アクティブデータウェアハウスの市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Active Data Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1639541

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

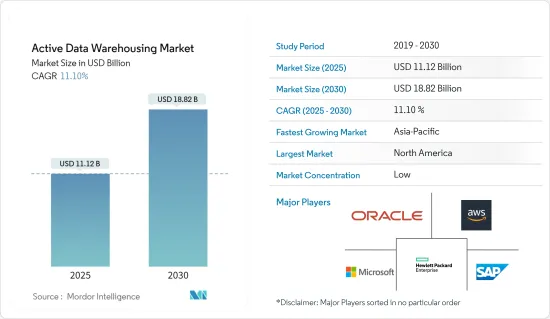

アクティブデータウェアハウスの市場規模は、2025年に111億2,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは11.1%で、2030年には188億2,000万米ドルに達すると予測されます。

また、新興国市場の需要成長により、予測期間を通じてアクティブデータウェアハウス市場に新たな機会がもたらされると予測されます。

主要ハイライト

- アクティブデータウェアハウス市場は、次世代ビジネスインテリジェンスへの継続的な需要と組織が生成するデータ量の増加といった要因によって、大きな変化を遂げようとしています。ADWによって、ユーザーは膨大で複雑な情報にリアルタイムでアクセスできるようになります。データは効率的かつ適切に整理されるため、予測期間中の市場成長を後押しするものと期待されています。低遅延かつ高速な分析に対する需要の高まりは、企業経営におけるビジネスインテリジェンスの役割の増大と相まって、市場の需要を大きく牽引すると予想されます。

- さらにOracleによると、人口の90%近くが都市部に居住するブラジルでは、SKY Brasilが家庭向け衛星直収サービスの市場シェア約29%を占めています。同社は、OracleのSiebel CRMに統合されたOracle Cloud Infrastructure上で稼働するOracleのAutonomous Data Warehouseを選択し、リアルタイムの先進的マーケティング分析を実行しました。この導入企業は、以前のオンプレミスソリューションと比較して、導入と本番稼動にかかる時間を90%短縮し、同時にインフラコストを60%削減することに成功しました。さらに、ADWは、データを1カ所にまとめることと相まって、コンピューティングのコストを大幅に削減します。

- さらに、ADWはデータを1カ所にまとめることと相まって、コンピューティングのコストを大幅に削減し、これも市場の成長にプラスの影響を与えると予測されます。こうした動向とともに、世界的には、企業におけるビッグデータ動向の大幅な高まりが分析需要の増加につながっており、これも市場成長を後押しすると予測されます。また、需要に合わせてコンピューティング能力を拡大し、使用量がピークに達したときに容易に規模を縮小できるよう、市場のベンダーはクラウドデータウェアハウジングの価格設定にリソース使用量ベースのモデルを採用しています。これは、ベンダーが求める規模の経済と、顧客が求める柔軟性の問題に対処するものです。しかし、固定容量のデータウェアハウスは、組織に必要以上のコンピューティング容量の購入を強います。

- データウェアハウスは、特に金融、ビジネス、医療、その他の産業において、データ管理や複雑性の増大に対する懸念の高まりから、実世界での応用に大きな関心を集めています。企業プロセスのデジタル化により、IT産業ではデータ分析機能を備えた新しい技術的に先進的業務が採用されるようになりました。その結果、最新のデータウェアハウスシステムは、デジタルビジネス運営に必要なリアルタイムで企業規模の分析と情報洞察の開発を促進します。

- しかし、アクティブなデータウェアハウスの市場は、高い導入コストやサイバー脅威の増加など、さまざまな要因によって抑制されています。

- COVID-19は市場にさまざまな影響を与えました。例えば、バート・ワークスとInternational Institute for Analytics(IIA)が米国の分析専門家300人を対象に実施した調査では、回答者の43%以上が、COVID-19問題に対して本質的な選択をするための行動において、分析が重要な要因であると回答したことが明らかになりました。企業はパンデミックの流行により業務を縮小し、経費を削減し、オフィスを閉鎖しました。在宅勤務のパラダイムの普及は、企業にとってによる困難をもたらしています。クラウドベースのデータウェアハウスの導入は、このような開発によって加速すると予想されます。パンデミックは、費用対効果、大規模なスキルプールへのアクセス、拡大性の強化など、データウェアハウスの導入に多くの利点をもたらしました。

アクティブデータウェアハウスの市場動向

スマートフォンの普及が市場成長を牽引

- 携帯電話、特にスマートフォンは、さまざまな人々の間でますます普及しています。現代の情報通信技術(ICT)により、ユーザーは必要な情報を迅速に入手することができます。GSMAによると、昨年時点でアクティブなiOSとAndroidスマートフォンは世界で62億台以上あり、2025年には74億台に達すると予想されています。さらに、データウェアハウス(DW)、ビジネスインテリジェンス(BI)システム、データ分析システムなど、さまざまなコンピューターシステムでモバイル技術の利用が増加しています。

- 携帯電話はデータベースとして機能し、かなりの量のユーザーデータが保存されます。保存されたデータは、ユーザーが承認したT&Cに従って分析することができます。データは様々なアクティブデータウェアハウスによって検索・分析され、ユーザーの複数の特徴を収集することができます。スマートフォンユーザーは、データアクセスのために膨大なクラウドデータベースを必要とするため、データウェアハウスソリューションが必要となり、市場の成長を促進しています。

- さらに、中国、ブラジル、インドなどの新興国でスマートフォンの利用が増加し、ソーシャル・メディアのトラフィックが増加した結果、データストリームの増加により、リアルタイムのデータストレージなど、より多くの機能が必要とされています。

- さらに、さまざまな国でスマートフォンの利用が増加していることも、市場の成長を促進すると予想されます。例えば、情報放送省によると、2022年11月、インドの携帯電話加入者数は12億人を超え、その中には6億人のスマートフォンユーザーが含まれています。さらに、データ通信料金が比較的安いことに加え、スマートフォンの普及により、個人がモバイル端末で多くの情報や娯楽を消費するようになったことが挙げられています。

北米が大きな市場シェアを占める見込み

- 米国の組織は、欧州やアジアの組織と比較して、複数の業種にわたって分析を大幅に導入しています。米国はかなりの需要があり、ベンダーも存在するため、市場には欠かせない国と考えられています。また、GSMAによると、北米の昨年のモバイルサービス加入者は3億2,900万人で、これは全人口の84%に相当します。この地域の新規ユニークカスタマーのほとんどが米国からのものであることから、この地域の通信事業者が対応可能な市場全体は飽和状態に近づいています。米国は、2025年までに同地域で増加すると予想される1,200万人のユーザーの75%を提供することになります。

- また、同国の消費者は、問題にリアルタイムで対応してくれるベンダーを高く評価しています。そのため、多くの小売企業がアクティブデータウェアハウスのコンセプトを採用し、消費者の囲い込みに重要な役割を果たすロイヤルティ管理用途を強化しています。

- モバイルブロードバンドの普及は、ビッグデータ分析やクラウドコンピューティングの増加につながりました。2022年に分析を採用する企業が相当数存在する米国では、複数の企業がオンプレミスからクラウドベースの展開に切り替えることを促し、データウェアハウス導入の対応市場と推定されます。さらに、貿易活動の増加や国内の企業数の増加に伴い、ロジスティクス活動も増加すると予想されます。しかし、増え続ける公的債務がインフレ率を押し上げ、小規模ベンダーの活動を抑制することが予想されます。

- Microsoftによると、AIを活用したバーチャルエージェントは、新興チャネルに大きく貢献しています。自然言語処理や機械学習のような機能は、スマートで、会話的で、迅速なソリューションを24時間365日提供する能力を持っています。このことは、企業が顧客満足度の向上を重要視し、投資していることを示しています。したがって、このような洗練されたプラットフォームと分析に対する需要は、アクティブデータウェアハウスの着実な成長率を記録し続けると考えられます。

- 市場のもう1つの主要促進要因は、BI機能を備えたソリューションに対するニーズの高まりです。政府の取り組みや、疾病の発見や予防といったプライマリケアの改善に向けた医師のデータ分析の増加が、市場を牽引しています。そのため、多くの医療組織は、コスト削減を拡大するために、積極的なデータウェアハウスへの支出を増やしています。予測期間中、保険会社やその他のBFSI企業によるリアルタイム分析とBIに対する需要の増加が、米国におけるADWの需要を強化すると予想されます。

アクティブデータウェアハウジング産業概要

アクティブデータウェアハウス市場は非常にセグメント化されており、Microsoft Corporation、Oracle Corporation、SAP SEなど、国内外の参入企業がかなり競合しています。技術の進歩も企業に大きな競争優位性をもたらしており、市場では複数の提携も見られます。

2022年5月、Dell Technologies Inc.とSnowflake Inc.は、同社のオンプレミス・ストレージ・ポートフォリオのデータをSnowflake Data Cloudと連携させる新たなプロジェクトに関する提携を発表しました。Snowflake Data Cloudと呼ばれるクラウドネイティブなプラットフォームは、企業全体で安全なデータ共有を可能にしながら、個によるデータレイクやウェアハウスの必要性をなくすことを目的としています。様々なSoftware-as-a-Serviceやクラウドプラットフォームからデータセットを集約し、あらゆるユーザーが利用できるようにします。また、2022年5月、Oracleとエンタープライズクラウドデータ管理の著名なプロバイダーである Informaticaは、 Informaticaのデータ統合とガバナンスソリューションをOracle Cloud Infrastructureで使用できるようにする戦略的関係を発表しました。さらに、Oracleは Informaticaを、OCI上のデータウェアハウスとレイクハウスソリューション向けのエンタープライズクラウドデータガバナンスと統合の推奨パートナーに指定しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- 様々な産業におけるビジネスインテリジェンスとビッグデータ分析ソリューションの採用増加

- スマートフォンの普及が市場成長を促進する可能性

- 市場課題

- 導入に必要なリソースと時間の高消費

- サイバー脅威の増大が市場成長を抑制する可能性

第6章 市場セグメンテーション

- 導入タイプ別

- オンプレミス

- クラウド

- ハイブリッド

- 企業規模別

- 中小企業

- 大企業

- 産業別

- BFSI

- 製造業

- 医療

- 小売

- その他産業別

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- その他のアジア太平洋

- その他

- 北米

第7章 競合情勢

- 企業プロファイル

- Treasure Data Inc.

- Cloudera Inc.

- Snowflake Computing Inc.

- Oracle Corporation

- Hewlett Packard Enterprise Company

- Microsoft Corporation

- SAP SE

- Amazon Web Services, Inc.

- VMware Inc.(Pivotal Software Inc.)

- Huawei Technologies Co. Ltd

- Teradata Corporation

- Kognitio Ltd

- IBM Corporation

第8章 投資分析

第9章 市場の将来

目次

The Active Data Warehousing Market size is estimated at USD 11.12 billion in 2025, and is expected to reach USD 18.82 billion by 2030, at a CAGR of 11.1% during the forecast period (2025-2030).

Additionally, the growth in demand from developing nations is anticipated to open up new opportunities for the active data warehousing market throughout the projection period.

Key Highlights

- The active data warehousing market is poised for a significant shift, owing to factors like the ongoing demand for next-gen business intelligence coupled with the growing amount of data organizations generate. ADW allows users to access an enormous range of complex information in real-time. The data is organized efficiently and relevantly, which is anticipated to aid market growth over the forecast period. The rising demand for low latency and high-speed analytics, combined with the growing role of business intelligence in enterprise management, is expected to drive the market demand significantly.

- Further, according to Oracle, in Brazil, with nearly 90% of the population living in urban areas, SKY Brasil has approximately 29% market share for direct-to-home satellite services. The company opted for Oracle's Autonomous Data Warehouse running on Oracle Cloud Infrastructure, integrated into Oracle's Siebel CRM, to perform real-time, sophisticated marketing analytics. The deployer achieved 90% less time in deployment and commencing production than its previous on-premise solution while realizing 60% of infrastructure cost savings. Furthermore, ADW significantly diminishes the cost of computing, coupled with combining data in a single location, which is further projected to impact market growth positively.

- Additionally, ADW substantially decreases the cost of computing, coupled with combining data in a single location, which is also expected to impact the market growth positively. Along with these factors, globally, the significant rise in the Big Data trend in organizations is leading to the increasing demand for analytics, which is also projected to aid market growth. Also, to scale the computing capacity to match the demand and effortlessly scale back down when the usage peaks, vendors in the market have been following resource usage-based models for the pricing of cloud data warehousing. It addresses the issues of economies of scale that vendors may look for and the flexibility that clients demand. However, fixed-capacity data warehouses force organizations to buy more computing capacity than needed.

- Data warehousing has generated a lot of interest in real-world applications, notably in finance, business, healthcare, and other industries, as a result of growing concerns about data management and rising complexity. Digitalizing corporate processes led to the adoption of new technologically advanced operations with data analytics capabilities in the IT industry. As a result, modern data warehouse systems facilitate the development of the real-time, enterprise-scale analytics and information insights required for digital business operations.

- However, the market for active data warehousing is being restrained by various factors, including high installation costs and increased cyber threats.

- COVID-19 created a mixed impact on the market. For instance, in a survey of 300 analytics professionals in the US, Burtch Works and the International Institute for Analytics (IIA) revealed that over 43% of respondents said that analytics was a crucial factor in their actions to make essential choices in response to the COVID-19 problem. Companies scaled back operations due to the pandemic epidemic, reduced expenses, and closed offices. The widespread adoption of the work-from-home paradigm presents another difficulty for firms. Cloud-based data warehouse installations are anticipated to be accelerated by such developments. The pandemic provided numerous advantages for adopting data warehousing, including cost-effectiveness, access to a large skill pool, and enhanced scalability.

Active Data Warehousing Market Trends

Rising Penetration of Smartphones may Drive the Market Growth

- Mobile phones, especially smartphones, are becoming increasingly widespread among various people. Users may get essential information rapidly owing to modern information and communication technology (ICT). According to the GSMA, there are more than 6.2 billion active iOS and Android smartphones worldwide as of last year, and it is expected to reach 7.4 billion by 2025. Additionally, the usage of mobile technology is increasing across a range of computer systems, including Data Warehouse (DW), Business Intelligence (BI) systems, and Data Analytic systems.

- Mobile phones act as a database, where a considerable amount of user data is stored. The stored data can be subjected to analysis as per the T&C approval by the user. The data can be retrieved and analyzed by various active data warehouses to collect multiple traits of the user. Smartphone users need a vast cloud database for data access, thereby needing data warehousing solutions, driving market growth.

- Further, an increasing data stream necessitates more capabilities, including real-time data storage, as a result of the rising smartphone usage in emerging nations like China, Brazil, and India, as well as the increased social media traffic.

- Moreover, the growing smartphone usage across various countries is anticipated to drive market growth. For instance, according to the Ministry of Information and Broadcasting, in November 2022, India had more than 1.2 billion mobile phone subscribers, including 600 million smartphone users. Furthermore, it was mentioned that in addition to having relatively cheap data rates, the widespread usage of smartphones has led to individuals consuming a lot of information and entertainment on their mobile devices.

North America is Expected to Hold a Significant Market Share

- The United States organizations are significant adopters of analytics across several verticals, compared with European or Asian organizations. The United States is considered an essential country in the market because of the considerable demand and presence of vendors. Also, according to GSMA, there were 329 million mobile service subscribers in North America last year, or 84% of the total population. With most of the region's new unique customers coming from the United States, the total addressable market for the operators in the area is approaching close to saturation. The United States would provide 75% of the 12 million more users anticipated in the region by 2025.

- Also, consumers in the country value vendors that provide real-time assistance with their issues; hence, many retail organizations are adopting active data warehousing concepts to enhance loyalty management applications that play a crucial role in retaining consumers.

- The growth of mobile broadband led to increased Big Data analytics and cloud computing in the country. The United States, with a considerable number of analytics adopters in 2022, encouraged multiple enterprises to switch from on-premise to cloud-based deployment, which is estimated to be an addressable market for data warehouse installations. Furthermore, logistics activities are expected to increase with the rise in trade activities and the growing number of businesses in the country. However, the ever-increasing public debt of the country is expected to drive the inflation rate up, thus curtailing small vendors' activities.

- As per Microsoft, AI-driven virtual agents have contributed significantly toward emerging channels. Features like natural language processing and machine learning possess capabilities to deliver smart, conversational, and fast solutions 24/7. It indicates the importance and spending that companies direct toward improving customer satisfaction. Therefore, the demand for such sophisticated platforms and analytics will continue to help register a steady growth rate of active data warehousing.

- Another key driver in the market is the increasing need for solutions with BI capabilities. Government initiatives and increased data analytics physicians use for improved primary care, such as the detection and prevention of diseases, are driving the market. Thus, many healthcare organizations have started spending more on active data warehousing to increase cost savings. Over the forecast period, the increasing demand for real-time analytics and BI from insurance and other BFSI companies is expected to bolster the demand for ADW in the United States.

Active Data Warehousing Industry Overview

The Active Data Warehousing Market is highly fragmented, with several domestic and international players in a fairly-contested market space, including Microsoft Corporation, Oracle Corporation, SAP SE, etc. Technological advancements are also bringing considerable competitive advantage to companies, and the market is also witnessing multiple partnerships.

In May 2022, Dell Technologies Inc. and Snowflake Inc. announced a partnership on a new project to link data from its on-premises storage portfolio with the Snowflake Data Cloud. A cloud-native platform called Snowflake Data Cloud is intended to do away with the need for separate data lakes and warehouses while enabling safe data sharing throughout enterprises. It allows users to aggregate datasets from various software-as-a-service and cloud platforms and make them available to any user. Also, in May 2022, Oracle and Informatica, a prominent provider of enterprise cloud data management, announced a strategic relationship that will enable Informatica's data integration and governance solutions to be used with Oracle Cloud Infrastructure. Additionally, Oracle has designated Informatica as a recommended partner for enterprise cloud data governance and integration for data warehouse and lakehouse solutions on OCI.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increase in the Adoption of Business Intelligence and Big Data Analytics Solutions in Various Industries

- 5.1.2 Rising Penetration of Smartphones may Drive the Market Growth

- 5.2 Market Challenges

- 5.2.1 High Consumption of Resources and Time Required for Implementation

- 5.2.2 Growing Cyber Threats may Restrain the Market Growth

6 MARKET SEGMENTATION

- 6.1 By Type of Deployment

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.1.3 Hybrid

- 6.2 By Size of Enterprise

- 6.2.1 Small and Medium-sized Enterprises

- 6.2.2 Large Enterprises

- 6.3 By Industry Vertical

- 6.3.1 BFSI

- 6.3.2 Manufacturing

- 6.3.3 Healthcare

- 6.3.4 Retail

- 6.3.5 Other Industry Verticals

- 6.4 Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Spain

- 6.4.2.5 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 Rest of Asia-Pacific

- 6.4.4 Rest of the World

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Treasure Data Inc.

- 7.1.2 Cloudera Inc.

- 7.1.3 Snowflake Computing Inc.

- 7.1.4 Oracle Corporation

- 7.1.5 Hewlett Packard Enterprise Company

- 7.1.6 Microsoft Corporation

- 7.1.7 SAP SE

- 7.1.8 Amazon Web Services, Inc.

- 7.1.9 VMware Inc. (Pivotal Software Inc.)

- 7.1.10 Huawei Technologies Co. Ltd

- 7.1.11 Teradata Corporation

- 7.1.12 Kognitio Ltd

- 7.1.13 IBM Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日