|

|

市場調査レポート

商品コード

1641868

木材プラスチック複合材料(WPC)-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Wood Plastic Composites (WPC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 木材プラスチック複合材料(WPC)-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

木材プラスチック複合材料(WPC)市場は、予測期間中に5%を超えるCAGRで推移する見込みです。

2020年と2021年前半にCOVID-19パンデミックが散発的に発生し、政府による禁止措置や規制が課されたため、主要な用途セグメントである世界の建設セグメントが大幅に縮小し、グリーン建築材料市場の成長が制限されました。

住宅用不動産は、主要都市における厳格な封鎖措置の結果、住宅登録が停止され、住宅ローンの決済が滞ったため、最悪の打撃を受けました。一方、商業用建設プロジェクトも、労働力不足と資金繰りの逼迫により打撃を受けました。しかし、規制解除後、このセクターは順調に回復しています。住宅販売の増加、新規プロジェクトの立ち上げ、新しいオフィスや商業スペースの需要増加が、ここ2年間の市場回復を牽引しています。

主要ハイライト

- 中期的には、建築・建設セクターの堅調な成長と、自動車産業におけるリサイクル可能な軽量材料への需要の高まりが、調査対象市場の成長を増大させる主要促進要因となっています。

- その反面、温度感受性や摩耗性などの技術的な問題が、予測期間中の対象産業の成長を抑制すると予想されています。

- よりサステイナブル最終製品を設計するために、さまざまな用途セグメントでリサイクル可能なプラスチックの使用が増加しており、世界市場に有利な成長機会がまもなく生まれると考えられます。

- 北米は木材プラスチック複合材料の最大市場として浮上し、アジア太平洋は予測期間中に最も高いCAGRで推移すると予想されています。北米が支配的な地位を占めているのは、建築・建設産業のデッキ材用途や自動車産業の車体軽量化部品用途で木材プラスチック複合材料の需要が伸びているためです。

木材プラスチック複合材料(WPC)市場動向

建築・建設用途が市場を独占

- 建築・建設は、木材プラスチック複合材料(WPC)の最大の用途セグメントです。耐湿性、耐腐朽性に優れ、美観を長く保つ木材プラスチック複合材料は、デッキ材、モールディング、トリミング、フェンス、造園、屋外用途に広く使用されています。

- デッキ材は、WPCの最も重要な用途のひとつです。建築においてデッキとは、重量を支えることができる平らな、またはプロファイル加工された(滑り止め加工された)表面のことです。デッキは床に似ているが、一般的に屋外に建設され、地面から高くなっていることが多く、通常は建物とつながっています。木材プラスティック複合材料デッキは、庭の造園の一部、住宅の居住エリアの拡大、石を使った設備(パティオなど)の代替、住宅のデッキ、調理、食事、座席のためのスペースなど、さまざまな用途に使用できます。

- WPCは、持続可能性を重視する建設手法への意識の高まりにより、現代の住宅や商業空間の建設手法に不可欠な建築材料として、急速に普及しつつあります。世界の建設セクターは継続的に拡大しています。世界銀行によると、建設支出総額は今後12年間で19兆2,000億米ドルに達すると予測されており、これは研究対象市場をさらに押し上げると期待されています。

- 中国の人口動態は、官民両セクターによる手頃な価格の住宅コロニーへの投資を誘発しました。中国国家統計局によると、中国の住宅着工面積は2022年7月の7,600万平方メートルから2022年8月には8,500万平方メートルに急増しました。さらに、中国は2030年までに建築物に13兆米ドル近くを投じると予想されており、WPCにとって明るい展望が開けています。

- Invest India Reportによると、インドの建設産業は2025年までに1兆4,000億米ドルの市場規模に達する展望で、100都市の変貌と手頃な価格の住宅を目標とするスマートシティ・ミッションに関連する計画に支えられています。

- 欧州はWPCの主要消費国のひとつです。Eurostatによると、2021年12月のドイツのGDPに住宅建設だけで7.2%寄与しており、これは過去10年間で最高のシェアです。ドイツ連邦統計局は、2021年の国内住宅ストック数を4,310万戸と報告し、前年比0.7%(i.28万戸)の増加を示しました。ドイツの建設部門が2021年に達成した建築許可総数は3回連続で増加し、24万8,688戸に達しました。

- 2022年7月、ドイツ政府は、持続可能性を高めるための建物の改修に年間130億~140億ユーロ(140億8,000万~151億7,000万米ドル)を助成する計画を発表しました。

- 上記の要因を考慮すると、建築・建設用途でのWPCの使用と需要は、予測期間中に増加すると予想されます。

北米地域が市場を独占

- 北米は木材プラスチック複合材料(WPCs)市場で最大の市場シェアを占めており、これは主に同地域での住宅と商業プロジェクトの増加によるものです。

- 米国は巨大な建設産業を誇っています。米国国勢調査局の統計によると、米国で実施された住宅建設は、2020年の6,442億5,700万米ドルに対し、2021年には8,029億3,300万米ドルとなりました。さらに、2022年8月までの総建築額は2021年の数字を上回り、9,129億1,300万米ドルに達しました。

- 米国は大規模な住宅改修を進めています。移民人口の増加に伴い、リフォームの必要性がますます高まっています。また、持続可能性と高効率構造に対する意識の高まりが、修復動向に拍車をかけています。政府による複数の融資が利用できることも、国内の住宅リフォームを支えています。

- カナダ(特にトロント)では超高層ビルの建設ブームが起きており、2025年までに30棟以上の高層ビルが完成する見込みです。2022年4月、カナダ政府は、2022年予算の下で発足した40億カナダドル(29億9,000万米ドル)の住宅促進基金からの支援により、今後10年間で住宅建設を倍増させる目標を発表しました。

- さらに、北米諸国における自動車生産と販売の成長は、木材プラスチック複合材料市場に好機を与えています。米国は、中国に次ぐ世界第2位の自動車生産国です。OICAによると、2021年の自動車生産台数は916万7,214台で、882万2,399台と報告された2020年の生産台数と比較して4%増加しています。

- カナダにおける電気自動車需要の高まりは、同国の主要自動車メーカーによる生産活動への投資を後押ししています。Fordは2021年、2~3カ所のバッテリー工場を新設し、2030年までに電気自動車と電気トラックを40万台生産する目標を発表しました。オンタリオ州政府と連邦政府は、オンタリオ州オークヴィルにあるFord Motorの工場での新たな電気自動車生産を支援するため、2億9,500万カナダドル(2億1,926万米ドル)を提供しました。

木材プラスチック複合材料(WPC)産業概要

木材プラスチック複合材料(WPC)市場は、多くの参入企業によって市場シェアが分割されているため、適度にセグメント化されています。市場の主要企業(順不同)には、FKuR、Biologic.、The Azek Company Inc.、Fiberon、CRH CompanyのOldcastle APGなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 建築・建設セグメントからの需要増加

- 自動車産業におけるリサイクル可能な軽量材料の需要増加

- 抑制要因

- 温度感受性、摩耗性などの技術的問題

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模(数量ベース))

- プラスチック材料

- ポリエチレン(PE)

- ポリプロピレン(PP)

- ポリスチレン(PS)

- ポリ塩化ビニル(PVC)

- その他のプラスチック材料

- 用途

- 建築・建材

- デッキ材

- 成形・トリミング

- フェンス

- 造園・アウトドア

- 自動車部品

- 工業製品

- 消費財

- 家具

- その他

- 建築・建材

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- AXION STRUCTURAL INNOVATIONS LLC

- The Azek Company Inc.

- Beologic

- CERTAINTEED

- Fiberon

- FKuR

- Geolam, Inc.

- JELU-WERK J. Ehrler GmbH & Co. KG

- Oldcastle APG a CRH Company

- PolyPlank AB

- Resysta International

- Trex Company Inc.

- UFP Industries, Inc.

第7章 市場機会と今後の動向

- 再生プラスチックの利用拡大

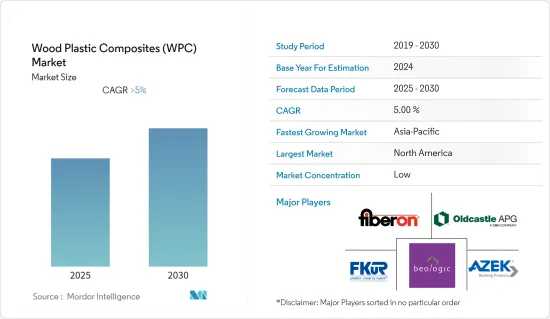

The Wood Plastic Composites Market is expected to register a CAGR of greater than 5% during the forecast period.

The sporadic outbreak of the COVID-19 pandemic in 2020 and the first half of 2021 drastically curtailed the major application sector, i.e., the global construction sector, due to imposed government bans and restrictions, thereby limiting the growth of the green building materials market.

Residential real estate was the worst hit as strict lockdown measures across major cities resulted in the suspension of home registrations and slow home loan disbursements. On the other hand, commercial construction projects were also hit due to a lack of labor and constrained financials. However, the sector has been recovering well since restrictions were lifted. An increase in house sales, new project launches, and increasing demand for new offices and commercial spaces have been leading the market recovery over the last two years.

Key Highlights

- Over the medium term, the robust growth in the building and construction sector and the growing demand for recyclable and lightweight materials in the automotive industry are the major driving factors augmenting the growth of the market studied.

- On the flip side, technical issues such as temperature sensitivity, wearability, etc. are anticipated to restrain the growth of the target industry over the forecast period.

- Nevertheless, the rising use of recyclable plastics in various application sectors to design more sustainable end-products is likely to create lucrative growth opportunities for the global market soon.

- North America emerged as the largest market for wood plastic composites, while Asia-Pacific is expected to witness the highest CAGR during the forecast period. The dominant position enjoyed by North America is attributed to the growing demand for wood-plastic composites in decking applications in the building and construction industry as well as for building lightweight components of vehicle bodies in the automotive industry.

Wood Plastic Composites (WPC) Market Trends

Building & Construction Application to Dominate the Market

- Building and construction is the largest application sector for wood-plastic composites (WPC). Being moisture and rot-resistant while retaining their aesthetic quality for longer, wood plastic composites are widely used in decking, moulding and trimming, fencing, landscaping, and outdoor applications.

- Decking is one of the most important applications of WPCs. In construction, a deck is a flat or profiled (anti-slip) surface that is capable of supporting weight. A deck is similar to a floor but is typically constructed outdoors, often elevated from the ground, and usually connected to a building. Wood plastic composite decking can be used in a number of ways, such as part of garden landscaping, the extension of the living areas of houses, an alternative to stone-based features (such as patios), and in residential decks, as well as spaces for cooking, dining, and seating.

- WPCs are soon gaining pace as a vital building material in modern housing and commercial space construction methods, owing to the growing consciousness toward sustainability-driven construction practices. The global construction sector is continuously expanding. As per the World Bank, the total construction spending value is projected to reach USD 19.2 trillion over the next 12 years, which is expected to give an upward push to the studied market.

- China's demographics have triggered investments in affordable residential colonies by both the public and private sectors. As per the National Bureau of Statistics of China, housing starts in China jumped to 85 million sq m in August 2022 from 76 million sq m in July of 2022. Furthermore, China is expected to spend nearly USD 13 trillion on buildings by 2030, creating a positive outlook for WPCs.

- As per the Invest India Report, India's construction industry is heading to reach USD 1.4 trillion market size by 2025 supported by schemes pertaining to the smart city mission targeting the transformation of 100 cities and affordable housing.

- Europe is one of the major consumers of WPCs. According to Eurostat, residential construction alone contributed 7.2% to Germany's GDP in December 2021, the highest share reached in the past decade. The German Federal Statistical Office reported the stock of dwellings at 43.1 million in 2021 in the country, showing an increase of 0.7% (i.e., 280,000 dwellings) from the previous year. The total number of building permits achieved by Germany's construction sector rose consecutively for the third time in 2021, reaching 248,688 units.

- In July 2022, the German government announced its plans to spend EUR 13-14 billion (USD 14.08-15.17 billion) annually in providing subsidies for the renovation of buildings to make them more sustainable.

- Considering all the above factors, the usage and demand of WPCs for building & construction applications are expected to drive up in the forecast period.

North America Region Dominates the Market

- North America accounts for the largest market share of the wood plastic composites (WPCs) market, driven primarily owing to the growing residential and commercial projects in the region.

- The United States flaunts a colossal construction industry. As per the statistics generated by the US Census Bureau, the value of residential construction put in place in the United States was valued at USD 802,933 million in 2021, compared to USD 644,257 million in 2020. Further, the value of total construction put in place till August 2022 surpassed the 2021 figures reaching USD 912,913 million.

- The United States is going massive on home renovations. With the growing population of migrants in the country, the need for renovation has become increasingly important. Also, the growing awareness toward sustainability and high-efficiency structures has created a spur in the restoration trend. The availability of several loans by the government also supports home remodeling in the country.

- There has been a boom in the construction of skyscrapers in Canada (more specifically in Toronto) with over 30 high-rise buildings expected to be completed by 2025. In April 2022, the Canadian government announced its target to double housing construction over the next decade with assistance from the Housing Accelerator Fund of CAD 4 billion (USD 2.99 billion) launched under Budget 2022, which aims to build 100,000 new housing units in the next five years.

- Furthermore, the growth in automotive production and sales in North American countries provides favorable opportunities to the wood plastic composites market. The United States is the second largest automotive manufacturing country in the globe falling only behind China. According to OICA, the automotive production in 2021 accounted for 9,167,214 units, an increase of 4% in comparison to the production in 2020, which was reported to be 8,822,399 units.

- The rising demand for electric vehicles in Canada has propelled the investment in production activities by key automotive manufacturers in the country. In 2021, Ford announced its aim to produce 400,000 electric cars and trucks by 2030 including two to three new battery plants. Ontario and federal governments offered CAD 295 million (USD 219.26 million) to support new EV production at Ford Motor's plant in Oakville, Ontario.

Wood Plastic Composites (WPC) Industry Overview

The wood plastic composites (WPC) market is moderately fragmented as the market share is divided among many players. Some of the major players in the market (in no particular order) include FKuR, Biologic., The Azek Company Inc., Fiberon, and Oldcastle APG, a CRH Company, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand From the Building & Construction Sector

- 4.1.2 Rising Demand for Recyclable and Lightweight materials in the Automotive Industry

- 4.2 Restraints

- 4.2.1 Technical Issues Like Temperature Sensitivity, Wearability, etc

- 4.2.2 Other Restraints

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Plastic Material

- 5.1.1 Polyethylene (PE)

- 5.1.2 Polypropylene (PP)

- 5.1.3 Polystyrene (PS)

- 5.1.4 Polyvinyl chloride (PVC)

- 5.1.5 Other Plastic Materials

- 5.2 Application

- 5.2.1 Building & Construction Products

- 5.2.1.1 Decking

- 5.2.1.2 Molding & Trimming

- 5.2.1.3 Fencing

- 5.2.1.4 Landscaping & Outdoor

- 5.2.2 Automotive Parts

- 5.2.3 Industrial

- 5.2.4 Consumer Goods

- 5.2.5 Furniture

- 5.2.6 Other Applications

- 5.2.1 Building & Construction Products

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 United Kingdom

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AXION STRUCTURAL INNOVATIONS LLC

- 6.4.2 The Azek Company Inc.

- 6.4.3 Beologic

- 6.4.4 CERTAINTEED

- 6.4.5 Fiberon

- 6.4.6 FKuR

- 6.4.7 Geolam, Inc.

- 6.4.8 JELU-WERK J. Ehrler GmbH & Co. KG

- 6.4.9 Oldcastle APG a CRH Company

- 6.4.10 PolyPlank AB

- 6.4.11 Resysta International

- 6.4.12 Trex Company Inc.

- 6.4.13 UFP Industries, Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Use of Recycled Plastics