ウルトラキャパシタ-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Ultracapacitor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636575

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

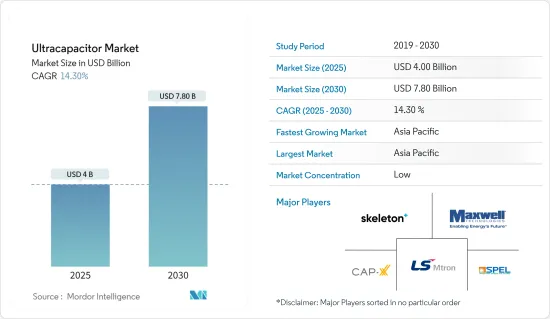

ウルトラキャパシタ市場規模は2025年に40億米ドルと推定され、予測期間中(2025~2030年)のCAGRは14.3%で、2030年には78億米ドルに達すると予測されます。

主要ハイライト

- 自動車産業がキャパシタ市場を牽引。産業が持続可能でエネルギー効率の高い自動車にシフトするにつれ、キャパシタは回生ブレーキ、エンジン始動停止システム、エネルギー回収システムなどの用途でますます使用されるようになっています。素早いエネルギー供給が可能なキャパシタは、こうした用途での有効性を高めています。さらに、自動車メーカーは現在、性能を最適化するためにバッテリーとキャパシタを組み合わせたハイブリッドエネルギー貯蔵ソリューションを模索しています。

- 再生可能エネルギープロジェクトの急増に伴い、効率的なエネルギー貯蔵と系統安定化ソリューションへの需要が高まっています。ウルトラキャパシタは、ピーク生産時に余剰エネルギーを貯蔵し、低発電時にそれを放出することにより、送電網の安定化を助けるという極めて重要な役割を担っています。この機能性は、再生可能エネルギーシステム、特に風力発電や太陽光発電におけるウルトラキャパシタの重要性を強調しています。

- 現在進行中の研究開発は、キャパシタのエネルギー密度を高め、従来のバッテリーに匹敵するようにすることを目指しています。特にグラフェンやカーボンナノチューブを用いた材料革新は、高出力や急速充電を損なうことなく、蓄電容量の向上を約束するものです。メルボルンのEnyGyは2023年、最先端のグラフェン技術を活用したウルトラキャパシタを発表しました。

- しかし、スーパーキャパシタは長期的なエネルギー貯蔵には限界があります。その放電速度はリチウムイオン電池を上回り、毎日10~20%の自己放電損失が生じます。電池は消耗するまでほぼ一定の電圧を維持するが、キャパシタは充電によって電圧が直線的に低下します。

- よりクリーンなエネルギーを求める世界の動きと厳しい環境規制は、キャパシタ市場にとって好都合な雰囲気を作り出しています。二酸化炭素排出量の削減、電気自動車や再生可能エネルギーの導入促進を目的とした施策が、市場の成長を後押ししています。さらに、研究開発、特にエネルギー貯蔵技術への政府と民間部門の投資は、先進的なキャパシタの進化を加速させています。

キャパシタ市場動向

需要を経験する自動車・運輸部門

- 電気自動車やハイブリッド車の急速な普及がキャパシタ需要を大きく押し上げています。従来の電池とは異なり、キャパシタは高い電力密度を誇り、急速な充放電を可能にします。このため、回生ブレーキやスタート・ストップシステムなどの用途に特に適しています。スーパーキャパシタ技術は、スーパーキャパシタの実装によってもたらされる課題と機会を活用し、回生ブレーキ検査装置で広く利用されています。その顕著な電力密度とサイクル特性により、非常に望ましいものとなっています。

- 例えば、Skeleton Technologiesのスーパーキャパシタは、ホンダCR-Vハイブリッド・レーサーに搭載されています。このデモ車両は、ホンダ・パフォーマンス開発の実力を示すとともに、ホンダの2023年インディカーハイブリッドパワーユニット技術を発表しています。スケルトンのスーパーキャパシタのおかげで、レースカーはハイパワー性能を向上させています。このスーパーキャパシタは、ブレーキエネルギーの回収と加速力向上のための完璧なソリューションとして注目されています。スーパーキャパシタには、低い内部抵抗、高いサイクル性、優れた耐老化性といった特筆すべき利点があります。

- KAIST(韓国科学技術院)の研究者は、革新的なエネルギー貯蔵ソリューションを発表しました。この新システムは、スーパーキャパシタの長所と、ナトリウムイオン電池化学のコスト効率とサプライチェーンの利点を融合させたものです。研究チームは、この新システムが電気自動車セグメントに波及することを期待しています。この新しい電池は、スーパーキャパシタ技術に合わせた正極と先進的な負極を統合しています。この相乗効果により、この電池は驚異的な蓄電容量と迅速な充放電速度の両方を誇り、リチウムイオン電池に対する強力な対抗馬となります。

- 米国では、主に3つの急速充電規格が主流です。CHAdeMO、複合充電システム(CCS)、北米充電規格(以前はTeslaの規格)です。このうち、急速充電ステーションの数ではCCS方式がリードしています。米国エネルギー省のデータによると、2024年にはCCSステーションが7,315カ所、CHAdeMOステーションが5,720カ所、NACSステーションが2,280カ所となります。このインフラの拡大は、電気自動車におけるキャパシタの利用拡大を後押しします。

- ウルトラキャパシタは、エネルギー回収システム、特に電気バス、路面電車、高速列車などの公共交通セグメントで極めて重要な役割を担っています。自動車産業における重要な課題は、摩耗することなくハイサイクル使用に耐える部品を調達することです。ウルトラキャパシタはこの領域で輝きを放ち、劣化を最小限に抑えながら何百万回もの充放電サイクルを難なくこなします。産業が電動化、燃費効率、持続可能性により傾くにつれ、ウルトラキャパシタの重要性は増大の一途をたどっています。

アジア太平洋が市場を牽引

- 中国、日本、韓国は、革新的なエネルギー貯蔵ソリューションに多額の投資を行っている確立された自動車産業によって支えられて、電気自動車生産をリードしています。この地域の電気自動車インフラの急速な拡大は、サステイナブル輸送への強い後押しと相まって、市場をさらに推進することになると考えられます。

- 電気自動車にとどまらず、アジア太平洋は再生可能エネルギー投資においても重要な役割を担っています。中国やインドなどの国々が太陽光発電や風力発電のプロジェクトを強化しているため、エネルギー貯蔵ソリューションの需要が急増しています。Carbon Briefの調査はこの動向を浮き彫りにしており、クリーンエネルギー投資が前年比40%増、2023年には総額8,900億米ドルに達すると指摘しています。この成長は、中国経済全体の投資急増の全体を占めています。迅速な充放電能力で知られるウルトラキャパシタは、こうした再生可能エネルギーシステムの安定化に極めて重要であることが証明されつつあります。

- 強力な製造基盤と技術進歩で知られるアジア太平洋は、研究開発に重点を置いています。多額の投資に支えられたこの重点は、キャパシタの性能を向上させただけでなく、民生用電子機器製品から産業機械に至るまで、多様なセグメントでの応用を広げています。

- エレクトロニクス製造業にとって重要な飛躍として、インドは2024年10月、ケララ州カヌールに初のスーパーキャパシタ製造工場を落成させました。この施設は、インドの国防、電気自動車、さらには宇宙ミッションなど、さまざまな部門向けに最高級のスーパーキャパシタを生産することを目的としています。

- 二酸化炭素排出量の削減を目標とし、グリーンエネルギーソリューションを支持する政府の取り組みが、キャパシタの迅速な導入に拍車をかけています。EV生産と再生可能エネルギーへの取り組みを強化する奨励金と補助金により、キャパシタ市場の成長環境は整っています。

キャパシタ産業概要

ウルトラキャパシタ市場は熾烈な競争を繰り広げており、既成の多国籍企業と技術革新と市場拡大を優先する新興企業の両方が存在します。このセグメントの注目すべき参入企業には、axwell Technologies、Skeleton Technologies、LS Mtron Ltd、Eaton Corporationなどがあります。これらの企業は、強固な世界のフットプリント、包括的な研究開発能力、幅広い製品提供を通じて、その地位を固めてきました。

競合は、自動車、再生可能エネルギー、産業用途などのセグメントからの需要の高まりとともに激化しています。大手企業は、市場での地位を固め、製品ラインアップを拡大するため、研究開発努力の強化、投資の確保、資金調達を行っています。例えば、Skeleton Technologiesは2023年10月に1億800万ユーロの資金を確保し、次世代製品の開発を急ピッチで進め、スーパーキャパシタの製造を拡大することを目的としています。

キャパシタ市場では、継続的な研究開発が競争優位性を獲得するために最も重要です。企業は、エネルギー密度を高め、コストを削減するために、カーボンナノチューブやグラフェンなどの先端材料を掘り下げています。今後、市場は、技術的ブレークスルー、コスト効率、主要産業のダイナミックなエネルギー需要への適応に焦点を当て、競争激化の構えを見せています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- マクロ経済動向の市場への影響評価

第5章 市場力学

- 市場促進要因

- エネルギー効率の高いソリューションに対する需要の高まり

- 電気自動車(EV)市場の成長

- 再生可能エネルギーシステムの進歩

- 市場抑制要因

- 初期コストの高さ

- バッテリーに比べて低いエネルギー密度

第6章 市場セグメンテーション

- タイプ別

- 静電キャパシタ

- 擬似キャパシタ

- ハイブリッドキャパシタ

- エンドユーザー産業別

- 自動車と輸送

- コンシューマー・エレクトロニクス

- エネルギー・電力

- 産業用製造

- 航空宇宙・防衛

- その他

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Skeleton Technologies

- Maxwell Technologies

- CAP-XX

- SPEL TECHNOLOGIES PRIVATE LTD.

- LS Mtron Co., Ltd.

- IOXUS

- Nippon Chemi-Con Corporation

- Shanghai Aowei Technology Development Co., Ltd

- KEMET Corporation

- Eaton Corporation

- Yunasko

- VINATech Co., Ltd

- SECH

第8章 投資分析

第9章 市場の将来

目次

The Ultracapacitor Market size is estimated at USD 4.00 billion in 2025, and is expected to reach USD 7.80 billion by 2030, at a CAGR of 14.3% during the forecast period (2025-2030).

Key Highlights

- The automotive sector drives the ultracapacitor market. As the industry shifts towards sustainable and energy-efficient vehicles, ultracapacitors are increasingly used in applications like regenerative braking, engine start-stop systems, and energy recovery systems. Their capability to deliver quick energy bursts enhances their effectiveness in these roles. Furthermore, automakers are now exploring hybrid energy storage solutions, merging batteries with ultracapacitors for optimized performance.

- With the surge in renewable energy projects, the demand for efficient energy storage and grid stability solutions has intensified. Ultracapacitors play a pivotal role by storing excess energy during peak production and releasing it during low generation periods, thus aiding grid stabilization. This functionality underscores their importance in renewable energy systems, particularly in wind and solar power.

- Ongoing research and development efforts aim to boost the energy density of ultracapacitors, allowing them to rival conventional batteries. Material innovations, especially with graphene and carbon nanotubes, promise enhanced storage capacity without compromising on high power output and rapid charging. A notable example is EnyGy, a Melbourne-based company, which in 2023 unveiled an ultracapacitor leveraging cutting-edge graphene technology.

- However, supercapacitors have limitations in long-term energy storage. Their discharge rate surpasses that of lithium-ion batteries, leading to a self-discharge loss of 10-20 percent daily. While batteries maintain a near-constant voltage until depleted, capacitors experience a linear decline in voltage with charge.

- Global pushes for cleaner energy and stringent environmental regulations have created a conducive atmosphere for the ultracapacitor market. Policies aimed at reducing carbon emissions and promoting electric vehicles and renewable energy adoption have bolstered market growth. Moreover, both government and private sector investments in research and development, particularly in energy storage technologies, have accelerated the evolution of advanced ultracapacitors.

Ultracapacitor Market Trends

Automotive and Transportation Sector Experiencing Demand

- The swift rise in the adoption of electric and hybrid vehicles has significantly driven up the demand for ultracapacitors. Unlike conventional batteries, ultracapacitors boast a high power density, enabling rapid charging and discharging. This makes them particularly suited for applications like regenerative braking and start-stop systems. Supercap technologies are being extensively utilized in regenerative braking test rigs, capitalizing on the challenges and opportunities presented by supercapacitor implementation. Their remarkable power density and cycling characteristics make them highly desirable.

- For example, Skeleton Technologies' supercapacitors are featured in the Honda CR-V Hybrid Racer. This demonstration vehicle highlights the prowess of Honda Performance Development and showcases Honda's 2023 IndyCar hybrid power unit technology. Thanks to Skeleton's supercapacitors, the race car enjoys enhanced high-power performance. These supercapacitors are touted as the perfect solution for braking energy recovery and boosting acceleration. They come with notable advantages: low internal resistance, high cyclability, and excellent aging resistance.

- Researchers at KAIST (Korea Advanced Institute of Science and Technology) have unveiled an innovative energy storage solution. This new system merges the strengths of supercapacitors with the cost-effectiveness and supply chain benefits of sodium-ion battery chemistry. The research team envisions their creation making waves in the electric vehicle sector. Their novel battery integrates an advanced anode with a cathode tailored for supercapacitor technology. This synergy enables the battery to boast both impressive storage capacities and swift charge-discharge rates, positioning it as a formidable contender against lithium-ion batteries.

- In the U.S., three primary fast-charging standards dominate: CHAdeMO, Combined Charging System (CCS), and the North American Charging Standard (previously Tesla's standard). Among these, the CCS method leads in the number of fast-charging stations. Data from the U.S. Department of Energy reveals that in 2024, there were 7,315 CCS stations, 5,720 CHAdeMO stations, and 2,280 NACS stations. This expanding infrastructure bolsters the growing use of ultracapacitors in electric vehicles.

- Ultracapacitors are carving out a pivotal role in energy recovery systems, especially in public transport realms like electric buses, trams, and high-speed trains. A key challenge in the automotive industry is sourcing components that can endure high-cycle usage without substantial wear. Ultracapacitors shine in this domain, effortlessly handling millions of charge and discharge cycles with minimal degradation. As the industry leans more towards electrification, fuel efficiency, and sustainability, the significance of ultracapacitors is poised to grow.

Asia-Pacific Region is Driving the Market

- China, Japan, and South Korea lead the charge in electric vehicle production, bolstered by their established automotive industries that heavily invest in innovative energy storage solutions. The region's rapid expansion of EV infrastructure, coupled with a strong push towards sustainable transportation, is set to propel the market further.

- Beyond electric vehicles, the Asia-Pacific region is a significant player in renewable energy investments. With countries like China and India intensifying their solar and wind energy projects, the demand for energy storage solutions has surged. Research from Carbon Brief highlights this trend, noting a 40% year-on-year rise in clean-energy investments, totaling USD 890 billion in 2023. This growth accounted for the entirety of the investment surge across China's economy. Ultracapacitors, known for their swift charging and discharging capabilities, are proving to be pivotal in stabilizing these renewable energy systems.

- The Asia-Pacific region, renowned for its strong manufacturing base and technological advancements, is channeling its focus on research and development. Backed by substantial investments, this emphasis has not only enhanced ultracapacitor performance but also broadened their applications across diverse sectors, from consumer electronics to industrial machinery.

- In a significant leap for electronics manufacturing, India inaugurated its first supercapacitor manufacturing plant in Kannur, Kerala in October 2024. This facility aims to produce top-tier supercapacitors for various sectors, including the Indian defense, electric vehicles, and even space missions.

- Government initiatives, targeting a reduction in carbon emissions and championing green energy solutions, have catalyzed the swift adoption of ultracapacitors. With incentives and subsidies bolstering EV production and renewable energy initiatives, the environment is ripe for the ultracapacitor market's growth.

Ultracapacitor Industry Overview

The ultracapacitor market is fiercely competitive, featuring both established multinational corporations and emerging players that prioritize technological innovation and market expansion. Notable players in this arena include Maxwell Technologies, Skeleton Technologies, LS Mtron Ltd, and Eaton Corporation. These companies have cemented their positions through a robust global footprint, comprehensive R&D capabilities, and a wide array of product offerings.

Competition intensifies with rising demand from sectors like automotive, renewable energy, and industrial applications. Major players are bolstering their R&D efforts, securing investments, and raising funds to solidify their market positions and broaden their product ranges. For example, in October 2023, Skeleton Technologies secured EUR 108M in funding, aimed at fast-tracking the development of next-gen products and expanding supercapacitor manufacturing.

In the ultracapacitor market, continuous R&D is paramount for gaining a competitive edge. Companies are delving into advanced materials, such as carbon nanotubes and graphene, to boost energy density and cut costs. Looking ahead, the market is poised for heightened competition, focusing on technological breakthroughs, cost efficiency, and adapting to the dynamic energy demands of key industries.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 An Assessment of Impact of Macroeconomic Trends on The Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand for Energy-Efficient Solutions

- 5.1.2 Growing Electric Vehicle (EV) Market

- 5.1.3 Advancements in Renewable Energy Systems

- 5.2 Market Restraints

- 5.2.1 High Initial Cost

- 5.2.2 Lower Energy Density Compared to Battery

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Electrostatic Ultracapacitors

- 6.1.2 Pseudocapacitors

- 6.1.3 Hybrid Capacitors

- 6.2 By End User Vertical

- 6.2.1 Automotive and Transportation

- 6.2.2 Consumer Electronics

- 6.2.3 Energy and Power

- 6.2.4 Industrial Manufacturing

- 6.2.5 Aerospace and Defense

- 6.2.6 Others

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Skeleton Technologies

- 7.1.2 Maxwell Technologies

- 7.1.3 CAP-XX

- 7.1.4 SPEL TECHNOLOGIES PRIVATE LTD.

- 7.1.5 LS Mtron Co., Ltd.

- 7.1.6 IOXUS

- 7.1.7 Nippon Chemi-Con Corporation

- 7.1.8 Shanghai Aowei Technology Development Co., Ltd

- 7.1.9 KEMET Corporation

- 7.1.10 Eaton Corporation

- 7.1.11 Yunasko

- 7.1.12 VINATech Co., Ltd

- 7.1.13 SECH

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日