|

市場調査レポート

商品コード

1851585

脅威インテリジェンスセキュリティサービス:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Threat Intelligence Security Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 脅威インテリジェンスセキュリティサービス:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月10日

発行: Mordor Intelligence

ページ情報: 英文 121 Pages

納期: 2~3営業日

|

概要

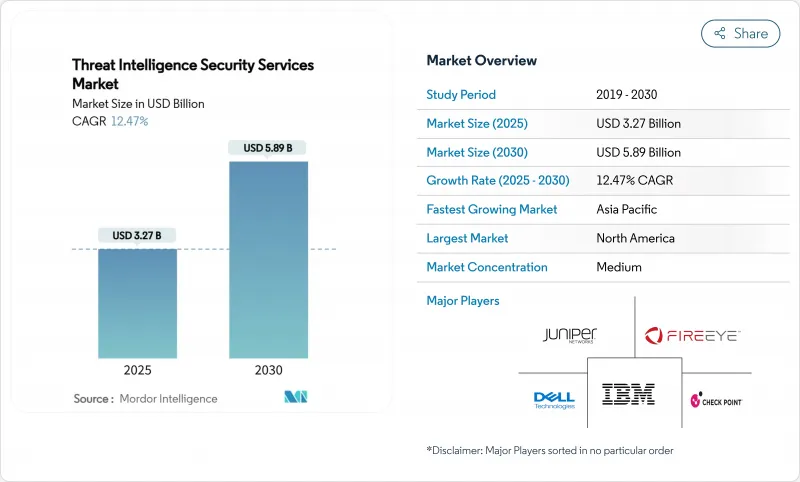

脅威インテリジェンスセキュリティサービス市場規模は、2025年に32億7,000万米ドル、2030年には58億9,000万米ドルに達すると予測され、期間中のCAGRは12.47%で推移します。

この市場拡大は、リアクティブな境界防御から継続的な脅威ハンティング、暴露管理、予測分析への決定的なシフトを反映しています。国家主導のキャンペーンが激化し、クラウドセキュリティインシデントが65%増加し、主要な司法管轄区で違反通知が義務化されたことで、リアルタイムの状況に即した脅威データに対する需要が高まっています。ゼロトラストやXDR(Extended Detection and Response)の展開に代表されるプラットフォームの融合は、セキュリティチームが統合された可視性と自動応答を求める中で、投資をさらに加速させています。同時に、アプリケーション・プログラミング・インターフェースの攻撃対象の急増や、生成的なAIコードアシスタントから生じるインサイダーリスクにより、企業はリスク態勢の見直しを迫られており、脅威インテリジェンスセキュリティサービス市場は活気に満ちています。

世界の脅威インテリジェンスセキュリティサービス市場の動向と洞察

国家が支援するAPTキャンペーンの急速な拡大

Volt TyphoonやSalt Typhoonのような国家グループは、重要インフラに対する活動を強化しており、組織は戦術的なインテリジェンスとインシデント発生前のアトリビューション能力を優先するよう求められています。Cybersecurity and Infrastructure Security Agencyは、2024年に3,368件のランサムウェア事前通知を発行しており、高度な侵入の試みが大量に行われていることを裏付けています。攻撃は今やスパイ活動の域を超え、破壊的な事前配置を含むようになり、継続的な監視と専門的なハンティングが要求されるようになっています。イランの攻撃者はヘルスケアと金融サービスを同時に標的としており、脅威インテリジェンスはセクターを超えた戦略的必須事項となっています。こうした動きにより、マネージド検知、マルウェア解析の強化、およびコンテキストに基づくアトリビューション・サービスへの投資が加速しています。

クラウドワークロードの急増とAPI攻撃の表面化

クラウドへの移行により、攻撃の入口は増加し、企業はマルチクラウド環境で何千ものAPIを運用しています。APIの障害は、2024年に報告されたクラウド侵害の大部分に寄与しており、東西トラフィックにおける可視性のギャップが明らかになっています。従来のネットワーク監視では、刹那的なワークロードに対するコンテキストが欠けているため、依存関係をリアルタイムでマッピングできるクラウドネイティブな脅威インテリジェンスの採用が加速しています。マイクロサービスアーキテクチャは資産目録をさらに複雑にし、自動検出と継続的なリスクスコアリングへの依存度を高めています。その結果、サーバーレス環境とコンテナ環境に合わせたクラウド提供の分析エンジンと暴露管理モジュールの勢いが持続しています。

Tier-1脅威ハンターとアナリストの不足

ディープ・フォレンジックとマルウェア・リバース・エンジニアリングの需要は供給を上回っています。国家レベルの敵の戦術をマスターするには長年のトレーニングが必要だが、セキュリティチームは人員削減と賃金の高騰に直面しています。このギャップは、小規模ベンダーがエキスパートの確保に苦戦し、クライアントがマネージド・ディテクション・アンド・レスポンスにターンキー・カバレッジを求めるようになるにつれて、統合を促しています。プロバイダーは現在、ルーチンのトリアージを自動化し、希少な専門家をより価値の高い業務に振り向けなければならないため、AI支援分析モジュールへの関心が高まっています。

セグメント分析

クラウド展開はすでに脅威インテリジェンスセキュリティサービス市場シェアの58%を占めています。このセグメントは2030年までCAGR 18.20%で拡大すると予測されており、クラウドネイティブな分析エンジンの重要性が高まっています。エラスティックコンピュート分散ストレージにより、プロバイダーは顧客側のハードウェアなしでペタバイト規模のテレメトリを処理できるようになります。これは、脅威インテリジェンス セキュリティ サービスの市場規模が 2030年に58億9,000万米ドルに拡大する中で非常に重要です。オンプレミスのデプロイは、ローカルなデータ処理を必要とするソブリン・クラウドや防衛の文脈で存続しているが、開発ロードマップは現在、スタンドアロンのアプライアンスよりもハイブリッド・コネクタを優先しています。

ハイブリッドの導入は、クラウドを利用して規模を拡大しながらも、コンプライアンス上、特定のデータセットを国内に保持する規制対象企業の間で増加しています。従来のセンサーではコンテナトラフィックのコンテキストが欠けていたため、API中心の攻撃ベクトルはクラウドとの共鳴を際立たせています。パロアルトネットワークスは、AIを中心とした年間経常収益が2億米ドルを超え、前年比4倍の成長を遂げたと報告しており、クラウド提供の機械学習モジュールに対する意欲を実証しています。そのため、クラウドの優位性は確立されているが、ベンダーはさらなる普及を加速させるために、レイテンシー、暗号化、ローカリティの要因に対処する必要があります。

マネージド・ディテクション&レスポンスは、2024年時点で脅威インテリジェンスセキュリティサービス市場シェアの56%を占め、年間18.55%の成長が予測されています。MDRが企業に支持されているのは、テクノロジー、遠隔測定、人間の専門知識を融合し、スタッフの負担なしに平均検知時間を短縮できるからです。MDR契約の急増は、脅威インテリジェンスセキュリティサービス市場がいかに成果ベースのデリバリーに軸足を置いているかを示しています。プロフェッショナルサービスは、成熟度評価、フレームワーク設計、継続的脅威暴露管理の展開に不可欠であることに変わりはないです。

サブスクリプションフィードは、コモディティベースを形成していますが、アクタープロファイリングとリスクスコアリングを備えたコンテキストリッチなパッケージへと進化しています。フォーティネットは、2025年第1四半期に前年同期比30.3%増の4億3,450万米ドルのセキュリティ・オペレーションARRを計上し、統合MDRとオーケストレーションが勢いを増していることを示しています。自動化された封じ込めワークフローにキュレートされたテレメトリーをブレンドするベンダーは、ツールの統合が進む中で、防御可能な差別化を構築しています。

脅威インテリジェンスセキュリティサービス市場は、導入形態(クラウド、オンプレミス)、サービスタイプ(マネージドディテクション&レスポンス、プロフェッショナル/コンサルティング、その他)、組織規模(大企業、中小企業)、エンドユーザー産業(銀行・金融サービス、ヘルスケア、その他)、地域別に区分されます。市場予測は金額(米ドル)で提供されます。

地域分析

北米は、2025年に向けた米国の275億米ドルのサイバーセキュリティ予算に支えられ、世界の収益の38%を占めています。この予算には、情報共有ネットワークを拡大するCISA助成金への30億米ドルが含まれています。ゼロトラストの高い採用率、ベンチャー企業の活発な資金調達、クラウドネイティブなベンダーのエコシステムが、この地域のリーダーシップを維持しています。連邦行政命令14028号は、政府機関に脅威インテリジェンスをセキュリティ業務に統合するよう強制しており、隣接する業界はサプライチェーン保証のモデルを模倣しています。カナダは米国の情報開示基準との調和を図り、メキシコの金融規制当局はインシデント報告をフィンテックにも拡大し、新たな需要ベクトルを加えています。

アジア太平洋地域のCAGRは18.90%で、世界最速の成長が予測されています。中国のサイバーセキュリティ市場は、政府プログラムによって国内のセキュリティ管理が強化され、2029年までに236億6,000万米ドルに達する勢いです。日本の戦略文書では、国内のサイバーセキュリティ売上高を3倍に増やし、国家予算を50%増額するとしており、業界グレードの脅威インテリジェンスに対する意欲が高まっています。インドでは、デジタル化が急速に進んでいます。CERT-IN指令では、特定インシデントのリアルタイム報告が義務付けられ、サービスの利用が促進されています。オーストラリアでは5億8,600万豪ドルのサイバー回復力強化策がマネージド・インテリジェンス需要を下支えし、各地域の電気通信プロバイダーは国境を越えた遠隔測定交換に投資しています。

欧州は、NIS2指令と各地域のデータ保護義務化によって着実な成長を維持しています。ドイツは、産業オートメーションを妨害行為から守るため、2025年に100億ユーロを超えるサイバーセキュリティ支出を見込んでいます。英国は情報機関に6億ポンドの追加予算を計上し、2035年までにGDPの5%を国家安全保障に充てる計画で、ベンダーにとって長期的な見通しが立てやすくなっています。データ主権要件は、国境内でテレメトリを処理できる地域セキュリティ・オペレーション・センターの成長を刺激します。そのため、居住地を考慮したクラウド・ファブリックと多言語アナリスト・サポートを提供するプロバイダーが好まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 国家主導のAPTキャンペーンが急増

- クラウド・ワークロードの急増とAPIアタック・サーフェス

- CISOによるゼロトラストとXDRのプラットフォーム化

- 違反通知義務化法(米国、EU、APAC)

- GEN-AIコードアシスタントによるインサイダーリスク

- 継続的管理バリデーションへのCTEM*の採用

- 市場抑制要因

- ティア1の脅威ハンターとアナリストの不足

- 中小企業セグメントの予算圧縮

- 国境を越えた遠隔測定共有に対するデータ主権上の障壁

- なりすましTIフィードを悪用する逆賊によるアラート疲労発生

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- ライバルの激しさ

第5章 市場規模と成長予測

- 展開モード別

- クラウド

- オンプレミス

- サービスタイプ別

- マネージド・ディテクション&レスポンス

- プロフェッショナル/ コンサルティング

- 購読データフィード

- 組織規模別

- 大企業

- 中小企業

- エンドユーザー業界別

- 銀行および金融サービス

- ヘルスケア

- ITおよび電気通信

- 小売とeコマース

- ライフサイエンス/ 製薬

- 政府および防衛

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 中東

- イスラエル

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- その他アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Google LLC(Mandiant)

- Recorded Future Inc.

- CrowdStrike Holdings Inc.

- Fortinet Inc.

- Cisco Systems Inc.

- International Business Machines Corporation

- Palo Alto Networks Inc.

- Dell Technologies Inc.

- Check Point Software Technologies Ltd.

- Trellix LLC(McAfee Enterprise)

- Broadcom Inc.(Symantec)

- LogRhythm Inc.

- Juniper Networks Inc.

- F-Secure Corporation

- LookingGlass Cyber Solutions Inc.

- Rapid7 Inc.

- Arctic Wolf Networks Inc.

- Trend Micro Incorporated

- Elastic N.V.(Security)

- Kaspersky Lab JSC