尿素ホルムアルデヒド樹脂:市場シェア分析、産業動向と統計、成長予測(2025~2030年)

Urea Formaldehyde Resins - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1639503

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

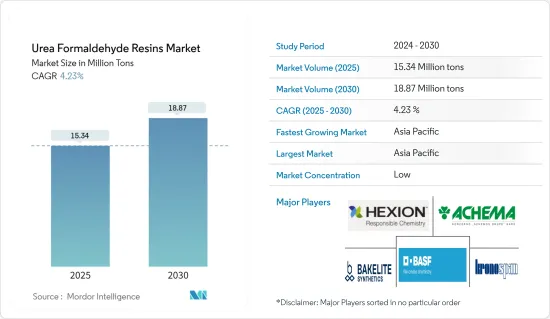

尿素ホルムアルデヒド樹脂市場規模は、2025年には1,534万トンと推定され、予測期間(2025~2030年)のCAGRは4.23%で、2030年には1,887万トンに達すると予測されます。

COVID-19の流行は尿素ホルムアルデヒド市場にマイナスの影響を与えました。世界の封鎖と厳しい政府規制により、ほとんどの生産拠点が閉鎖され、壊滅的な打撃を受けました。それでも市場は2021年に回復し、今後数年間で大幅に上昇すると予想されます。

主要ハイライト

- 短期的には、家具セクターからのパーティクルボード需要の増加と中密度繊維板(MDF)需要の増加が市場の成長を牽引すると予想されます。

- しかし、尿素-ホルムアルデヒド樹脂に関する健康被害が市場成長の妨げになると予想されます。

- 自動車や電化製品における良質な樹脂の需要は、調査対象市場にとって新たな機会を生み出すと予想されます。

- アジア太平洋が世界市場を独占しており、中国とインドからの消費が最も多いです。

尿素ホルムアルデヒド樹脂市場の動向

建築・建設セグメントが市場を独占すると予測

- パーティクルボード、合板、中密度繊維板のような材料に大きく依存する建築・建設セクターは、尿素ホルムアルデヒド樹脂市場の成長の重要な促進要因です。

- 建設活動が活発化するにつれて、これらの建材の需要と生産も増加します。ボードや合板における尿素ホルムアルデヒドの広範な使用は、その重要性を強調し、尿素ホルムアルデヒド市場の全体的な成長を推進しています。

- Oxford Economicsは、世界の建設生産高が堅調な成長軌道を描くと予測しており、2037年までに4兆2,000億米ドル超から13兆9,000億米ドル超に増加すると予測しています。

- アジア太平洋も北米も住宅建設が急増しています。アジア太平洋では、インド、中国、フィリピン、ベトナム、インドネシアといった国々が最先端を走っています。一方、北米の住宅建設は、人口の増加、移民の増加、核家族化の動向に後押しされています。

- 韓国の建設産業は主要な経済貢献者であり、外国為替と輸出収益の重要な源泉です。韓国の国内建設市場規模は、主に民間住宅建設の堅調な伸びによって拡大しています。

- 政府はまた、2025年までにソウルやその他の都市に83万戸の住宅を供給する大規模再開発プロジェクトの実施を計画しています。この計画では、ソウルに32万3,000戸、京畿道と仁川に29万3,000戸が新たに建設されます。釜山、大邱、大田などの大都市も、4年間で22万戸の新築住宅の恩恵を受ける。

- 住宅市場の上昇に伴い、中国とインドを筆頭とするアジア太平洋が、世界の住宅建設ラッシュをリードすることになりそうです。

- 世界の建設投資の20%を占める中国は、2030年までに約13兆米ドルを建築物に投入すると予測されており、ニオブ市場の強気な展望を裏付けています。

- その重要性を認識するインド政府は、13億人の国民のニーズに応えることを目指し、住宅建設への取り組みを強化しています。

- National Real Estate Development Corporation(NAREDCO)の報告によると、2023年には上位7都市で合計43万5,000戸が完成し、2024年には大幅に増加する見込みです。この動向をさらに裏付けるように、ノイダを拠点とする著名な不動産開発業者であるCounty Group,は、今年、3つの野心的な住宅プロジェクトで400万平方フィート超を発表する予定です。

- 北米の建設産業を支配しているのは米国で、カナダとメキシコも多額の投資を行っています。米国国勢調査局によると、米国の新築住宅戸数は2023年に4.46%増加し、2022年の139万500戸から145万2,000戸に達しました。さらに、同国の年間建設額は2023年に1兆9,700億米ドルに達し、2022年の1兆8,400億米ドルから7%増加しました。

- カナダでは、アフォーダブル・ハウジング・イニシアチブ(AHI)、ニュー・ビルディング・カナダ・プラン(NBCP)、メイド・イン・カナダといった政府の取り組みが、建設部門を大幅に強化する構えです。2022年8月、カナダ政府はこれらのイニシアチブに20億米ドルを超える大規模投資を行うことを発表し、相当数の手頃な価格の住宅を含め、全国で約1万7,000戸の住宅開発を目指しました。

- こうした動きを踏まえると、建築・建設部門は予測期間中も市場の主導的地位を維持するものと考えられます。

アジア太平洋が市場を独占する

- 中国とインドを筆頭に、アジア太平洋が世界市場を独占しています。

- 中国は世界トップの尿素ホルムアルデヒド樹脂生産国として極めて重要な役割を果たしています。人口の増加に伴い、中国の農業部門は食糧需要の増加に対応するために進化しています。この進化は肥料の性能と効率にかかっており、尿素ホルムアルデヒド樹脂の消費を押し上げています。

- 世界最大の建設市場を誇る中国は、世界の建設投資の20%を占めています。予測によると、中国は2030年までに約13兆米ドルを建築物に投資する見込みで、堅調な市場展望を示しています。住宅需要の高まりは、高層ビルやホテルの顕著な増加とともに、公共と民間の住宅建設を後押しします。

- 低コストの住宅プロジェクトを加速させるため、香港の住宅当局は、2030年までに30万1,000戸の公共住宅を供給することを目標とする構想を発表しました。

- 建築以外にも、尿素ホルムアルデヒド樹脂は繊維板製造において重要な役割を果たしています。この繊維板は、ダッシュボードやドアシェルのような部品を成形する自動車セグメントで利用されています。中国汽車工業協会(CAAM)が発表した最新データによると、2023年の自動車生産台数は3,016万台を超え、前年比11.6%増となります。2023年の国内乗用車販売台数は3,009万台で、前年比12%増となりました。

- インド自動車製造協会(SIAM)が発表したデータによると、2023年度の自動車生産台数は458万台で、2022年度の生産台数は365万台でした。2023年度の自動車生産台数は前年度比で約25%増加しました。

- インドの電子機器製造部門は着実に成長しており、政府の好意的な施策に後押しされています。これには、100%の外国直接投資(FDI)、産業ライセンス要件の撤廃、自動化生産へのシフトなどが含まれます。2023年8月、インドは国内エレクトロニクス製造を支援するため、1億1,400万米ドルの予算でM-SIPS(Modified Incentive Special Package Scheme)とEDF(Electronics Development Fund)を立ち上げました。

- こうした力学から、アジア太平洋は予測期間を通じて市場の優位性を維持するとみられます。

尿素ホルムアルデヒド樹脂産業概要

世界の尿素ホルムアルデヒド樹脂市場は細分化されています。市場の主要企業(順不同)には、Achema、BASF SE、Hexion、Kronoplus Limited、Bakelite Syntheticsが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 中密度繊維板(MDF)の需要増加

- 家具セクターにおけるパーティクルボード需要の増加

- その他の促進要因

- 抑制要因

- 尿素ホルムアルデヒド樹脂に関する健康被害

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模(数量ベース))

- 用途別

- パーティクルボード

- 木材接着剤

- 合板

- 中密度繊維板

- その他

- エンドユーザー産業別

- 自動車

- 電化製品

- 農業

- 建築・建設

- その他

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- カタール

- アラブ首長国連邦

- ナイジェリア

- エジプト

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Achema

- ARCL Organics Ltd

- Arclin Inc.

- Ashland

- Asta Chemicals

- Bakelite Synthetics

- BASF SE

- Hexion

- Hexza Corporation Berhad

- Jiangsu Sanmu Group Co. Ltd

- Kronoplus Limited

- Melamin kemicna tovarna d.d. Kocevje

- Metadynea Metafrax Group

- QAFCO

- SABIC

第7章 市場機会と今後の動向

- 自動車と民生用電子機器製品における高品質樹脂の需要増加

- その他の機会

目次

The Urea Formaldehyde Resins Market size is estimated at 15.34 million tons in 2025, and is expected to reach 18.87 million tons by 2030, at a CAGR of 4.23% during the forecast period (2025-2030).

The COVID-19 epidemic negatively impacted the urea formaldehyde market. Global lockdowns and severe government rules resulted in a catastrophic setback, as most production hubs were shut down. Nonetheless, the market recovered in 2021 and is expected to rise significantly in the coming years.

Key Highlights

- Over the short term, the growing demand for particle boards from the furniture sector and the increasing demand for medium-density fiberboard (MDF) are expected to drive the market's growth.

- However, health hazards regarding urea-formaldehyde resins are expected to hinder the market's growth.

- Nevertheless, the demand for good-quality resins in automobiles and electrical appliances is expected to create new opportunities for the market studied.

- Asia-Pacific dominates the market globally, with the most consumption from China and India.

Urea Formaldehyde Resins Market Trends

Building and Construction Segment Anticipated to Dominate the Market

- The building and construction sector, heavily dependent on materials like particle boards, plywood, and medium-density fiberboard, is a crucial driver of the urea formaldehyde resin market's growth.

- As construction activities ramp up, so does the demand and production of these building materials. The extensive use of urea-formaldehyde in boards and plywood underscores its importance and propels the overall growth of the urea-formaldehyde market.

- Oxford Economics forecasts a robust growth trajectory for global construction output, projecting an increase from over USD 4.2 trillion to a staggering USD 13.9 trillion by 2037, predominantly fueled by the construction powerhouses of China, the United States, and India.

- Both Asia-Pacific and North America are experiencing a surge in residential construction. Countries like India, China, the Philippines, Vietnam, and Indonesia are at the forefront in Asia-Pacific. Meanwhile, North America's residential construction is buoyed by a growing population, rising immigration, and the trend toward nuclear families.

- South Korea's construction industry is a major economic contributor and an essential source of foreign exchange and export earnings. The size of South Korea's local construction market is expanding mainly due to solid growth in private residential construction.

- The government has also planned to execute large-scale redevelopment projects to supply 830,000 housing units in Seoul and other cities by 2025. From the planned construction, Seoul will get 323,000 new houses, and 293,000 will be built near Gyeonggi Province and Incheon. Major cities like Busan, Daegu, and Daejeon will also benefit with 220,000 new houses in 4 years.

- With housing markets rising, the Asia-Pacific region, spearheaded by China and India, is set to lead the global surge in housing construction.

- China, commanding 20% of the world's construction investments, is projected to channel nearly USD 13 trillion into buildings by 2030, underscoring a bullish outlook for the niobium market.

- Recognizing its significance, the Indian government is ramping up housing construction efforts, aiming to cater to the needs of its 1.3 billion citizens.

- Highlighting India's momentum, the National Real Estate Development Corporation (NAREDCO) reports that the top 7 cities collectively completed 4.35 lakh units in 2023, with 2024 poised for a substantial uptick. Further underscoring this trend, County Group, a prominent Noida-based real estate developer, is set to unveil over 4 million sq. ft across three ambitious housing projects this year.

- The United States dominates the construction industry in North America, with Canada and Mexico also making substantial investments. According to the US Census Bureau, the United States saw a 4.46% increase in new housing units in 2023, reaching 1,452 thousand units, up from 1,390.5 thousand in 2022. Additionally, the annual construction value in the country hit USD 1.97 trillion in 2023, marking a 7% rise from USD 1.84 trillion in 2022.

- In Canada, government initiatives like the Affordable Housing Initiative (AHI), New Building Canada Plan (NBCP), and Made in Canada are poised to bolster the construction sector significantly. In August 2022, the Canadian government unveiled a major investment exceeding USD 2 billion for these initiatives, aiming to develop around 17,000 homes nationwide, including a substantial number of affordable units.

- Given these dynamics, the building and construction segment is poised to retain its leading position in the market during the forecast period.

Asia-Pacific to Dominate the Market

- With China and India at the forefront, the Asia-Pacific region dominates the global market.

- China plays a pivotal role as the world's top producer of urea formaldehyde resins. With its growing population, China's agricultural sector is evolving to meet rising food demands. This evolution hinges on fertilizer performance and efficiency, boosting the consumption of urea formaldehyde resins.

- Boasting the world's largest construction market, China accounts for 20% of global construction investments. Projections indicate that by 2030, China is expected to invest nearly USD 13 trillion in buildings, signaling a robust market outlook. The nation's escalating housing demand is set to bolster public and private residential construction, with a notable uptick in tall buildings and hotels.

- To accelerate low-cost housing projects, Hong Kong's housing authorities have unveiled initiatives targeting the delivery of 301,000 public housing units by 2030.

- Beyond construction, urea formaldehyde resin plays a pivotal role in fiberboard production. This fiberboard finds its application in the automotive sector, shaping components like dashboards and door shells. According to the latest data released by the China Association of Automobile Manufacturers (CAAM), car production in the country it exceeded 30.16 million units in the year 2023, registering an 11.6% increase compared to the previous year. A total of 30.09 million units of passenger cars were sold in the country in 2023, registering a 12% increase compared to last year.

- According to the data released by the Society of India Automotive Manufacturing (SIAM), 4.58 million automotive vehicles were manufactured in the FY2023, compared to 3.65 million vehicles produced in 2022. The country saw a rise of around 25% in automotive production in 2023 compared to the previous year.

- India's electronics manufacturing sector is growing steadily and is driven by favorable government policies. These include 100% Foreign Direct Investment (FDI), no industrial license requirements, and a shift to automated production. In August 2023, India launched the Modified Incentive Special Package Scheme (M-SIPS) and the Electronics Development Fund (EDF), with a budget of USD 114 million to support domestic electronics manufacturing.

- Given these dynamics, the Asia-Pacific region is set to uphold its market dominance throughout the forecast period.

Urea Formaldehyde Resins Industry Overview

The global urea formaldehyde resins market is fragmented in nature. The major players in the market (not in a particular order) include Achema, BASF SE, Hexion, Kronoplus Limited, and Bakelite Synthetics.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Medium Density Fiberboard (MDF)

- 4.1.2 Rising Demand for Particle Board in the Furniture Sector

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Health Hazards Regarding Urea Formaldehyde Resins

- 4.2.2 Other Restraints

- 4.3 Industry Value-chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 By Application

- 5.1.1 Particle Board

- 5.1.2 Wood Adhesives

- 5.1.3 Plywood

- 5.1.4 Medium Density Fiberboard

- 5.1.5 Other Applications

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.2 Electrical Appliances

- 5.2.3 Agriculture

- 5.2.4 Building and Construction

- 5.2.5 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Achema

- 6.4.2 ARCL Organics Ltd

- 6.4.3 Arclin Inc.

- 6.4.4 Ashland

- 6.4.5 Asta Chemicals

- 6.4.6 Bakelite Synthetics

- 6.4.7 BASF SE

- 6.4.8 Hexion

- 6.4.9 Hexza Corporation Berhad

- 6.4.10 Jiangsu Sanmu Group Co. Ltd

- 6.4.11 Kronoplus Limited

- 6.4.12 Melamin kemicna tovarna d.d. Kocevje

- 6.4.13 Metadynea Metafrax Group

- 6.4.14 QAFCO

- 6.4.15 SABIC

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rise in Demand for Good Quality Resins in Automobile and Electrical Appliances

- 7.2 Other Opportunities

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日