|

市場調査レポート

商品コード

1639434

世界のフッ素エラストマー-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Global Fluoro Elastomers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 世界のフッ素エラストマー-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

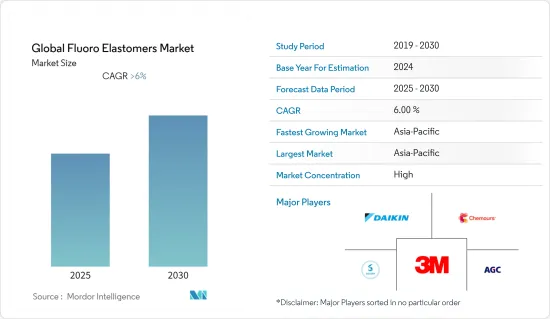

フッ素エラストマーの世界市場は、予測期間中に6%を超えるCAGRで推移する見込みです。

COVID-19の発生により、世界各地で操業停止、製造活動やサプライチェーンの混乱、生産停止が発生し、市場に悪影響を与えました。しかし、状況は回復に向かい、予測期間中に市場の成長軌道を回復しました。

主要ハイライト

- 市場成長の主要要因は、シーリング用途での使用量の増加と自動車産業での用途の急増です。

- 厳しさを増す環境法と危険な労働環境が市場の成長を鈍らせる可能性が高いです。

- 今後数年間で、市場はパーフッ素カーボンエラストマーの新しい使用方法を活用できるようになるはずです。

- アジア太平洋が市場を独占し、予測期間中に最も高いCAGRで推移すると予想されます。

フッ素エラストマー市場動向

フッ素カーボンエラストマー需要の増加

- フッ素カーボンエラストマーは、フッ素を多く添加した炭素ベースのポリマーです。過酷な化学品やオゾンに耐える必要がある場所で使用されます。しかし、フッ素含有量が高く、低温特性が得られる特殊グレードのフッ素カーボンもあります。

- フッ素カーボンエラストマーは、シール製造において極めて重要な役割を果たすようになりました。幅広い化学的適合性、広い温度範囲、低圧縮永久ひずみ、優れた老化特性により、フッ素カーボンゴムは長年にわたって開発された最も重要なエラストマーです。

- フッ素カーボンは、エラストマーよりも幅広い化学品に耐性があり、高温でも優れた性能を発揮します。このため、フッ素カーボンで作られたOリングやその他のカスタムシールは、世界中で他タイプのエラストマーよりも頻繁に使用されています。

- これらのエラストマーは、ガソリンや紫外線、オゾンにさらされても膨潤したり分解したりすることがありません。フッ素カーボンエラストマーは4°Fで硬くなりますが、低温でも使用できます。しかし、これらのコンパウンドは、低温で優れた柔軟性が必要な用途には適していないです。

- さらに、モノマーの組成やフッ素含有量(低温・高温や化学品に対する耐性を向上させるために65~71%)の異なる他の材料も存在します。フッ素カーボンエラストマーはガス透過性が低いため、真空サービス用途やその他多くの産業用途に適しています。

- 防衛省は、極限の耐久条件下で安定性を発揮する最高品質の部品を必要とする高性能機械の製造にフッ素カーボンエラストマーを使用しています。フッ素カーボンエラストマーは、航空宇宙産業や自動車産業にもソリューションを提供しています。

- 米国では2021年に航空機の数が増加し、一般航空会社の保有機数は204,405機、ハイヤー航空会社の保有機数は5,815機に減少しました。米国は世界最大の航空市場のひとつです。米国の航空会社によって輸送される人の数は、他のどの国の航空会社よりも多く、世界で収益をあげている航空会社上位10社の約半数が米国を拠点としています。

- 中国国内の商業航空産業の繁栄は、所得、観光、ビジネス活動の上昇の結果であり、これらはすべて国内旅行と国際旅行の促進要因です。中国民用航空局は、2035年までに合計450の大規模な商業サービス空港が存在することになると発表しています。つまり、民間航空は今後も成長を続けると予想されます。

- 2021年6月までに、中国で運航されている一般航空機の数は3,066機で、2020年と比べて4%増加しました。2014年以降、中国における一般航空機の数は103%近く着実に増加しています。

- これらの要因から、フッ素エラストマー市場は予測期間中、世界中で成長すると予想されます。

アジア太平洋が市場を独占

- アジア太平洋が市場を独占すると予想されます。中国とインドは、この地域で最大の経済大国です。同国の製造部門は世界最大級の生産拠点となっており、フッ素エラストマーに莫大な需要をもたらしています。

- フッ素エラストマーは、油圧Oリングシール、逆止弁ボール、ダイヤフラム、工業用ロールカバー、Vリングパッカーなどの製造に、工業と化学処理産業で使用されています。

- 国家統計局によると、中国の製造業生産高は2021年には31兆4,000億人民元(4兆6,400億米ドル)に成長し、世界の製造業の約30%にまで増加しました。

- 中国の航空機産業はここ数年、著しい成長を遂げています。Boeingによると、中国の航空会社は8,700機の新型機を必要とし、これは前年度の予測8,600機より1.2%多いです。2040年には1兆4,700億米ドルに達すると考えられます。

- OICAによると、2021年の自動車総生産台数は8,015万台で、前年比3%増となりました。これらの要因から、同地域のフッ素エラストマー市場は予測期間中に安定した成長が見込まれます。

フッ素エラストマー産業概要

フッ素エラストマー市場は部分的に統合されています。市場の主要企業(順不同)には、3M、Daikin Industries, Ltd.、Solvay、The Chemours Company、AGC Inc.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- シーリング用途での用途拡大

- 自動車産業における用途の急増

- 抑制要因

- 厳しさを増す環境規制と危険な作業環境

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模(数量ベース))

- 製品タイプ

- フッ素カーボンエラストマー

- フッ素シリコーンエラストマー

- パーフッ素カーボンエラストマー

- 用途

- ダイヤフラム

- バルブ

- Oリング、シール、シーラント

- その他の用途(フューエルホース、ジョイント)

- エンドユーザー産業

- 自動車

- 航空宇宙

- 石油・ガス

- 産業用

- その他のエンドユーザー産業(化学、防衛)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他の欧州

- その他

- ブラジル

- サウジアラビア

- 南アフリカ

- その他

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- 3M

- AGC Inc.

- All Seals Inc.

- Daikin Industries Ltd

- Eagle Elastomer Inc.

- Freudenberg Sealing Technologies

- GARLOCK

- Gujarat Fluorochemicals Limited

- HaloPolymer

- KUREHA CORPORATION

- LANXESS

- Minor Rubber Products

- Parker Hannifin Corp.

- Precision Associates, Inc.

- Shanghai Fluoron Chemicals Co.Ltd.

- Solvay

- Stockwell Elastomerics Inc.

- The Chemours Company

- Trp Polymer Solutions Limited

- Zhonghao Chenguang Research Institute of Chemical Industry

- Zrunek Gummiwaren GmbH

第7章 市場機会と今後の動向

- パーフッ素カーボンエラストマーの新規用途

The Global Fluoro Elastomers Market is expected to register a CAGR of greater than 6% during the forecast period.

Due to the COVID-19 outbreak, there were nationwide lockdowns around the world, disruptions in manufacturing activities and supply chains, and production halts that negatively impacted the market. However, the conditions started recovering, restoring the market's growth trajectory during the forecast period.

Key Highlights

- The major factors driving the market's growth are rising usage in sealing applications and the surge in applications in the automotive industry.

- Environmental laws that are getting stricter and dangerous working conditions are likely to slow the growth of the market.

- In the coming years, the market should be able to take advantage of new ways to use perfluorocarbon elastomers.

- The Asia-Pacific region is expected to dominate the market and to register the highest CAGR during the forecast period.

Fluoroelastomers Market Trends

Increasing Demand for Fluorocarbon Elastomers

- Fluorocarbon elastomers are carbon-based polymers that have a lot of fluorine added to them. They are used in places where they need to be resistant to harsh chemicals and ozone. There are, however, specialty-grade fluorocarbons that can provide high fluorine content with low-temperature properties.

- Fluorocarbon elastomers have become of vital importance in seal manufacturing. Due to its wide chemical compatibility, wide temperature range, low compression set, and excellent aging characteristics, fluorocarbon rubber is the most significant single elastomer developed over the years.

- Fluorocarbons are more resistant to a wider range of chemicals and work better at high temperatures than elastomers. Because of this, O-rings and other custom seals made from fluorocarbons are used more often than other types of elastomers around the world.

- These elastomers are very resistant to swelling and breaking down when they are exposed to gasoline, UV light, and ozone. Fluorocarbon elastomers can get hard at 4 °F, but they can still be used at low temperatures. However, these compounds are not ideal for applications that need good flexibility at low temperatures.

- Additionally, some of the other materials are also present with a differing composition of monomers and fluorine content (65-71% for improved resistance against low and high temperatures or chemicals). Fluorocarbon elastomers provide low gas permeability, making them suitable for vacuum service applications and many other industrial applications.

- The Ministry of Defense uses fluorocarbon elastomers to build high-performance machinery that needs premium quality components to provide stability in extreme endurance conditions. Fluorocarbon elastomers also offer a solution to the aerospace and automotive industries.

- In the United States, the number of aircraft increased in 2021; the general aviation fleet was 204,405 and the for-hire carrier fleet decreased to 5,815 aircraft. The United States has one of the world's largest aviation markets. More people are transported by U.S. airlines than by airlines from any other nation, and about half of the top ten revenue-generating airlines in the globe are based in the United States.

- A thriving domestic Chinese commercial aviation industry is the result of rising incomes, tourism, and business activity, which are all driving factors in domestic and international travel. The Civil Aviation Administration of China says that by 2035, there will be a total of 450 large commercial service airports. This means that commercial aviation is expected to keep growing.

- By June 2021, there were 3,066 general aviation aircraft operating in China, an increase of four percent compared to 2020. Since 2014, the number of general aviation aircraft in China has grown steadily by nearly 103 percent.

- Owing to all these factors, the market for fluoroelastomers is expected to grow across the world during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is expected to dominate the market. China and India are among the region's largest economies. The country's manufacturing sector has become one of the biggest production houses in the world, thus providing huge demand for fluoroelastomers.

- Fluoroelastomers are used in the industrial and chemical processing industries to make things like hydraulic O-ring seals, check valve balls, diaphragms, industrial roll covers, V-ring packers, and so on.

- According to the National Bureau of Statistics, China's manufacturing output grew to CNY 31.4 trillion (USD 4.64 trillion) in 2021, up from around 30% of the global manufacturing sector.

- The Chinese aircraft industry has depicted significant growth over the years. According to Boeing, Chinese airlines will need 8,700 new airplanes, 1.2% more than its previous prediction of 8,600 planes made the previous year. These would be worth USD 1.47 trillion by 2040.

- Nearly 60% of the world's cars are made in this area, making it the biggest center for making cars.According to OICA, the total production of vehicles stood at 80.15 million units in 2021, an increase of 3% compared to the previous year.

- Due to all these factors, the fluoroelastomers market in the region is expected to have steady growth during the forecast period.

Fluoroelastomers Industry Overview

The fluoroelastomers market is partially consolidated in nature. Some of the major players (not in any particular order) in the market include 3M, Daikin Industries Ltd, Solvay, The Chemours Company, and AGC Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Usage in Sealing Applications

- 4.1.2 Surging Applications in the Automotive Industry

- 4.2 Restraints

- 4.2.1 Increasingly Stringent Environmental Regulations and Hazardous Working Conditions

- 4.2.2 Other Restraints

- 4.3 Industry Value-chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Product Type

- 5.1.1 Fluorocarbon Elastomers

- 5.1.2 Fluorosilicone Elastomers

- 5.1.3 Perfluorocarbon Elastomers

- 5.2 Application

- 5.2.1 Diaphragms

- 5.2.2 Valves

- 5.2.3 O-rings, Seals, and Sealants

- 5.2.4 Other Applications (Fuel Hoses, Joints)

- 5.3 End-user Industry

- 5.3.1 Automotive

- 5.3.2 Aerospace

- 5.3.3 Oil and Gas

- 5.3.4 Industrial

- 5.3.5 Other End-user Industries (Chemical, Defense)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 Rest of the World

- 5.4.4.1 Brazil

- 5.4.4.2 Saudi Arabia

- 5.4.4.3 South Africa

- 5.4.4.4 Rest of the World

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 AGC Inc.

- 6.4.3 All Seals Inc.

- 6.4.4 Daikin Industries Ltd

- 6.4.5 Eagle Elastomer Inc.

- 6.4.6 Freudenberg Sealing Technologies

- 6.4.7 GARLOCK

- 6.4.8 Gujarat Fluorochemicals Limited

- 6.4.9 HaloPolymer

- 6.4.10 KUREHA CORPORATION

- 6.4.11 LANXESS

- 6.4.12 Minor Rubber Products

- 6.4.13 Parker Hannifin Corp.

- 6.4.14 Precision Associates, Inc.

- 6.4.15 Shanghai Fluoron Chemicals Co.Ltd.

- 6.4.16 Solvay

- 6.4.17 Stockwell Elastomerics Inc.

- 6.4.18 The Chemours Company

- 6.4.19 Trp Polymer Solutions Limited

- 6.4.20 Zhonghao Chenguang Research Institute of Chemical Industry

- 6.4.21 Zrunek Gummiwaren GmbH

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Novel Applications of Perfluorocarbon Elastomers