欧州のボイラー水処理化学品:市場シェア分析、産業動向、成長予測(2025年~2030年)

Europe Boiler Water Treatment Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1637765

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

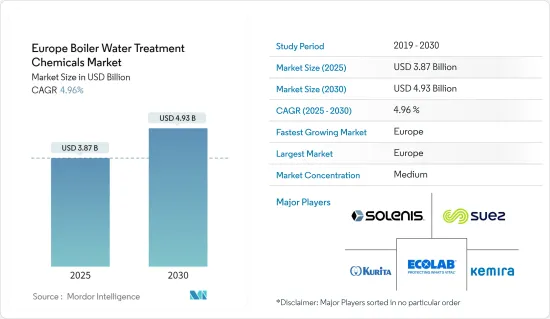

欧州のボイラー水処理化学品の市場規模は2025年に38億7,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは4.96%で、2030年には49億3,000万米ドルに達すると予測されています。

COVID-19の流行は水処理化学品セクターに打撃を与えました。世界の封鎖と政府による厳しい規則により、ほとんどの生産拠点が閉鎖され、壊滅的な打撃を受けました。それにもかかわらず、2021年以降事業は回復しており、今後数年間で大幅に上昇すると予想されます。

主なハイライト

- ボイラー水処理化学品の消費を牽引している主な要因としては、発電・加工産業での使用加速とブローダウン液の普及が挙げられます。

- しかし、ヒドラジンの危険な性質が、予測期間中の市場調査を抑制すると予想されます。

- グリーンケミカルの使用と化学技術の開発に焦点が移っていることが、予測期間中の市場に大きな成長機会をもたらすと思われます。

- 欧州諸国の中では、英国が現在最大の市場シェアを占めており、予測期間中も市場を独占すると予想されます。

欧州のボイラー水処理化学品市場動向

発電産業が市場を独占

- 欧州のボイラー水処理化学品市場の大半を支配しているのは発電産業です。発電産業は産業廃水の主要な生産者です。

- その排水は、鉛、水銀、ヒ素、クロム、カドミウムなどの危険な金属汚染物質で汚染されています。これらの汚染物質は、適切に管理されなければ、環境に重大な害を及ぼす可能性があります。

- 欧州全域、特にドイツ、フランス、英国では電力需要が高いです。電力需要の増加に伴い、発電産業のボイラー水処理化学品消費量は増加すると予測されています。

- 国際エネルギー機関(IEA)の月次統計によると、2023年2月の欧州の総電力生産量は284.756TWhでした。

- IEAはまた、再生可能エネルギーの発電量が最も多く、2023年2月の発電量の59.25TWhを占め、次いで原子力エネルギー(53.71TWh)、風力エネルギー(50.78TWh)であったことを示しました。

- 欧州連合理事会によると、EUは2022年に2,641TWhの電力を生産しました。このうち40%近くが再生可能エネルギーによるものです。原子力エネルギーが20%以上を占め、化石燃料が38.6%を占めました。化石燃料の中で最も多く利用されているのはガス(19.6%)であり、次いで石炭(15.8%)です。

- したがって、上記の要因から、予測期間中は発電産業が市場を独占する可能性が高いです。

市場を独占する英国

- エンドユーザー部門からの需要が大きいため、欧州のボイラー水処理化学品市場では英国が最も高いシェアを占めています。

- 英国では、環境と人々の健康保護が極めて重要です。その重要性から、効果的な水・廃水処理システムが構築され、ドイツでは実質的にすべての廃水がEUの最高基準を満たすように処理されています。

- 飲食品産業、化学製造、発電は、英国で確立されたセクターであり、将来的にボイラー水処理用化学薬品の使用を押し上げると思われます。

- 国際エネルギー機関(IEA)によると、2023年2月の英国の総電力生産量は約24.19 TWhです。また、2022年の英国の総電力生産量は約318.38TWhでした。

- また、世界鉄鋼協会の発表によると、同国における2022年の粗鋼生産量は596万トンでした。

- 国家統計局(英国)によると、英国における2022年の食品・非アルコール飲料への消費支出は1,267億3,000万ポンド(1,567億米ドル)に達し、前年比約3.2%増となった。

- したがって、上記の要因により、予測期間中、英国が欧州のボイラー水処理化学品市場を独占する可能性が高いです。

欧州のボイラー水処理化学品産業の概要

欧州のボイラー水処理化学品市場は適度に断片化されています。同市場の主要企業には、エコラボ、スエズ、栗田工業、ソレニス、ケミラなどがある(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 電力産業からの需要増加

- ブローダウン液の人気の高まり

- その他の促進要因

- 抑制要因

- ヒドラジンの危険性

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- タイプ別

- スケール・腐食抑制剤

- 凝固剤と凝集剤

- pHブースター

- 脱酸素剤

- その他

- 化学別

- 基礎化学品

- ブレンド/特殊化学品

- エンドユーザー産業別

- 発電

- 鉄鋼・金属産業

- 石油精製

- 化学・石油化学

- 繊維・染料産業

- 製糖工場

- 製紙工場

- 飲食品工場

- 施設

- 製薬

- その他エンドユーザー産業

- 地域別

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Aries Chemical, Inc.

- BASF SE

- Buckman

- Cannon Water Technology

- Eastman Chemical Compnay

- Ecolab

- Kemira

- Kurita Water Industries Ltd.

- Lenntech B.V.

- Solenis

- Suez

- Veolia Water Technologies

第7章 市場機会と今後の動向

- グリーンケミカルへのシフト

- 化学技術の開発

目次

The Europe Boiler Water Treatment Chemicals Market size is estimated at USD 3.87 billion in 2025, and is expected to reach USD 4.93 billion by 2030, at a CAGR of 4.96% during the forecast period (2025-2030).

The COVID-19 epidemic harmed the water treatment chemicals sector. Global lockdowns and severe rules enforced by governments resulted in a catastrophic setback as most production hubs were shut down. Nonetheless, the business is recovering since 2021 and is expected to rise significantly in the coming years.

Key Highlights

- A few of the major factors driving the consumption of boiler water treatment chemicals are the accelerating usage in power generation and processing industries and the growing popularity of blowdown liquids.

- However, the hazardous nature of hydrazine is expected to restrain the market studied during the forecast period.

- The shifting focus on the usage of green chemicals and development in chemical technology will likely provide a major growth opportunity for the market studied during the forecast period.

- Among the European countries, the United Kingdom currently accounts for the largest market share and is expected to dominate the market during the forecast period.

Europe Boiler Water Treatment Chemicals Market Trends

Power Generation To Dominate the Market

- The power generation industry controls most European boiler water treatment chemicals market. The electric power generation industry is a major producer of industrial wastewater.

- Its effluent is contaminated with dangerous metal pollutants such as lead, mercury, arsenic, chromium, and cadmium. These contaminants, if not well controlled, can cause significant environmental harm.

- Electricity is in high demand throughout Europe, particularly in Germany, France, and the United Kingdom. The power production industry's boiler water treatment chemicals consumption is projected to increase as the electricity demand continues to rise.

- According to the International Energy Agency's (IEA) monthly figures, total electricity production in Europe in February 2023 was 284.756 TWh, while total electricity production in the first two months of 2023 was more than 602 TWh.

- The IEA also showed that renewable energy produced the most power, accounting for 59.25 TWh of electricity produced in February 2023, followed by nuclear energy (53.71 TWh) and wind energy (50.78 TWh).

- According to the European Union Council, the EU produced 2,641 TWh of electricity in 2022. Nearly 40% of this was derived from renewable sources. Nuclear energy accounted for more than 20%, with fossil fuels accounting for 38.6%. Gas was the most often utilized fossil fuel to create power (19.6%), followed by coal (15.8%).

- Hence, the power generation industry will likely dominate the market during the forecast period due to the abovementioned factors.

United Kingdom to Dominate the Market

- Due to considerable demand from end-user sectors, the United Kingdom includes the highest share of the European boiler water treatment chemicals market.

- Environmental and human health protection is vitally important in the United Kingdom. Its importance resulted in effective water and wastewater treatment systems and practically all wastewater in Germany is treated to satisfy the highest European Union standards.

- The food and beverage industry, chemical manufacture, and power generation are well-established sectors in the United Kingdom that would boost the use of boiler water treatment chemicals in the future.

- According to the International Energy Agency (IEA), the total electricity production in the United Kingdom in February 2023 was about 24.19 TWh. Moreover, the total electricity production in 2022 was about 318.38 TWh in the United Kingdom.

- Moreover, the total crude steel production in the country accounted for 5.96 million tons of crude steel during the year 2022, as stated by the World Steel Association.

- According to the Office for National Statistics (United Kingdom), consumer spending on food and non-alcoholic drinks in the United Kingdom reached GBP 126.73 billion (USD 156.7 billion) in 2022, approximately 3.2% more than the previous year's consumption.

- Thus, the United Kingdom will likely dominate the European boiler water treatment chemicals market during the forecast period due to the abovementioned factors.

Europe Boiler Water Treatment Chemicals Industry Overview

The European boiler water treatment chemicals market is moderately fragmented. Some of the major players in the market include (not in any particular order) Ecolab, Suez, Kurita Water Industries Ltd, Solenis, and Kemira, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from Power Industry

- 4.1.2 Growing Popularity of the Blowdown Liquids

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Hazardous Nature of Hydrazine

- 4.2.2 Other Restraints

- 4.3 Industry Value-chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Scale and Corrosion Inhibitors

- 5.1.2 Coagulants and Flocculants

- 5.1.3 pH Boosters

- 5.1.4 Oxygen Scavengers

- 5.1.5 Others

- 5.2 Chemistry

- 5.2.1 Basic Chemicals

- 5.2.2 Blended/Specialty Chemicals

- 5.3 End-user Industry

- 5.3.1 Power Generation

- 5.3.2 Steel and Metal Industry

- 5.3.3 Oil Refinery

- 5.3.4 Chemical and Petrochemical

- 5.3.5 Textile and Dye Industry

- 5.3.6 Sugar Mill

- 5.3.7 Paper Mill

- 5.3.8 Food and Beverage

- 5.3.9 Institutional

- 5.3.10 Pharmaceutical

- 5.3.11 Other End-user Industries

- 5.4 Geography

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aries Chemical, Inc.

- 6.4.2 BASF SE

- 6.4.3 Buckman

- 6.4.4 Cannon Water Technology

- 6.4.5 Eastman Chemical Compnay

- 6.4.6 Ecolab

- 6.4.7 Kemira

- 6.4.8 Kurita Water Industries Ltd.

- 6.4.9 Lenntech B.V.

- 6.4.10 Solenis

- 6.4.11 Suez

- 6.4.12 Veolia Water Technologies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Shifting Focus Towards Green Chemicals

- 7.2 Development in Chemical Technology

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日