|

市場調査レポート

商品コード

1640529

海底送電システム:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Submarine Electricity Transmission Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 海底送電システム:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

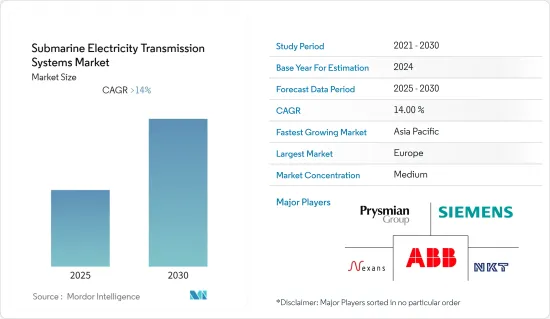

海底送電システム市場は、予測期間中に14%を超えるCAGRで推移すると予想されます。

COVID-19の大流行により、世界のエネルギー需要の急減がいくつかのプロジェクトを遅らせたため、市場はマイナスの影響を受けました。しかし、その後市場は回復し、予測期間中は安定した成長が見込まれます。

主なハイライト

- 長期的には、洋上風力発電コストの低下とともに、洋上風力発電容量のシェアが拡大している風力発電分野の成長が、海底送電システム市場を牽引すると予想されます。

- その反面、海底ケーブルに必要な保守・修理作業の頻度の高さとコストが、調査中の市場を抑制すると予想されます。

- とはいえ、プロジェクトの持続可能性を向上させ、海洋の生物多様性と生態系を保護するために、大規模な海底送電システムの環境への影響と設置面積を削減することは、予測期間以降も市場にとって大きなチャンスとなります。

- アジア太平洋地域は、同地域全体で電力消費が伸びており、市場を独占すると予想されます。

海底送電システム市場動向

HVDCシステムが大きな成長を遂げる

- 海底送電は、国家間の電力取引に注目が集まっていることから重要性を増しています。HVDC海底送電システムは、将来の送電網開発に不可欠と考えられています。長い海底距離を大電力で送電するための唯一のソリューションです。こうした理由から、HVDC送電線は世界中の洋上風力発電所を相互接続するのに好まれています。

- HVDC送電システムでは、海底送電ケーブルは、特にケーブルの静電容量が多くの追加充電電流を必要とする長いリンク上では、コストを低く抑えることができ、予測期間中の送電システム市場を促進します。

- GE Grid Solutionsによると、+-800kV UHVDCの場合、送電損失は5%未満で、送電路の幅はわずか50メートルと大幅に縮小されます。物理的な設置面積、インフラコスト、視覚的な影響は、従来の500kV交流トランスミッションと比べて大幅に減少します。

- マトリックスにおける再生可能エネルギーの割合が高まるにつれ、HVDCリンクの利用率も高まっています。例えば、ENTSOE-e(欧州電力トランスミッション運営者ネットワーク)によると、2012年以降の欧州における全HVDCリンクの年間利用率は57%から62%に増加しています。このことは、HVDCインフラに対する利用率と需要の高まりを浮き彫りにしており、予測期間中の市場の牽引役となることが期待されます。

- 2022年12月、Xlinks Morocco-UK Power ProjectはConergyから数百万ポンドの投資を受けました。このプロジェクトは、モロッコのGuelmim Oued Noun地域で発電された再生可能エネルギーを、世界最長となる3,800kmのHVDC海底ケーブル4本を通して輸出するものです。

- 同様に2022年7月、日立製作所はオーステッド社から、ホーンジー3洋上風力発電所からグリーン電力を送電する高電圧直流(HVDC)システム2基を受注したと発表しました。

- 洋上風力発電所の増加やHVDCケーブルによる各国間の相互接続などの要因により、予測期間中に海底送電システムの需要が増加すると予想されます。

アジア太平洋地域が市場を独占

- アジア太平洋地域が海底送電システム市場を独占すると予想され、中国が市場をリードし、ASEAN諸国がこれに続く。

- 中国政府は、公害を抑制し、火力発電の割合を減らすため、再生可能エネルギーのインフラ開発を積極的に推進しています。このことは、予測期間中、同国における風力発電プロジェクトの開発を促進すると思われます。洋上風力発電市場では、中国が世界のリーダーであり、2021年現在、中国の洋上風力発電設備容量は約2639万kWです。

- インドの洋上風力発電市場はまだ初期段階にあり、約60GWの潜在力があります。同国の洋上風力発電の潜在的な地域は、グジャラート州とタミル・ナードゥ州の海岸に位置しています。また、60GWの洋上風力発電のポテンシャルを持つインドは、2030年までに30GWの設置を目指しています。2022年11月、インドの新・再生可能エネルギー省(MNRE)は、2022年から23年にかけて4GW相当の洋上風力発電プロジェクトを行うため、タミル・ナードゥ州沖の海底をリースする入札案を発表しました。

- さらに、島国である日本やASEAN諸国は、島と島の間に大規模な送電設備を持っています。島国である日本には洋上風力発電に適した場所が多いです。同国は、洋上風力発電は陸上風力発電の5倍の発電量があると分析しています。

- また、フィリピンには7,500以上の島があり、そのうち2,000島に人が住んでいます。ASEAN諸国の大半は小さな島の集まりで構成されており、各島で発電することはできないです。そのため、島々の間を結ぶトランスミッションが必要となり、市場を牽引しています。

- 以上のことから、予測期間中、アジア太平洋地域が海底送電システム市場を独占すると予想されます。

海底送電システム産業概要

海底送電システム市場は適度に統合されています。同市場の主要企業(順不同)には、ABB Ltd、Siemens AG、Prysmian SpA、NKT AS、Nexans SAなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2027年までの市場規模および需要予測(単位:10億米ドル)

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 抑制要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- エンドユーザー別

- 洋上風力タービン

- 石油・ガス洋上プラットフォーム

- 国間および島間コネクター

- システムタイプ別

- HVDCシステム

- HVACシステム

- 地域別

- 北米

- 欧州

- アジア太平洋

- 南米

- 中東・アフリカ

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- ABB Ltd

- Sumitomo Electric Industries Ltd

- Siemens AG

- LS Cable & System

- Nexans SA

- NKT AS

- Norddeutsche Seekabelwerke GmbH(NSW)

- Prysmian SpA

- Furukawa Electric Co. Ltd

第7章 市場機会と今後の動向

The Submarine Electricity Transmission Systems Market is expected to register a CAGR of greater than 14% during the forecast period.

The market was negatively impacted by the Covid-19 pandemic, as plummeting global energy demand delayed several projects. However, the market has since rebounded and is expected to grow steadily during the forecast period.

Key Highlights

- Over the long term, the growth in the Wind Power Generation sector, which is witnessing an increasing share of the offshore wind generation capacity, along with the decrease in the cost of offshore wind power generation, is expected to drive the submarine electricity transmission systems market.

- On the flip side, the high frequency and costs of maintenance and repair work needed for submarine cables are expected to restrain the market being studied.

- Nevertheless, reducing the environmental impact and footprint of large submarine electricity transmission systems to improve project sustainability and protect marine biodiversity and ecosystems is a significant opportunity for the market beyond the forecast period.

- Asia-Pacific region is expected to dominate the market, with growing electricity consumption across the region.

Submarine Electricity Transmission Systems Market Trends

HVDC System to Witness Significant Growth

- Submarine electricity transmission is gaining importance because of the increasing focus on power trading between countries. The HVDC submarine power transmission system is considered critical for developing future power transmission networks. It is the only solution for transferring high power across long subsea distances. For these reasons, HVDC lines are preferred for interconnecting offshore wind plants worldwide.

- In the HVDC transmission system, the submarine power cables can be less costly, especially on a long link where the capacitance of the cable requires too much additional charging current, promulgating the transmission systems market during the forecast period.

- According to GE Grid Solutions, with an +-800 kV UHVDC, transmission losses are under 5%, and the width of the right-of-way is significantly reduced at only 50 meters. The physical footprint, infrastructure costs, and visual impact are decreased considerably compared to traditional 500 kV AC transmission systems.

- As shares of renewable energy in the matrix have risen, the utilization of HVDC links has grown. For instance, according to ENTSOE- e (European Network of Transmission System Operators for Electricity), the annual utilization of all HVDC links since 2012 has grown from 57% to 62% in Europe. This highlights the growing utilization and demand for HVDC infrastructure, which is expected to drive the market during the forecast period.

- In December 2022, The Xlinks Morocco-UK Power Project received a multi-million-pound investment from Conergy. The project will export renewable energy generated in Morocco's Guelmim Oued Noun region through four 3,800km HVDC subsea cables, which will be the longest in the world.

- Similarly, in July 2022, Hitachi announced it had won a major order from Orsted to provide two High-Voltage Direct Current (HVDC) systems to transmit green electricity from the Hornsea 3 Offshore wind farm.

- Factors, such as the increasing number of offshore wind farms along with interconnections between countries through HVDC cables, are expected to increase the demand for submarine transmission systems over the forecast period.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region is expected to dominate the submarine electricity transmission systems market, with China leading the market, followed by the ASEAN countries.

- The Chinese government is actively promoting the development of renewable infrastructure, to curb pollution, as well as to reduce the share of thermal power in the country's power generation profile. This is likely to drive the development of wind power projects in the country during the forecast period. In the offshore wind market, China is a global leader, as of 2021, China has nearly 26.390 GW of offshore wind energy installed capacity.

- The Indian offshore wind power market is still in its early stages and has a potential of around 60 GW. The potential areas of the country's offshore wind power are located on the coasts of Gujarat and Tamil Nadu. Besides, with an offshore wind potential of 60 GW, India aims to install 30 GW by 2030. In November 2022, India's Ministry of New and Renewable Energy (MNRE) issued a draft tender to lease seabed areas off Tamil Nadu for 4 GW equivalent offshore wind project capacity during 2022-23.

- Moreover, Japan and ASEAN countries being a group of island nations, has massive installations between the islands for power transmission. Japan, being an island nation, has many suitable locations for offshore wind power generation. The country analyzed that offshore wind turbines can generate five times more electricity than onshore wind turbines.

- Furthermore, the Philippines comprises of over 7,500 islands of which 2,000 islands are inhabited. The majority of the ASEAN countries consists of a cluster of small islands, where the power generation is not possible on each island. This creates a need for power transmission between the islands, hence driving the market.

- Owing to above points, Asia-Pacific is expected to dominate the Submarine Electricity Transmission Systems Market during the forecast period.

Submarine Electricity Transmission Systems Industry Overview

The Submarine Electricity Transmission Systems Market is moderately consolidated. Some of the key players in the market (not in particular order) include ABB Ltd, Siemens AG, Prysmian SpA, NKT AS, and Nexans SA, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2027

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 End User

- 5.1.1 Offshore Wind Turbines

- 5.1.2 Offshore Oil and Gas Platforms

- 5.1.3 Intercountry and Island Connectors

- 5.2 System Type

- 5.2.1 HVDC System

- 5.2.2 HVAC System

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 South America

- 5.3.5 Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 ABB Ltd

- 6.3.2 Sumitomo Electric Industries Ltd

- 6.3.3 Siemens AG

- 6.3.4 LS Cable & System

- 6.3.5 Nexans SA

- 6.3.6 NKT AS

- 6.3.7 Norddeutsche Seekabelwerke GmbH(NSW)

- 6.3.8 Prysmian SpA

- 6.3.9 Furukawa Electric Co. Ltd