|

市場調査レポート

商品コード

1939008

炭酸カルシウム:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Calcium Carbonate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 炭酸カルシウム:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

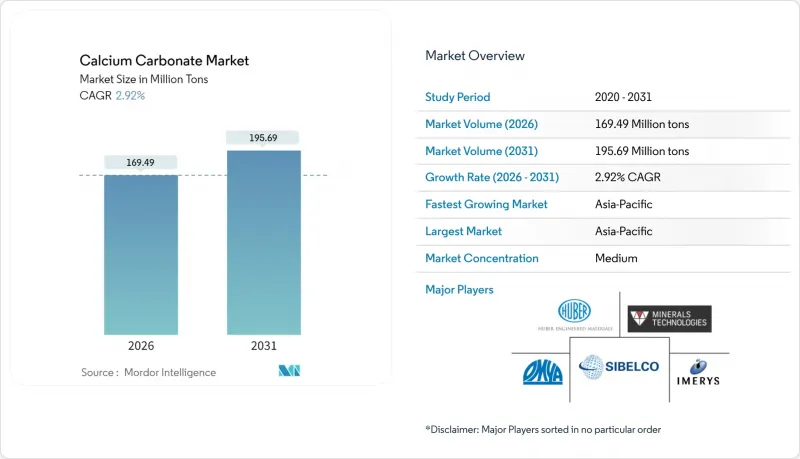

2026年の炭酸カルシウム市場規模は1億6,949万トンと推定され、2025年の1億6,468万トンから成長が見込まれます。

2031年の予測値は1億9,569万トンで、2026年から2031年にかけてCAGR2.92%で拡大する見通しです。

この着実な数量ベースの成長は、プラスチック、紙、建設資材、医薬品、農業分野において、コスト削減用充填剤かつ性能向上剤として確立された本鉱物の役割を裏付けております。新興国におけるインフラ投資の増加、電子商取引に伴う包装・紙製品の持続的な需要、カルシウムサプリメントを配合した健康・栄養製品への着実な移行が、需要をさらに強化しております。鉱山から応用までの一貫生産能力を有するメーカーは、有利な物流体制と最終用途仕様に合わせたグレード調整能力の恩恵を受けております。一方、環境規制の強化により、省エネルギー型粉砕設備、低炭素沈殿ライン、再生石灰岩原料への投資が加速し、主要地域全体でコスト構造の再構築が進んでおります。

世界の炭酸カルシウム市場の動向と展望

建設・インフラ開発の加速

アジア太平洋地域における公共事業支出の急増は、建設業者がセメント、ポリマー改質コンクリート、建築用塗料、シーラント向けのコスト効率の高い鉱物フィラーを求める中、炭酸カルシウム市場を後押ししています。統合生産者はこの需要に対応するため生産能力を拡大:イメリスはアラバマ州サイラカウガ工場の生産量を倍増させ、建設用グレード材料の供給と北米顧客へのリードタイム改善を図りました。都市計画担当者による低炭素建材の推進も、ReMined(100%プレコンシューマー再生炭酸カルシウム)などの製品需要を増加させています。この製品は、強度と耐久性の基準を維持しながら、製品に内在する炭素量を削減します。こうした持続可能性に関連するニッチ市場により、販売業者は大量販売が着実に増加する中でも、より高い利益率を確保することが可能となります。

プラスチック・ポリマー用途の拡大

ナノスケール粉砕技術と表面処理化学の急速な進歩により、フィルム・マスターバッチ・エンジニアリングプラスチックグレードの性能限界が向上しました。ナノ炭酸カルシウムは包装材の引張強度・バリア性・熱安定性を高めつつ透明性を維持するため、コンバーターは樹脂使用量を重量比で最大5%削減できます。中国メーカーの湖北微晶新材料は、生分解性ポリマー中に分散した100ナノメートル未満の粒子により、フィルムの強化と分解速度の微調整を同時に実現する手法を実証し、循環型経済包装の要件を直接支援しています。自動車メーカーや電子機器ブランドは、軽量化、耐熱性、リサイクル性の目標達成に向け、こうした機能性フィラーの採用を拡大しています。

炭酸カルシウムに関連する健康被害

粉塵を吸入する可能性のある炭酸カルシウム粉塵への労働者曝露により、規制監視が強化され、工場や下流プラントにおける許容曝露限界値の引き下げや、より厳格な封じ込め基準が求められています。ナノ粒子の毒性学は現在も研究中であり、食品や医薬品用途の承認には、現在では広範なリスク評価が日常的に必要とされ、これが商品化のタイムラインを延長し、コンプライアンスコストを増加させる可能性があります。資本が限られている小規模生産者は、クローズドループ処理や高効率ろ過装置の導入に苦労することが多く、供給の柔軟性を制約しています。

セグメント分析

粉砕炭酸カルシウムは、豊富な石灰岩鉱床と低エネルギー製粉プロセスにより、2025年の需要の76.92%を占め、炭酸カルシウム市場の中核であり続けております。基礎紙、ポリオレフィンフィルム、レディーミクストコンクリートなどの大量消費分野では、粉砕炭酸カルシウムの優れたコストパフォーマンスが決定的な要因となっております。しかしながら、沈殿炭酸カルシウム(PCC)は、粒子径分布の狭さ、高い輝度、カスタマイズ可能な表面化学特性に対して顧客がプレミアムを支払うことから、2031年までCAGR3.31%で成長ペースを加速させております。この変化は、研究者が大豆ウレアーゼを用いた酵素誘起沈殿を実現したことで顕著となり、PCCの適用範囲を拡大する可能性のあるコスト削減経路を示唆しております。

成熟したGCCメーカーは、炭酸反応装置の高額な設備投資を回避しつつPCC性能に近づけるため、分級粉砕システムや乾式コーティング装置を備えたプラントの改造を進めています。一方、PCCサプライヤーは、多国籍顧客にとって重要性を増す調達基準であるカーボンフットプリント削減に向け、自社内二酸化炭素回収設備と再生可能エネルギー投入量の拡大を進めています。こうした戦略が収束する中、競争は激化していますが、建設、プラスチック、ライフサイエンス産業における需要プロファイルの差異を考慮すると、両サブセグメントの炭酸カルシウム市場規模は着実に拡大すると予測されます。

本カルシウムカーボン酸レポートは、タイプ別(微粉砕炭酸カルシウム、沈殿炭酸カルシウム)、用途別(建設資材用原料、栄養補助食品、熱可塑性プラスチック添加剤、充填剤・顔料など)、エンドユーザー産業別(製紙、プラスチック、接着剤・シーラント、建設など)、地域別(アジア太平洋、北米、欧州、南米、中東・アフリカ)に分析されています。

地域別分析

アジア太平洋地域は2025年に炭酸カルシウム市場の48.25%を占め、2031年までCAGR3.62%で拡大すると予測されています。中国は地域需要の大部分を占めており、イメリスは蕪湖、清陽、岳陽に施設を運営し、包装、建設、ライフサイエンス分野の顧客に供給しています。東南アジア諸国でもコート紙やPVCパイプの生産能力が拡大しており、地域の需要基盤が広がっています。

北米は、テクニカルグレードを優先し厳格な品質管理を特徴とする先進的なプラスチック・医薬品サプライチェーンにより、確固たる基盤を維持しています。アラバマ州とジョージア州における最近の投資は、輸送時の排出量を削減し迅速な技術サポートを確保する現地調達への同地域の意欲を裏付けています。欧州では、厳格な炭素削減規制と採石場復元規則により、再生原料と省エネルギー型沈殿プラントが重要視されています。南米では、ブラジルとアルゼンチンの建設ブームに加え、農業ビジネスの成長が土壌処理剤の消費を押し上げています。中東では石油化学コンビナートや大規模インフラプロジェクトからの安定した需要が見込まれます。一方、アフリカの採石ポテンシャルは未開発ながら有望であり、特にエジプト、ナイジェリア、南アフリカが注目されます。高品質石灰岩鉱床の地理的分散は今後も貿易フローや地域価格に影響を与え続けますが、現地設置型沈殿プラントや高度化された粉砕拠点の整備により、世界の炭酸カルシウム市場における輸送負荷は徐々に軽減されつつあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 建設・インフラ開発の加速

- プラスチックおよびポリマー用途の拡大

- 紙・包装産業からの需要拡大

- 医療・医薬品分野における使用量の増加

- 市場抑制要因

- 炭酸カルシウムに関連する健康被害

- 環境規制および鉱業規制

- 物流およびサプライチェーン上の課題

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替製品・サービスの脅威

- 競合の程度

- 輸入・輸出貿易統計

第5章 市場規模と成長予測

- タイプ

- 微粉砕炭酸カルシウム(GCC)

- 沈殿炭酸カルシウム(PCC)

- アプリケーション

- 建設資材用原料

- 栄養補助食品

- 熱可塑性プラスチック用添加剤

- 充填剤および顔料

- 接着剤の構成要素

- 燃料ガスの脱硫処理

- 土壌中の中和剤

- その他の用途

- エンドユーザー産業

- 紙

- プラスチック

- 接着剤およびシーラント

- 建設

- 塗料およびコーティング

- 医薬品

- 自動車

- 農業

- ゴム

- その他のエンドユーザー産業

- 地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ASEAN諸国

- オーストラリアおよびニュージーランド

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- ロシア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東

- サウジアラビア

- アラブ首長国連邦

- イラン

- イラク

- クウェート

- カタール

- その他中東諸国

- アフリカ

- 南アフリカ

- その他アフリカ

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/順位分析

- 企業プロファイル

- ACCM

- GCCP Resources Limited

- Gulshan Polyols Ltd.

- Huber Engineered Materials

- Imerys

- Jordan Carbonate Company

- Manaseer Group

- Minerals Technologies Inc.

- Nigtas

- OKUTAMA KOGYO CO.,LTD.

- Omya International AG

- Provencale SA

- SaudiCarbonate

- SCHAEFER KALK GmbH & Co. KG

- Shiraishi Group

- Sibelco

- SigmaRoc Plc

- VMPC Joint Stock Company.

- Zantat Sdn. Bhd.