|

|

市場調査レポート

商品コード

1639484

海洋向け防汚塗料:市場シェア分析、産業動向と統計、成長予測(2025~2030年)Marine Anti-fouling Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 海洋向け防汚塗料:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

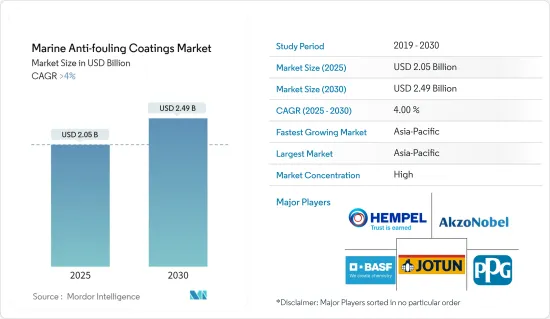

海洋向け防汚塗料の市場規模は2025年に20億5,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは4%を超え、2030年には24億9,000万米ドルに達すると予測されます。

2020年に発生したCOVID-19は、世界の封鎖、サプライチェーンと製造の断絶、生産停止を引き起こし、これらすべてが市場に悪影響を与えました。しかし、2021年半ばには状況が好転し始めたため、予測期間の残りの期間、市場は上昇傾向を再開することができました。

主なハイライト

- 市場が拡大しているのは、レジャーボートやクルーズ船の製造が増え、船の修理やメンテナンスの仕事が増え、石油・ガス産業が買い増しをしているためです。

- 一方、政府の規制が厳しく、高品質で長持ちする製品を購入する人が増えているため、調査対象市場の成長は鈍化しています。

- しかし、人々は高級品により多くのお金を費やすようになっており、新しいコーティングとアプリケーション技術は、予測期間中に調査した市場に機会を開くと思われます。

- 造船業界からの需要が増加しているため、アジア太平洋が市場を独占しています。

海洋向け防汚塗料市場動向

船底塗料セグメントが市場を独占

- 船底防汚塗料の用途は、今回調査された市場の大半を占める。これは、貨物船や旅客船などの海洋船舶や海洋掘削の数が増加しているためです。

- ほとんどの防汚船底塗料は、船やヨットの水中にある部分に塗られます。これにより、船体に付着している部分に生物や微生物が繁殖するのを防ぐことができます。コーティングは見栄えを良くし、長持ちさせる。また、それ自体で汚れを落とすことができたり、落書きに耐えたりといった利点もあります。

- 国連貿易開発会議の統計によると、2023年1月の世界の船舶総数は、100総トン(gt)以上の船舶が約10万5500隻で、そのうち1000gt以上の船舶は5万6500隻だった。ばら積み貨物船、石油タンカー、貨物船が全体の大半(20%)を占めています。船隊が増えれば、腐食から守り、よく固着する船底防汚塗料の需要も増えると思われます。

- UNCTADの統計によると、2023年の世界のトン数の半分強はアジア企業が所有し、次いで欧州が38%、北米が5%となっています。

- 2022年には、中国、韓国、日本が世界の全船舶の約93%を建造すると予想されています。UNCTADの統計によると、船舶リサイクルの86%はバングラデシュ、インド、パキスタンによって行われています。

- 経済分析局によると、米国の水運産業は2022年第1~3四半期に540億米ドル近くを経済にもたらしました。これは前年の同時期の増加額より約35%多いです。

- こうした世界の動向から、造船業界は成長を続けており、船底防汚塗料の需要は今後数年間で増加すると予想されます。

アジア太平洋が市場を独占

- アジア太平洋が世界市場シェアを独占。アジア太平洋は世界最大の船舶生産・修繕地域であり、小型ボート、フェリー、曳船、漁船、タグボートから石油産業用船舶、ばら積み貨物船、旅客船、貨物船、コンテナ船まで、さまざまな種類の船舶に対する高い需要に対応しています。

- アジア太平洋では、日本、中国、韓国などが主要な船舶生産国です。同時に、この地域の他のさまざまな国にも大規模な造船所が存在します。

- 国連貿易開発会議の統計によると、アジア太平洋は2023年に世界の船舶数の50%以上を占めました。同地域の船舶保有数は、全10万5,500隻のうち約5万2,750隻以上です。

- 中国、韓国、日本は造船の中心地と考えられており、造船の約93%がこの3カ国で行われています。それとは別に、船舶のリサイクルは2021年にパキスタン、バングラデシュ、日本でほとんど行われました。

- さらに、工業・情報技術省(MIIT)は、2023年においても中国が引き続き世界トップの造船国であると報告しています。例えば、2023年には、中国の新規受注、造船生産量、手持ち受注がそれぞれ世界の造船市場シェアの50.2%、66.6%、55%を占めました。さらに、2023年の中国の造船生産量は4,232万重量トン(載貨重量トン)で、前年比11.8%増となった。

- 中国工程院の調査によると、2023年の中国の造船完成量は前年比約12%増の4,232万載貨重量トンとなり、他のすべての国の合計を上回った。

- したがって、生産に向けた大量注文は、予測期間中、この地域で最も速いペースで造船業界からの防汚塗料需要を促進する可能性があります。

海洋向け防汚塗料産業の概要

海洋向け防汚塗料市場は、その性質上、少数のプレーヤーが市場需要のかなりの部分を占めており、統合されています。市場の主要企業には、PPG Industries Inc.、Akzo Nobel NV、Hempel A/S、Jotun、BASF SEが含まれる(順不同)。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- レジャーボートとクルーズ船の生産増加

- 船舶の修理・メンテナンス活動の増加

- 石油・ガス産業からの需要急増

- 抑制要因

- 厳しい政府規制

- 高水準耐久製品の使用増加

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- タイプ別

- 銅ベース

- セルフポリシング(銀系)

- ハイブリッド

- その他のタイプ(有機金属、シラン)

- 用途別

- 船底塗料

- タンクコーティング

- その他の用途(ヨット、船舶)

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- タイ

- ベトナム

- インドネシア

- マレーシア

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- トルコ

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- ナイジェリア

- アラブ首長国連邦

- カタール

- エジプト

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)分析**/市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Akzo Nobel NV

- Axalta Coatings Systems

- BASF SE

- Boero

- Chugoku Marine Paints Ltd

- Hempel A/S

- Jotun

- Kansai Paint Co. Ltd

- Lanxess

- Nippon Paint Marine Coatings Co. Ltd

- PPG Industries Inc.

- RPM International Inc.

- The Sherwin-Williams Company

第7章 市場機会と今後の動向

- 高級品への支出の増加

- 新しい革新的コーティングと応用技術

The Marine Anti-fouling Coatings Market size is estimated at USD 2.05 billion in 2025, and is expected to reach USD 2.49 billion by 2030, at a CAGR of greater than 4% during the forecast period (2025-2030).

The COVID-19 outbreak in 2020 caused a global lockdown, a break in supply chains and manufacturing, and a stop in production, all of which negatively impacted the market. However, things started to get better in mid-2021, which allowed the market to resume its upward trend for the remainder of the projected period.

Key Highlights

- The market is growing because more leisure boats and cruise ships are being made, there are more ship repairs and maintenance jobs, and the oil and gas industry is buying more.

- On the other hand, the growth of the market studied is being slowed down by strict government rules and more people buying high-quality, long-lasting products.

- However, people are spending more money on luxury goods, and new coatings and application technology are likely to open up opportunities for the market studied during the forecast period.

- Due to the rising demand from the shipbuilding industry, Asia-Pacific dominated the market.

Marine Anti-fouling Coatings Market Trends

Hull Coatings Segment to Dominate the Market

- Antifouling hull coating applications make up most of the market that was looked at. This is because the number of offshore ships, such as cargo and passenger ships, and offshore drilling is growing.

- Most antifouling hull coatings are put on the parts of a ship or yacht that are underwater. This keeps organisms and microbes from growing in the parts that are attached to the hull. The coatings make things look better and last longer. They also have other benefits, like being able to clean themselves and resisting graffiti.

- According to the United Nations Conference on Trade and Development statistics, the total number of ships in the world in January 2023 was about 1,05,500 vessels of at least 100 gross tons (gt), of which 56,500 ships were over 1000 gt. Bulk carriers, oil tankers, and cargo ships made up the majority of the total (20%). With more fleets, there would be more demand for antifouling hull coatings, which protect against corrosion and stick well.

- The UNCTAD statistics also showed that just over half of the world's tonnage in 2023 was owned by Asian companies, followed by Europe, which accounted for 38%, and North America, which accounted for 5%.

- In 2022, China, the Republic of Korea, and Japan were anticipated to build about 93% of all ships in the world. UNCTAD statistics also showed that 86% of ship recycling was done by Bangladesh, India, and Pakistan together.

- According to the Bureau of Economic Analysis, the water transportation industry in the United States added close to USD 54 billion to the economy in the first three quarters of 2022. This is about 35% more than what was added in the same time period the year before.

- Because of these global trends, the shipbuilding industry has been growing, and the demand for antifouling hull coatings is expected to increase in the coming years.

Asia-Pacific to Dominate the Market

- Asia-Pacific dominated the global market share. Asia-Pacific is the largest ship-producing and ship-repairing region in the world, thereby catering to the high demand for various types of vessels, ranging from small boats, ferries, towboats, fishing vessels, and tugboats to vessels for the oil industry, bulk carriers, passenger ships, cargo ships, and container ships.

- In Asia-Pacific, countries such as Japan, China, and South Korea are the leading producers of vessels. At the same time, large shipyards also exist in various other nations of the region.

- According to the United Nations Conference on Trade and Development statistics, Asia-Pacific accounted for over 50% of the number of ships worldwide in 2023. The region had approximately more than 52,750 ships under its ownership out of a total of 105,500 ships.

- China, the Republic of Korea, and Japan were considered the hubs for shipbuilding, as approximately 93% of the shipbuilding happened in these three countries. Apart from that, the recycling of ships was mostly done in Pakistan, Bangladesh, and Japan in 2021.

- Moreover, the Ministry of Industry and Information Technology (MIIT) reported that China continued to be the world's leading shipbuilder in 2023. For instance, in 2023, the country's newly received orders, shipbuilding output, and orders on hand accounted for 50.2%, 66.6%, and 55%, respectively, of the global shipbuilding market share. Furthermore, China's shipbuilding output for 2023 was 42.32 million dwt (deadweight tonnage), a rise of 11.8% Y-o-Y.

- According to research by the Chinese Academy of Engineering, Chinese shipbuilding completions in 2023 grew by about 12% Y-o-Y to 42.32 million deadweight tonnes, higher than all other countries combined.

- Hence, bulk orders in line for production may drive the demand for antifouling coatings from the shipbuilding industry at the fastest rate in the region during the forecast period.

Marine Anti-fouling Coatings Industry Overview

The marine antifouling coatings market is consolidated by its very nature, with a small number of players accounting for a sizable portion of market demand. Some of the major players in the market include (not in any particular order) PPG Industries Inc., Akzo Nobel NV, Hempel A/S, Jotun, and BASF SE.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Production of Leisure Boats and Cruise Ships

- 4.1.2 Increase in Ship Repairs and Maintenance Activities

- 4.1.3 Surging Demand from Oil and Gas Industry

- 4.2 Restraints

- 4.2.1 Stringent Government Regulations

- 4.2.2 Increased Usage of High-standard Durable Products

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Type

- 5.1.1 Copper-based

- 5.1.2 Self-polishing (Silver-based)

- 5.1.3 Hybrid

- 5.1.4 Other Types (Organo Metallic, Silane)

- 5.2 By Application

- 5.2.1 Hull Coatings

- 5.2.2 Tank Coatings

- 5.2.3 Other Applications (Yachts and Vessels)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Thailand

- 5.3.1.6 Vietnam

- 5.3.1.7 Indonesia

- 5.3.1.8 Malaysia

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Turkey

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 United Arab Emirates

- 5.3.5.5 Qatar

- 5.3.5.6 Egypt

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis**/Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Akzo Nobel NV

- 6.4.2 Axalta Coatings Systems

- 6.4.3 BASF SE

- 6.4.4 Boero

- 6.4.5 Chugoku Marine Paints Ltd

- 6.4.6 Hempel A/S

- 6.4.7 Jotun

- 6.4.8 Kansai Paint Co. Ltd

- 6.4.9 Lanxess

- 6.4.10 Nippon Paint Marine Coatings Co. Ltd

- 6.4.11 PPG Industries Inc.

- 6.4.12 RPM International Inc.

- 6.4.13 The Sherwin-Williams Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Expenditure on Luxury Goods

- 7.2 New Innovative Coatings and Application Technology