|

市場調査レポート

商品コード

1641846

住宅用ルーター:市場シェア分析、産業動向と統計、成長予測(2025~2030年)Residential Routers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 住宅用ルーター:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

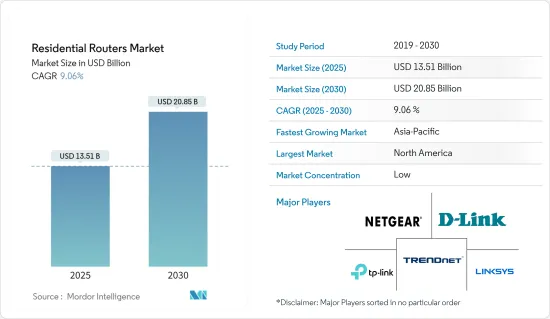

住宅用ルーター市場規模は2025年に135億1,000万米ドル、2030年には208億5,000万米ドルに達すると予測、予測期間(2025~2030年)のCAGRは9.06%。

主要ハイライト

- IoTデバイスの家庭への統合は、堅牢なインターネット接続とネットワークに大きく依存しています。スマートホームがシームレスに機能するのは、すべての自動化デバイスが設置場所でインターネットに適切に接続されている場合に限られます。そこで活躍するのが、家庭内のインターネット接続を管理するルーターです。このように、ルーターは中断のないスムーズなネットワーク機能を確保する上で重要な役割を果たしています。

- 2022年3月、Vodafone-Ideaは、最大10台のWi-Fi対応機器を接続できるポケットサイズの4Gルーター、Vi MiFiを発売しました。このルーターは2,700mAhの大容量バッテリーを誇り、1回の充電で最大5時間使用できます。さらに2022年8月、Reliance JioはJio Wi-Fiメッシュ・ルーターを発売しました。このルーターは家庭内のネットワーク・カバレッジを拡大し、ワンフロアで最大1,000平方フィートのエリアをカバーします。

- COVID-19の大流行により、ネットワークトラフィックは大幅に増加し、最初の数週間で40%の急増が確認されました。流行が拡大するにつれ、トラフィックパターンはビジネスパークから住宅地へとシフトし、コンテンツ消費、ゲーム、OTT需要の継続的な急増につながりました。このことは、効率的な家庭用ルーターの必要性を浮き彫りにしています。

- ルーターとデバイス間の距離がWi-Fiの速度と接続強度に大きく影響することは注目に値します。そのため、ルーターは家のあらゆる場所に届くよう、強く広い信号を提供するよう設計されていることが不可欠です。競争の激しい市場に耐えるため、ルーターメーカーには絶え間ない技術革新と技術進歩が求められています。

住宅用ルーター市場の動向

ワイヤレス接続が市場成長を牽引

- インターネットは長年にわたり、特に都市部ではより手頃な価格で利用できるようになり、無線技術の普及に伴って半都市部や農村部でも利用されるようになりました。ワイヤレス接続はケーブルを必要とせず、有線接続よりも高速であるため、人々の生活に利便性をもたらしただけでなく、生産性も大幅に向上しました。その結果、Wi-Fiルーターはほとんどの家庭で当たり前のものとなりました。

- 2023年3月、QualcommはWeSchool、Telecom Italia(TIM)社、Acerと共同で、イタリアの学校に次世代ワイヤレス技術ソリューションを提供する5G Smart Schoolsプログラムを開始しました。このプログラムは、中高生のデジタルスキルを向上させ、教師に専門能力開発の機会を提供することを目的としています。

- さらに、コックス・プライベート・ネットワークスは、地方で高速インターネットを提供するための固定ワイヤレス(FWA)検査を実施しています。この取り組みは、デジタルデバイドを解消し、遠隔地に住む人々にインターネットへのアクセスを提供する一助となります。

- 2022年3月、米国政府は、農村地域のインターネットサービス料金を支援するため、Affordable Connectivity Program(ACP)に142億米ドルを調達しました。ミッドバンドの周波数で、CBRS(Citizens Band Radio Service)は農村地域にブロードバンドを記載しています。地域のインターネット・プロバイダーであるブロードバンドは、農村地域に特化したCBRSベースの固定無線アクセスサービスをデビューさせ、遠隔地でのインターネットへのアクセスをさらに改善しました。

- 全体として、インターネットのアクセシビリティと利用しやすさの向上は、新しい無線技術の開発とともに、人々の生活に多くの恩恵をもたらし、教育、コミュニケーション、経済成長の機会を向上させています。

北米が大きな市場シェアを占める見込み

- GSMAの最新レポートによると、5Gは現在北米で活況を呈しており、2025年までに無線サービスセグメントを支配すると予測されています。米国の5G普及率は世界第2位で、これを上回るのは韓国のみと予想されています。2025年までには、通信事業者がミッドバンド周波数帯の導入を増やすため、モバイル設備投資のほぼすべてを5Gが占めるようになると予測されています。その結果、5Gの売上は2021年の2,940億米ドルから2025年には3,330億米ドルに増加すると予想され、この技術の巨大な成長の可能性を示しています。

- さらに、5Gはカナダの人口の92%、米国の人口の100%をカバーすると予想されています。米国の大手通信会社は、5G固定無線アクセス(FWA)技術を活用し、固定ブロードバンドセグメントでケーブル・プロバイダーから市場シェアを獲得しようとしています。なかでも、2022年第1四半期時点でFWA加入者数98万人のT-Mobileは、5G FWAサービスの単一プロバイダーとしては最大手です。

- 2022年10月、トランザクション・ネットワークサービス(TNS)は世界のワイヤレスアクセス向けのスマートシム機能を開始しました。TNSの広範な地域と国際ワイヤレスカバレッジにより、北米の顧客は、展開が必要な場所であればどこでも、24時間体制のサポートとともに、同じ信頼できる安全なワイヤレス接続を利用することができ、さまざまな地域でローミングや国内接続の選択肢へのアクセスを提供することができます。

- まとめると、5Gは北米で急速な成長を遂げており、2025年までに無線サービスセグメントを支配し続けると予想されます。米国は、T-Mobileが5G FWAサービスをリードしており、5Gの普及率が世界的に最も高い国のひとつとなります。TNSのSmart Sim機能により、北米の顧客は、包括的なカバレッジとサポートに支えられた、ビジネスニーズに対応した信頼性の高い安全な無線接続の恩恵を受けることができます。

住宅用ルーター産業概要

新しい帯域幅の使用とサービス提供シナリオがネットワークインフラを再構築しているため、住宅用ルーター市場は大きな変化を経験しています。機器メーカーは、より広範なサービスやアプリケーションをサポートし、容量の拡大性と高いデータ転送速度を提供するキャリアクラスのルーターを開発することで対応しています。このセグメントには多くの参入企業が参入しているため、市場は非常に細分化されており、メーカーが製品の革新的なハードウェアやソフトウェア機能に投資することで、さらに成長する可能性を秘めています。このセグメントでサービスを提供している主要企業には、D-Link Corporation、Netgear Inc.、Linksys Group(Foxconn)、Synology Inc.などがあります。

2022年5月、HFCL LimitedはWiproと協業し、企業が5G対応ビジョンを実現し、高品質な5Gソリューションを市場に投入するスピードを高めることを可能にする5Gトランスポートソリューションを発表しました。2022年10月、MediaTekはInvendisと提携し、Made in Indiaの5GルーターとWi-Fiソリューションを発表し、消費者と企業顧客に安全で強力かつシームレスなワイヤレスネットワーキングソリューションを記載しています。また、2023年2月には、Telecom26とTrasna Solutionsが提携し、携帯電話ルーター向けのeSIM管理ソリューションを開発し、ルーターメーカーに既存のSIMベースのデバイスでeSIMを管理する効率的でユーザーフレンドリーな方法を提供しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- COVID-19の市場への影響

- 市場促進要因

- コネクテッドデバイスの需要増加とスマートホーム市場の拡大

- IPトラフィックの増加

- 市場課題

- セキュリティ侵害の脅威の増大

第5章 市場セグメンテーション

- 接続タイプ

- 有線

- ワイヤレス

- 標準規格

- 802.11b/g/n

- 802.11ac

- 802.11ax

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- その他のアジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 北米

第6章 競合情勢

- 企業プロファイル

- Netgear Inc.

- D-Link Corporation

- TP-Link Technologies Co. Ltd

- Linksys Group(Foxconn)

- TRENDnet Inc.

- Synology Inc.

- AsusTek Computer Inc.

- Google Inc.

- Nokia Networks

- Xiaomi Inc.

第7章 投資分析

第8章 市場の将来

The Residential Routers Market size is estimated at USD 13.51 billion in 2025, and is expected to reach USD 20.85 billion by 2030, at a CAGR of 9.06% during the forecast period (2025-2030).

Key Highlights

- The integration of IoT devices into households is heavily reliant on robust internet connections and networks. A smart home can only function seamlessly if all automation devices are properly connected to the internet at the location where they are installed. This is where the router comes into play as it manages internet connectivity within the home. Thus, a router plays a crucial role in ensuring uninterrupted and smooth network functioning.

- In March 2022, Vodafone-Idea launched the Vi MiFi, a pocket-sized 4G router that enables users to connect up to 10 Wi-Fi-enabled devices. This router boasts a high battery capacity of 2700 mAh, which can last for up to 5 hours on a single charge. Additionally, in August 2022, Reliance Jio launched the Jio Wi-Fi Mesh router, which expands network coverage across homes, covering an area of up to 1000 sq ft across a single floor.

- The Covid-19 pandemic led to a significant increase in network traffic, with a 40% surge observed in the first few weeks. As the outbreak spread, traffic patterns shifted from business parks to residential areas, leading to a continued surge in content consumption, gaming, and OTT demand. This highlights the need for efficient home routers.

- It is worth noting that the distance between the router and the device can greatly impact Wi-Fi speed and connection strength. Therefore, it is essential that routers are designed to provide a strong and wide signal to reach all areas of the house. To withstand the competitive market, router manufacturers require constant innovation and technological advancements.

Residential Router Market Trends

Wireless Connectivity to Witness the Market Growth

- The Internet has become more affordable and accessible over the years, particularly in urban areas, and has even made its way to semi-urban and rural areas with the widespread adoption of wireless technology. This has not only brought convenience to people's lives but has also significantly improved productivity, as wireless connections do not require cables and are faster than wired connections. As a result, Wi-Fi routers have become a norm in most houses.

- In March 2023, Qualcomm, in partnership with WeSchool, Telecom Italia (TIM), and Acer, launched the 5G Smart Schools program to provide next-generation wireless technology solutions to schools in Italy. The program aims to develop digital skills among secondary school students and provide professional development opportunities for teachers.

- Moreover, Cox Private Networks is running Fixed Wireless (FWA) trials to deliver high-speed internet in rural areas. This initiative will help bridge the digital divide and provide access to the internet to people living in remote areas.

- In March 2022, the US Government raised 14.2 billion USD for the Affordable Connectivity Program (ACP) to help rural communities pay for their internet service. With mid-band frequencies, Citizens Band Radio Service (CBRS) will offer broadband in rural communities. Broadband, a regional internet provider, debuted CBRS-based Fixed Wireless Access services focused on rural areas, further improving access to the internet in remote locations.

- Overall, the increasing accessibility and affordability of the Internet, along with the development of new wireless technologies, are bringing numerous benefits to people's lives and improving opportunities for education, communication, and economic growth.

North America Is Expected to Hold Significant Market Share

- Based on the latest report from GSMA, 5G is currently booming in North America and is projected to dominate the wireless services sector by 2025. The United States is expected to have the world's second-highest 5G adoption rate, with only South Korea surpassing it. By 2025, 5G is forecasted to account for almost all mobile capex as operators increase mid-band spectrum deployments. As a result, 5G revenues are expected to increase from 294 billion USD in 2021 to 333 billion USD in 2025, showing the immense growth potential for this technology.

- Moreover, 5G is expected to cover 92% of the Canadian population and 100% of the US population. Major telcos in the US are leveraging 5G Fixed Wireless Access (FWA) technology to gain market share from cable providers in the fixed broadband sector. Among them, T-Mobile, with 0.98 million FWA subscribers as of Q1 2022, is the largest single provider of 5G FWA services.

- In October 2022, Transaction Network Services (TNS) launched its Smart Sim capability for Global Wireless Access, which benefits processors, ISOs, and merchants across the US. TNS's extensive local and international wireless coverage allows North American customers to take advantage of the same dependable and secure wireless connectivity, with round-the-clock assistance, wherever they need to deploy, providing access to roaming and domestic connectivity choices in various geographies.

- In summary, 5G is experiencing rapid growth in North America and is expected to continue to dominate the wireless services sector by 2025. The US is poised to have one of the highest 5G adoption rates globally, with T-Mobile leading the charge in 5G FWA services. With TNS's Smart Sim capability, North American customers can benefit from reliable and secure wireless connectivity for their business needs, backed by comprehensive coverage and support.

Residential Router Industry Overview

The residential router market is experiencing significant changes as new bandwidth usage and service delivery scenarios are reshaping network infrastructures. Equipment manufacturers are responding by developing carrier-class routers that support a broader range of services and applications and offer capacity scalability and higher data rates. With many players involved in this sector, the market is highly fragmented and has the potential to grow further as manufacturers invest in innovative hardware and software features in their products. Some significant players offering their services in this sector include D-Link Corporation, Netgear Inc., Linksys Group (Foxconn), Synology Inc., and more.

In May 2022, HFCL Limited collaborated with Wipro to introduce 5G transport solutions that enable enterprises to realize their 5G-enabled vision and increase the speed with which they can bring high-quality 5G solutions to the market. In October 2022, MediaTek partnered with Invendis to launch Made in India 5G Routers and Wi-fi solutions, providing consumers and enterprise customers with secure, strong, and seamless wireless networking solutions. And in February 2023, Telecom26 and Trasna Solutions partnered to develop eSIM management solutions for cellular routers, offering router manufacturers an efficient and user-friendly way to manage eSIMs on their existing SIM-based devices.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 on the Market

- 4.4 Market Drivers

- 4.4.1 Increasing Demand of Connected Devices and Proliferating Smart Homes Market

- 4.4.2 Growth in IP Traffic

- 4.5 Market Challenges

- 4.5.1 Increasing Threat of Security Breaches

5 MARKET SEGMENTATION

- 5.1 Connectivity Type

- 5.1.1 Wired

- 5.1.2 Wireless

- 5.2 Standard

- 5.2.1 802.11b/g/n

- 5.2.2 802.11ac

- 5.2.3 802.11ax

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.5 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Netgear Inc.

- 6.1.2 D-Link Corporation

- 6.1.3 TP-Link Technologies Co. Ltd

- 6.1.4 Linksys Group (Foxconn)

- 6.1.5 TRENDnet Inc.

- 6.1.6 Synology Inc.

- 6.1.7 AsusTek Computer Inc.

- 6.1.8 Google Inc.

- 6.1.9 Nokia Networks

- 6.1.10 Xiaomi Inc.