|

市場調査レポート

商品コード

1640469

中東の潤滑油:市場シェア分析、産業動向、統計、成長予測(2025~2030年)Middle-East Lubricants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東の潤滑油:市場シェア分析、産業動向、統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

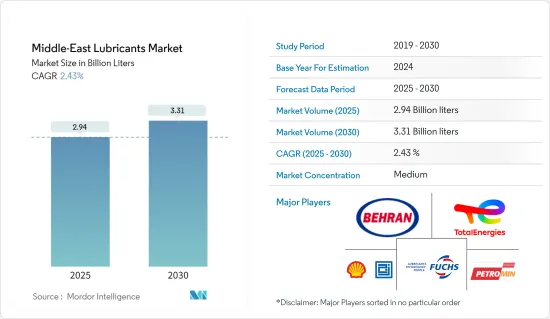

中東の潤滑油市場規模は2025年に29億4,000万リットルと推定され、予測期間(2025~2030年)のCAGRは2.43%で、2030年には33億1,000万リットルに達すると予測されます。

COVID-19の発生により、製造業は深刻な影響を受け、その結果2020年には潤滑油の使用量が減少しました。しかし、多くの建設プロジェクトやその他の産業活動の回復に伴い、2021年には市場は回復局面を迎えました。今後数年間はプラス基調で推移すると予想されます。自動車販売とエンジニアリング製品の増加が、過去2年間の市場回復を牽引してきました。

サウジアラビア、イラン、アラブ首長国連邦の産業成長と、高性能潤滑油の使用拡大が、調査対象市場の成長を増大させる主要原動力となっています。

その反面、高性能潤滑油のコスト高が市場成長の妨げになると予想されます。

合成潤滑油やバイオベースの潤滑油の開発は、将来的に市場の好機となると予測されます。

サウジアラビアは潤滑油の最大市場として浮上し、予測期間中に最も高いCAGRで推移すると予測されます。

中東の潤滑油市場動向

自動車セクターが市場を独占

- 潤滑油は通常、摩耗低減、腐食防止、エンジン内部のスムーズな動作確保などの用途に使用されます。

- 高燃費エンジンオイルは、オイル漏れ防止やオイルの焼き付き防止といった特殊な特性により、大きな需要があります。

- ほとんどの小型車と大型車のディーゼルエンジンとガソリンエンジンには10W40と15W40の粘度グレードのオイルが使用され、航空機エンジンには15W50と20W50のようなマルチグレードのオイルが一般的に使用されています。

- 自動車の平均車齢は、長年にわたって一定の割合で増加しており、これはアフターマーケット補充油市場にとって好機です。乗用車の平均年齢の上昇と新興国での都市人口の増加は、輸送用潤滑油市場を牽引すると予想されます。

- 自動車産業は、その国の社会経済の発展に不可欠です。現地の自動車産業の専門家によると、世界的に電気自動車の販売が伸びているにもかかわらず、サウジアラビアでは今後15~20年間は内燃機関車(ICE)が自動車の大半を占めると予想されています。

- サウジアラビアの自動車産業を支配している主要企業には、30%のシェアを持つToyota、26%のシェアを持つHyundaiとKIA、9%のシェアを持つRenault-Nissan-Mitsubishiなどがあります。General Motors、Ford、Fiat Chrysler Automobilesが残りのシェアを占めています。

- サウジアラビアは、同国の「ビジョン2030」の目標に沿って現地生産能力を開発するという自動車産業に関する国家戦略の目標を達成するため、自動車部門の現地化と投資機会の拡大を目指しています。

- イランの自動車市場は、過去にわたって上昇を確認しており、国内での生産需要が増加しています。例えば、OICAによると、イランの自動車生産台数は2022年に19%増加し、2021年の乗用車生産台数が約89万4,000台であったのに対し、2022年には106万4,000台となりました。

- 国際自動車工業会(通称OICA)は、2022年のイランの自動車生産台数の伸びを世界第6位としました。

- また、欧州自動車工業会(ACEA)は、2022年にイランを世界第11位の自動車メーカーにランク付けしました。

- アラブ首長国連邦の自動車市場は、生産と販売の需要が増加し、自動車登録台数が増加しています。

- 産業筋によると、2023年1月から9月までの同国の自動車登録台数は19万3,698台で、前年同期比20.2%増となりました。

- さらに、2022年の同国自動車市場の新車販売台数は40万台を超え、前年比10%増となりました。この成長は、同国の人口増加と所得の上昇に牽引され、今後も続くと予想されます。

- したがって、上記の要因は、予測期間中にこの地域で調査された市場の成長を増強すると予想されます。

サウジアラビアは急成長が期待される

- サウジアラビアは中東地域で最大の経済大国です。サウジアラビアの経済は主に石油産業に依存しています。

- サウジアラビアはGCC最大の自動車市場のひとつです。同地域の自動車市場の約80%を乗用車が占めています。

- サウジアラビアは、家庭用と商業用消費者からの電力需要の増加に効率的に対応し、国内のエネルギーミックスの多様化を支援するため、電力部門(発電、トランスミッション、配電、スマートグリッド)の能力を強化しています。

- エネルギー省によると、サウジアラビアの電力・再生可能エネルギープロジェクトへの支出は、2030年までに2,930億米ドルに達する見込みです。さらに2021年12月、サウジアラビアのエネルギー相は、2030年までにエネルギー配給に380億米ドルを支出する計画を発表しました。

- サウジアラビアは急速に成長するエネルギー消費国として浮上しました。同国における電力需要の増加に伴い、発電インフラも増加しています。同国では、増大する需要を満たすために、2040年までに発電能力を160GWまで増強する必要があると推定されています。これを達成するために、政府は発電に約50億米ドル、配電(D&T)に約40億米ドルの年間投資を計画しています。同国の再生可能エネルギー発電計画では、2023年までに再生可能エネルギーの発電量を950万kWに増やすことを目指しています。

- 一貫した潤滑は、ベアリング、ギア、チェーンの寿命に不可欠です。他の機械システムと同様、飲食品工場の可動部品が最適に機能するためには適切な潤滑が必要です。汚染、湿気、高温、湿度はすべて、ベアリング、チェーン、ギアの寿命を脅かすものです。サウジアラビアは金属産業に多額の投資を行っています。世界鉄鋼協会によると、2023年のサウジアラビアの粗鋼生産量は2022年比で約0.8%増加し、約990万トンの鉄鋼を生産しました。

- 2023年12月、サウジアラビア政府は、鉄鋼生産を増加させ、国内需要の大幅な増加に対応するため、鉄鋼プロジェクトに約120億米ドルを投資すると発表しました。プロジェクトの総生産能力は約620万トンとなる予定です。

- ネスレは、2025年に製造工場を設立し、3億7,500万SAR(9,972万米ドル)の初期投資を行い、その後、研究開発プログラムを備えた地域センターと、中小企業や新興企業のための初のビジネスインキュベーターを設立すると発表しました。

- 石油・ガス探査では、かなりの量の潤滑油が使用されます。これらの要因により、アラブ首長国連邦では予測期間中、市場が緩やかに牽引されると予想されます。

中東の潤滑油産業概要

中東の潤滑油市場はセグメント化されています。主要企業(順不同)には、TotalEnergies、Petromin、Aljomaih、Shell Lubricating Oil Company(JOSLOC)、Behran Oil Co.、FUCHSなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- サウジアラビア、イラン、アラブ首長国連邦における産業の成長

- 高性能潤滑油の利用拡大

- その他の促進要因

- 抑制要因

- 高性能潤滑油のコスト高

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 規制施策分析

第5章 市場セグメンテーション(市場規模(数量ベース))

- グループ

- グループI

- グループII

- グループIII

- グループIV(PAO)

- ナフテン

- ベースストック

- バイオベース潤滑油

- 鉱物油潤滑油

- 合成潤滑油

- 半合成潤滑油

- 製品タイプ

- エンジンオイル

- トランスミッション・油圧作動油

- 金属加工油

- 一般工業用オイル

- ギアオイル

- グリース

- プロセスオイル

- その他の製品タイプ(タービン油、冷凍機油、航空油、船舶油、変圧器油)

- エンドユーザー産業

- 発電

- 自動車とその他輸送機器

- 重機

- 飲食品

- 冶金・金属加工

- 化学製造

- その他のエンドユーザー産業(海洋、繊維、製造、石油・ガス)

- 地域

- サウジアラビア

- イラン

- イラク

- アラブ首長国連邦

- クウェート

- その他の中東

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Aljomaih And Shell Lubricating Oil Company Limited

- AMSOIL INC.

- Behran Oil Co.

- Emarat

- Exxon Mobil Corporation

- FUCHS

- GP Global MAG LLC

- GULF OIL Middle East Limited(Gulf Oil International Ltd.)

- Idemitsu Kosan Co., Ltd.

- IRANOL(LLP)

- Lubrex FZC

- Pars Oil Company

- Petromin

- Saudi Arabian Oil Co.

- Sepahan Oil Company

- TotalEnergies

第7章 市場機会と今後の動向

- 合成潤滑油とバイオベース潤滑油の開発

- その他の機会

The Middle-East Lubricants Market size is estimated at 2.94 billion liters in 2025, and is expected to reach 3.31 billion liters by 2030, at a CAGR of 2.43% during the forecast period (2025-2030).

Due to the COVID-19 outbreak, the manufacturing industry was severely affected, and this resulted in a decrease in the use of lubricants in 2020. However, with the recovery of many construction projects and other industrial activities, the market saw a recovery phase in the year 2021. It is expected to see a positive trend in the forecasted years. An increase in automotive sales and engineering goods has been leading the market recovery over the last two years.

The industrial growth in Saudi Arabia, Iran, and the United Arab Emirates and the growing usage of high-performance lubricants are the major driving factors augmenting the growth of the market studied.

On the flip side, costlier high-performance lubricants are expected to hinder the growth of the market.

Developments in synthetic and bio-based lubricants are projected to act as an opportunity for the market in the future.

Saudi Arabia emerged as the largest market for lubricants and is expected to register the highest CAGR during the forecast period.

Middle East Lubricants Market Trends

Automotive Sector to Dominate the Market

- Lubricants are typically used for applications such as wear reduction, corrosion protection, and ensuring smooth operation of the engine internals.

- High-mileage engine oils are experiencing great demand owing to specific properties, such as oil leak prevention and reduction in oil burn-off.

- Most light and heavy vehicle diesel and gasoline engines use 10W40 and 15W40 viscosity grade oils, while multi-grade oils, such as 15W50 and 20W50, are commonly used for aircraft engines.

- The average vehicle age has been increasing at a constant rate over the years, which is an opportunity in terms of the aftermarket refill market. The increasing average age of passenger cars and the growing urban population in developing countries is expected to drive the market for lubricants in transportation.

- The automotive industry is essential to the country's socio-economic development. According to some local automotive industry experts, despite the growing electric vehicle sales worldwide, Saudi Arabia expects internal combustible engines (ICE) vehicles to make up the majority of cars driven in for the next 15-20 years.

- Some of the major players controlling the automotive industry in the country include Toyota, with a 30% share, followed by Hyundai and KIA, with 26%, and Renault-Nissan-Mitsubishi, with 9%. General Motors, Ford, and Fiat Chrysler Automobiles comprise the remaining share.

- Saudi Arabia aims to localize the automotive sector and increase investment opportunities to achieve the national strategy's objectives for the industry in developing local manufacturing capabilities in line with the goals of the Kingdom's Vision 2030.

- The Iran automotive market has witnessed a rise over the historic period, with demand for production increasing in the country. For instance, according to the OICA, car manufacturing in Iran increased by 19% in 2022, as the country manufactured 1.064 million vehicles in 2022, while the passenger vehicles produced were around 894,000 units in 2021.

- The International Organization of Motor Vehicle Manufacturers (known as OICA) ranked Iran sixth in the world in terms of car manufacturing growth in 2022.

- Also, as per the European Automobile Manufacturers' Association (ACEA), the organization ranked Iran as the world's 11th largest automaker in 2022.

- The United Arab Emirates automotive market has been experiencing a rise in vehicle registrations over the current period, with demand in production and sales increasing in the country.

- As per industry sources, the country's automotive vehicle registration in the period January to September 2023 stood at 193,698, up 20.2% in comparison to the same period in the previous year.

- Moreover, in 2022, the country's car market sold over 400,000 new cars, representing a 10% increase over the previous year. This growth is expected to continue in the coming years, driven by the country's growing population and rising incomes.

- Thus, the factors above are expected to augment the growth of the market studied in the region during the forecast period.

Saudi Arabia is Expected to Experience a Surge in Growth

- Saudi Arabia is the largest economy in the Middle East region. Saudi Arabia's economy is mainly dependent on the oil industry.

- Saudi Arabia is one of the largest automotive markets in the GCC. Passenger cars account for approximately 80% of the region's automotive market.

- Saudi Arabia is enhancing the capacity of its power sector (electricity generation, transmission, distribution, and smart grid) to meet increasing demand efficiently from residential and commercial consumers for electricity and to support the diversification of its domestic energy mix.

- According to the Ministry of Energy, Saudi Arabia's spending on power and renewable energy projects is expected to reach USD 293 billion by 2030. Additionally, in December 2021, Saudi Arabia's Energy Minister announced the country's plan to spend USD 38 billion on energy distribution by 2030.

- Saudi Arabia emerged as a rapidly growing energy consumer. With the increasing demand for electricity in the country, the power generation infrastructure has been growing. It is estimated that the country is required to increase its power generation capacity to 160 GW by 2040 to fulfill its increasing demand. To achieve this, the government is planning to make an annual investment of around USD 5 billion in generation and USD 4 billion in distribution (D&T). The National Renewable Energy Program in the country aims to increase the generation of renewable energy to 9.5 GW by 2023.

- Consistent lubrication is vital to the life of bearings, gears, and chains. Like any mechanical system, moving parts in a food and beverage plant need proper lubrication to function optimally. Contamination, moisture, high temperatures, and humidity are all threats to bearing, chain, and gear service life. Saudi Arabia is heavily investing in metal industries. According to the World Steel Association, Saudi Arabia's crude steel production in 2023 observed an increase of about 0.8% as compared to 2022 and produced approximately 9.9 million metric tons of steel.

- In December 2023, the Saudi Arabian government announced to investment of about USD 12 billion in steel projects to increase steel production and meet the significant growth in domestic demand. The project is planned to have a total production capacity of about 6.2 million tons.

- Nestle has announced an initial investment of SAR 375 million (USD 99.72 million) with the establishment of a manufacturing plant in 2025, followed by a regional center with a research and development program and its first business incubator for small and medium-sized companies and start-ups.

- A significant amount of lubricants are used in oil and gas exploration. These factors are expected to drive the market slowly over the forecast period in the United Arab Emirates.

Middle East Lubricants Industry Overview

The Middle-East lubricants market is fragmented. The major companies (in no particular order) include TotalEnergies, Petromin, Aljomaih, Shell Lubricating Oil Company (JOSLOC), Behran Oil Co., and FUCHS, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Industrial Growth in Saudi Arabia, Iran, and the United Arab Emirates

- 4.1.2 Growing Usage of High-performance Lubricants

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Costlier High Performance Lubricants

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Regulatory Policy Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Group

- 5.1.1 Group I

- 5.1.2 Group II

- 5.1.3 Group III

- 5.1.4 Group IV (PAO)

- 5.1.5 Naphthenics

- 5.2 Base Stock

- 5.2.1 Bio-based Lubricant

- 5.2.2 Mineral Oil Lubricant

- 5.2.3 Synthetic Lubricant

- 5.2.4 Semi-synthetic Lubricant

- 5.3 Product Type

- 5.3.1 Engine Oil

- 5.3.2 Transmission and Hydraulic Fluid

- 5.3.3 Metalworking Fluid

- 5.3.4 General Industrial Oil

- 5.3.5 Gear Oil

- 5.3.6 Greases

- 5.3.7 Process oils

- 5.3.8 Other Product Types (Turbine oils, Refrigeration oils, Aviation oils, Marine oils, and Transformer oils)

- 5.4 End-user Industry

- 5.4.1 Power Generation

- 5.4.2 Automotive and Other Transportation

- 5.4.3 Heavy Equipment

- 5.4.4 Food and Beverage

- 5.4.5 Metallurgy and Metalworking

- 5.4.6 Chemical Manufacturing

- 5.4.7 Other End-user Industries (Marine, Textiles, Manufacturing, and Oil and gas)

- 5.5 Geography

- 5.5.1 Saudi Arabia

- 5.5.2 Iran

- 5.5.3 Iraq

- 5.5.4 United Arab Emirates

- 5.5.5 Kuwait

- 5.5.6 Rest of Middle-East

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aljomaih And Shell Lubricating Oil Company Limited

- 6.4.2 AMSOIL INC.

- 6.4.3 Behran Oil Co.

- 6.4.4 Emarat

- 6.4.5 Exxon Mobil Corporation

- 6.4.6 FUCHS

- 6.4.7 GP Global MAG LLC

- 6.4.8 GULF OIL Middle East Limited (Gulf Oil International Ltd.)

- 6.4.9 Idemitsu Kosan Co., Ltd.

- 6.4.10 IRANOL (LLP)

- 6.4.11 Lubrex FZC

- 6.4.12 Pars Oil Company

- 6.4.13 Petromin

- 6.4.14 Saudi Arabian Oil Co.

- 6.4.15 Sepahan Oil Company

- 6.4.16 TotalEnergies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Developments in Synthetic and Bio-based Lubricants

- 7.2 Other Opportunities