AB

- 6.4.15 Kraton Corporation

- 6.4.16 Kuraray Co.Ltd.

- 6.4.17 Momentive

- 6.4.18 Romar

- 6.4.19 RTP Company

- 6.4.20 Solvay

- 6.4.21 Sumitomo Rubber Industries Ltd.

- 6.4.22 Tekni-Plex

- 6.4.23 Teknor Apex

- 6.4.24 The Rubber Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Introduction of Bio-based Thermoplastic Elastomer in Market

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日