金属加工油剤:市場シェア分析、産業動向と統計、成長予測(2025~2030年)

Metal Working Fluids - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1640577

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

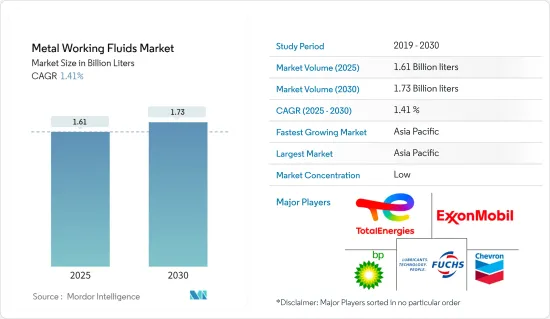

金属加工油剤市場規模は2025年に16億1,000万リットルと推定され、予測期間(2025~2030年)のCAGRは1.41%で、2030年には17億3,000万リットルに達すると予測されます。

主要ハイライト

- 自動車セクターと重機産業からの需要の伸びが金属加工油剤の需要を牽引する主要要因です。

- しかし、ドライ加工技術の採用や厳しい環境規制が市場の妨げになると予想されます。

- 複相金属加工油剤の出現と技術の進歩は、調査対象市場に新たな機会をもたらすと予想されます。

- アジア太平洋が市場を独占しており、中国、インド、日本などが最大の消費国です。

金属加工油剤市場の動向

自動車セクターからの需要の高まり

- 金属加工油剤は自動車産業において極めて重要です。工具とワークピース間の摩擦を減らし、表面品質を向上させ、金属切屑の除去を容易にし、工具寿命を延ばします。機械加工の効率を高めることで、機械生産量の向上に貢献します。

- 国際自動車製造者機構(OICA)によると、2023年には世界中で約9,355万台の自動車が生産され、2022年の8,483万台と比較して約10.26%の成長率を示しています。

- アジア・オセアニア地域は、自動車製造のトップランナーとして浮上し、他地域を圧倒しました。OICAのデータによると、この地域の自動車生産台数は2023年に5,511万台に達し、2022年の5,002万台から10.18%増加しました。特に、この生産は中国、日本、韓国、インドなどの主要企業が主導しています。

- OICA(Organisation Internationale des Constructeurs d'Automobiles)によると、2023年、中国は世界最大の自動車生産拠点としての地位を固め、3,016万台の自動車を生産します。これは、2022年の生産台数2,702万台から12%増加したことを意味します。

- 一方、米国は世界第2位の自動車メーカーとしての地位を固めました。自動車部門は米国経済の要であり、2023年のGDPに3%から3.5%寄与します。米国には大手自動車メーカーがあり、国内の需要を満たすだけでなく、南北アメリカ、欧州、アジア太平洋にまたがる市場に自動車を輸出しています。

- 国際自動車製造者機構(OICA)の報告によると、米国の2023年の自動車生産台数は1,061万台で、前年比6%増となりました。

- 欧州では2023年の自動車生産台数が顕著な伸びを示しました。全体として、生産台数は前年比で13%急増しました。特に乗用車とLCVの生産台数は12%と19%増加し、2023年にはそれぞれ1,540万台と160万台となりました。

- 自動車産業が拡大していることから、金属加工油剤の需要は予測期間中に増加するとみられます。

アジア太平洋が急成長

- アジア太平洋は、自動車と重機械・設備部門からの需要増に牽引され、市場をリードしています。中国、インド、日本などの国々では、工業化と経済成長に後押しされて重機械産業が急成長しています。

- 金属加工油剤は、重機械・装置の製造において重要な役割を果たしています。

- 重機械産業には、工作機械、重電機器、セメント機械、マテリアルハンドリング、プラスチック加工、プロセスプラント機器、土木・建設・採鉱用機器など、多様なサブセクターが含まれます。

- 中国の第14次5ヵ年計画は、農業と農村の変革を強化することを目的としており、これは農業と建設における重機使用の増加に直接関係しています。

- 中国の農業機械セクターは着実に上昇軌道にあり、1万社近くの農業機械企業と2万社以上の流通事業体を擁しています。2023年にアグロページが取り上げたように、14の対外貿易小部門の中で、農業機械の輸出は前年比33.5%増と好調で、特に大型・中型トラクターが伸びています。

- さらに、中国建設機械協会(CCMA)のデータによると、掘削機の販売台数は前年比5.31%増で、2024年6月には合計1万6,603台に達しました。国内販売台数は7,661台に達し、年率25.6%の高い伸びを示しました。

- インドの農業機械部門は世界的に大きなウェイトを占めており、多数のインドメーカーが国内外市場に対応しています。トラクター製造業者協会によると、2023年12月のトラクター販売台数は19.24%減少し、2022年の5万5,390台から4万4,735台に減少しました。しかし、海外輸出は2022年の13万1,850台から減少したもの、2023年には9万6,223台と好調を維持しました。

- インドの建設機械産業は、2023~24会計年度に26%の成長を遂げたが、これは主に政府のインフラ主導のアジェンダによるものです。インド建設機械工業会(ICEMA)によると、2023年の販売台数は13万5,650台に達し、前年の10万7,779台から増加しました。特に、産業最大のセグメントである土木機械の販売台数は、2023~24年度に21%増の9万3,531台となり、販売台数全体の約70%を占めました。

- インドにおける乗用車の販売台数は、2023会計年度に23%急増したと自動車販売協会連合会が報告しています。大手メーカーは、特に半導体とエレクトロニクスを中心に、断続的なサプライチェーンの課題を乗り切った。可処分所得の増加、新型スポーツ・公益事業車の波、魅力的なローン金利に牽引され、インドの乗用車販売台数は2023年度に初めて400万台を突破しました。

- インド自動車工業会(SIAM)によると、2023年度の乗用車、セダン、多目的車の販売台数は410万台を突破しました。これは2022年の379万台から8.2%増加したことになります。急増の主役は実用車で、総販売台数の57.4%を占めます。

- こうした力学を考えると、アジア太平洋は今後数年間、金属加工油剤市場をリードしていくことになります。

金属加工油剤産業概要

金属加工油剤市場は部分的に統合されています。主要参入企業(順不同)には、ExxonMobil、FUCHS、TotalEnergies、BP PLC、Chevron Corporationが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 自動車産業からの需要拡大

- 重機産業からの需要増加

- その他の促進要因

- 市場抑制要因

- ドライ加工技術の採用

- 厳しい環境規制

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- 製品タイプ別

- 除去液

- 成形液

- 保護液

- 処理液

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- カタール

- アラブ首長国連邦

- ナイジェリア

- エジプト

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- BP PLC

- Carl Bechem Lubricants India Private Limited

- Chevron Corporation

- Exxon Mobil Corporation

- FUCHS

- Hindustan Petroleum Corporation Limited

- Indian Oil Corporation Ltd

- Kemipex

- SKF

- Motul

- PETRONAS Lubricants International

- TotalEnergies

- Saudi Arabian Oil Co.

第7章 市場機会と今後の動向

- 多相金属加工油剤の出現

- 技術の進歩

- その他の機会

目次

Product Code: 55158

The Metal Working Fluids Market size is estimated at 1.61 billion liters in 2025, and is expected to reach 1.73 billion liters by 2030, at a CAGR of 1.41% during the forecast period (2025-2030).

Key Highlights

- The growing demand from the automotive sector and the heavy machinery industry are the major factors driving the demand for metalworking fluids.

- However, the adoption of dry machining technologies and stringent environmental regulations are expected to hinder the market.

- Nevertheless, the emergence of multi-phase metal working fluids and advancements in technology are expected to create new opportunities for the market studied.

- Asia-Pacific dominates the market, with countries like China, India, and Japan being the biggest consumers.

Metal Working Fluids Market Trends

Growing Demand from the Automotive Sector

- Metalworking fluids are crucial in the automotive sector. They reduce friction between tools and workpieces, enhance surface quality, facilitate metal chip removal, and extend tool life. By boosting the efficiency of machining operations, these fluids contribute to heightened machine output.

- According to the Organisation Internationale des Constructeurs d'Automobiles (OICA), in 2023, around 93.55 million units of vehicles were produced worldwide, witnessing a growth rate of around 10.26% compared to 84.83 million units of vehicles in 2022, thereby indicating an increased demand for metalworking fluids from the automotive industry.

- The Asia-Oceania region emerged as the frontrunner in vehicle manufacturing, outpacing other regions. OICA data highlights that automotive production in this region reached 55.11 million units in 2023, up by 10.18% from 50.02 million units in 2022. Notably, this production is spearheaded by key players like China, Japan, South Korea, and India.

- According to the OICA (Organisation Internationale des Constructeurs d'Automobiles), in 2023, China solidified its position as the world's largest automotive production hub, churning out 30.16 million vehicles. This marks a notable 12% uptick from the 27.02 million units produced in 2022.

- Meanwhile, the United States solidified its position as the world's second-largest automotive manufacturer. The automotive sector stands as a cornerstone of the US economy, contributing between 3% and 3.5% to the nation's GDP in 2023. The United States is home to major automakers who not only meet domestic demands but also export vehicles to markets spanning the Americas, Europe, and the Asia-Pacific.

- The Organisation Internationale des Constructeurs d'Automobiles (OICA) reported that the United States produced 10.61 million units of vehicles in 2023, marking a 6% increase from the previous year.

- Europe witnessed a notable growth in motor vehicle production in 2023. Overall, production surged by 13% compared to the previous year. Specifically, passenger car and LCV production saw increases of 12% and 19%, culminating in 15.4 million units and 1.6 million units, respectively, in 2023.

- Given the expanding automotive industry, the demand for metalworking fluids is poised to rise during the forecast period.

Asia-Pacific to Witness the Fastest Growth

- Asia-Pacific leads the market, driven by rising demand from the automotive and heavy machinery and equipment sectors. Countries like China, India, and Japan are witnessing a surge in their heavy machinery industry, fueled by industrialization and economic growth.

- Metalworking fluids play a crucial role in manufacturing heavy machinery and equipment.

- The heavy machinery industry encompasses diverse sub-sectors, including machine tools, heavy electrical equipment, cement machinery, material handling, plastics processing, process plant equipment, and equipment for earth moving, construction, and mining.

- China's 14th Five-Year Plan aims to bolster its agricultural and rural transformation, which is directly related to the heightened use of heavy machinery in agriculture and construction.

- China's agricultural equipment sector has been on a steady upward trajectory, featuring close to 10,000 farming machinery firms and over 20,000 distribution entities. As highlighted by AgroPages in 2023, amidst 14 foreign trade sub-sectors, agricultural machinery exports showcased a robust 33.5% year-on-year surge, particularly in large and medium-sized tractors.

- Moreover, data from the China Construction Machinery Association (CCMA) indicates a 5.31% year-on-year rise in excavator sales, totaling 16,603 units in June 2024. Domestic sales reached 7,661 units, reflecting a strong 25.6% annual growth.

- India's agricultural equipment sector holds immense weight in the global arena, with numerous Indian manufacturers catering to both domestic and international markets. The Tractor Manufacturers Association reported a 19.24% dip in tractor sales in December 2023, with figures dropping from 55,390 units in 2022 to 44,735 units. However, overseas exports remained robust at 96,223 units in 2023, albeit down from 131,850 units in 2022.

- The Indian construction equipment industry experienced a 26% growth in the fiscal year 2023-24, largely due to the government's infrastructure-driven agenda. According to the Indian Construction Equipment Manufacturers' Association (ICEMA), 2023 sales reached 135,650 units, up from 107,779 units the previous year. Notably, earthmoving equipment sales, the industry's largest segment, rose by 21% to 93,531 units in FY 2023-24, constituting about 70% of the total sales.

- Passenger vehicle sales in India jumped 23% in the financial year 2023, as reported by the Federation of Automobile Dealers Associations. Leading manufacturers navigated intermittent supply chain challenges, particularly with semiconductors and electronics. Driven by rising disposable incomes, a wave of new sport-utility vehicles, and attractive loan rates, India's passenger vehicle sales touched 4 million units for the first time in FY 2023.

- According to the Society of Indian Automobile Manufacturers (SIAM), in 2023, sales of cars, sedans, and utility vehicles surpassed 4.1 million. This marks an 8.2% rise from the 3.79 million sold in 2022. The surge was predominantly fueled by utility vehicles, making up 57.4% of the total sales.

- Given these dynamics, Asia-Pacific is poised to lead the metalworking fluids market in the coming years.

Metal Working Fluids Industry Overview

The metal working fluids market is partially consolidated in nature. The major players (not in any particular order) include Exxon Mobil Corporation, FUCHS, TotalEnergies, BP PLC, and Chevron Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Growing Demand from the Automotive Sector

- 4.1.2 Increasing Demand from the Heavy Machinery Industry

- 4.1.3 Other Drivers

- 4.2 Market Restraints

- 4.2.1 Adoption of Dry Machining Technologies

- 4.2.2 Stringent Environmental Regulations

- 4.2.3 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Product Type

- 5.1.1 Removal Fluids

- 5.1.2 Forming Fluids

- 5.1.3 Protection Fluids

- 5.1.4 Treating Fluids

- 5.2 By Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Malaysia

- 5.2.1.6 Thailand

- 5.2.1.7 Indonesia

- 5.2.1.8 Vietnam

- 5.2.1.9 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 France

- 5.2.3.4 Italy

- 5.2.3.5 Spain

- 5.2.3.6 NORDIC Countries

- 5.2.3.7 Turkey

- 5.2.3.8 Russia

- 5.2.3.9 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 Qatar

- 5.2.5.3 United Arab Emirates

- 5.2.5.4 Nigeria

- 5.2.5.5 Egypt

- 5.2.5.6 South Africa

- 5.2.5.7 Rest of Middle East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BP PLC

- 6.4.2 Carl Bechem Lubricants India Private Limited

- 6.4.3 Chevron Corporation

- 6.4.4 Exxon Mobil Corporation

- 6.4.5 FUCHS

- 6.4.6 Hindustan Petroleum Corporation Limited

- 6.4.7 Indian Oil Corporation Ltd

- 6.4.8 Kemipex

- 6.4.9 SKF

- 6.4.10 Motul

- 6.4.11 PETRONAS Lubricants International

- 6.4.12 TotalEnergies

- 6.4.13 Saudi Arabian Oil Co.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emergence of Multi-phase Metal Working Fluids

- 7.2 Advancements in Technology

- 7.3 Other Opportunities

金属加工油剤:市場シェア分析、産業動向と統計、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日