欧州の難燃剤市場:市場シェア分析、業界動向、統計、成長予測(2026年~2031年)

Europe Flame Retardant Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1907209

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

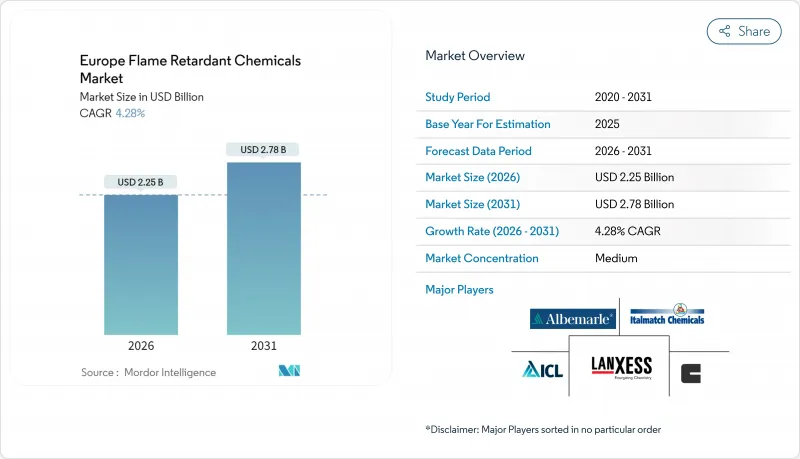

欧州の難燃剤化学品市場規模は、2026年に22億5,000万米ドルと推定されております。

2025年の21億6,000万米ドルから成長し、2031年には27億8,000万米ドルに達する見込みで、2026年から2031年にかけてCAGR4.28%で拡大いたします。

REACH規制への適合、臭素系システムの加速的な代替、持続的なインフラ投資により、同地域は非ハロゲン系添加剤の信頼できる需要拠点となっています。外壁材、断熱材、構造用鋼材に対する防火安全基準の強化により、建設分野が消費量の主導役を担っています。半導体自給率向上策や5G展開により活性化された電子機器生産が第二の成長エンジンとなり、中東欧における自動車軽量化や家具製造が下流顧客基盤を拡大しています。生産者が、EUの今後の持続可能性目標を満たすPFASフリーで循環型経済対応のグレードを競って投入する中、競合の激化が進んでおります。アルミニウム、リン、マグネシウム市場における原材料価格の変動が依然として主なリスク要因ではありますが、調達先の多様化戦略と在庫バッファーの増強により、供給側の変動性は一部緩和されております。

欧州難燃剤市場動向と分析

消費者向け電気電子機器製造の増加

欧州の電子機器メーカーは、供給ラインを短縮しEUチップス法に沿ったリショアリング計画を強化しています。難燃剤の選定は、バッテリーハウジングや5G無線ユニット向けのハロゲンフリー規制によって規定されています。LANXESS社が最近導入したポリアミド6グレードは、1.5mm厚でUL 94 V-0規格を達成しており、自動車メーカーが安全性を損なうことなく厚いバッテリーカバーを統合するのに貢献しています。USB-Cケーブル向けの配合メーカーは現在、データセンターや充電インフラの要件である低煙ゼロハロゲン基準も満たすハロゲンフリーTPEブレンドを採用しています。EUが地域内の準拠ポリマー調達を優先する半導体ファブへの補助金を提供していることも、需要の強さを後押ししています。

建築分野における防火規制の強化

EN 13501-1規格の2024年改訂版および木質外装材に関する各国規制により、低層住宅ファサードにはクラスD-s3,d1が義務付けられ、高層建築物には従来通りB-s3,d1が維持されました。これにより膨張性塗料や水酸化アルミニウム充填材の採用が促進されています。ドイツのDIBt(建築技術研究所)は不燃性ボードおよび塗装鋼板システムの認可リストを拡充し、メーカーに明確な認証取得経路を提供しました。EUグリーンディールに基づくプロジェクトでは、難燃性と炭素排出量削減を両立するリン系膨張性システムが指定されています。新規住宅及び改修工事はより高い基準を満たす必要があり、法的枠組みにより長期的な消費拡大が確実視されます。

臭素系難燃剤に関する毒性懸念

欧州化学物質庁(ECHA)は2025年4月の報告書において、複数の芳香族臭素化化合物に対する認可要件の可能性を示唆し、市場におけるこの化学物質への忌避感を強めています。北欧閣僚理事会は2030年までの完全廃止を継続して働きかけており、需要をさらに減退させています。臭素系システムは薄肉電子機器に優れていますが、代替圧力によりOEMメーカーは筐体形状の再設計や、リンー窒素の二重相乗効果システムへの移行を迫られています。コンプライアンスコストと潜在的な陳腐化により、新たな臭素系生産能力への投資意欲が低下し、将来の売上減少につながります。

セグメント分析

欧州の難燃剤化学品市場において、非ハロゲン系システムのシェアは88.83%を占めております。建設・電子機器分野におけるREACH規制対応を簡素化するリン系・無機系・窒素系化学品の採用拡大により、2031年までCAGR5.52%で成長が続きます。水酸化アルミニウムは煙抑制作用により壁板・電線ケーブル分野で最大シェアを維持、水酸化マグネシウムは高温用途へ進出中です。リン系添加剤は電気自動車用電池筐体に不可欠な薄肉効率を実現します。

イノベーション活動は、ポリウレタンやエポキシドネットワークへ重合する反応性リンオリゴマーを中心に展開され、リサイクル時の移行を防止します。特殊化学品分野からの新規参入企業は、金属ホスフィネート系添加剤の相乗効果を活用し、添加量を低減しながら材料の機械的特性を維持します。自社生産のリン系メーカーが高純度誘導体へ垂直統合することでコスト競争力が向上し、価格急騰の緩和が図られます。再生原料グレードへのアクセスは依然としてボトルネックですが、ドイツでのパイロット試験では、回収ポリカーボネートにリン酸エステルを25%封入した混合物の導入に成功し、UL-94 V-0規格を損なうことなく実現しています。

欧州難燃剤化学品レポートは、製品タイプ(非ハロゲン系・ハロゲン系)、エンドユーザー産業(電気電子、建築建設、輸送、繊維家具)、地域(ドイツ、英国、イタリア、フランス、スペイン、その他欧州)別に分類されています。市場予測は金額ベース(米ドル)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 消費者向け電気・電子機器製造の増加

- 建設分野における防火安全規制の強化

- 中東欧地域における家具・室内装飾品生産の成長

- 循環型経済に適合した難燃剤添加剤への移行

- 5Gケーブルおよびデータセンター設置の急増

- 市場抑制要因

- 臭素系難燃剤の毒性に関する懸念

- 原材料価格の変動性(アルミニウム、リン、マグネシウム鉱石)

- EUにおけるポリマー使用を制限するマイクロプラスチック規制の施行待ち

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- 製品タイプ別

- 非ハロゲン系

- 無機系

- 水酸化アルミニウム

- 水酸化マグネシウム

- ホウ素化合物

- リン系

- 窒素系

- その他

- 無機系

- ハロゲン化

- 臭素系化合物

- 塩素系化合物

- 非ハロゲン系

- エンドユーザー業界別

- 電気・電子機器

- 建築・建設

- 交通機関

- 繊維・家具

- 地域別

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/順位分析

- 企業プロファイル

- Adeka Corporation

- Albemarle Corporation

- BASF

- Clariant

- DIC Corporation

- Dow

- Eti Maden

- ICL

- Italmatch Chemicals SpA

- J.M. Huber Corp.(Huber Engineered Materials)

- LANXESS

- MPI Chemie BV

- Nabaltec AG

- RTP Company

- THOR Group

- TOR Minerals

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日