|

|

市場調査レポート

商品コード

1641854

エアゾール:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Aerosol - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| エアゾール:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

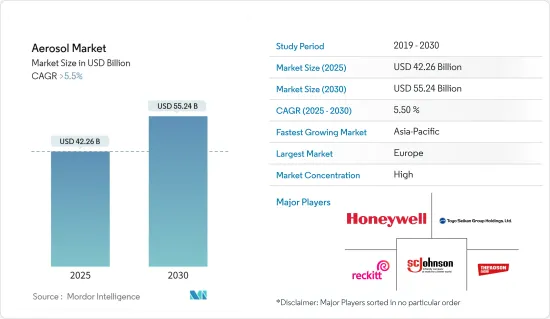

エアゾールの市場規模は2025年に422億6,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは5.5%を超え、2030年には552億4,000万米ドルに達すると予測されます。

2020年、COVID-19パンデミックはサプライチェーンを混乱させ、生産を一時的に停止させたため、エアゾール市場全体の成長を妨げました。しかし、パーソナルケア製品におけるエアゾール消費の増加が、パンデミック後の業界成長を後押ししました。

主なハイライト

- この市場の成長を促す主な要因は、塗料・コーティング業界からのエアゾール缶需要の増加と、衛生とパーソナルケアに関する意識の高まりです。

- エアゾールの使用に関連する厳しい規制は、市場の成長を妨げる可能性が高いです。

- 製品の革新と医療産業への投資の増加は、今後数年間で市場に機会をもたらすと予想されます。

- 欧州が市場を独占し、アジア太平洋が予測期間中に最も高いCAGRで推移すると予想されます。

エアゾール市場の動向

パーソナルケア産業が市場を独占

- エアロゾルは科学的には、空気または他の気体中の小さな固体粒子または液滴のコロイドと表現されます。この定義には、人工製品や霧などの自然現象が含まれます。ヘアスプレー、クリーム、フォーム、ジェル、トイレ用リキッドなどの化粧品は、現在のシナリオではより実用的かつ衛生的に扱われています。

- エアゾール製品は非接触で塗布できるため、使用者を感染症から守り、火傷や裂傷のリスクを減らすことができます。さらに、密封されたパッケージは製品の汚染を防ぐ。その結果、エアゾールの需要はパーソナルケア市場で急増しています。エアゾール缶は、パーソナルケアと化粧品業界全体のパッケージとして最良の選択肢の一つです。エアゾール缶はリサイクル率が高いため、持続可能性の観点からエアゾール缶の需要は高まる傾向にあります。

- ロレアルの報告書によると、世界の美容・パーソナルケアの売上は2025年に7,846億米ドルに増加すると予想されています。

- 日本には、資生堂、花王、コーセー、ポーラ・オルビスといった世界的ブランドを含め、3,000社以上の美容関連企業があります。日本の美容産業は幅広い化粧品に支えられており、中でもスキンケアとメーキャップは需要が高いです。

- 中国国家統計局(NBS)によると、中国の化粧品市場は2023年に約5.1%成長し、4,141億7,000万人民元(~586億1,000万米ドル)に達します。中国の美容市場は、経済の不確実性、パンデミック政策の転換、閉鎖による困難な年を経て急速に回復しています。しかし、売上の落ち込みにもかかわらず、中国の消費者の間で化粧品や美容製品が牽引し続けていることは否定できないです。

- インド・ブランド・エクイティ財団(IBEF)によると、インドの美容・化粧品・グルーミング市場は、中産階級の可処分所得の増加と、健康で美しく生きたいという願望の高まりにより、2025年までに200億米ドルに成長するといいます。

- 北米のパーソナルケア市場は、ここ数年回復力を維持しています。同市場は革新を続け、品質、性能、革新性以上のものを求める消費者の新たな需要に適応しています。消費者は、美容を含め、購入に意味を求めています。

- グルーポンの調査によると、アメリカ人女性は年間3,700米ドル近くを様々な美容製品やサービスに費やしており、このような製品への支出がかなり多いことがわかる。

- 2023年の世界の美容・パーソナルケア市場で最も収益を上げたのは米国で978億1,000万米ドル、次いで中国が671億8,000万米ドル、さらに日本が459億6,000万米ドルでした。ドイツは200億米ドルを超え、欧州諸国の中で第1位となった。

- パーソナル・ケア製品市場は、ロレアル、P&G、ユニリーバ、資生堂など少数の主要企業が独占しています。

- こうしたすべての要因が、予測期間中、パーソナルケア業界のエアゾール市場に貢献すると予想されます。

アジア太平洋が急成長地域に

- アジア太平洋は、パーソナルケア製品需要の増加、医療産業への投資の増加、同地域での自動車生産の増加により、エアゾール需要の力強い成長が見込まれます。

- アジア太平洋地域では、自動車産業からの旺盛な需要や建設・建築プロジェクトの増加により、中国が予測期間中にエアゾール需要の顕著な伸びを目の当たりにすると予想され、塗料・コーティング剤の需要をさらに増加させる可能性が高いです。

- 香港貿易発展局によると、中国は世界第2位の化粧品消費市場です。国家統計局のデータによると、2022年、中国の化粧品売上は前年比14%増だった。

- ロレアルの報告書によると、2022年の同国の美容・パーソナルケア市場は553億米ドルに達します。同国の美容市場は、経済の不確実性、多数の閉鎖、その他の流行政策の変更により減速に直面した後、2022年に力強い回復を示しました。

- アメリカン・コーティング協会によると、中国はアジア太平洋のコーティング剤全体の約60%を占めています。この間の急速な都市化が、国内の塗料・コーティング産業に拍車をかけています。

- アジア太平洋地域の生産と販売は、主に中国、インド、日本といった国々が独占しており、これらの国々は大手自動車メーカーと膨大な数の生産拠点で構成されています。

- 中国汽車工業協会(CAAM)によると、中国は世界で最も重要な自動車生産拠点であり、2023年の自動車総生産台数は3,016万966台と、昨年の2,702万615台に比べて11.6%増加します。国際貿易局(ITA)によれば、国内の自動車生産台数は2025年までに3,500万台に達すると予想されています。

- 中国では、電気自動車の生産と販売を拡大することに主眼が置かれています。そのために、2025年までに年間700万台の電気自動車を生産するという目標を掲げています。2025年までに、中国の新車生産台数の20%を電気自動車にすることが目標です。

- 国家投資促進・円滑化庁(インベスト・インディア)によると、インドは美容・パーソナルケア(BPC)市場で8位につけています。意識の高まり、アクセスの容易さ、ライフスタイルの変化といった要因が市場を牽引しています。2023年には、個人衛生市場は150億米ドルに達すると予想されています。

- インドはこの地域で第2位の自動車メーカーとなっています。Organisation Internationale des Constructeurs d'Automobiles(OICA)によると、2023年、インドの自動車製造業は2022年比で約7%の成長を記録し、約585万1,507台の自動車を生産しました。

- 日本化粧品工業連合会は、東京都化粧品工業連合会、日本化粧品工業連合会、西日本化粧品工業連合会、中部化粧品工業連合会を統合し、2023年4月に設立されました。

- 日本の化粧品業界の主要企業の一つである花王株式会社が発表した報告書によると、日本の化粧品市場全体は2022年に3%以上の成長を遂げ、市場の回復に伴い今後数年間はさらなる成長が見込まれています。

- 日本には、資生堂、花王、コーセー、ポーラ・オルビスなどの世界的ブランドを含め、3,000社を超えるトイレタリー、美容、パーソナルケア企業があります。さらに、資生堂、マンダム、ロレアル、プロクター・アンド・ギャンブル、ユニリーバがその主要企業です。しかし、人口動態の縮小は市場に大きな影響を与えています。

- 日本自動車工業会(JAMA)によると、2023年の自動車生産台数は14.84%増加し、899万8,538台となった。

- したがって、自動車、塗料・コーティング、家具産業におけるこのような成長は、今後数年間でエアゾール製品の需要を増加させ、エアゾール市場の需要をさらに促進すると思われます。

エアゾール産業の概要

エアゾール市場は部分的に統合されています。市場の主要企業(順不同)には、Guangdong Theaoson Technology、Johnson &Son Inc.、Honeywell International Inc.、Toyo Seikan Group Holdings Ltd.、Reckitt Benckiser Group PLCなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 塗料業界からのエアゾール缶需要の増加

- 衛生とパーソナルケアに関する意識の高まり

- その他の促進要因

- 抑制要因

- エアゾール使用に関する厳しい規制

- その他の阻害要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- 推進剤タイプ別

- ジメチルエーテル(DME)

- ハイドロフルオロカーボン(HFC)

- ハイドロフルオロオレフィン(HFO)

- その他のタイプ(亜酸化窒素、二酸化炭素など)

- 缶タイプ別

- スチール

- アルミニウム

- プラスチック

- その他の缶タイプ(ガラス、錫)

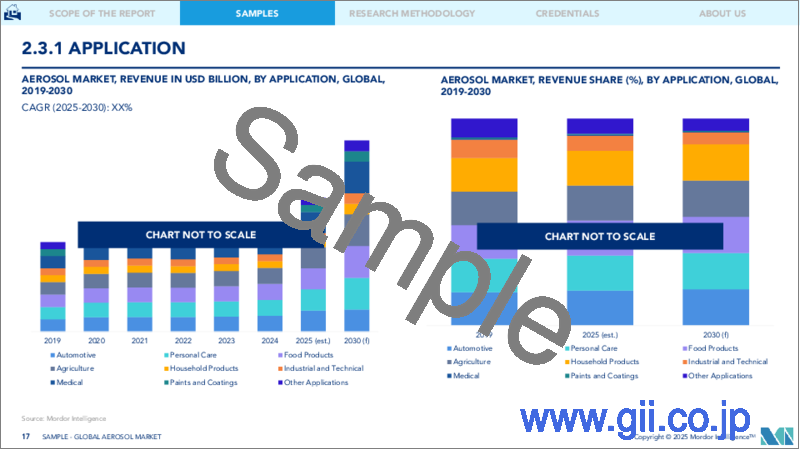

- 用途別

- 自動車

- パーソナルケア

- 食品

- 農業

- 家庭用品

- 工業・技術

- メディカル

- 塗料・コーティング

- その他の用途(洗浄剤、スプレーなど)

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- ナイジェリア

- カタール

- エジプト

- アラブ首長国連邦

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- ACT Aerosol Chemie Technik GmbH

- Beiersdorf

- Guangdong Theaoson Technology Co. Ltd

- Honeywell International Inc.

- Hydrokem Aerosols Limited

- Reckitt Benckiser Group PLC

- S.C. Johnson & Son Inc.

- Shenzhen Sunrise New Energy Co. Ltd

- Suhan Aerosol

- Toyo Seikan Group Holdings Ltd

第7章 市場機会と今後の動向

- 医療業界における製品革新と投資の増加

- その他の機会

The Aerosol Market size is estimated at USD 42.26 billion in 2025, and is expected to reach USD 55.24 billion by 2030, at a CAGR of greater than 5.5% during the forecast period (2025-2030).

In 2020, the COVID-19 pandemic hindered the growth of the aerosol market as a whole because it messed up the supply chain and put a temporary stop to production. However, the rising consumption of aerosols in personal care products has propelled industry growth post-pandemic.

Key Highlights

- The major factors driving the growth of the market studied are the increasing demand for aerosol cans from the paint and coatings industry and rising awareness related to hygiene and personal care.

- Stringent regulations related to the use of aerosols are likely to hinder the growth of the market.

- Product innovation and increasing investments in the medical industry are expected to create opportunities for the market in the coming years.

- Europe is expected to dominate the market, while Asia-Pacific is likely to witness the highest CAGR during the forecast period.

Aerosol Market Trends

Personal Care Industry to Dominate the Market

- Aerosols are described scientifically as colloids of small, solid particles or liquid droplets in air or another gas. This definition encompasses man-made products and natural phenomena, such as fog. Cosmetic products, such as hair sprays, creams, foams and gels, toilette liquids, and others, are handled more practically and hygienically in the current scenario.

- Aerosol products can be applied without contact, protecting users from infections and reducing the risk of burns or lacerations. Furthermore, the sealed package prevents product contamination. As a result, the demand for aerosol has surged in the personal care market. Aerosol cans are one of the best choices for packaging across the personal care and cosmetics industry. Since aerosol cans hold high recycling rates, the demand for aerosol cans tends to rise in terms of sustainability.

- According to the reports by L'Oreal, the revenue of global beauty and personal care is anticipated to ascend to USD 784.6 billion in 2025.

- Japan is home to more than 3,000 beauty care companies, including global brands of Shiseido, Kao, Kose, and Pola Orbis. The Japanese beauty industry is carried by a wide range of cosmetic products, with skincare and makeup being in high demand.

- According to China's National Bureau of Statistics (NBS), the cosmetics market in China grew by around 5.1% in 2023, reaching CNY 414.17 billion (~USD 58.61 billion). The Chinese beauty market is rapidly recovering after a challenging year due to economic uncertainty, pandemic policy shifts, and lockdowns. However, despite the drop in sales, there is no denying that cosmetic and beauty products continue to gain traction among Chinese consumers.

- According to the Indian Brand Equity Foundation (IBEF), the Indian beauty, cosmetic, and and grooming market will grow to USD 20 billion by 2025, driven by the increasing disposable income of the middle class and the growing desire to live well and look good.

- The North American personal care market has remained resilient over the past years. The market continues to innovate and adapt to the new demands of consumers, who want more than just quality, performance, and innovation; they want meaning in their purchases, including beauty.

- According to a study by Groupon, American women spend nearly USD 3,700 on various beauty products and services yearly, signifying the considerably high expenditure on such products.

- The United States generated the most revenue from the global beauty and personal care market in 2023, with USD 97.81 billion, followed by China, generating a revenue of USD 67.18 billion, further followed by Japan, with a revenue of USD 45.96 billion. Germany ranked first among European nations, with over USD 20 billion.

- The market for personal care products is dominated by a few key players like L'Oreal, P&G, Unilever, and Shiseido.

- All such factors are expected to contribute to the aerosol market in the personal care industry during the forecast period.

Asia-Pacific to be the Fastest-growing Region

- Asia-Pacific is expected to witness strong growth in the demand for aerosol, driven by increasing demand for personal care products, increasing investments in the medical industry, and increasing automotive production in the region.

- In Asia-Pacific, China is expected to witness noticeable growth in the demand for aerosol during the forecast period, owing to the robust demand from the automotive industry and increasing construction and architectural projects, which is further likely to increase the demand for paints and coatings.

- According to the Hong Kong Trade Development Council, China is the world's second-largest consumer market for cosmetic products. In 2022, cosmetics sales in China increased by 14% compared to the year before, according to data from the National Bureau Of Statistics.

- According to a report by L'Oreal, the country generated USD 55.3 billion in the beauty and personal care market in 2022. The country's beauty market witnessed a strong rebound in 2022 after facing a slowdown due to economic uncertainties, numerous lockdowns, and other pandemic policy changes.

- China consists of around 60% of the entire coatings volume of Asia-Pacific, according to the American Coatings Association. Rapid urbanization during this period has spurred the domestic paints and coating industry.

- The production and sales in Asia-Pacific are primarily dominated by countries like China, India, and Japan, which consist of large automotive manufacturers and a vast number of production bases within the countries.

- According to the China Association of Automobile Manufacturers (CAAM), China has the most significant automotive production base in the world, accounting for a total vehicle production of 30,160,966 units in 2023, registering an increase of 11.6% compared to 27,020,615 units produced last year. As per the International Trade Administration (ITA), domestic automotive production is expected to reach 35 million units by 2025.

- In China, the main focus is to increase production and sales of electric vehicles. To this end, the country has set a target to produce 7 million electric vehicles per year by 2025. By 2025, the goal is to bring electric vehicles into 20 % of total new vehicle production in China.

- According to the National Investment Promotion and Facilitation Agency (Invest India), India stands eighth in the beauty and personal care (BPC) market. Factors such as growing awareness, easier access, and changing lifestyles are driving the market. In 2023, the personal hygiene market was expected to reach USD 15 billion.

- India has become the second-largest automotive vehicle manufacturer in the region. According to Organisation Internationale des Constructeurs d'Automobiles (OICA), in 2023, Indian automotive manufacturing industry observed a growth of about 7% compared to 2022 and produced about 58,51,507 vehicles.

- The Japan Cosmetic Industry Association (JCIA) was established in April 2023 by integrating the Tokyo Cosmetic Industry Association, the Japan Cosmetic Industry Federation, the West Japan Cosmetic Industry Association, and the Chubu Cosmetic Industry Association.

- According to a report published by Kao Corporation, one of the key players in the Japanese cosmetic industry, the overall market in Japan grew by over 3% in 2022, with further growth anticipated in the next several years as the market recovers.

- Japan has over 3,000 toiletries, beauty, and personal care companies, including global brands like Shiseido, Kao, Kose, and Pola Orbis. Furthermore, its major players are Shiseido Company, Mandom Corporation, Loreal, Procter and Gamble, and Unilever. However, shrinking demographics is highly affecting the market.

- According to Japan Automobile Manufacturers Association (JAMA), the motor vehicles production of the country in 2023 grew by 14.84% and accounted for 8,998,538 units.

- Therefore, such growth in the automotive, paints and coatings, and furniture industries is likely to increase the demand for aerosol products in the coming years, further driving the demand in the aerosol market.

Aerosol Industry Overview

The aerosol market is partially consolidated in nature. Some of the major players in the market (not in any particular order) include Guangdong Theaoson Technology Co. Ltd, Johnson & Son Inc., Honeywell International Inc., Toyo Seikan Group Holdings Ltd, and Reckitt Benckiser Group PLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Aerosol Cans from Paints and Coatings Industry

- 4.1.2 Increasing Awareness Related to Hygiene and Personal Care

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Regulations Related to Use of Aerosol

- 4.2.2 Other Restraints

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Propellant Type

- 5.1.1 Dimethyl Ether (DME)

- 5.1.2 Hyrdofluorocarbons (HFC)

- 5.1.3 Hydrofluoro Olefins (HFO)

- 5.1.4 Other Types (Nitrous Oxide, Carbon Dioxide, etc.)

- 5.2 By Can Type

- 5.2.1 Steel

- 5.2.2 Aluminum

- 5.2.3 Plastic

- 5.2.4 Other Can Types (Glass and Tin)

- 5.3 By Application

- 5.3.1 Automotive

- 5.3.2 Personal Care

- 5.3.3 Food Products

- 5.3.4 Agriculture

- 5.3.5 Household Products

- 5.3.6 Industrial and Technical

- 5.3.7 Medical

- 5.3.8 Paints and Coatings

- 5.3.9 Other Applications (Cleaning Products, Sprays, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Nigeria

- 5.4.5.4 Qatar

- 5.4.5.5 Egypt

- 5.4.5.6 United Arab Emirates

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ACT Aerosol Chemie Technik GmbH

- 6.4.2 Beiersdorf

- 6.4.3 Guangdong Theaoson Technology Co. Ltd

- 6.4.4 Honeywell International Inc.

- 6.4.5 Hydrokem Aerosols Limited

- 6.4.6 Reckitt Benckiser Group PLC

- 6.4.7 S.C. Johnson & Son Inc.

- 6.4.8 Shenzhen Sunrise New Energy Co. Ltd

- 6.4.9 Suhan Aerosol

- 6.4.10 Toyo Seikan Group Holdings Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Product Innovation and Increasing Investments in Medical Industry

- 7.2 Other Opportunities