|

|

市場調査レポート

商品コード

1637751

タイの太陽エネルギー:市場シェア分析、産業動向、成長予測(2025年~2030年)Thailand Solar Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| タイの太陽エネルギー:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 95 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

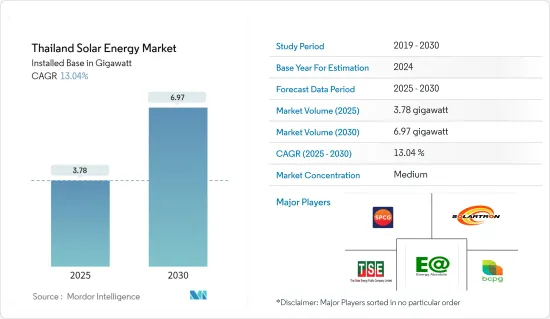

タイの太陽エネルギー市場規模(設置ベース)は、2025年の3.78ギガワットから2030年には6.97ギガワットに拡大し、予測期間(2025~2030年)のCAGRは13.04%と予測されます。

主要ハイライト

- 長期的には、支援施策、電力価格上昇、技術進歩、企業需要、エネルギー安全保障目標などの要因が、予測期間中のタイの太陽エネルギー市場を牽引するとみられます。

- 一方、送電網の制限、インフラ格差、エネルギー貯蔵の課題は、予測期間中の太陽エネルギー市場の成長を大きく妨げます。

- 2037年までに再生可能エネルギー30%を達成するというタイの目標は、太陽エネルギー市場に大きな機会をもたらします。さらに、スマートグリッド技術、エネルギー貯蔵システムの統合、Energy Absoluteのような企業による大規模バッテリー生産への投資は、太陽光発電プロジェクトと送電網の安定性をさらに後押しします。

タイの太陽エネルギー市場動向

太陽光発電(PV)セグメントが市場を独占する見込み

- 太陽電池モジュールのコスト低下と、発電や給湯など多様な用途に対応するシステムの汎用性により、予測期間中は太陽光発電(PV)セグメントが大きな市場シェアを占めるとみられます。

- 国際再生可能エネルギー機関(IRENA)によると、2019~2023年にかけて、タイの太陽光発電(PV)設置容量は2979MWから3181MWに増加し、この期間の成長率は6.78%でした。さらに、タイでは政府主導による太陽光発電の増加や太陽光発電コストの低下により、太陽光発電セグメントは大幅な成長が見込まれています。

- 近年、タイでは太陽光発電プロジェクトが大幅に増加しています。こうしたイニシアチブは、自然エネルギーに対する政府の野心的なコミットメントと一致しており、2037年までに発電ミックスに占める割合を従来の20%から50%に引き上げるという目標を掲げています。

- 例えば、2024年10月、TotalEnergies ENEOSは、S. Kijchai Enterpriseとの2件目のプロジェクトとして、タイで1.8MWpの浮体式太陽光発電システムを完成させました。3,000枚以上のモジュールを搭載したこのシステムは、年間2,650MWhを発電し、CO2排出量を1,125トン削減します。このプロジェクトは、TotalEnergies ENEOSが長期PPAの下で資金を提供し運営しています。

- さらに2024年5月、Gulf Energy Development Private Limitedは、タイ発電公社(EGAT)と25年間の長期売電契約(PPA)を締結し、合計1,353MWの太陽光発電所25カ所を建設しました。エネルギー規制委員会による大規模な自然エネルギー計画の一環であるこれらのプロジェクトは、固定価格買取制度の適用を受け、2024~2029年の間に商業運転を開始する予定で、費用対効果の高い電力ソリューションを記載しています。

- こうした開発により、タイでは予測期間中、太陽光発電セグメントが圧倒的な市場シェアを占めると予想されます。

市場を牽引する政府の支援施策

- タイ政府は、7年間で温室効果ガス排出量を20~25%削減するため、国全体で再生可能エネルギーの導入を奨励しています。政府はまた、様々なインセンティブや規制上の支援を提供することで、太陽光発電市場を支援しています。

- タイは、2037年までに再生可能エネルギーが電力構成の30%を占めるという目標を掲げています。2023年には1万2,547MWの再生可能エネルギー容量を導入し、2015年の7,902MWを上回りました。

- 2024年8月、タイは公共部門を対象とした省エネ計画を承認し、年間5億8,500万kWhの節電を目指しました。このプログラムでは、エネルギーサービス会社(ESCO)モデルを採用し、長期契約を通じてソーラーパネルやその他の省エネ対策を導入します。

- 2024年7月、サステイナブル開発目標(SDGs)とカーボンニュートラルに焦点を当てた循環型経済をタイで推進するため、ピムパットラ・ウィチャイクン工業大臣が来日しました。この協力には、サステイナブル資源管理を強化することを目的としたBio, Circular, and Green(BCG)経済モデルの一環として、ソーラーパネルのリサイクルも含まれます。

- 2023年5月、Electricity Generating Authority of Thailand(EGAT)はメーホンソン県のスマートグリッドパイロットプロジェクトの下、3MWの太陽光発電所と4MWの蓄電池(BESS)プロジェクトの商業運転開始(COD)式典を開催しました。

- さらに2023年3月、タイの国家エネルギー施策審議会(NEPC)は、固定価格買取制度によるクリーン電力の買取枠を導入しました。固定価格買取制度の税率は、地上設置型太陽光発電が1基あたり2.1679バーツ、太陽光発電+蓄電池が1基あたり2.8331バーツです。どちらのタイプの発電所も、固定価格買取制度の期間は25年間です。

- このため、政府の施策やイニシアティブが、予測期間中のタイの太陽エネルギー市場を牽引すると予想されます。

タイの太陽エネルギー産業概要

タイの太陽エネルギー市場は半集中型です。市場の主要企業(順不同)には、Energy Absolute Public Company Limited、SPCG Public Company Limited、Solartron PCL、Thai Solar Energy PLC、BCPG Public Company Limitedなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 太陽エネルギー設置容量と2029年までの予測

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

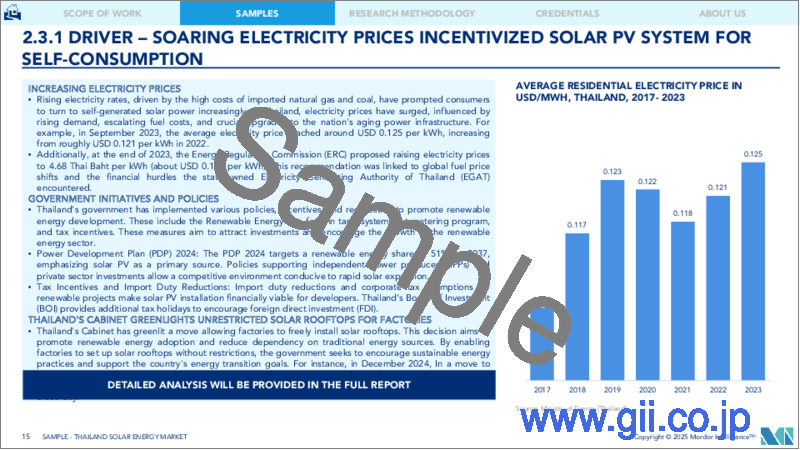

- タイにおける電気料金の上昇とエネルギー安全保障の目標

- 太陽エネルギー導入に対する政府の支援施策

- 抑制要因

- 送電網の制限、インフラ格差、エネルギー貯蔵の課題

- 促進要因

- サプライチェーン分析

- PESTLE分析

- 投資分析

第5章 市場セグメンテーション-技術

- 太陽光発電(PV)

- 集光型太陽熱発電(CSP)

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略とSWOT分析

- 企業プロファイル

- SPCG Public Company Limited

- BCPG Public Company Limited(BCPG)

- Thai Solar Energy PLC

- B. Grimm Power Public Company Limited

- Solaris Green Energy Co. Ltd.

- Energy Absolute PCL

- Solartron PLC

- Marubeni Corporation

- Black & Veatch Holding Company

- Jinkosolar Holding Co. Ltd.

- Trina Solar Co., Ltd.

- その他の著名な企業一覧

- 市場ランキング分析

第7章 市場機会と今後の動向

- スマートグリッド開発とグリッド拡大

The Thailand Solar Energy Market size in terms of installed base is expected to grow from 3.78 gigawatt in 2025 to 6.97 gigawatt by 2030, at a CAGR of 13.04% during the forecast period (2025-2030).

Key Highlights

- Over the long term, factors such as supportive policies, rising electricity prices, technological advancements, corporate demand, and energy security goals will likely drive Thailand's solar energy market during the forecast period.

- On the other hand, grid limitations, infrastructure gaps, and energy storage challenges significantly hinder the growth of the solar energy market during the forecast period.

- Nevertheless, Thailand's goal of achieving 30 percent renewable energy by 2037 presents significant opportunities for the solar energy market. Furthermore, The integration of smart grid technologies, energy storage systems, and Investments by companies like Energy Absolute in large-scale battery production further support solar projects and grid stability.

Thailand Solar Energy Market Trends

Solar Photovoltaic (PV) Segment Expected to Dominate the Market

- The solar PV segment is likely to hold the major market share during the forecast period, owing to the declining costs of solar modules and the versatility of these systems for various applications, like electricity generation and water heating.

- According to the International Renewable Energy Agency (IRENA), From 2019 to 2023, Thailand's Solar Photovoltaic (PV) Installed Capacity increased from 2979 MW to 3181 MW, with the growth rate over this period being 6.78 percent. Moreover, the solar PV segment is expected to witness massive growth with the increasing solar PV encouraged by government initiatives and falling solar PV costs in Thailand.

- In recent years, Thailand has seen a significant uptick in solar energy projects. These initiatives align with the government's ambitious commitment to renewables, which targets a 50 percent share in the power generation mix by 2037, up from an earlier goal of 20 percent.

- For instance, in October 2024, TotalEnergies ENEOS completed a 1.8 MWp floating solar PV system in Thailand, their second project with S. Kijchai Enterprise. The system, with over 3,000 modules, generates 2,650 MWh annually, reducing CO2 emissions by 1,125 tons, equivalent to planting 16,800 trees. This project is funded and operated by TotalEnergies ENEOS under a long-term PPA.

- Additionally, in May 2024, Gulf Energy Development Private Limited finalized 25-year-long power purchase agreements (PPAs) with the Electricity Generating Authority of Thailand (EGAT) to construct 25 solar PV farms, totaling 1,353 MW. These projects, part of a larger renewables scheme by the Energy Regulatory Commission, will receive feed-in tariffs and are expected to start commercial operations between 2024 and 2029, offering a cost-effective power solution.

- Owing to such developments, the solar PV segment is expected to have a dominant market share in Thailand during the forecast period.

Supportive Government Policies to Drive the Market

- The Thai government is encouraging renewable energy installations across the country to reduce greenhouse gas emissions by 20-25% in seven years. The government has also supported the solar power market by providing various incentives and regulatory support.

- Thailand has set a target for renewables to account for 30 percent of the power mix by 2037. In 2023, the country installed 12,547 MW of renewable energy capacity, which was higher than the 7,902 MW installed in 2015.

- In August 2024, Thailand approved an energy-saving scheme targeting public sector agencies, aiming to save 585 million kWh annually. The program will use the energy service company (ESCO) model to install solar panels and other energy-saving measures through long-term contracts.

- In July 2024, Industry Minister Pimphattra Wichaikul visited Japan to promote a circular economy in Thailand, focusing on sustainable development goals (SDGs) and carbon neutrality. The collaboration includes recycling solar panels as part of the Bio, Circular, and Green (BCG) economy model, aiming to enhance sustainable resource management.

- In May 2023, the Electricity Generating Authority of Thailand (EGAT), under the Smart Grid Pilot Project in Mae Hong Son Province, held a Commercial Operation Date (COD) ceremony for the 3 MW Solar Power Plant and 4 MW Battery Energy Storage System (BESS) Project.

- Moreover, in March 2023, Thailand's National Energy Policy Council (NEPC) introduced quotas for purchasing clean electricity via the Feed-in-Tariff Scheme, which will be implemented in two phases. The feed-in tariff rates are 2.1679 THB per unit for ground-mounted solar and 2.8331 THB per unit for solar + storage. Both types of power plants will have a 25-year term for the feed-in tariff.

- Therefore, supportive government policies and initiatives are expected to drive the Thailand solar energy market in the forecast period.

Thailand Solar Energy Industry Overview

The Thailand solar energy market is semi-concentrated. Some of the major companies in the market (in no particular order) include Energy Absolute Public Company Limited, SPCG Public Company Limited, Solartron PCL, Thai Solar Energy PLC, BCPG Public Company Limited, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Solar Energy Installed Capacity and Forecast, until 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Rising Electricity Prices and Energy Security Goals in Thailand

- 4.5.1.2 Supportive Government Policies to Adopt Solar Energy

- 4.5.2 Restraints

- 4.5.2.1 Grid Limitations, Infrastructure Gaps, and Energy Storage Challenges

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

- 4.8 Investment Analysis

5 MARKET SEGMENTATION - TECHNOLOGY

- 5.1 Solar Photovoltaic (PV)

- 5.2 Concentrated Solar Power (CSP)

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted & SWOT Analysis for Leading Players

- 6.3 Company Profiles

- 6.3.1 SPCG Public Company Limited

- 6.3.2 BCPG Public Company Limited (BCPG)

- 6.3.3 Thai Solar Energy PLC

- 6.3.4 B. Grimm Power Public Company Limited

- 6.3.5 Solaris Green Energy Co. Ltd.

- 6.3.6 Energy Absolute PCL

- 6.3.7 Solartron PLC

- 6.3.8 Marubeni Corporation

- 6.3.9 Black & Veatch Holding Company

- 6.3.10 Jinkosolar Holding Co. Ltd.

- 6.3.11 Trina Solar Co., Ltd.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Smart Grid Development and Grid Expansion