|

市場調査レポート

商品コード

1851516

欧州のポリ塩化ビニル(PVC):市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Europe Polyvinyl Chloride (PVC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のポリ塩化ビニル(PVC):市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月22日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

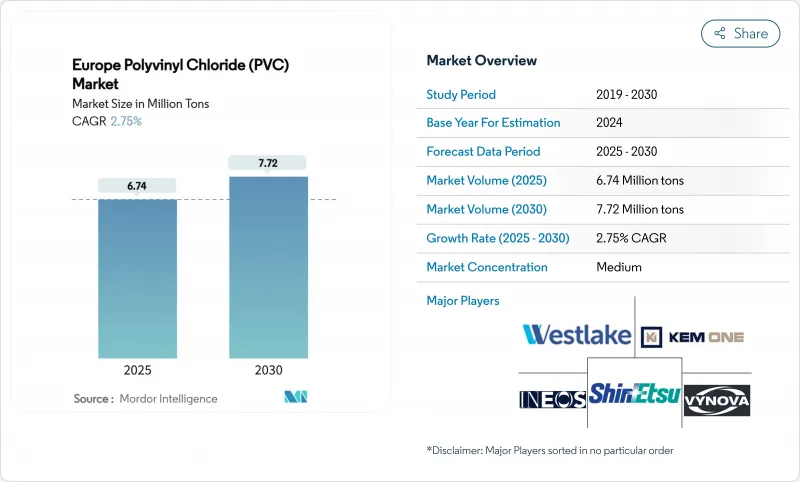

欧州のポリ塩化ビニル市場規模は2025年に674万トンと推定・予測され、予測期間(2025~2030年)のCAGRは2.75%で、2030年には772万トンに達すると予測されます。

パイプ、プロファイル、継手の堅調な需要は、住宅建設の緩やかな回復と相まって、当面の数量増加を下支えします。REACHによる規制圧力は引き続きカルシウム亜鉛安定剤の採用を加速させるが、持続的なインフラ支出が移行コストを緩和します。エネルギー効率の高い改築プログラム、電力網の整備、水管理プロジェクトが構造需要を支える一方、循環型経済の義務化により、リサイクルや生物由来のPVCへの投資が急ピッチで進められています。競合の激しさは中程度にとどまるが、これは総合メーカーが規模、専用原料、独自技術を活用してコンプライアンス・コストを相殺しているためです。

欧州のポリ塩化ビニル(PVC)市場動向と洞察

建設業界からの需要拡大

この地域の住宅不足と建物ストックの老朽化により、改築の動きが活発化しており、欧州の塩ビ市場では窓材とサイディングの数量が伸びています。熱可塑性樹脂インサートで強化されたPVCフレームの熱性能は12~13%向上し、EUのエネルギー効率規制への適合性が高まるため、硬質PVCは改修プロジェクトにさらに浸透しています。加盟国の復興基金が土木工事への支出に充てられ、農業インフラにおける塩ビの機能的・コスト的優位性が保水排水システムで実証されています。金利の安定化と材料価格の正常化は、北欧市場全体のプロジェクトの実行可能性を高めていますが、南欧では財政的制約が引き続き成長を抑制しています。全体的な効果として、PVCパイプとプロファイルの需要は中期的にうまく分散して増加しています。

自動車産業からの需要増加

電気自動車の普及により内装部品の仕様が変更され、ワイヤーハーネスや床材に難燃性軟質PVCが使用される機会が広がっています。2025年初頭のドイツの自動車生産台数は前年比3%増となり、地域のコンパウンド工場からの樹脂引き取りを押し上げました。バイオ添加PVCグレードは、引張性能と熱性能を維持しながら、ゆりかごからゲートまでのCO2排出量を58%削減し、OEMがプラットフォームを再設計することなくESG目標を達成することを可能にします。ドイツ、フランス、北イタリア周辺の成長クラスターは、最適化されたロジスティクスとジャスト・イン・シーケンス供給モデルを促進しています。ティアワン・サプライヤーは、デジタル品質管理ツールと素材イノベーションを組み合わせることで、トリムの無駄をなくし、サイクルタイムを短縮しています。

小売業者によるPVC食品包装の禁止が加速する

西欧の大手スーパーマーケット・チェーンは、PVCトレーやクリンフィルムを段階的に廃止しており、コンバーター各社は単素材のPETや紙をベースとしたフォーマットへの移行を迫られています。近々予定されている包装および包装廃棄物規制では、PFASとBPAの規制が追加され、従来のPVC製剤のコンプライアンス経路が複雑になります。医薬用ブリスターパックは依然として適用除外であるが、大量の生鮮食品分野は即座に代替品に切り替わるため、欧州PVC市場のフレキシブルフィルム需要は減少します。ブランドオーナーの購買方針が上流に連鎖し、コンパウンド業者は代替樹脂の認定や、ニッチでバリア性が重要な用途向けのリサイクル可能なPVCブレンドの開発を余儀なくされます。東欧市場では禁止措置の導入が遅れており、一時的な緩和にはなっているもの、最終的には地域全体の移行を示唆しています。

セグメント分析

2024年の欧州PVC市場シェアは、パイプ、プロファイル、継手が建築物や給水ネットワークで優位を保っていることから、硬質グレードが60.74%を占めています。低煙塩ビは、ベースは小さいもの、大量輸送機関、トンネル、公共施設建設プロジェクトにおける防火安全規制を背景に、2030年までのCAGRが3.89%と最も高くなる見込みです。軟質PVCは、医療用チューブ向けのバイオプラスチック化透明グレードの需要が、食品包装用フィルムの縮小を補っています。塩素化PVCは、輸入関税と物流コストを軽減するために現地生産を活用し、工業用温水ラインに浸透しています。

成熟した需要パターンが稼働率を80%前後に安定させるため、生産能力増強は規律正しく維持されます。押出機は、グリーンフィールドの拡張よりも、ダイヘッドのアップグレードとインライン測定システムに重点を置いて歩留まりを高める。コンバーターは、化学処理用サイトグラスのリジッドクリアオーダーと市管契約のバルクコミットメントを両立させるため、製品ミックスの敏捷性が競争上の差別化要因となります。このように、欧州のPVC市場は、安定した大量硬質需要と、低煙やCPVCの特殊成長ニッチ分野とのバランスを保っています。

2024年にはカルシウム亜鉛溶液が安定剤消費量の42.88%を占めるが、これはEUの鉛禁止令後の市場の軸足を明確に示すものです。これらのパッケージは2030年までCAGR 3.61%で拡大すると予測され、欧州PVC市場の添加剤レベルの価値成長の大半を牽引します。鉛系安定剤は現在、一時的な規制緩和の下で、主に再生硬質材料の流れの中で存続しているが、錫系は耐熱電線被覆のニッチ分野で存続しています。バリウム亜鉛系と液状混合金属系は、特殊シートカレンダーに供給されているが、グリーンケミストリーの統一基準が下流に広がるにつれて、販売量の減少に直面しています。

化学薬品サプライヤーは、主要な押出ハブの近くにモジュール式配合施設を拡張し、ジャスト・イン・タイム納入と厳格な配合管理を確保します。プロファイルメーカーとの共同資格認定プログラムは、ライン変更の承認を加速し、変換スケジュールを圧縮します。安定剤のシフトは、規制の要請がいかにサプライチェーンを再編成し、研究開発の深さと統合されたロジスティクスを持つ事業者に有利であるかを明確に示しています。

欧州PVC市場レポートは、製品タイプ(硬質PVC、軟質PVC、低発煙PVC、その他)、安定剤タイプ(カルシウム系、鉛系、スズ・有機スズ系、その他)、用途(パイプ・継手、フィルム・シート、電線・ケーブル、その他)、エンドユーザー産業(建築・建設、自動車、電気・電子、その他)、地域(ドイツ、フランス、英国、イタリア、その他)で分類されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 建設業界からの需要の高まり

- 自動車産業からの需要増加

- 水インフラプロジェクトによる需要の増加

- 医療用PVCのヘルスケア需要

- 包装用途における使用の増加

- 市場抑制要因

- 加速する小売店による食品包装のPVC禁止

- 従来の鉛とスズ安定剤に対するREACH規制の強化

- ウィンドウ・プロファイル分野におけるバイオベースポリマー代替の高まり

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- 製品タイプ別

- リジッドPVC

- 透明リジッドPVC

- 非透明リジッドPVC

- フレキシブルPVC

- 透明フレキシブルPVC

- 非透明フレキシブルPVC

- 低発煙PVC

- 塩素化PVC

- リジッドPVC

- 安定剤タイプ別

- カルシウムベース(Ca-Zn)

- 鉛ベース(Pb)

- スズおよび有機スズベース(Sn)

- バリウム系その他(液体混合金属)

- 用途別

- パイプと継手

- フィルム・シート

- ワイヤー・ケーブル

- ボトル

- プロファイル,ホースとチューブ

- その他の用途

- エンドユーザー業界別

- 建築・建設

- 自動車

- 電気・電子

- パッケージング

- フットウェア

- ヘルスケア

- その他のエンドユーザー業界

- 地域別

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- トルコ

- その他欧州地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/順位分析

- 企業プロファイル

- Benvic Group

- Ercros S.A.

- Formosa Plastics Corporation

- Hanwa Solutions Chemical Division Corporation

- Industrie Generali S.p.A.

- INEOS

- KEM ONE

- LG Chem

- Lukoil

- Oltchim SA

- Orbia

- Shin-Etsu Chemical Co. Ltd.

- SIBUR Holding PJSC

- Solvay

- Teknor Apex

- Vynova Group

- Westlake Corporation