|

市場調査レポート

商品コード

1850004

ろう付け合金:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Braze Alloys - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ろう付け合金:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月25日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

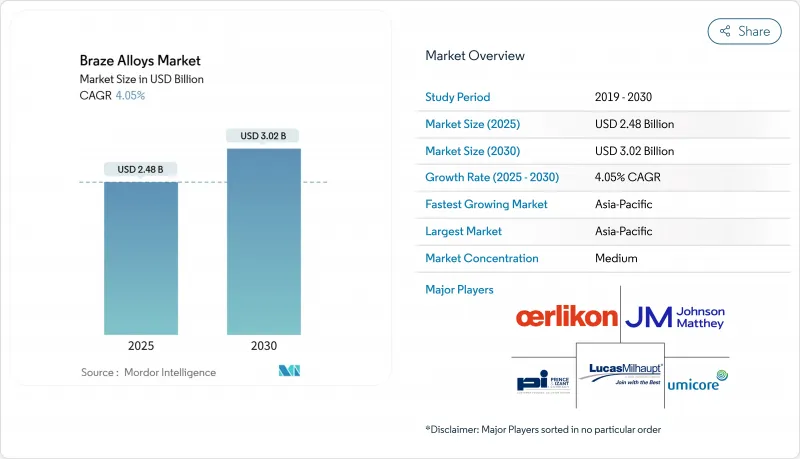

ろう付け合金の市場規模は2025年に24億8,000万米ドル、2030年には30億2,000万米ドルに達する見込みで、CAGRは4.05%です。

この市場は、自動車熱交換器、EVパワーエレクトロニクス、先進航空宇宙構造物における精密金属接合への需要の高まりから力を得ています。中温作業における溶接のろう付けによる着実な代替が数量を高水準に維持する一方、新しいアモルファス箔合金が異種金属接合への応用の幅を広げています。アジア太平洋は、中国のアルミニウム二次加工ブームと各地域の電子機器生産能力拡張に支えられて、数量と成長を支配しています。サプライチェーン参入企業は、価格重視のグレードよりも高性能の配合を好むようになっており、ろう付け合金市場全体が品質重視の購買にシフトしていることを示しています。

世界のろう付け合金市場の動向と洞察

溶接・はんだ付けよりもろう付けの採用

ろう付けは低温で材料を接合するため、航空宇宙やエレクトロニクス用途の厳しい公差のアセンブリに不可欠な母材特性を維持できることから、メーカーに好まれています。炉ろう付けは、複数の接合部を1回のサイクルで統合するため、連続した溶接工程が不要になり、労力が削減され、歪みも最小限に抑えられます。フィラーの化学的性質が改善され、溶接継手の強度に適合すると同時に高い耐疲労性が得られるようになったため、ろう付けは複雑な薄肉構造に適したプロセスとなっています。自動車部品サプライヤーは、手作業による溶接補修からバッチろう付けに切り替えたことで、アルミニウム・ラジエーター・ラインのタクトタイムが短縮されたと報告しています。OEMがリーン生産方式を推し進める中、この促進要因が中温度域のろう付け合金市場を強化しています。

自動車用熱交換器におけるアルミブレイズ需要の急増

電気自動車とターボチャージャー付き内燃機関は、いずれもコンパクトな熱管理システムを必要とします。アルミシリコンフィラーは、航続距離と燃費に不可欠な軽量化目標を損なうことなく、漏れのない接合部を形成します。A2L冷媒の導入により、接合部の完全性要件が強化され、フィラー量がさらに増加しています。NOCOLOKのようなフラックス技術は、制御雰囲気炉で均一な濡れを実現し、Tier-1熱交換器工場の数百万ユニットの年間処理量を支えています。これらの要因は、短期的にはアルミニウムろうの高い需要につながり、APAC、NAFTA、欧州の自動車クラスターにおけるろう付け合金市場を押し上げます。

ベースメタル価格の変動

銅と銀は、供給のボトルネックとインフラ需要により、急激な価格変動を示します。コスト高騰は、金属をヘッジしたり、コストを顧客に転嫁したりするフィラー生産者の利幅を圧迫し、価格に敏感なHVACや白物家電セクターの受注延期のリスクを招きます。このボラティリティは、一部の加工業者に機械式締結を検討させ、短期的なサイクルではろう付け合金市場に下落圧力をかける。バランスの取れた調達戦略と貴金属含有量の低い合金の改良は、抑制を部分的に相殺するが、エクスポージャーを完全に中和することはできないです。

セグメント分析

銅ベースのフィラーは、2024年には売上の35.86%を占め、自動車、HVAC、一般産業など幅広い分野での応用が可能であることを示しています。ユーザーは銅の熱伝導性、適度な融点、フラックスとの相性を評価しており、ろう付け合金市場はこの金属クラスで安定しています。銀を含むグレードは接合抵抗が重要な高級電子機器に使われ、金合金は過酷な環境での微小腐食のニッチを埋める。

他の卑金属、主にニッケルとコバルトは、その高温安定性がEVバッテリー・モジュールやタービン部品に適しているため、2030年までCAGR4.71%で急速に拡大します。アリゾナ州立大学では、銅とタンタルとリチウムの合金が、800 °C、1万時間で1120 MPaの降伏強度を維持することを実証し、銅の高度な変種への軌道を実証しました。このような開発は、特殊高熱グレードの市場規模を拡大するものであり、銅の量的優位を奪うものではありません。

ロッドとワイヤー製品は2024年のろう付け合金市場の30.94%を占める。MROの技術者たちはトーチ作業でこの馴染みのある形状を頼りにしており、小ロットの加工業者は参入コストの低さを評価しています。粉末、ペースト、箔の各形態は、ニッチな電子機器や航空宇宙産業の接合部に対応し、形状が要求される場合に合金を正確に配置できます。

リングとプリフォームは、再現性を重視する自動車用ラジエーターラインに後押しされ、CAGR 4.97%で進歩しています。予備成形リングは、サイクルタイムを最大30%短縮し、一貫したフィレットサイズを提供することで、検査後の再加工を削減します。ロボット工学の統合により、自動的にピッキング・配置できるプリフォームが好まれ、2030年までろう付け合金市場は平均以上の成長を維持します。

地域分析

アジア太平洋地域は、2024年に世界収益の46.28%を生み出し、CAGR 5.03%で成長すると予測され、同時に最大かつ最速の地域となります。中国のアルミニウム二次製品セグメントは、新エネルギー自動車とインフラに牽引されて年間13%拡大しており、アルミニウムベースのフィラー需要を高めています。日本の精密メーカーと韓国の電子機器組立メーカーが先進的な炉ラインを設置し、地域の専門知識を深めています。賃金上昇とESG規制により、生産能力の一部がベトナムとタイに移りつつあるが、強固なサプライチェーンがAPACをろう付け合金市場の中心に据えています。

北米は、高性能のニッケルやコバルトのフィラーを指定する航空宇宙エンジンや防衛電子機器プログラムに後押しされ、2番手の地位を堅持しています。米国のリショアリング政策とインフレ削減法は、近代的な炉のアップグレードに資本を注ぎ込み、メキシコの自動車輸出はアルミニウムラジエーターの消費を加速させる。熟練労働者の不足と断続的な銅価格の高騰は、絶対的な成長を弱めるが、ろう付け合金市場の勢いは衰えないです。

欧州の成熟した産業基盤は、自動車、HVAC、一般エンジニアリングに安定した需要をもたらします。厳しいRoHSとREACHの要件が、カドミウムフリーと鉛フリーの製品の迅速な採用を後押ししています。ドイツのEVプラットフォーム展開がアルミシリコンフィラーの生産量を刺激し、英国の航空宇宙複合材料クラスターは金属セラミック接合用のアモルファス箔に目を向けています。サーキュラー・エコノミー(循環型経済)指令はリサイクル金属フィラーにニッチを開き、この地域のろう付け合金市場の微妙な成長経路を示します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 溶接やはんだ付けよりもろう付けを採用

- 自動車用熱交換器におけるアルミニウムベースのろう付けの需要が急増

- 低温異種接合を可能にするアモルファス箔合金の台頭

- EVパワーエレクトロニクスにおけるNiベース誘導ペーストの採用

- HVACおよび冷凍業界の成長

- 市場抑制要因

- ベースメタル価格の変動

- 有害金属(Cd、Pb)規制禁止

- 付加製造による代替

- バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- ベースメタル別

- 銅

- 銀

- 金

- アルミニウム

- その他の卑金属(ニッケル、コバルトなど)

- フィラーフォーム別

- 粉

- ペースト

- 箔/リボン

- ロッド/ワイヤー

- リングとプリフォーム

- 温度範囲別

- 低温(450℃未満)

- 中温(450~800℃)

- 高温(800℃以上)

- エンドユーザー業界別

- 自動車

- 航空宇宙および防衛

- 電気・電子工学

- 建設

- その他のエンドユーザー産業(医療機器、エネルギー・電力など)

- 地域別

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/ランキング分析

- 企業プロファイル

- Aimtek, Inc.

- Cupro Alloys Corporation

- Fusion, Inc.

- Indian Solder and Braze Alloys Pvt. Ltd.

- Johnson Matthey

- Lucas-Milhaupt Inc.

- Materion Corporation

- Morgan Advanced Materials plc

- Nihon Superior Co., Ltd.

- OC Oerlikon Management AG

- Prince & Izant Company

- Saru Silver Alloy Private Limited

- Sulzer Ltd

- The Lincoln Electric Company

- Umicore

- VBC Group

- Wieland Group