殺生物剤:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

Biocides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1850263

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

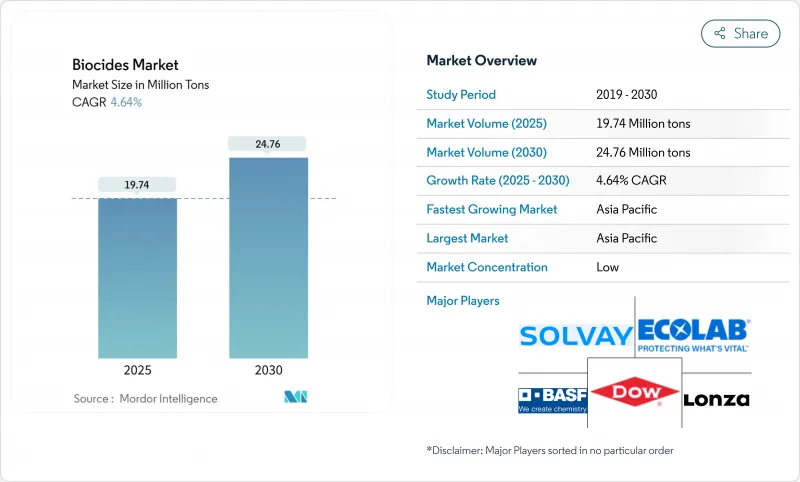

殺生物剤の市場規模は2025年に1,974万トンとなり、2030年には2,476万トンに達すると予測され、2025-2030年のCAGRは4.64%です。

水処理、食品安全、ヘルスケア、建築における抗菌ソリューションへの旺盛な需要は、エンドユーザーが環境規制の強化に直面しているにもかかわらず、引き続き数量成長を支えています。工業用水の再利用プロジェクトが着実に増加しているため、用途の裾野が広がっており、その結果、消費量が増加していることから、投与量の最適化技術がそのまま対応可能量の拡大につながることが示唆されます。同時に、持続可能性の要件が、酸化剤やバイオベース製剤へのポートフォリオの多様化をメーカーに促しており、これは業界全体の拡大が、技術の質的アップグレードを伴っていることを示唆しています。生産量の増加と環境に優しい化学物質の共存は、コンプライアンスへの対応と同時に、スケール効率が向上していることを示唆しています。主要サプライヤーの投資計画から得られる証拠は、業界が投機的な成長を追い求めるのではなく、予測される需要曲線に合わせて生産能力を増強していることを示しています。

世界の殺生物剤市場動向と洞察

世界的な水処理需要の増加

水不足と再利用目標の高まりにより、自治体や産業事業者は、より低い有効成分負荷で残留効力を維持する殺生物剤製剤の導入を進めています。公益事業者は、センサーとクラウド分析を統合した投与量制御プラットフォームを採用しており、殺生物剤市場をパフォーマンスベースの調達モデルへと誘導しています。過酢酸と安定化臭素は、米国の規制当局によって最近地下水浄化のために承認されたもので、迅速な分解と組み合わされた酸化力がコンプライアンスのスイートスポットと考えられていることを示しています。重要な推論は、データ主導の投与ガイダンスを製品に組み込むサプライヤーは、コモディティ化の圧力から市場での地位を守れる可能性が高いということです。

飲食品業界からの需要の高まり

食品加工業者は、検出可能な残留物を残すことなく交差汚染を最小限に抑えるために衛生管理プロトコルを見直しており、その結果、表面だけでなく周囲の空気中でも作用するヒドロキシルラジカル・システムに対する需要が高まっています。包装工場では現在、腐敗生物を抑制して保存期間を延長するため、殺生物剤を組み込んだナノ複合体の試用が行われています。このような空気、表面、パッケージの殺菌の収束は、統合衛生ソリューションが複数の予算ラインにわたるクロスセルの機会を解き放つことができることを示唆しています。このパターンは、従来の湿式化学殺菌剤から連続作用技術へと徐々に置き換わっていることを示しています。

殺生物剤に関連する環境問題と健康被害

規制当局は、難分解性や発がん性が懸念される活性物質を段階的に廃止しています。欧州委員会による酸化エチレンの廃止は、製剤メーカーが直面している規制の予測不可能性を物語っています。洗浄時に船体10,000m2あたり最大4.3kgのマイクロプラスチック塗料粒子が放出されるという調査は、特定の塗料が生態系に与える影響を強調しています。このような調査結果は、分解可能な活性剤への需要を高め、ひいてはバイオベース原料の研究開発を促しています。新たなシグナルとして、保険会社や港湾当局が従来のコーティング剤に依存する事業者に罰則を課し始める可能性があり、間接的に環境に最適化された殺生物剤の採用を後押ししています。

セグメント分析

2024年の殺生物剤市場シェアはハロゲン化合物が28%を占め、2030年までCAGR 5.8%で拡大すると予測されています。臭素ベースのソリューションは、塩素消毒が困難な場合でも生物静電効果が持続するため、高温冷却システムの第一選択肢であり続け、このセグメントの成長の背景にある運用上の根拠を明らかにしています。臭素の放出量を測定するカプセル化方式は、現在ではサービス間隔を延長し、全体的な化学薬品排出量を削減し、強化される廃水規則に合致しています。つまり、積極的な切り替えではなく、段階的なプロセス調整によって、性能とコンプライアンスを両立させることができるということです。

生分解性プロファイルを向上させることで、より環境に優しい製品であることをサプライヤーが求めるようになり、ハロゲン内での競合が激化しています。アルベマールの抽出最適化は、臭素単位あたりのエネルギー投入量を削減し、上流の持続可能性の向上が下流の需要拡大に連鎖することを示唆しています。並行して行われた研究開発では、リアルタイムのモニタリングが可能な二酸化塩素発生装置が研究されており、化学と並んでデジタル機能が差別化要因になりつつあることを示しています。これらのイニシアチブを総合すると、ハロゲン・サプライヤーは製品の売り手からソリューション・パートナーへと軸足を移しつつあることがうかがえます。

地域分析

アジア太平洋地域は2024年の殺生物剤世界市場シェアの35%を占め、2030年までのCAGRは5.15%と最も速いです。工業団地における水の再利用率を高めようとする中国の動きは、高性能の酸化性殺生物剤の採用を加速させています。日本のサプライヤーは、特殊なノウハウを活用して高純度活性剤を近隣諸国に輸出しており、これはアジア域内のサプライ・チェーンが深化していることを示しています。一方、東南アジア諸国は、臭素ベースのモジュール式システムを採用することで、従来の塩素処理から脱却しつつあります。この地域の需要パターンを総合すると、生産量の増加には迅速な技術同化が伴うことが示唆されます。

北米は、米国環境保護庁のTSCAとFIFRAの継続的な見直しにより、製剤メーカーに堅牢な毒性データパッケージの維持を義務付けているため、依然として技術の先駆者であり続けています。このような規制の厳しさが、難分解性の低い活性剤の技術革新に拍車をかけ、それが他の管轄区域にも輸出されています。カナダは林業の伝統があるため、木材保存の分野でもかなりの規模があり、州当局が浸出液の閾値を低く規定しているため、サプライヤーは銅とアゾールのハイブリッドに向かおうとしています。この地域の市場は、石油化学コンビナートの大規模な冷却塔の改修からも恩恵を受けており、これは需要が新築だけでなく、メンテナンス・サイクルにも結びついていることを示唆しています。

欧州は、世界で最も厳しい殺生物剤製品認可の枠組みで際立っており、申請者が新たな環境リスクデータの提出を怠った場合、活性物質の認可が失効する可能性があります。最近の酸化エチレンの撤退は、このような動きを浮き彫りにし、より安全な代替物質を求めるビジネス・ケースを強めています。消費量はドイツと英国が圧倒的に多いが、北欧諸国が生分解性の解決策を開拓し、それが後に南へ拡大することも多いです。サーキュラー・エコノミー(循環型経済)法は、使用済み製品のフットプリントを最小限に抑えた活性物質を優遇しているため、ゆりかごから墓場までの評価に投資するサプライヤーは、将来の入札で有利な立場に立つことができます。その結果、欧州は実証の場として機能することになります。欧州のルールの下で成功した製品は、通常、他の国でもわずかな改良を加えるだけで受け入れられる可能性があるのです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 世界的な水処理の需要の高まり

- 食品・飲料業界からの需要の高まり

- 健康と衛生への意識の高まり

- 塗料・コーティング業界における需要の高まり

- より安全な代替品に対する規制支援

- 市場抑制要因

- 殺生物剤に関連する環境問題と健康被害

- 原材料価格の変動

- 高い研究開発費

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- タイプ別

- ハロゲン化合物

- 金属化合物

- 有機硫黄

- 有機酸

- フェノール類

- その他のタイプ(第四級アンモニウム化合物)

- 用途別

- 水処理

- 医薬品およびパーソナルケア

- 木材保存

- 食品・飲料

- 塗料とコーティング

- その他の用途(石油・ガス、農業、消毒剤および衛生管理)

- 作用機序別

- 酸化殺生物剤

- 非酸化性殺生物剤

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- タイ

- マレーシア

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- ロシア

- 北欧諸国

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- ナイジェリア

- エジプト

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Albemarle Corporation

- Arxada

- Baker Hughes Company

- BASF SE

- Dow

- Ecolab

- IRO Group Inc.

- Italmatch AWS

- Kemipex

- Kemira

- LANXESS

- Lonza

- Merck KGaA

- Nouryon

- Solvay

- Stepan Company

- The Lubrizol Corporation

- Thor Group Ltd.

- Valtris Specialty Chemicals

- Veolia

- Vink Chemicals GmbH & Co. KG

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日