|

市場調査レポート

商品コード

1640686

インドの医薬品包装:市場シェア分析、産業動向、成長予測(2025~2030年)India Pharmaceutical Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドの医薬品包装:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 122 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

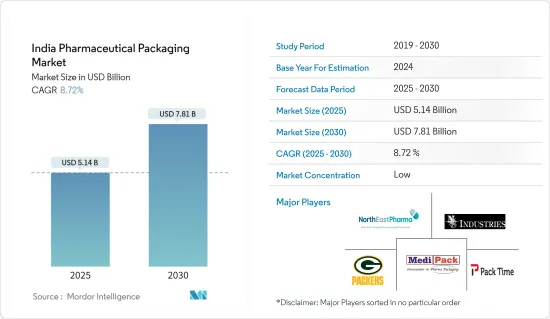

インドの医薬品包装の市場規模は2025年に51億4,000万米ドルと推計され、予測期間中(2025~2030年)のCAGRは8.72%で、2030年には78億1,000万米ドルに達すると予測されています。

医薬品包装は、医薬品を安全に移送・保管するために設計された材料を使用します。これらの材料は医薬品の特性に基づいて選択され、封入された製品の保護、識別、完全性の維持を目的としています。包装工程では、汚染、物理的損傷、環境条件など、医薬品の有効性と安全性を損なう可能性のある外的要因から医薬品を確実に保護します。医薬品の包装は、服用方法や規制遵守の詳細など、医薬品に関する重要な情報を提供する上で極めて重要です。

主なハイライト

- 医薬品は、機械的、化学的、生物学的、気候的リスクなど様々な危険に直面しています。医薬品は、プラスチック、紙、ガラス、金属など複数の素材を用いて包装され、経口、肺、注射、経皮、局所、インターベンション、経鼻、点眼など、さまざまな送達方法に合わせて調整されます。

- インド政府は、製薬業界を強化するために広範かつ継続的な改革を実施しており、外国直接投資(FDI)を促進する政策を発表しています。Aatmanirbhar Bharat Abhiyaanイニシアチブの一環として、政府は医療制度を強化するための短期的・長期的な施策を導入しています。その中には、国内の医薬品・医療機器製造を強化するために特別に設計された生産連動奨励金(PLI)制度の実施も含まれています。さらに、インドはアーユルヴェーダとヨガの強みを生かし、スピリチュアル・ツーリズムとウェルネス・ツーリズムの目的地として積極的に位置づけています。このような戦略的な動きは、調査された市場に大きな影響を与えようとしています。

- インドの医薬品包装市場は、環境問題への関心の高まりから、生態系や人の健康への影響に対する監視の目を強めています。製薬業界における持続可能性の推進は、二酸化炭素排出量の削減だけでなく、特にインドのような国では、長期にわたって生態系と公衆衛生を守ることでもあります。こうした環境課題に効果的に対処する必要性から、環境に優しく持続可能な医薬品包装ソリューションへの需要が急速に高まっています。

- さらに、供給企業の交渉力は価格や品質に直接影響するため、バリューチェーン、ひいては消費者に提供される製品やサービスを左右します。サプライヤーの力が強まれば、原材料費も上昇し、最終製品の価格も上昇します。

- インドの製薬業界は、すでにジェネリック医薬品の製造で知られる世界の大手企業でした。国内外での医薬品需要の高まりは、多様で先進的なパッケージング・ソリューションの必要性を後押ししました。COVID-19ワクチンの開発と流通には、安全で効果的な配送を確保するため、バイアル、シリンジ、コールドチェーン包装などの特殊な包装ソリューションが必要だった。インド保健家族福祉省(Ministry of Health and Family Welfare)によると、インドのウター・プラデシュ州は、2023年11月13日現在、コロナウイルスに対するワクチンの投与数が最も多いと報告しています。

インドの医薬品包装の市場動向

プラスチックセグメントが市場の成長を牽引

- インドのヘルスケア業界では、衛生、安全性、利便性が重視され、フレキシブルな使い捨てプラスチック包装の需要が顕著に急増しています。多くの産業が環境への懸念から使い捨てプラスチックからの脱却を進めているが、ヘルスケアは例外であり、その主な理由は安全性と衛生面です。これは、この業界が使い捨てプラスチック包装に依存していることを意味し、プラスチック包装の需要を牽引しています。プラスチックはHDPE、PET、PPなど汎用性の高い素材で、柔軟性、機械的強度、安定性などの特性から製薬業界で使用されています。

- インド政府は製薬業界を強化するため、広範かつ継続的な改革を実施しています。インド・ブランド・エクイティ財団(IBEF)によると、インド政府は2023会計年度にGDPの2.6%をヘルスケアに支出しました。2025年にはGDPの2.5%になると予想されています。

- 製品タイプのうち、ボトル分野は、同国におけるHDPEボトルとPETボトルの生産量の伸びと、HDPE(高密度ポリエチレン)ボトルがその強度、弾力性、耐薬品性により製薬業界の業界標準として台頭してきたことに伴い、市場の成長に大きく貢献すると予想されます。HDPEボトルは、その強度、弾力性、耐薬品性により、医薬品業界の業界標準として台頭してきました。これらの特性は、様々な医薬品の保護や保管に最適であり、市場におけるプラスチックボトル使用の拡大を支えています。

- この製品タイプは、添加剤によって本来の特性をさらに向上させることができ、最終製品の酸素、湿気、紫外線に対する性能や特性を改善することができるため、インドの製薬業界ではプラスチック包装が非常に好まれる包装タイプとなっています。

インド市場ではボトルが最も急成長する製品セグメントとなる

- 液体医薬品包装用ボトルの需要は、ガラス、プラスチック、その他の素材ベースのボトル包装の需要を促進しています。これらのボトルは、液体医薬品、固形錠剤、ゲル錠剤以外にも使用できます。特定の用量や製品に合わせた様々なサイズがあります。ガラス製とプラスチック製の両方があり、指示通りに保管すれば、開封後も品質が保たれます。

- アクセスしやすく、質の高いヘルスケア、特に慢性疾患に対する手ごろな価格のヘルスケアを求めて、インドでは持続可能なボトル医薬品包装ソリューションの必要性が高まっています。国連アジア太平洋経済社会委員会(ESCAP)によると、2023年には15歳から64歳の人口がインドの人口の68.9%を占める。この層は2050年には67.0%を占めると予測されています。

- HDPEベースのボトルの生産と入手可能性は、市場におけるボトル分野の成長を支えることができます。なぜなら、ボトルは保存期間中、汚染や劣化から医薬品を守り、安全で効果的な状態を保つことを保証するからです。インドでは、安全な医薬品包装の需要が伸び続けています。HDPEボトルは、医薬品の保管と保護に必要な厳しい基準を満たす能力があるとして、ますます認知されるようになっています。

- PETボトルは、製品の保護、視認性、カスタマイズ性などの用途や利点から、医薬品包装に好まれる選択肢となっています。PETボトルはリサイクル可能で、二酸化炭素排出量を削減し、資源を保護するため、環境的に持続可能です。これらの要因から、予測期間中、インドの製薬業界ではPETボトルの包装への利用が増加すると予想されます。

インドの医薬品包装業界の概要

インドの医薬品包装市場は断片化されており、Medipack Innovations Private Limited、Packtime Innovations Private Limited、North East Pharma Pack、NS Industries、AS Packersなどの大手企業が独占しています。これらの企業は、市場シェアと収益性を高めるために戦略的な共同イニシアティブを活用しています。しかし、技術の進歩や製品の革新に伴い、中堅・中小企業は新たな契約を獲得し、新市場を開拓することで市場での存在感を高めています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の度合い

- 産業バリューチェーン分析

- ミクロ経済要因が市場に与える影響の評価

第5章 市場力学

- 市場促進要因

- 環境問題に対する意識の高まりと新たな規制基準の採用

- インドにおける慢性疾患患者数の急増

- 市場抑制要因

- 供給企業の交渉力による原材料コストの変動

第6章 市場セグメンテーション

- 材料タイプ別

- プラスチック

- ガラス

- その他の素材タイプ

- 製品タイプ別

- ボトル

- バイアル・アンプル

- シリンジ

- チューブ

- キャップと栓

- パウチとバッグ

- ラベル

- その他の製品タイプ

第7章 競合情勢

- 企業プロファイル

- Medipack Innovations Private Limited

- Packtime Innovations Private Limited

- North East Pharma Pack

- N S Industries

- A S Packers

- JK Print Packs

- West Pharmaceutical Packaging India Pvt. Ltd(West Pharmaceutical Services Inc.)

- Huhtamaki India Ltd(Huhtamaki Oyj)

- SGD Pharma India Ltd(SGD Pharma)

- Uflex Limited

- Amcor Flexibles India Pvt. Ltd(Amcor PLC)

- Essel Propack Ltd

- Parekhplast India Limited

- Regent Plast Pvt. Ltd

- Graham Blow Pack Pvt. Limited

- Hoffmann Neopac AG

- ベンダー市場シェア分析

第8章 投資分析

第9章 市場の将来

The India Pharmaceutical Packaging Market size is estimated at USD 5.14 billion in 2025, and is expected to reach USD 7.81 billion by 2030, at a CAGR of 8.72% during the forecast period (2025-2030).

Pharmaceutical packaging uses materials designed to transfer and store pharmaceutical drugs safely. These materials are selected based on the drugs' characteristics, aiming to safeguard, identify, and maintain the integrity of the enclosed product. The packaging process ensures that the drugs are protected from external factors such as contamination, physical damage, and environmental conditions, which could potentially compromise their efficacy and safety. Pharmaceutical packaging is crucial in providing essential information about the drug, including dosage instructions and regulatory compliance details.

Key Highlights

- Pharmaceutical drugs face various hazards, spanning mechanical, chemical, biological, and climatic risks. They are packaged using multiple materials, including plastics, paper, glass, and metal, and tailored to different delivery methods, such as oral, pulmonary, injectable, transdermal, topical, interventional, nasal, and ocular.

- The Indian government has implemented extensive and ongoing reforms to bolster the pharmaceutical industry, unveiling policies to foster foreign direct investments (FDI). As part of the Aatmanirbhar Bharat Abhiyaan initiative, the government has introduced a range of short- and long-term measures to fortify the health system. These include implementing Production-linked Incentive (PLI) schemes specifically designed to enhance domestic pharmaceutical and medical device manufacturing. Moreover, India is actively positioning itself as a destination for spiritual and wellness tourism, leveraging its strengths in Ayurveda and yoga practices. These strategic moves are poised to impact the market studied significantly.

- The pharmaceutical packaging market in India is under increasing scrutiny for its impact on ecosystems and human health, given the escalating environmental concerns. The push for sustainability in the pharmaceutical industry is not just about reducing its carbon footprint but also about safeguarding ecosystems and public health for the long haul, especially in a country like India. The demand for eco-friendly and sustainable pharmaceutical packaging solutions is growing rapidly, driven by the need to address these environmental challenges effectively.

- Moreover, supplier bargaining power directly impacts pricing and quality, thereby dictating the value chain and, ultimately, the products and services delivered to consumers. As a supplier's power grows, so do the costs of raw materials, subsequently elevating the final product's price tag.

- The Indian pharmaceutical industry was already a major global player known for its generic drug manufacturing. The increasing demand for pharmaceutical products both domestically and internationally drove the need for diverse and advanced packaging solutions. The development and distribution of COVID-19 vaccines required specialized packaging solutions, including vials, syringes, and cold chain packaging, to ensure safe and effective delivery. According to the Ministry of Health and Family Welfare (India), the Indian state of Utter Pradesh reported the highest number of administered doses of the vaccine against the coronavirus as of November 13, 2023.

India Pharmaceutical Packaging Market Trends

Plastic Segment to Witness Major Market Growth

- The healthcare industry in India is witnessing a notable surge in the demand for flexible single-use plastic packaging, driven by a heightened emphasis on hygiene, safety, and convenience. While many industries are moving away from single-use plastics due to environmental concerns, healthcare is an exception, primarily due to safety and hygiene. This signifies the industry's reliance on single-use plastic packaging and drives the demand for plastic packaging. Plastic is a highly versatile material, including HDPE, PET, and PP, and is used in the pharmaceutical industry due to its flexibility, mechanical strength, and stability characteristics.

- The Indian government has implemented extensive and ongoing reforms to bolster the pharmaceutical industry. According to the India Brand Equity Foundation (IBEF), the Indian government spent 2.6% of the country's GDP on healthcare in the financial year 2023. Government healthcare spending is anticipated to be 2.5% of the GDP in the financial year 2025.

- Among product types, the bottle segment is anticipated to contribute significantly to the market's growth in line with the growth of HDPE and PET bottle production in the country and the emergence of HDPE (high-density polyethylene) bottles as the industry standard in the pharmaceutical industry due to their strength, resilience, and chemical resistance. These qualities make them perfect for safeguarding and storing a variety of medical supplies, supporting the growth of plastic bottle usage in the market.

- The material's intrinsic properties can be further improved through additives, improving performance and properties to act against oxygen, moisture, and UV radiation to the finished product, making plastic packaging a highly preferable type of packaging in the Indian pharmaceutical industry.

Bottles to be the Fastest-growing Product Segment in the Indian Market

- The demand for bottles for liquid pharmaceutical product packaging fuels the demand for glass, plastic, and other material-based bottle packaging. These bottles can be used for more than liquid medicines, solid pills, and gel tablets. They come in various sizes tailored to the specific dosage or product. Available in both glass and plastic, they maintain quality even after opening, provided they are stored as directed.

- The push for accessible, high-quality healthcare, especially for chronic diseases, at affordable rates is fueling the need for sustainable bottle pharmaceutical packaging solutions in India. According to the United Nations Economic and Social Commission for Asia and the Pacific (ESCAP), individuals aged between 15 and 64 constituted 68.9% of India's population in 2023. This demographic is projected to account for a share of 67.0% by 2050.

- The production and availability of HDPE-based bottles can support the growth of the bottles segment in the market because bottles ensure that medications remain safe and effective throughout their shelf life, shielding them from contamination and degradation. The demand for safe pharmaceutical packaging continues to grow in India. HDPE bottles are increasingly recognized for their ability to meet the rigorous standards required for storing and protecting medicinal products.

- PET plastic bottles have become the favored choice for pharmaceutical packaging owing to their applications and advantages in offering product protection, visibility, and customization. PET bottles can be environmentally sustainable due to their recyclability, reduced carbon footprint, and resource conservation. These factors are expected to support their increasing usage for packaging in the Indian pharmaceutical industry during the forecast period.

India Pharmaceutical Packaging Industry Overview

The Indian pharmaceutical packaging market is fragmented and dominated by significant players like Medipack Innovations Private Limited, Packtime Innovations Private Limited, North East Pharma Pack, NS Industries, and AS Packers. These companies leverage strategic collaborative initiatives to increase their market share and profitability. However, with technological advancements and product innovations, mid-size to smaller companies are growing their market presence by securing new contracts and tapping new markets.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of Microeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Awareness of Environmental Issues and Adoption of New Regulatory Standards

- 5.1.2 Surging Number of Chronic Disease Cases in India

- 5.2 Market Restraints

- 5.2.1 Fluctuations in Raw Material Costs Due to Suppliers' Bargaining Power

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Plastic

- 6.1.2 Glass

- 6.1.3 Other Material Types

- 6.2 By Product Type

- 6.2.1 Bottles

- 6.2.2 Vials and Ampoules

- 6.2.3 Syringes

- 6.2.4 Tubes

- 6.2.5 Caps and Closures

- 6.2.6 Pouches and Bags

- 6.2.7 Labels

- 6.2.8 Other Product Types

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Medipack Innovations Private Limited

- 7.1.2 Packtime Innovations Private Limited

- 7.1.3 North East Pharma Pack

- 7.1.4 N S Industries

- 7.1.5 A S Packers

- 7.1.6 JK Print Packs

- 7.1.7 West Pharmaceutical Packaging India Pvt. Ltd (West Pharmaceutical Services Inc.)

- 7.1.8 Huhtamaki India Ltd (Huhtamaki Oyj)

- 7.1.9 SGD Pharma India Ltd (SGD Pharma)

- 7.1.10 Uflex Limited

- 7.1.11 Amcor Flexibles India Pvt. Ltd (Amcor PLC)

- 7.1.12 Essel Propack Ltd

- 7.1.13 Parekhplast India Limited

- 7.1.14 Regent Plast Pvt. Ltd

- 7.1.15 Graham Blow Pack Pvt. Limited

- 7.1.16 Hoffmann Neopac AG

- 7.2 Vendor Market Share Analysis