|

市場調査レポート

商品コード

1640357

アジア太平洋の医薬品包装:市場シェア分析、産業動向、成長予測(2025~2030年)Asia Pacific Pharmaceutical Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋の医薬品包装:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

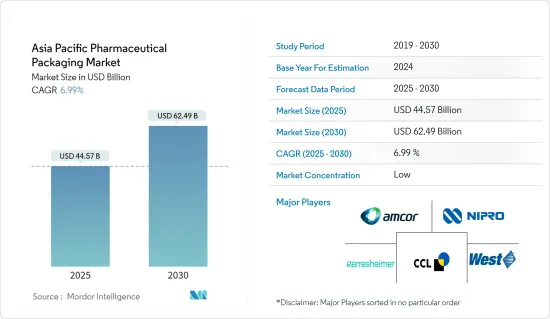

アジア太平洋の医薬品包装市場規模は2025年に445億7,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは6.99%で、2030年には624億9,000万米ドルに達すると予測されています。

主要ハイライト

- 医薬品包装は、安全で効果的な医薬品を封入、維持、保護、流通させるために必要な要素の集合体であり、医薬品の有効期限前であればいつでも安全で効果的な剤形にアクセスできることを保証します。適切な包装材料は、偽造医薬品の消費を抑止するのに役立つ、改ざんを防止する安全性を提供するために不可欠です。さらに、高級包装材は厳格な規制ガイドラインに準拠しなければならないです。

- 医薬品包装メーカーは、医薬品セクターへの投資の増加により、アジア太平洋で大きなビジネス機会を目の当たりにすると予想されています。医薬品需要の高まりと製薬技術の先進化は、ガラス瓶、アンプル、その他のガラス包装ソリューションの需要に直接貢献しています。慢性疾患が増加し続け、COVID-19ワクチンの生産量が依然として多いため、一次包装、特にガラス容器の需要が急増すると予想されます。

- この地域の医薬品包装セグメントでは、ガラス製包装が市場の成長を牽引すると期待されています。製薬会社はガラス容器を利用して、注射薬、経口固形剤、液体製剤、生物製剤など多様な医薬品を包装しています。ガラス製容器包装の急成長の背景には、医薬品製造事業、特殊医薬品の需要増加、医療インフラの拡大といった要因があります。この動向は特に中国、インド、日本、韓国といった国々で顕著であり、製薬産業は著しい成長を遂げているため、ガラス製包装ソリューションの需要が急増しています。

- プラスチックボトル産業は今後数年で大幅な成長を遂げると予測されています。この地域ではPETの利用が着実に増加しており、その結果、ガラスに比べて最大90%の軽量化が実現し、より費用対効果の高い輸送が可能になります。現在、PETから作られたプラスチックボトルは、医薬品セグメントでかさばりデリケートなガラスボトルに取って代わり、さまざまな液体の再利用可能な包装を提供しています。製薬産業におけるプラスチックPET技術の進歩は、市場展望を押し上げると予想されます。

- さらに、この地域の製薬セクターを強化するための政府の取り組みが、市場の拡大を促進すると予想されています。例えば、国の医療システムの近代化を促進するために中国政府によって実施された措置は、医薬品包装産業の進歩を刺激すると予測されています。さらに、中国は医薬品包装のインフラやリソースを積極的に改善する一方、医薬品タイプを増やしており、医薬品包装企業に新たな道を開く可能性があります。

- 世界の医薬品市場における中国の存在感は着実に高まっており、主要な消費国であると同時に、世界の医薬品産業とサプライチェーンの重要なコンポーネントとしての役割を果たしています。科学技術の進歩に牽引された近年の医薬品セクターの急拡大は、今後も続くと予測されています。2023年12月、デンマークの製薬会社ノボ・ノルディスクは、2026年6月までに同地域の新設会社に4億人民元(5,960万米ドル)を投資する計画を明らかにしました。こうした実質的な開発は、医薬品包装サービスの需要を促進すると予想されます。

- 包装産業はCOVID-19の大流行により大きな影響を受けました。感染症やワクチンに重点が移されたことで、糖尿病や高血圧などの治療領域で成功した臨床検査や研究開発活動は減少しました。しかし、製薬産業はパンデミックの間、様々な疾患に対する医薬品需要の急増を目の当たりにし、包装事業への多額の投資につながりました。幸い、製薬産業はパンデミックに対応して安全で衛生的な包装の必要性を強調することで、すぐに回復しました。

アジア太平洋の医薬品包装市場の動向

ガラス製包装が大きな成長を遂げる見込み

- ガラス包装は、包装産業において医薬品の主要な選択肢であると広く考えられています。その人気の理由は、サステイナブル性質、不活性、不浸透性、リサイクル性、品質を損なうことなく再利用できる能力にあります。COVID-19のパンデミックは、投薬の必要性が大幅に増加したため、ガラス包装の需要をさらに煽った。各国の製薬メーカーによる新薬やワクチンの承認と流通に伴い、ガラス包装の使用は拡大し続けると予想されます。

- ガラス包装は主に医薬品の主要包装オプションとして提供されており、製薬産業ではトップクラスの選択肢となっています。その主要理由は、持続可能性、不活性、不浸透性、品質を損なうことなくリサイクル可能、再利用可能などの利点があるからです。ガラス容器は、主要な包装材料の一つとして医薬品セグメントで広く利用されるようになっています。慢性疾患の流行が増加し、COVID-19ワクチンの生産量が増加し続けるにつれて、一次包装、特にガラス容器の需要が急増すると予想されます。

- アジア太平洋における慢性疾患の有病率の増加は、医薬品包装市場の拡大を促進する主要要因です。糖尿病、心血管疾患、がん、呼吸器疾患などの疾患は継続的な投薬が必要です。その結果、これらの医薬品を安全に保管、保護し、最適な効率で流通させるための多様な医薬品包装ソリューションに対するニーズが高まっています。世界保健機関(WHO)によると、非伝染性疾患の増加がこの地域、特に中東・アフリカの慢性疾患の負担増に寄与しています。

- 一次包装ガラスソリューションメーカーのStoelzleは、2023年11月に開催されたCPHIバルセロナ見本市で、環境に優しい最新のPharmaCosラインを発表しました。この包装ソリューションの新ラインは、リサイクルガラスの割合が高く(アンバーガラスで73%、フリントガラスで38%)、軽量なボトルデザインを誇っています。さらに、この新ラインは医療産業の厳しい基準を満たすため、医薬品グレードの施設で生産されています。ベンダーによるこのような重要なイノベーションは、市場の成長を促進すると予想されます。

- Bormioli Pharmaによると、現在、タイプIIとタイプIIIのガラス用に特別に設計された様々な再生ガラス製品が販売されています。これらの製品は、医薬用として認証された外部のサプライチェーンから調達した材料を利用しています。化学的・機械的処理により、再生材料は新しい生産サイクルの基礎となるガラス粉末に変換されます。同時に、ボルミオリファーマは低排出ガス炉の開発プロジェクトにも積極的に取り組んでいます。これらの炉は、環境フットプリントを最小限に抑える革新的な技術と工業プロセスを取り入れています。

- さらに、日本のような国々におけるガラス包装技術の市場は、医薬品ベンダーが医薬品生産を強化するために行う投資の増加によって牽引されるであると考えられます。顕著な例としては、Takedaが2023年3月に発表した、大阪に血漿由来治療(PDT)の新しい製造施設を建設するために約1,000億円(7億5,000万米ドル)を投資する計画があります。今回の投資は、Takedaにとって、日本における過去最大規模の生産能力増強となります。2030年までの稼働を予定しているこの最新鋭施設は、この種の施設としては国内最大となり、Takedaの血漿製造能力を大幅に増強することになります。

著しい成長が期待されるインド

- インドは医薬品包装市場において最も急成長している地域のひとつであると予想されています。医薬品包装セグメントは、技術革新と新しい治療の台頭により、近年著しい成長を遂げています。COVID-19パンデミックの発生は、効率的な製品包装と流通の重要性を浮き彫りにしました。その結果、包装を含む製造と流通の両プロセスを加速させることが重視されるようになっています。その結果、包装企業は迅速な技術革新を迫られるようになり、より迅速なオペレーションを求める声が高まっている

- インドは、特にジェネリック医薬品や費用対効果の高い医薬品の生産において、医薬品セクターの主要企業として台頭してくると予想されます。同国は、多くの先進国へのジェネリック医薬品の主要供給国として重要な役割を果たしています。ジェネリック医薬品の生産量の増加と国際的な流通は、インドの医薬品包装産業の拡大を促進する重要な要因です。さらに、慢性疾患の急増と医薬品製造事業への投資の増加は、市場内の需要の大幅な増加につながります。

- 同地域では、プラスチック包装タイプの需要が顕著に増加すると予想されます。医療用品や医薬品に対するニーズの急増が、インドにおけるプラスチック製医薬品包装の拡大を後押ししています。この地域の市場ポテンシャルを高めるため、数多くの企業がこの技術に多額の投資を行っています。例えば、2023年3月、スペインの包装会社Inden Pharmaは、医薬品用プラスチック包装を専門とするオーストリアのALPLApharmaとの提携を通じて、インドでの事業拡大を意図しています。こうした注目すべき進歩が市場の成長を促すと予測されています。

- InvestIndiaの報告によると、インドは世界最大のジェネリック医薬品供給国であり、世界供給量の20%を占めています。さらに、インドは世界最大のワクチン生産国でもあります。米国以外では、米国食品医薬品局(US FDA)の定める基準に準拠した製薬工場の数が最も多いのもインドです。3,000社を超える製薬会社と1万0,500を超える製造施設を擁するインドは、製薬産業において強固なネットワークと先進的技能を有する労働力を有しています。さらに、インドは世界のワクチン需要の約60%を満たしており、DPT、BCG、麻疹ワクチンの主要供給国でもあります。医薬品製造におけるこうした幅広い能力は、間違いなく同地域の包装ビジネス市場を刺激すると考えられます。

- さらに、InvestIndiaによると、インドの製薬産業は、主に輸出の増加と国内市場の成長により、2018年度から22年度にかけて平均成長率9.47%を記録し、423億4,000万米ドルに達しました。予測によると、医薬品部門は2024年に650億米ドル、2030年には1,200億米ドルに達する見込みです。持続的な成長を確保するため、政府は研究と技術革新を促進するさまざまなイニシアチブを実施しています。2047年に向けたビジョンの一環として、政府は、Vasudhaiva Kutumbakamの原則に沿って、インドを、手頃な価格で革新的かつ高品質の医薬品・医療機器の生産における世界的リーダーとして確立することを目指しています。このような重要な開発は、包装セグメントに市場開拓の機会をもたらすと考えられます。

アジア太平洋の医薬品包装産業概要

アジア太平洋の医薬品包装市場は競争が激しく、多くの地域と世界参入企業が存在します。主要参入企業としては、Amcor Ltd.、West Pharmaceutical Services Inc.、CCL Industries Inc.、NIPRO Corporationなどが挙げられます。各社は新製品を発売し、生産部門を拡大することで市場シェアを伸ばしています。最近の動向をいくつか発表します。

- 2024年1月、100%再生ポリエチレンテレフタレート(「PET」)樹脂とポリエステル繊維を製造し、循環型プラスチック経済を加速することを使命とするクリーン技術企業、Loop Industries Inc.と、医薬品包装と医療機器の国際的参入企業であるBormioli Pharmaは、100%再生バージン品質のループPET樹脂で製造された革新的な医薬品包装ボトルを発売しました。

- 2023年6月、CIncorporatedはSGD Pharmaと提携し、テランガナ州に医薬品包装用ガラスを製造する最新鋭施設を設立。この施設の設立には、両社で合わせて50億インドルピー以上を投資すると報告されています。今回のコーニング社との提携は、製薬産業におけるコンバーティング技術の向上と、強固なサプライチェーンの確保に向けた重要な一歩です。両社が協力することで、製薬メーカーが生産能力や品質に関する増大する課題に対処し、必要不可欠な医薬品に対する世界の需要の高まりに対応できるよう支援することを目指しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 市場促進要因

- 新興国における医薬品包装の採用増加

- 市場抑制要因

- 原料コストの変動

第5章 市場セグメンテーション

- 材料別

- プラスチック

- 紙・板紙

- ガラス

- アルミ箔

- タイプ別

- アンプル

- ブリスターパック

- プラスチックボトル

- シリンジ

- バイアル

- 輸液

- その他

- ドラッグデリバリーモード別

- 経口薬包装

- 注射剤包装

- 肺用薬剤包装

- その他

- 国別

- インド

- 日本

- 中国

- オーストラリア

- その他のアジア太平洋

第6章 競合情勢

- 企業プロファイル

- Amcor Ltd

- CCL Industries Inc.

- West Pharmaceutical Services Inc.

- Gerresheimer AG

- Schott AG

- NIPRO Corporation

- Wihuri Group

- Klockner Pentaplast Group

- Catalent Pharma Solutions Inc.

- Berry Global Group Inc.

第7章 投資分析

第8章 市場の将来

The Asia Pacific Pharmaceutical Packaging Market size is estimated at USD 44.57 billion in 2025, and is expected to reach USD 62.49 billion by 2030, at a CAGR of 6.99% during the forecast period (2025-2030).

Key Highlights

- Pharmaceutical packaging involves the assembly of elements required to enclose, maintain, safeguard, and distribute a secure and effective medicinal product, ensuring that a secure and effective dosage form is accessible at any given time prior to the drug product's expiration date. Appropriate packaging materials are essential for offering tamper-evident security, which aids in deterring the consumption of counterfeit medications. Furthermore, premium packaging materials must comply with rigorous regulatory guidelines.

- The pharmaceutical packaging manufacturers are anticipated to witness significant opportunities in Asia-Pacific, thanks to the increasing investments in the pharmaceutical sector. The rising demand for pharmaceutical drugs and advancements in pharmaceutical technology are directly contributing to the demand for glass bottles, ampules, and other glass packaging solutions. As chronic illnesses continue to rise and the production of COVID-19 vaccine doses remains substantial, the demand for primary packaging is expected to surge, specifically for glass containers.

- Glass packaging is expected to drive the market's growth in the region's pharma packaging sector. Pharmaceutical companies utilize glass containers to package a diverse array of pharmaceutical products, including injectable medications, solid oral pills, liquid formulations, and biologics. The rapid growth of glass packaging is driven by factors such as pharmaceutical manufacturing operations, the rising demand for specialty pharmaceuticals, and the expansion of healthcare infrastructure. This trend is particularly evident in countries like China, India, Japan, and South Korea, where pharmaceutical industries are experiencing significant growth, leading to a surge in demand for glass packaging solutions.

- The plastic bottles industry is projected to experience substantial growth in the coming years. The utilization of PET is steadily increasing in the region, resulting in a weight reduction of up to 90% compared to glass, thus enabling a more cost-effective transportation procedure. Presently, plastic bottles crafted from PET are extensively substituting bulky and delicate glass bottles in the pharmaceutical sector, providing reusable packaging for different liquids. The rising advancements in plastic PET technology for the pharmaceutical industry are anticipated to boost market prospects.

- Additionally, the government's initiatives to enhance the pharmaceutical sector in the area are anticipated to propel the market's expansion. For example, the measures implemented by the Chinese government to expedite the modernization of the nation's healthcare system are projected to stimulate the advancement of the pharmaceutical packaging industry. Moreover, China is proactively improving its pharmaceutical packaging infrastructure and resources while broadening its range of pharmaceutical products, potentially opening up new avenues for pharmaceutical packaging companies.

- China's presence in the global pharmaceutical market has been steadily growing, serving as both a major consumer and a vital component in the global pharmaceutical industry and supply chains. The rapid expansion of the pharmaceutical sector in recent years, driven by scientific and technological advancements, is projected to continue in the future. In December 2023, Danish pharmaceutical firm Novo Nordisk revealed its plan to invest CNY 400 million (USD 59.6 million) in a newly established company in the region by June 2026. These substantial developments are anticipated to drive the demand for pharmaceutical packaging services.

- The packaging industry experienced significant effects due to the COVID-19 pandemic. With a shift in focus toward infectious diseases and vaccines, there was a decrease in successful clinical trials and research and development activities in therapeutic areas like diabetes and hypertension. However, the pharmaceutical industry witnessed a surge in drug demand for various diseases during the pandemic, leading to substantial investments in the packaging business. Fortunately, the pharmaceutical industry quickly recovered by emphasizing the need for safe and hygienic packaging in response to the pandemic.

Asia Pacific Pharmaceutical Packaging Market Trends

Glass Packaging is Expected to Witness Significant Growth

- Glass packaging is widely considered the leading choice for pharmaceutical products in the packaging industry. Its popularity stems from its sustainable nature, inertness, impermeability, recyclability, and ability to be reused without compromising quality. The COVID-19 pandemic further fueled the demand for glass packaging as the need for medication significantly increased. With the approval and distribution of new drugs and vaccines by pharmaceutical manufacturers in various countries, the use of glass packaging is expected to continue expanding.

- Glass packaging is primarily provided as the main packaging option for pharmaceutical products and is one of the top choices in the pharmaceutical industry. This is mainly because it offers several advantages, including sustainability, inertness, impermeability, recyclability without any compromise in quality, and reusability. Glass containers have become widely utilized in the pharmaceutical sector as one of the primary packaging materials. As the prevalence of chronic diseases increases and the production of COVID-19 vaccine doses continues to rise, there is an anticipated surge in the demand for primary packaging, specifically glass containers.

- The increasing prevalence of chronic diseases in the APAC region is a major factor driving the expansion of the pharmaceutical packaging market. Conditions such as diabetes, cardiovascular diseases, cancer, and respiratory ailments necessitate continuous medication. As a result, there is a rising need for diverse pharmaceutical packaging solutions to securely store, safeguard, and distribute these medications with optimal efficiency. As per the World Health Organization (WHO), the rise in noncommunicable diseases is contributing to the escalating burden of chronic illnesses in the region, especially in the SEA region.

- The primary packaging glass solutions manufacturer, Stoelzle, unveiled their latest eco-friendly PharmaCos line at the CPHI Barcelona trade show in November 2023. This new line of packaging solutions boasts a high percentage of recycled glass (73% in amber glass and 38% in flint glass) and lightweight bottle design. Additionally, the new line is produced in a pharmaceutical-grade facility to meet the strict standards of the healthcare industry. Such significant innovations by the vendors are expected to drive the market's growth.

- Bormioli Pharma states that currently, various recycled glass products are available specifically designed for type II and type III glass. These products utilize materials sourced from an external supply chain that is certified for pharmaceutical use. Through chemical and mechanical processing, the recycled materials can be transformed into glass powder, which serves as the foundation for the new production cycle. Simultaneously, Bormioli Pharma is actively involved in projects aimed at developing low-emission furnaces. These furnaces incorporate innovative technologies and industrial processes that minimize their environmental footprint.

- Moreover, the market for glass packaging techniques in countries like Japan will be driven by the increasing investments made by pharmaceutical vendors to enhance pharmaceutical production. A notable example is Takeda's announcement in March 2023, stating its plan to invest approximately JPY 100 billion (USD 0.75 billion) in constructing a new manufacturing facility for plasma-derived therapies (PDTs) in Osaka, Japan. This investment represents Takeda's largest-ever expansion of manufacturing capacity in Japan. The upcoming state-of-the-art facility, expected to be operational by 2030, will be the largest of its kind in the country and will significantly increase Takeda's plasma manufacturing capacity.

India is Expected to Witness Significant Growth

- India is expected to be one of the fastest-growing regions in the pharmaceutical packaging market. The pharmaceutical packaging sector has witnessed significant growth in recent years, driven by innovations and the rise of new treatments. The onset of the COVID-19 pandemic underscored the importance of efficient product packaging and distribution. As a result, there's a growing emphasis on accelerating both manufacturing and distribution processes, including packaging. Consequently, packaging firms are under mounting pressure to innovate swiftly, meeting the demand for faster operations.

- India is anticipated to emerge as a key player in the pharmaceutical sector, especially in the production of generic drugs and cost-effective medication. The country plays a vital role as a primary provider of generic medicines to numerous advanced nations. The rising output and international distribution of generic drugs are significant factors driving the expansion of the Indian pharmaceutical packaging industry. Additionally, the surge in chronic illnesses and the rise in investments in drug manufacturing operations will lead to a substantial increase in demand within the market.

- The region is anticipated to experience a notable increase in demand for plastic packaging types. The surge in the need for medical supplies and medications has propelled the expansion of plastic pharma packaging in India. Numerous companies are making substantial investments in this technology to enhance the region's market potential. For instance, in March 2023, Spanish packaging company Inden Pharma intended to broaden its operations in India through a partnership with Austria-based ALPLApharma, which specializes in plastic packaging for pharmaceuticals. These noteworthy advancements are projected to stimulate growth in the market.

- InvestIndia reports that India is the largest global provider of generic medicines, making up 20% of the global supply by volume. Additionally, India is the top producer of vaccines worldwide. Outside of the United States, India has the highest number of pharmaceutical plants that comply with the standards set by the US Food and Drug Administration (US FDA). With over 3,000 pharmaceutical companies and more than 10,500 manufacturing facilities, India possesses a robust network and a highly skilled workforce in the pharmaceutical industry. Moreover, India fulfills approximately 60% of the global demand for vaccines and is a major supplier of DPT, BCG, and Measles vaccines. These extensive capabilities in pharmaceutical manufacturing will undoubtedly stimulate the packaging business market in the region.

- Moreover, InvestIndia states that the Indian pharmaceutical industry experienced an average growth rate of 9.47% from FY18 to FY22, reaching USD 42.34 Billion, mainly due to increased exports and a growing domestic market. Forecasts suggest that the pharma sector is expected to reach a value of USD 65 billion in 2024 and USD 120 billion in 2030. To ensure sustained growth, the government has implemented various initiatives to promote research and innovation. As part of its vision for 2047, the government aims to establish India as a global leader in producing affordable, innovative, and high-quality pharmaceuticals and medical devices, in line with the principle of Vasudhaiva Kutumbakam. Such significant developments will provide market opportunities in the packaging sector.

Asia Pacific Pharmaceutical Packaging Industry Overview

The Asia-Pacific pharmaceutical packaging market is competitive, with many regional and global players. Some major players are Amcor Ltd, West Pharmaceutical Services Inc., West Pharmaceutical Services Inc., CCL Industries Inc., and NIPRO Corporation. Companies are increasing their market share by launching new products and expanding production units. Some of the recent developments are:

- January 2024: Loop Industries Inc., a clean technology company whose mission is to accelerate a circular plastics economy by manufacturing 100% recycled polyethylene terephthalate ("PET") plastic and polyester fiber, and Bormioli Pharma, an international player in pharmaceutical packaging and medical devices, launched an innovative pharmaceutical packaging bottle manufactured with 100% recycled virgin quality Loop PET resin.

- June 2023: CIncorporated partnered with SGD Pharma to establish a state-of-the-art facility for producing pharmaceutical packaging glass in Telangana. It was reported that the two companies would collectively invest more than INR 500 crore in setting up this facility. This collaboration with Corning is a significant move in advancing converting technology within the pharmaceutical sector and ensuring a robust supply chain. By working together, these companies aim to assist pharmaceutical manufacturers in addressing the growing challenges related to capacity and quality, as well as meeting the rising global demand for essential medications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Supplier

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Market Drivers

- 4.4.1 Increasing Adoption of Pharmaceutical Packaging in Emerging Economies

- 4.5 Market Restraints

- 4.5.1 Fluctuations in Raw Material Cost

5 MARKET SEGMENTATION

- 5.1 By Material

- 5.1.1 Plastic

- 5.1.2 Paper and Paper Board

- 5.1.3 Glass

- 5.1.4 Aluminum Foil

- 5.2 By Type

- 5.2.1 Ampoules

- 5.2.2 Blister Packs

- 5.2.3 Plastic Bottles

- 5.2.4 Syringes

- 5.2.5 Vials

- 5.2.6 IV fluids

- 5.2.7 Other Types

- 5.3 By Drug Delivery Mode

- 5.3.1 Oral Drug packaging

- 5.3.2 Injectable Drug packaging

- 5.3.3 Pulmonary Drug Packaging

- 5.3.4 Other Drug Delivery Modes

- 5.4 By Country

- 5.4.1 India

- 5.4.2 Japan

- 5.4.3 China

- 5.4.4 Australia

- 5.4.5 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Amcor Ltd

- 6.1.2 CCL Industries Inc.

- 6.1.3 West Pharmaceutical Services Inc.

- 6.1.4 Gerresheimer AG

- 6.1.5 Schott AG

- 6.1.6 NIPRO Corporation

- 6.1.7 Wihuri Group

- 6.1.8 Klockner Pentaplast Group

- 6.1.9 Catalent Pharma Solutions Inc.

- 6.1.10 Berry Global Group Inc.