ポリシロキサン:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

Polysiloxane - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1641850

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

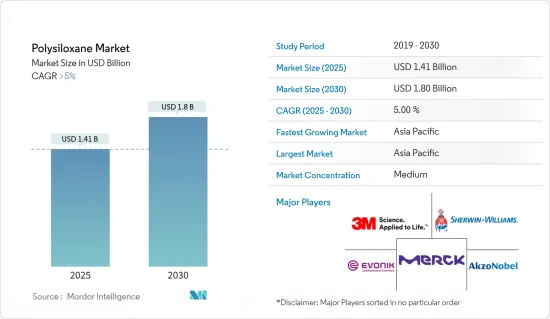

ポリシロキサンの市場規模は2025年に14億1,000万米ドルと推定され、予測期間中(2025-2030年)のCAGRは5%を超え、2030年には18億米ドルに達すると予測されます。

主なハイライト

- COVID-19パンデミックによって市場はマイナスの影響を受け、生産と移動が減速し、輸送、インフラストラクチャーなどの業界が封じ込め対策と経済的混乱によって生産の延期を余儀なくされました。現在、市場はパンデミックから回復しています。市場は2022年にはパンデミック以前の水準に達し、今後も安定した成長が見込まれます。

- 調査対象となった市場の成長を牽引する主な要因は、保護・工業用コーティングの用途の拡大とヘルスケア産業における膨大な用途です。技術的な欠点や、他の材料や添加剤との相性の悪さが、市場成長の妨げになる可能性が高いです。

- 新たな用途開発のためのポリシロキサン技術の継続的な研究開発は、今後数年間で市場にチャンスをもたらすと思われます。アジア太平洋地域が市場を独占し、予測期間中に最も高いCAGRで推移すると予想されます。

ポリシロキサン市場の動向

エレクトロニクス分野からの需要の増加

- ポリシロキサンは、その優れた溶解性、フィルム形成能力、さまざまな基材への適度な接着性、優れた放熱性、無毒性、低誘電率、優れた熱・化学抵抗性により、有機発光ダイオード(OLED)、太陽電池、電気メモリ、液晶材料などの電子製品の製造に広く使用されています。

- 電気・電子産業における使用量の増加と応用分野の広さは、世界中で市場の成長を促進すると期待されています。

- 例えば、日本電子情報技術産業協会(JEITA)によると、世界の電子・IT産業の生産額は2021年の3兆4,159億米ドルに対し、2022年には3兆4,368億米ドルと推定され、前年比1%の成長率を記録しました。さらに、2023年末には前年比3%の成長率で3兆5,266億米ドルに達すると予想されています。

- さらに、電子情報技術省によると、インド全土の家電(テレビ、アクセサリー、オーディオ)の生産額は、2022年度には7,450億インドルピー(94億6,000万米ドル)を超えています。このように市場の成長を支えています。

- このような積極的な成長により、予測期間を通じてエレクトロニクス分野でのポリシロキサン消費が増加すると予想されます。

市場を独占するアジア太平洋地域

- アジア太平洋地域は、主に中国、インド、日本、韓国などの国々によって牽引され、市場調査において最大のシェアを占めました。医療機器、接着剤・シーラント、エラストマー、エレクトロニクスなどの生産基盤が大きいためです。

- 2023年6月、ヘンケルは中国に新しい接着剤製造施設を追加すると発表しました。中国山東省の煙台化学工業園区にヘンケル・アドヒーシブ・テクノロジーズの新しい製造施設を建設。新工場「Kunpeng」の建設費は約8億7,000万人民元(1億1,900万米ドル)。この新工場は、ヘンケルの中国における高衝撃接着剤製品の生産能力を増強し、国内外市場からの需要増に対応するため、サプライチェーンをさらに最適化するもので、ひいては市場成長にもプラスになると期待されます。

- さらに、2023年5月、接着剤メーカーのジョワットは、中国に独自の接着剤センターを設立し、アジア太平洋におけるプレゼンスを拡大すると発表しました。アジアにおける新しい接着剤センターの表面積は11,000平方メートルを超え、2023年末までに完成する予定です。

- さらに、中国は世界最大のエレクトロニクス生産拠点でもあります。スマートフォン、有機ELテレビ、タブレット端末、電線、ケーブルなどの電子製品は、エレクトロニクス分野で最高の成長を記録しました。同国はエレクトロニクスの国内需要に応えるだけでなく、エレクトロニクス生産物を他国に輸出しています。中国における中産階級の可処分所得の増加と、中国からエレクトロニクス製品を輸入している国々におけるエレクトロニクス製品に対する需要の高まりにより、エレクトロニクス生産は予測期間中にさらに成長すると予測されます。

- 中国メーカーは、エレクトロニクスの国際市場に進出するため、海外生産拠点を設立しています。例えば、TCLは海外に工場を設立し、ベトナム、マレーシア、メキシコ、インドでテレビ、モジュール、太陽電池を生産することで、国際市場での存在感を高めています。さらに、ブラジルの現地企業とパートナーシップを結び、生産施設、サプライチェーン、研究開発インフラを共同で開発しています。

- 以上のような要因により、予測期間中、同地域におけるポリシロキサンの需要が高まると予想されます。

ポリシロキサン業界の概要

ポリシロキサン市場は部分的に統合されています。調査対象市場の主要企業(順不同)には、3M、Akzo Nobel N.V.、Evonik Industries AG、Merck KGaA、The Sherwin-Williams Company、Wacker Chemie AGなどが含まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 保護・工業用コーティングにおける用途の拡大

- ヘルスケア産業における幅広い用途

- オプトエレクトロニクス分野での用途拡大

- 抑制要因

- 技術的な欠点と、他の材料や添加剤との非相溶性

- その他の阻害要因

- バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- 用途別

- 医療

- 塗料・コーティング

- 無機ポリシロキサン

- エポキシ-ポリシロキサンハイブリッド

- アクリル-ポリシロキサンハイブリッド

- 接着剤とシーラント

- エラストマー

- 有機電子材料

- ファブリック

- その他の用途(パーソナルケア、化粧品など)

- エンドユーザー産業別

- ヘルスケア

- 石油・ガス

- 電力

- インフラ

- 運輸

- エレクトロニクス

- 飲食品

- テキスタイル

- その他のエンドユーザー産業(メンブレン、消泡剤など)

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- 3M

- Akzo Nobel N.V.

- Asian Paints

- Biro Technology Inc.

- Dampney Company

- Evonik Industries AG

- Gelest Inc.

- Huntsman Corporation LLC

- Merck KGaA

- Restek Corporation

- The Sherwin-Williams Company

- Wacker Chemie AG

第7章 市場機会と今後の動向

- 新規用途開発のためのポリシロキサン技術の継続的研究開発

- その他の機会

目次

Product Code: 59591

The Polysiloxane Market size is estimated at USD 1.41 billion in 2025, and is expected to reach USD 1.80 billion by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

Key Highlights

- The market was negatively impacted by the COVID-19 pandemic as there was a slowdown in production and mobility wherein industries, such as transportation, infrastructure, etc., were forced to delay their production due to containment measures and economic disruptions. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022 and is expected to grow steadily in the future.

- The major factors driving the growth of the market studied are the growing usage of protective and industrial coatings and vast applications in the healthcare industry. Technological drawbacks and incompatibility with a few other materials or additives are likely to hinder the growth of the market.

- Continuous R&D of polysiloxane technologies for the development of newer applications is likely to create opportunities for the market in the coming years. Asia-Pacific region is expected to dominate the market and is also likely to witness the highest CAGR during the forecast period.

Polysiloxane Market Trends

Increasing Demand from Electronics Sector

- Polysiloxanes, owing to their good solubility, film-forming ability, fair adhesion to various substrates, excellent heat radiation, non-toxic characteristics, low dielectric constants, and superior thermal & chemical resistivity, are widely used to manufacture electronic items such as organic light-emitting diodes (OLEDs), solar cells, electrical memories, and liquid crystalline materials, among other products.

- The increasing usage and wide areas of application in the electrical and electronics industry are expected to drive market growth across the globe.

- For instance, according to the Japan Electronics and Information Technology Industries Association (JEITA), the production by the global electronics and IT industry was estimated at USD 3,436.8 billion in 2022, registering a growth rate of 1% year on year, compared to USD 3,415.9 billion in 2021. Moreover, the industry was expected to reach USD 3,526.6 billion, with a growth rate of 3% year on year, at the end of 2023.

- Moreover, according to the Ministry of Electronics and Information Technology, the production value of consumer electronics (TV, accessories, and audio) across India was above INR 745 billion (USD 9.46 billion) in fiscal year 2022. Thus supporting the growth of the market.

- Such positive growth is expected to increase the consumption of polysiloxane in the electronics sector through the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific accounted for the largest share of the market studied, mainly driven by countries such as China, India, Japan, and South Korea. Owing to its large production base of medical devices, adhesives and sealants, elastomers, electronics, etc.

- In June 2023, Henkel announced the addition of a New adhesive Manufacturing Facility in China. The new manufacturing facility of Henkel Adhesive Technologies in the Yantai chemical industry park in Shandong province, China. The new plant, 'Kunpeng,' will cost approximately CNY 870 million (USD 119 million). The new plant will increase Henkel's production capacity of high-impact adhesive products in China and further optimize the supply chain to meet the increasing demand from domestic and foreign markets, which in turn is expected to benefit the market growth.

- Moreover, in May 2023, Jowat, the adhesive manufacturer, announced to expand its presence in Asia-Pacific with the establishment of its own adhesive center in China. The new adhesive center in Asia will have a surface area of more than 11,000 sq meters and is planned to be finished by the end of 2023.

- Furthermore, China has the world's largest electronics production base. Electronic products, such as smartphones, OLED TVs, tablets, wires, and cables, recorded the highest growth in the electronics segment. The country not only serves the domestic demand for electronics but also exports electronic output to other countries. Owing to the increase in the disposable incomes of the middle-class population in China and the rising demand for electronic products in the countries that import electronic products from China, the production of electronics is estimated to grow further during the forecast period.

- The Chinese manufacturers are setting up overseas production bases in order to expand in the electronics international markets. For instance, TCL has broadened its presence in international markets by establishing factories abroad, producing televisions, modules, and photovoltaic cells in Vietnam, Malaysia, Mexico, and India. In addition, it has formed partnerships with local companies in Brazil to collaboratively develop production facilities, supply chains, and an R&D infrastructure.

- The factors above are expected to boost the demand for polysiloxane in the region during the forecast period.

Polysiloxane Industry Overview

The polysiloxane market is partially consolidated in nature. The major players in the studied market (not in any particular order) include 3M, Akzo Nobel N.V., Evonik Industries AG, Merck KGaA, The Sherwin-Williams Company, and Wacker Chemie AG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Usage in Protective and Industrial Coatings

- 4.1.2 Vast Applications in the Healthcare Industry

- 4.1.3 Augmenting Usage in Optoelectronic Applications

- 4.2 Restraints

- 4.2.1 Technological Drawbacks and Incompatibility with Few Other Materials or Additives

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Application

- 5.1.1 Medical

- 5.1.2 Paints and Coatings

- 5.1.2.1 Inorganic Polysiloxane

- 5.1.2.2 Epoxy-Polysiloxane Hybrids

- 5.1.2.3 Acrylic-Polysiloxane Hybrids

- 5.1.3 Adhesives and Sealants

- 5.1.4 Elastomers

- 5.1.5 Organo Electronic Materials

- 5.1.6 Fabrics

- 5.1.7 Other Applications (Personal Care, Cosmetics, Etc.)

- 5.2 End-user Industry

- 5.2.1 Healthcare

- 5.2.2 Oil and Gas

- 5.2.3 Power

- 5.2.4 Infrastructure

- 5.2.5 Transportation

- 5.2.6 Electronics

- 5.2.7 Food and Beverage

- 5.2.8 Textile

- 5.2.9 Other End-user Industries (Membranes, Antifoaming Agents, Etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 Asian Paints

- 6.4.4 Biro Technology Inc.

- 6.4.5 Dampney Company

- 6.4.6 Evonik Industries AG

- 6.4.7 Gelest Inc.

- 6.4.8 Huntsman Corporation LLC

- 6.4.9 Merck KGaA

- 6.4.10 Restek Corporation

- 6.4.11 The Sherwin-Williams Company

- 6.4.12 Wacker Chemie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Continuous R&D of Polysiloxane Technologies for Development of Newer Applications

- 7.2 Other Opportunities

ポリシロキサン:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日