タンパク質工学におけるラボオートメーション:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Lab Automation in Protein Engineering - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1640326

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

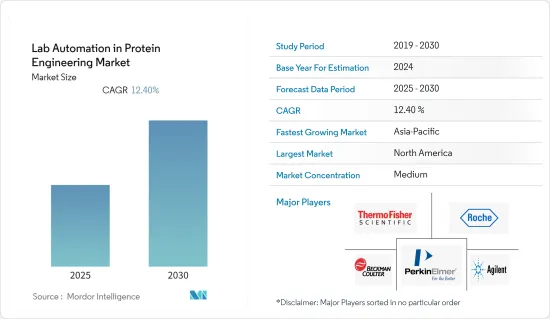

タンパク質工学におけるラボオートメーション市場は予測期間中にCAGR 12.4%を記録する見込みです。

主なハイライト

- タンパク質エネルギー栄養失調(PEM)は、新興国の農村地域で増加しています。クワシオルコル、マラスムス、マラスムス-クワシオルコル移行期を含む病気の集合体を指します。そのため、クワシオルコルの発症率は地域によって異なります。米国ではかなり珍しいです。中南米、東南アジア、コンゴ、ジャマイカ、プエルトリコ、南アフリカが影響を受けています。その結果、タンパク質欠乏症の頻度が高まっており、市場全体の需要を押し上げています。

- ヘルスケア事業は、タンパク質工学の研究開発や意識向上プログラムのスポンサーなど、政府の取り組みが増加している影響を受けています。その結果、政府は先行していくつかの研究イニシアチブに資金を提供しています。例えば、プロテイン・テクノロジーズ社(PTL)は、画期的なタンパク質工学研究のために、英国政府の技術戦略委員会(現イノベートUK)から資金を得ています。

- タンパク質工学は農薬ビジネスにおいても大きな可能性を秘めています。なぜなら、より優れた機能を持つ酵素を生み出し、作物の収量を向上させ、バイオ燃料の生産を容易にすることができるからです。また、将来のニーズを満たすために必要な、より高い農業成果を達成するための技術としても重要な役割を果たすと予想されています。

- COVID-19の発生以来、研究所はその敷地と資源をCOVID-19検査施設に変え、自動化機器の使用を増やしています。ワシントン大学の研究室がその最初の例です。この声明は、ブロード研究所がその臨床処理ラボを大規模なCOVID-19検査施設に転換すると発表した後のことです。

タンパク質工学におけるラボオートメーション市場動向

自動リキッドハンドラー装置が最大の市場シェアを占める

- リキッドハンドラーは通常、生化学・化学研究所で採用されています。自動リキッドハンドリングロボットは、ラボにおけるサンプルやその他の液体の分注に役立ちます。自動リキッドハンドラーは運転時間を最小化し、精度を最大化します。さらに、リキッドハンドラーは、ナノリットルに及ぶ幅広い容量で動作することができるため、分注作業における有用性が証明されています。

- 主要企業は自動リキッドハンドラー開発のベンチマークを設定し、生産性を効果的に向上させるためのプレミアム製品の開発に絶えず投資しています。微量の液体を扱うことができるリキッドハンドラーの進化は、市場におけるモジュラー式ラボオートメーションシステムの急速な開拓に貢献しています。

- Robotic Industries Associationによると、ライフサイエンス分野では、自動液体ハンドラー、自動プレートハンドラー、ロボットアームなどの産業用ロボットの需要が3番目に高い伸びを示しています。

- パーカー氏によると、ライフサイエンス・ロボットの動向のひとつは、ロボット分析装置においてフルイディクスがより分かりやすくなっていることです。この動向は、臨床検査室や病院が、重要なサンプルを扱う際に、装置がダウンするわけにはいかないことから生じたものです。以前は分注ユニットの先端に50本の針があり、多くのチューブを使用していた特定のロボットシステムは、チューブを不要にし、故障の可能性を少なくする特殊なバルブ・マニホールドを使用するようになってきています。マニホールドは漏れの可能性を最小限に抑えます。

北米が最大の市場シェアを占める

- 北米は長年臨床研究のパイオニアです。この地域にはファイザー、ノバルティス、グラクソ・スミスクライン、J&J、ノバルティスなどの大手製薬会社があります。また、この地域には開発業務受託機関(CRO)が最も集中しています。重要なCROには、Laboratory Corp. of America Holdings、IQVIA、Syneos Health、Parexel International Corp.などがあります。業界大手各社の存在とFDAの厳しい規制により、この地域の市場競争は激しいです。競合他社より優位に立つために、この地域のゲノミクス研究機関は、ラボにロボット工学と自動化を採用する傾向を強めています。

- ゲノム産業は、特に米国では現在も成長を続けており、今後数年間でさらに拡大すると予想されています。新しいゲノムシーケンシング技術の利用可能性、確立されたヘルスケアインフラ、高齢者人口の増加が、収益拡大の大きな要因となっています。米国では、成長への対応と効率化の必要性から、血液センターが全自動ウォークアウェイシステムを導入し、血液型検査やスクリーニング、感染症検査を行っています。

- 多くの企業は、その広範な研究開発能力により、技術革新に関与しています。自動化の個々の領域は、精製、タンパク質工学、化合物合成、生物学的試験、およびマグナモーション・トラックを備えた研究室での分析を網羅することができます。

タンパク質工学におけるラボオートメーション産業の概要

タンパク質工学におけるラボオートメーション市場は、多くの大小のプレーヤーが多くの国に製品を輸出しているため、競争は中程度です。大手企業が採用する主な戦略は、開発における技術進歩、パートナーシップ、M&Aです。同市場の主要企業には、サーモフィッシャーサイエンティフィック社、F.ホフマン・ラ・ロシュ社、シーメンス・ヘルスイニアーズ社、ダナハー社、パーキンエルマー社などがあります。最近の市場動向は以下の通り:

- 2023年1月-大手医療技術プロバイダーであるBD(ベクトン・ディッキンソン・アンド・カンパニー)は、BDキエストラ微生物検査室ソリューション用の新しいロボティックトラックシステムを全世界で発表しました。このシステムは、ラボ検体の処理を自動化し、手作業を削減することができます。新しいBDキエストラ第3世代コンプリートラボオートメーションシステムは、ラボの特定の要求に合わせて拡張可能であり、柔軟でカスタマイズされたトータルラボオートメーション構成で複数のBDキエストラモジュールを接続することができます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- バリューチェーン/サプライチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の業界への影響評価

第5章 市場力学

- 市場促進要因

- IoTによる検査室のデジタルトランスフォーメーションの動向の高まり

- 膨大なデータの効率的管理

- 市場抑制要因

- 高額な初期設定費用

第6章 市場セグメンテーション

- 機器別

- 自動リキッドハンドラー

- 自動プレートハンドラー

- ロボットアーム

- 自動保管・検索システム(AS/RS)

- その他の機器

- 地域別

- 北米

- 欧州

- アジア太平洋

- 世界のその他の地域

第7章 競合情勢

- 企業プロファイル

- Thermo Fisher Scientific Inc.

- Danaher Corporation/Beckman Coulter

- Hudson Robotics Inc.

- Becton, Dickinson and Company

- Synchron Lab Automation

- Agilent Technologies Inc.

- Siemens Healthineers AG

- Tecan Group Ltd

- Perkinelmer Inc.

- Eli Lilly and Company

- F. Hoffmann-La Roche Ltd

第8章 投資分析

第9章 市場機会と今後の動向

目次

The Lab Automation in Protein Engineering Market is expected to register a CAGR of 12.4% during the forecast period.

Key Highlights

- Protein-energy malnutrition (PEM) is rising in emerging economies' rural communities. It refers to a collection of illnesses that includes kwashiorkor, marasmus, and marasmus-kwashiorkor transitional phases. As a result, the incidence of kwashiorkor varies by region. It is pretty uncommon in the United States. Central America, Southeast Asia, Congo, Jamaica, Puerto Rico, and South Africa are impacted. As a result, the rising frequency of protein-deficiency illnesses boosts total market demand.

- The healthcare business has been affected by a growing number of government efforts, such as sponsoring R&D for protein engineering and awareness programs. As a result, the government is funding several research initiatives ahead of time. For example, Protein Technologies Ltd (PTL) obtained money from the UK government's Technology Strategy Board (now Innovate UK) for their ground-breaking protein engineering research.

- Protein engineering also has great potential in the agrochemical business because it can lead to better-functioning enzymes, boost crop yields, or make biofuel production easier. It is also anticipated to play a vital role as a technique for achieving the higher agricultural outcomes required to satisfy future needs.

- Since the outbreak of COVID-19, labs have been turning their premises and resources into COVID-19 testing facilities, increasing automation equipment use. The University of Washington's laboratories were the first to do so. The statement came after the Broad Institute announced that its clinical processing lab would be converted into a large-scale COVID-19 testing facility.

Lab Automation in Protein Engineering Market Trends

Automated Liquid Handler Equipment Accounted for the Largest Market Share

- Liquid handlers are usually employed in biochemical and chemical laboratories. Automated liquid handling robots help in dispensing samples and other fluids in laboratories. Automated liquid handlers minimize run times and maximize accuracy. Moreover, liquid handlers can operate across a wide range of volumes, extending into nanolitres, thus proving their usefulness in dispensing operations.

- Leading companies have set the benchmark for the development of automated liquid handlers and are constantly investing in developing premium products to increase productivity effectively. The evolution of liquid handlers, capable of handling minute volumes of liquids, has contributed to the rapid development of modular lab automation systems in the market.

- According to the Robotic Industries Association, the life science sector has the third-highest growth in industrial robots, in terms of automated liquid handlers, automated plate handlers, robotic arms, and others, to meet the demand.

- According to Parker, one of the trends in life science robotics is fluidics getting more straightforward in robotic analyzers. This trend arose because clinical laboratories and hospitals cannot afford an instrument to go down when critical samples are involved. Specific robotic systems that used to have 50 needles on the end of a dispensing unit and lots of tubing increasingly use special valve manifolds that eliminate the need for tubing and result in less chance of failure. The manifolds minimize the possibility of leakage.

North America Occupied the Largest Market Share

- North America has been a pioneer in clinical research for years. This region is home to major pharmaceutical companies, like Pfizer, Novartis, GlaxoSmithKline, J&J, and Novartis. The part also has the highest concentration of contract research organizations (CROs). Some significant CROs are Laboratory Corp. of America Holdings, IQVIA, Syneos Health, and Parexel International Corp. Owing to the presence of all the major players in the industry and stringent FDA regulations; the market is very competitive in the region. To gain an advantage over competitors, the genomics research organizations in the area are increasingly adopting robotics and automation in labs.

- The genomic industry, especially in the United States, is still growing and is expected to increase over the coming years. The availability of new genome sequencing technologies, well-established healthcare infrastructure, and the increasing geriatric population are significant contributing factors to revenue growth. In the United States, the need to accommodate growth and the drive to boost efficiency are priming blood centers to acquire fully automated walkaway systems to perform types and screens or test specimens for infectious diseases.

- Many companies are involved in innovation due to their extensive R&D capabilities. Individual areas of automation can encompass purification, protein engineering, compound synthesis, biological testing, and analysis in the lab equipped with a Magnamotion track.

Lab Automation in Protein Engineering Industry Overview

The lab automation in protein engineering market is moderately competitive, owing to many small and big players exporting products to many countries. The key strategies adopted by the major players are technological advancement in development, partnerships, and merger and acquisition. Some of the major players in the market are Thermo Fisher Scientific Inc., F. Hoffmann-La Roche Ltd, Siemens Healthineers, Danaher Corporation, and PerkinElmer. Some of the recent developments in the market are:

- January 2023 - BD (Becton, Dickinson and Company), a leading medical technology provider, unveiled a new robotic track system for the BD Kiestra microbiology laboratory solution worldwide. This system automates the processing of lab specimens, which could help to cut down on manual labor. The new BD Kiestra 3rd Generation Complete Lab Automation System is expandable to fit the specific demands of labs and allows them to connect several BD Kiestra modules in a flexible and customized total lab automation configuration.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Value Chain/Supply Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the COVID-19 Impact on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Trend of Digital Transformation for Laboratories with IoT

- 5.1.2 Effective Management of the Huge Amount of Data Generated

- 5.2 Market Restraints

- 5.2.1 Expensive Initial Setup

6 MARKET SEGMENTATION

- 6.1 By Equipment

- 6.1.1 Automated Liquid Handlers

- 6.1.2 Automated Plate Handlers

- 6.1.3 Robotic Arms

- 6.1.4 Automated Storage and Retrieval Systems (AS/RS)

- 6.1.5 Other Equipment

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia-Pacific

- 6.2.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Thermo Fisher Scientific Inc.

- 7.1.2 Danaher Corporation/Beckman Coulter

- 7.1.3 Hudson Robotics Inc.

- 7.1.4 Becton, Dickinson and Company

- 7.1.5 Synchron Lab Automation

- 7.1.6 Agilent Technologies Inc.

- 7.1.7 Siemens Healthineers AG

- 7.1.8 Tecan Group Ltd

- 7.1.9 Perkinelmer Inc.

- 7.1.10 Eli Lilly and Company

- 7.1.11 F. Hoffmann-La Roche Ltd

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日