油田通信-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Oilfield Communications - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1640464

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

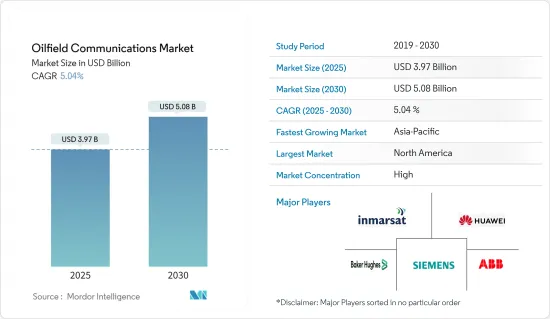

油田通信市場規模は2025年に39億7,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは5.04%で、2030年には50億8,000万米ドルに達すると予測されます。

油田通信市場は、機械学習、人工知能、コグニティブインテリジェンス、クラウドなどの最先端技術が急激に拡大し、広く受け入れられていることが背景にあり、一貫した通信に依存する油田のミッションクリティカルな活動には信頼性の高いハードウェアが必要であるため、ネットワークインフラを改善するための投資が増加しています。

主要ハイライト

- GCCのようないくつかの国では、通信インフラのアップグレードに多額の投資を行っています。企業は、コグニティブ(認知)技術や人工知能(AI)技術と自動化を融合させることで、ビジネスプロセスの能力を急速に拡大しています。インフラは、スタッフの福利厚生、リソース管理、ネットワーク接続性、安全衛生規制の改善に役立ちます。

- こうした利点が、野心的なデジタルトランスフォーメーションの野望をサポートするためにネットワーク通信への投資を増加させており、これが油田通信製品の需要を押し上げ、産業の拡大を予見しています。

- また、石油・ガス産業では、クラウドベースの最新技術の採用が増加しており、市場の成長を後押ししています。これらのサービスは、より優れたリアルタイムデータ、インフラコストの柔軟性、データ管理とストレージの拡大性を記載しています。生産ユニット、油井、油田のメンテナンスとモニタリングは、コンピューティングサービスなどのクラウドベースの技術によって可能になった魅力的なオプションです。企業は資産をデジタル化し、データ処理を分散化し、運用のためのSaaSソリューションを展開するために、エッジサービスとクラウドサービスに依存し、変革しています。最先端の画期的な技術により、クラウドソリューションは、斬新でエキサイティングな油田オプションの豊富さを変革し、切り開くことができます。

- エネルギーセグメントでは、クラウドプラットフォームが提供する高いコンピューティング能力により、クラウドベースのサービス機能が大量に利用されており、物理的資産のインテリジェントな管理など、他の技術の採用も促進し、業務効率の向上を促しています。そのため、石油・ガス産業ではクラウドベースの最新技術の採用が進んでおり、油田通信のニーズが高まると予想されます。

- 石油は限られた資源であり、賞味期限も短いです。また、油田通信の需給の変化や地政学的な出来事により、石油価格は長年にわたって変動しています。地球科学者たちは、常に新しい石油源を見つけ、未発見の埋蔵量を調査することに取り組んでいます。その一方で、研究者たちは非伝統的エネルギー源にも目を向けています。コロナウイルスが発生した時点で、油田通信の需要や市場の将来動向は凋落していました。このまま数年間、状況が悪化すれば、市場は悲惨なことになります。

油田通信市場の動向

クラウドベースのサービス採用が市場成長を牽引

- クラウドベースのサービスの採用が進むにつれ、石油会社は油田通信を利用せざるを得なくなっています。これにより、オフショアサイトとインショアサイトが生産統計について接続され、より良いサプライチェーン管理に役立っています。石油会社にとって、資材のスムーズな流れは非常に重要です。収益性は回転率に大きく左右されるため、ダウンタイムは避けなければならないです。

- 例えば、石油・ガス会社にサービスを提供するGE石油・ガスは、過去2年半の間に350のアプリケーションをAmazonのクラウドサービスであるAWSに移行しました。GEは、エンタープライズアプリケーションをクラウドシステムで運用することで、総所有コストを平均52%削減できることを発見しました。これは、このセグメントで最も先進的な企業における支配的な動向です。

- SiemensAGによると、データによるソリューションは、効率性の向上とコスト削減の面で大きな利益をもたらすといわれています。Siemensによると、デジタル化によってバレルあたりのブレント価格コストを45%削減できる一方、上流の資本コスト指数を25%、操業コスト指数を18%削減できるといいます。

- クラウド技術は、以前はその採用を抑制していたセキュリティ上の懸念に効果的に対処しており、その結果、時代遅れのオンプレミスシステムに革命を起こす透明性を備えた先駆的企業が報われることになりました。

北米が主要シェアを占める

- 北米はこの市場のパイオニアであり、最大の石油・ガス産出国であるため、大きなシェアを占めると予想されます。北米では、オンショアと海上での油田操業のために先進的なデジタル通信ソリューションを求める企業が多いです。

- 産油企業の多くは米国に本社を置いています。ほとんどの企業は、世界の立ち上げや展開の前に、国内で新しいサービスを検査的に導入しています。

- この国の新技術導入の速さと、世界の通信への関心の高まりが、市場を押し上げます。

- さらに、新たに発見されたシェール資源と、OCSによって承認された大陸棚外リースプログラムによる探査・生産活動の急速な増加により、この地域は予測期間中、油田通信の最も急成長する市場の1つになると予想されます。

油田通信産業概要

油田通信市場には、全領域のソリューションを提供する大手企業が数社あります。主要参入企業には、SiemensAG、ABB Ltd、Huawei Technologies、Baker Hughes(General Electric Company)、Inmarsat PLC、Speedcast International Limitedなどがあります。M&Aは市場の主要成長戦略のひとつであり、この産業の競合学を変化させ、新製品開発の機会を増やすと予想されます。

2022年7月、Baker Hughesは、人工リフトソリューションの最先端技術サプライヤーの1つであるAccessESPを買収すると発表しました。AccessESPの「GoRigless ESP System」は、リグを使用したり、ワイヤライン、コイルドチュービング、坑井トラクターなどの坑井生産管を引っ張ったりする代わりに、一般的な軽量介入ツールを使用して電気水中ポンプ(ESP)の設置や解体を可能にする独自のソリューションを提供しています。オフショアや遠隔地の状況でますます重要になっているESPの交換作業の重要性は、コストとダウンタイムの面で、これらのソリューションによって大幅に削減されます。

2022年5月、リグの訪問回数を減らすことで坑井ヘッドの総設置コストを削減するため、米国を拠点とする油田通信事業のBaker Hughesは、MS-2アニュラス・シールと呼ばれる斬新な海底坑井ヘッド技術を発表しました。2022年にヒューストンで開催されたオフショア技術会議では、北米と南米の複数の顧客がこの統合シールシステムを発表、展示、採用しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- クラウドベースのサービスの採用拡大

- 地理的課題により、油田の回復と生産性向上のためのデジタル通信への依存度が高まる

- 効果的な通信技術の開発と採用

- 市場抑制要因

- 厳しい規制枠組みと不十分なデータ資産セキュリティのリスク増大

第6章 市場セグメンテーション

- ソリューション別

- M2M通信

- ユニファイド通信(UC)ソリューション

- ビデオ会議

- VoIP

- 有線/無線インカム

- その他のソリューション

- 通信ネットワーク別

- セルラー通信ネットワーク

- VSAT通信ネットワーク

- 光ファイバー通信ネットワーク

- マイクロ波通信ネットワーク

- テトラネットワーク

- サイト別

- オンショア通信

- オフショア通信

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- その他の欧州

- アジア太平洋

- 中国

- 日本

- その他のアジア太平洋

- ラテンアメリカ

- メキシコ

- ブラジル

- その他のラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- その他の中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Huawei Technologies Co. Ltd.

- Siemens AG

- Speedcast International Limited

- ABB Ltd.

- Commscope, Inc.

- Inmarsat PLC(Triton Bidco)

- Tait Communications

- Baker Hughes(General Electric Company)

- Alcatel-Lucent France, S.A.

- Ceragon Networks Ltd.

- Rad Data Communications, Inc.

- Rignet, Inc.

- Hughes Network Systems LLC

- Airspan Networks, Inc.

- Commtel Networks Pvt. Ltd.

第8章 投資分析

第9章 市場機会と今後の動向

目次

The Oilfield Communications Market size is estimated at USD 3.97 billion in 2025, and is expected to reach USD 5.08 billion by 2030, at a CAGR of 5.04% during the forecast period (2025-2030).

The oilfield communication market is being driven by the exponential expansion and widespread acceptance of cutting-edge technologies like machine learning, artificial intelligence, cognitive intelligence, and cloud, owing to the rising investment in improving network infrastructure as dependable hardware is needed for mission-critical activities in the oilfields, which depend on consistent communication.

Key Highlights

- Several nations, like the GCC, have significantly invested in upgrading their telecommunications infrastructure. Companies are quickly expanding the capabilities of business processes by fusing automation with cognitive and artificial intelligence (AI) technology. The infrastructure helps to improve staff welfare, resource management, network connectivity, and health and safety regulations.

- These advantages are driving up investments in network communication to support their ambitious digital transformation ambitions, which is driving up demand for oilfield communications products and has foreseen the industry's expansion.

- Additionally, the rising adoption of contemporary cloud-based technologies in the oil and gas industry propels market growth. These services provide better real-time data, more flexibility in infrastructure costs, and the capacity to scale data management and storage. Maintenance and monitoring of production units, wells, and oilfields are now appealing options made possible by cloud-based technologies, such as computing services. Businesses are transforming and relying on edge and cloud services to digitalize their assets, decentralize data processing, and deploy SaaS solutions for operations. With cutting-edge breakthrough technology, cloud solutions can transform and open up a wealth of novel and exciting oilfield options.

- A significant amount of cloud-based service capabilities are being used in the energy sector due to the high computing power made available by cloud platforms, which also encourages the adoption of other technologies like the intelligent management of physical assets and promotes greater operational efficiency. Therefore, the oil and gas industry's growing embrace of contemporary cloud-based technology is anticipated to drive the need for oilfield communications.

- Oil is a limited resource that has a little shelf life. Oil prices have also fluctuated throughout the years because of shifting supply and demand for oilfield communication and geopolitical events. Geoscientists are constantly working to find new oil sources and investigate undiscovered reserves. On the other hand, researchers are looking at non-traditional energy sources nonstop. At the coronavirus outbreak, the demand for oilfield communications and market future trends were waning. It will be disastrous for the market if the situation worsens for several years.

Oilfield Communications Market Trends

Growing Adoption of Cloud-based Services to Drive the Market Growth

- With the growing adoption of cloud-based services, oil companies are compelled to use oil field communication. This keeps their offshore sites connected with the inshore site about production stats, which helps in better supply chain management. The smooth flow of materials is very important for oil companies as their profitability is highly dependent upon the turnover, and downtime needs to be avoided.

- For instance, over the past two and a half years, GE Oil & Gas, the service provider to oil and gas companies, has shifted 350 of its applications to Amazon's cloud offering, AWS. GE found that the total cost of ownership of running its enterprise applications on the cloud systems provided a saving of 52% on average. This is the dominant trend in the sector's most progressive companies.

- According to Siemens AG, data-based solutions will lead to huge gains in terms of efficiency gains and cost savings. According to Siemens, digitization can reduce Brent price cost per barrel by 45% while reducing the upstream capital cost index and operations cost index by 25% and 18%, respectively.

- Cloud technology has effectively addressed security concerns that previously restrained its adoption, thereby rewarding pioneering companies with the transparency to revolutionize their outdated on-premise systems.

North America to Account for a Major Share

- North America is the pioneer in this market and is expected to hold a significant share as it is the largest oil and gas producer, with companies seeking advanced digital communication solutions for their onshore and offshore field operations.

- Many oil-producing companies are headquartered in the United States. Most companies pilot new services in the country before global launches and deployment.

- This country's fast adoption of new technology and the growing focus on global communication push the market forward.

- Moreover, with newfound shale resources and rapidly increasing exploration and production activities due to the Outer Continental Shelf Leasing Program approved by OCS, the region is expected to be one of the fastest-growing markets for oilfield communications over the forecast period.

Oilfield Communications Industry Overview

The oilfield communications market has a few major players who provide the entire spectrum of solutions. The major players include Siemens AG, ABB Ltd, Huawei Technologies Co. Ltd, Baker Hughes (General Electric Company), Inmarsat PLC, and Speedcast International Limited. Merger and Acquisition are expected to be one of the key growth strategies of the market, which will change the dynamics of competition in this industry and increase opportunities for new product development.

In July 2022, Baker Hughes announced it would acquire AccessESP, one of the top cutting-edge technology suppliers for artificial lift solutions. Oil and gas operations might be modernized by cutting operational expenses and downtime and becoming considerably more productive.AccessESP's "GoRigless ESP System" offers its unique solutions that enable the installation and dismantling of an electrical submersible pump (ESP) using common, light-duty intervention tools instead of a rig or pulling well production tubings, such as a wireline, coiled tubing, or well tractors. The importance of ESP replacement workovers, which are becoming increasingly crucial in offshore and remote situations, is considerably reduced by these solutions in terms of cost and downtime.

In May 2022, to reduce total wellhead installation costs due to fewer rig visits, Baker Hughes, a US-based oilfield communications business, introduced a novel subsea wellhead technology called the MS-2 Annulus Seal. At the offshore technology conference in Houston in 2022, several clients in North and South America presented, displayed, and adopted this integrated sealing system.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers/Consumers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Adoption of Cloud-based Services

- 5.1.2 Geographically Challenging Locations will Increase Reliance on Digital Communication for Oilfield Recovery and Productivity

- 5.1.3 Development and Adoption of Effective Communication Technologies

- 5.2 Market Restraints

- 5.2.1 Stringent Regulatory Framework and the Rising Risk of Inadequate Data and Asset security

6 MARKET SEGMENTATION

- 6.1 By Solution

- 6.1.1 M2M Communication

- 6.1.2 Unified Communication Solutions

- 6.1.3 Video Conferencing

- 6.1.4 VoIP

- 6.1.5 Wired/Wireless Intercom

- 6.1.6 Other Solutions

- 6.2 By Communication Network

- 6.2.1 Cellular Communication Network

- 6.2.2 VSAT Communication Network

- 6.2.3 Fiber Optic-Based Communication Network

- 6.2.4 Microwave Communication Network

- 6.2.5 Tetra Network

- 6.3 By Field Site

- 6.3.1 Onshore Communications

- 6.3.2 Offshore Communications

- 6.4 Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.4.1 Mexico

- 6.4.4.2 Brazil

- 6.4.4.3 Rest of Latin America

- 6.4.5 Middle East & Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 Rest of Middle-East & Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Huawei Technologies Co. Ltd.

- 7.1.2 Siemens AG

- 7.1.3 Speedcast International Limited

- 7.1.4 ABB Ltd.

- 7.1.5 Commscope, Inc.

- 7.1.6 Inmarsat PLC (Triton Bidco)

- 7.1.7 Tait Communications

- 7.1.8 Baker Hughes (General Electric Company)

- 7.1.9 Alcatel-Lucent France, S.A.

- 7.1.10 Ceragon Networks Ltd.

- 7.1.11 Rad Data Communications, Inc.

- 7.1.12 Rignet, Inc.

- 7.1.13 Hughes Network Systems LLC

- 7.1.14 Airspan Networks, Inc.

- 7.1.15 Commtel Networks Pvt. Ltd.

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日