高速度鋼-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

High Speed Steel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1641887

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

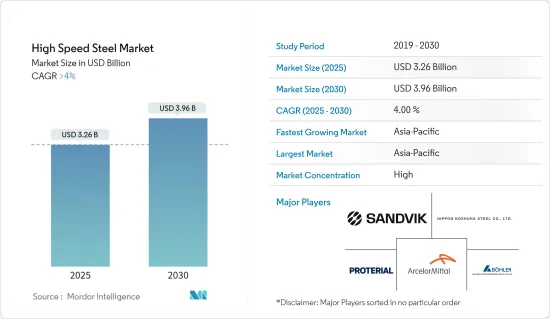

高速度鋼市場規模は2025年に32億6,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは4%を超え、2030年には39億6,000万米ドルに達すると予測されます。

COVID-19の大流行は世界の高速度鋼(HSS)市場に大きな影響を与え、サプライチェーンの混乱と需要の減少を引き起こしました。しかし、2021年以降、経済が再開し、産業活動が再開したため、市場は徐々に回復しています。サプライチェーンの回復力に再び注目が集まっています。自動車や航空宇宙などの産業が勢いを取り戻すにつれて、HSSの需要は増加し、市場のさらなる回復が見込まれます。

主要ハイライト

- 市場成長の主要要因は、産業用途の増加と航空宇宙産業からの需要の増加です。

- さまざまな最終用途セグメントで超硬ベースの切削工具の使用が増加していることが、市場の成長を鈍らせる可能性が高いです。

- 今後数年間は、技術の急速な変化により高速度鋼市場の成長が見込まれます。

- 予測期間中、アジア太平洋が高速度鋼市場を独占すると予想されます。

高速度鋼市場動向

自動車産業が市場を独占する見込み

- 高速度鋼は、自動車の軽量化、高剛性化、場所によってはエネルギー吸収に優れるなど、自動車産業で様々な形で使用されています。

- 高速度鋼は、機械的特性と範囲、厚さと幅の能力、熱間と冷間圧延の可用性、コーティングの仕様、化学組成の仕様など、自動車産業での需要を高める様々な特性を持っています。

- 自動車産業では、鋼材の強度は通常、その化学組成、熱履歴、生産スケジュール中に通過する変形プロセスに基づいて変化する微細構造によって決定されます。

- 高速度鋼は、特に重量が燃料の使用率に大きく影響する自動車産業では、通常の鋼よりも多くの利点があります。溶接性、疲労、静的強度、カソード保護、耐水素脆化性などの機械的特性は、自動車産業にとって有用です。

- 高速度鋼は、カムシャフトやクランクシャフトスプロケット、コネクティングロッド、シンクロナイザーリング、ベアリングキャップ、オイルポンプギアなどの構造用途に使用されています。これらの用途に使用されるステンレスには、エンジンのバルブシートも含まれます。Fe-Cr-Mn-Si系材料などの鉄系合金は、ショックアブソーバー部品、油圧システム用フィルター、マニホールド・フランジ、排気コンバーター出口フランジ、排気ガス再循環システムなどに使用されます。

- 自動車産業は、パンデミック以降、従来型自動車と電気自動車の両方の需要が急増しています。

- 国際自動車工業会(OICA)によると、2022年には世界中で約8,501万台の自動車が生産され、2021年の8,020万台と比較して5.99%の成長率を示しました。

- 北米では、OICAによると、2022年の自動車生産台数は1,479万8,146台で、2021年の1,346万7,065台に比べ9.88%増加しました。さらに北米では、2022年の電気自動車販売台数が110万8,000台となり、2021年の74万8,000台と比較しました。

- 欧州では、ドイツが主要な自動車メーカーのひとつです。ドイツの自動車製造業は、欧州の自動車生産全体の有力な株主です。同国には、Volkswagen、Mercedes-Benz、Audi、BMW、Porscheなど、主要な自動車製造ブランドがあります。

- 国際自動車製造者機構(OICA)によると、2022年の同国の自動車生産台数は367万7,820台で、2021年の330万8,692台に比べ11%増加しました。

- 全体として、燃費向上と自動車軽量化のための高速度鋼の使用増加が自動車産業の成長を後押しします。

アジア太平洋が市場を独占する見込み

- 今後数年間、アジア太平洋が高速度鋼の最大市場になると予想されます。中国やインドなどの国々では、自動車、航空宇宙などの産業が成長し、高速度鋼の需要が急増しています。

- アジア太平洋の生産と販売は、主に中国、インド、日本などの国々が独占しており、これらの国々は大手自動車メーカーと膨大な数の生産拠点で構成されています。

- 中国汽車工業協会(CAAM)によると、2022年の自動車総生産台数は2,700万台と、2021年比で3.4%増加し、中国は世界的に最も重要な自動車生産拠点となりました。

- 中国では、電気自動車の生産と販売を拡大することに主眼が置かれています。同国は2025年までに年間700万台の電気自動車を生産する目標を掲げています。2025年までに、中国の新車生産台数の20%を電気自動車にすることを目標としています。

- インドはこの地域で第2位の自動車メーカーとなりました。インド自動車工業会(SIAM)によると、2022~23年には、2021~2022年度比で約12.55%増加し、2,593万1,867台を記録しました。

- 日本自動車工業会によると、2023年度の国内自動車生産台数は14.84%増の899万8,538台を記録しました。

- 予測期間中、こうした変化により高速度鋼のニーズが高まる可能性が高いです。

高速度鋼産業概要

高速度鋼市場は、その性質上、部分的に統合されています。市場の主要企業には、Sandvik AB、voestalpine BOHLER Edelstahl GmbH & Co.KG、NIPPON KOSHUHA STEEL、PROTERIAL Ltd、ArcelorMittalなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- さまざまな産業用途での用途拡大

- 航空宇宙産業からの需要増加

- その他の促進要因

- 抑制要因

- 様々な最終用途部門における超硬ベースの切削工具の使用の増加

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- タイプ

- タングステン高速度鋼

- モリブデン高速度鋼

- その他のタイプ(コバルト高速度鋼、クロム高速度鋼、バナジウム高速度鋼)

- 製品タイプ

- 金属切削工具

- 冷間工具

- その他の製品タイプ(フライス工具、ドリル工具など)

- エンドユーザー産業

- 自動車産業

- 航空宇宙

- プラスチック

- その他のエンドユーザー産業(鉱業、製造、工具製造など)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- ノルディック

- トルコ

- ロシア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- ナイジェリア

- カタール

- エジプト

- アラブ首長国連邦

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)分析**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- ArcelorMittal

- CRS Holdings LLC

- ERASTEEL

- Friedr. Lohmann GmbH

- NACHI-FUJIKOSHI CORP.

- NIPPON KOSHUHA STEEL CO. LTD

- PROTERIAL Ltd

- Sandvik AB

- thyssenkrupp AG

- VILLARES METALS SA

- voestalpine BOHLER Edelstahl GmbH & Co. KG

第7章 市場機会と今後の動向

- 急速な技術向上

- その他の機会

目次

The High Speed Steel Market size is estimated at USD 3.26 billion in 2025, and is expected to reach USD 3.96 billion by 2030, at a CAGR of greater than 4% during the forecast period (2025-2030).

The COVID-19 pandemic significantly impacted the global high-speed steel (HSS) market, causing disruptions in supply chains and reducing demand. However, since 2021, the market has been gradually recovering as economies reopened and industrial activities resumed. There is a renewed focus on supply chain resilience. As industries like automotive and aerospace regain momentum, the demand for HSS is expected to increase, driving further recovery in the market.

Key Highlights

- The major factors driving the market's growth are the growing number of industrial uses and the increasing demand from the aerospace industry.

- The growing use of carbide-based cutting tools in different end-use sectors is likely to slow the market's growth.

- In the coming years, the high-speed steel market is expected to grow due to the rapid changes in technology.

- Asia-Pacific is expected to dominate the high-speed steel market over the forecast period.

High Speed Steel Market Trends

The Automotive Industry is Expected to Dominate the Market

- High-speed steel is used in many ways in the automotive industry to make vehicles lighter, stiffer, and better at absorbing energy in some places.

- High-speed steel has various properties that enhance its demand in the automotive industry, such as mechanical properties and ranges, thickness and width capabilities, hot- and cold-rolled availability, coating specifications, and chemical composition specifications.

- In the automotive industry, steel's strength is usually determined by its microstructure, which varies based on its chemical makeup, its history with heat, and the deformation processes it goes through during its production schedule.

- High-speed steel has a lot of advantages over regular steel, especially in the automotive industry, where weight is a significant factor in how well fuel is used. The mechanical properties, such as weldability, fatigue, static strength, cathodic protection, and resistance to hydrogen embrittlement, are useful to the auto industry.

- High-speed steel is used in structural applications such as camshaft and crankshaft sprockets, connecting rods, synchronizer rings, bearing caps, oil pump gears, etc. The stainless steel used in these applications includes engine valve seats. Ferrous-based alloys, such as Fe-Cr-Mn-Si materials, are used in shock absorber parts, filters for hydraulic systems, manifold flanges, exhaust converter outlet flanges, and exhaust gas recirculation systems.

- The automotive industry has been witnessing an upsurge in demand for both conventional and electric vehicles post-pandemic, primarily due to the increased traveling activities of people across the globe.

- According to the International Organization of Motor Vehicle Manufacturers (OICA), in 2022, around 85.01 million vehicles were produced worldwide, showcasing a growth rate of 5.99% compared to 80.20 million vehicles in 2021.

- In North America, according to the OICA, automotive production in 2022 accounted for 14,798,146 units, an increase of 9.88% compared to the show in 2021, which was reportedly 13,467,065 units. Additionally, in North America, the sales of electric vehicles in 2022 accounted for 1,108 thousand units, compared to 748 thousand unit sales in 2021.

- In Europe, Germany is among the key manufacturers of vehicles. The automobile manufacturing industry in Germany is a prominent shareholder of the overall automotive production in the European region. The country hosts major car-making brands, including Volkswagen, Mercedes-Benz, Audi, BMW, Porsche, etc.

- According to the Organization Internationale des Constructeurs d'Automobiles (OICA), in 2022, the country produced 3,677,820 vehicles, which increased by 11% compared to 3,308,692 cars in 2021.

- Overall, the increasing usage of high-speed steel for better fuel efficiency and lighter vehicles will boost the growth of the automotive industry.

Asia-Pacific is Expected to Dominate the Market

- During the next few years, the Asia-Pacific region is expected to be the largest market for high-speed steel. In countries like China and India, the growth of industries like automotive, aerospace, and others has caused the demand for high-speed steel to surge.

- The production and sales in the Asia-Pacific region are primarily dominated by countries like China, India, and Japan, which consist of large automotive manufacturers and a vast number of production bases within the countries.

- According to the China Association of Automobile Manufacturers (CAAM), China had the most significant automotive production base globally, with a total vehicle production of 27 million units in 2022, an increase of 3.4% compared to 2021.

- In China, the main focus is to increase production and sales of electric vehicles. The country has set a target to produce 7 million electric vehicles per year by 2025. By 2025, the goal is to have electric vehicles comprise 20% of total new vehicle production in China.

- India has become the second-largest automotive vehicle manufacturer in the region. According to the Society of Indian Automobile Manufacturers (SIAM), in FY 2022-23, the total number of automobile manufacturers in the country grew by about 12.55% compared to FY 2021-2022, recording 25,931,867 units.

- According to the Japan Automobile Manufacturers Association (JAMA), motor vehicle production in the country in 2023 grew by 14.84%, recording 8,998,538 units.

- During the forecast period, these changes are likely to increase the need for high-speed steel.

High Speed Steel Industry Overview

The high-speed steel market is partially consolidated in nature. Some of the major players in the market include Sandvik AB, voestalpine BOHLER Edelstahl GmbH & Co. KG, NIPPON KOSHUHA STEEL CO. LTD, PROTERIAL Ltd, and ArcelorMittal.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Usage in Different Industrial Applications

- 4.1.2 Increasing Demand from Aerospace industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 The Rising Use of Carbide-based Cutting Tools Across Various End-use Sectors

- 4.2.2 Other Restraints

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Tungsten High Speed Steel

- 5.1.2 Molybdenum High Speed Steel

- 5.1.3 Other Types (Cobalt High-Speed Steel, Chromium High-Speed Steel, and Vanadium High-Speed Steel)

- 5.2 Product Type

- 5.2.1 Metal Cutting Tools

- 5.2.2 Cold Working Tools

- 5.2.3 Other Product Types (Milling Tools, Drilling Tools, etc.)

- 5.3 End-user Industry

- 5.3.1 Automotive

- 5.3.2 Aerospace

- 5.3.3 Plastics

- 5.3.4 Other End-user Industries (Mining, Manufacturing, Tool Making, etc)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Nigeria

- 5.4.5.4 Qatar

- 5.4.5.5 Egypt

- 5.4.5.6 United Arab Emirates

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis **/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ArcelorMittal

- 6.4.2 CRS Holdings LLC

- 6.4.3 ERASTEEL

- 6.4.4 Friedr. Lohmann GmbH

- 6.4.5 NACHI-FUJIKOSHI CORP.

- 6.4.6 NIPPON KOSHUHA STEEL CO. LTD

- 6.4.7 PROTERIAL Ltd

- 6.4.8 Sandvik AB

- 6.4.9 thyssenkrupp AG

- 6.4.10 VILLARES METALS SA

- 6.4.11 voestalpine BOHLER Edelstahl GmbH & Co. KG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rapid Technological Improvement

- 7.2 Other Opportunities

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日