アジア太平洋地域の電子廃棄物管理:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

APAC E-Waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636556

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

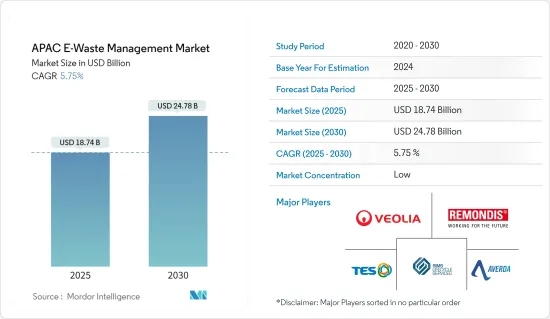

アジア太平洋地域の電子廃棄物管理市場規模は、2025年に187億4,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは5.75%で、2030年には247億8,000万米ドルに達すると予測されています。

アジア太平洋地域は、急速な技術進歩、家電製品の普及拡大、力強い経済成長により、電子廃棄物が大幅に増加しています。中国、インド、日本が主な貢献国です。

2023年8月、日本は電子廃棄物の課題に取り組むためのASEAN諸国とのパートナーシップを発表しました。環境大臣会合で設立されたこの協力関係は、電子廃棄物処理に関する規制の開発に焦点を当てています。日本は、2024年度予算を通じて、廃棄物処理事業者の登録・認証システムの構築を支援します。

このイニシアチブは、廃棄物輸入規制が緩いために環境汚染や健康リスクに悩まされている東南アジアの電子廃棄物処理を改善することを目的としています。日本もまた、電気自動車産業を支援し、国内の限られた金属資源を軽減するために、電子廃棄物から貴重な金属を回収しようとしています。

一方、2024年5月、韓国のプライベート・エクイティおよび環境関連企業は、埋立地部門への投資を増加させました。アフィルマ・キャピタルは、大手埋立地運営会社であるジェンテックを5,000億ウォン(3億6,800万米ドル)で買収しました。ジェンテックは忠清南道唐津市で大規模な埋立地を運営しています。このような関心の高まりは、廃棄物管理に対する信頼の高まりを反映しており、電子廃棄物処理技術の進歩の可能性を示唆しています。

アジア太平洋地域の電子廃棄物管理市場動向

インドのEPR認証プラットフォームが電子廃棄物のリサイクル効率を高める

2022会計年度、インドでは160万トンを超える電子廃棄物が排出され、52万7,000トンが回収・処理されました。2024年3月現在、政府はこの深刻化する課題に対処するため、拡大生産者責任(EPR)証明書を取引するためのオンラインプラットフォームを展開する予定です。EPRの義務化により、生産者は廃棄後の製品のリサイクルについて責任を負うことになり、それにより、よりリサイクル可能で再利用可能な商品の創出が促進されます。

中央汚染管理委員会(CPCB)は、EPR認証市場の透明性と効率性を高めるため、このプラットフォームを監督しています。企業は、社内で廃棄物を管理するか、リサイクル基準を上回る事業体からEPR証書を調達することで、リサイクル義務を果たすことができます。CPCBは、未達成のEPR目標に対する環境補償の割合に応じて、これらの証書のガイドラインと価格を設定します。

2022年の電子廃棄物(管理)規則におけるEPR指令の開始以来、政府は5,615件のEPR申請を処理し、4,865件を承認し、リサイクル業者から285件の申請を受け、196件を許可しました。注目すべきは、政府はすでに廃電気電子機器(WEEE)のリサイクル目標10億5,000万トンを突破していることです。政府は現在、今後のプラットフォームでこうした取り組みを強化しようとしています。

中国、北京のイベントで電子廃棄物の革新と持続可能性への取り組みを強調

業界の専門家によると、2022年、世界最大の電子廃棄物生産国である中国は、1,200万トンを超える電子廃棄物を排出しました。早いもので2024年4月、北京の契家園外交居住区(DRC)は、中国の廃棄物分別とリサイクルの躍進にスポットライトを当てたイベントの舞台となった。この展示会では、AIを活用した最先端の廃棄物選別機が展示され、リサイクル素材から作られた製品が紹介されました。特筆すべきは、このイベントには子供向けのインタラクティブなアクティビティが含まれており、リサイクルの重要性が強調されていたことです。

北京市対外環境衛生サービスセンターが主催したこのイベントは、AI、IoT、ビッグデータ、クラウドコンピューティングの進歩を活用し、電子廃棄物と闘う中国の決意を強調しました。中国パブリック・ディプロマシー協会(CPDA)傘下の中国国際プレス・コミュニケーション・センター(CIPCC)は、COVID-19の大流行で一時中断していたメディア交流の一環として、今回の訪問を実現させました。このプログラムでは、90カ国以上から100人以上のジャーナリストを招き、メディア交流に焦点を当て、現在進行中の中国の開発に関する見識を提供しました。

このようなショーケースやイニシアチブを通じて、中国は持続可能な電子廃棄物管理技術のフロントランナーであるという物語を作り上げています。この戦略的な動きは、中国の世界の地位を強化し、国際的な環境対話における中国のソフトパワーと影響力を増幅することを目的としています。

アジア太平洋地域の電子廃棄物管理産業の概要

アジア太平洋地域の電子廃棄物管理市場では、Sims Recycling SolutionsやTES-AMMと並んで、Veolia Group、Remondis、Averdaなどの大手企業が激しい競争を繰り広げています。特にヴェオリア・グループとリモンディスは、高度なリサイクル技術に重点を置き、多様な電子廃棄物の流れに対応するサービス・ポートフォリオを広げている点で際立っています。

市場をリードするこれらの企業は、持続可能性を最優先し、地方自治体とのパートナーシップを結んで、電子廃棄物の収集とリサイクルのインフラを強化しています。インドの電子廃棄物業界における有力企業であるAtteroは、広範な回収ネットワークと最先端のリサイクル手法を有しています。これらの企業は、技術、規制状況、持続可能な取り組みに戦略的に注力することで、アジア太平洋地域の電子廃棄物市場を前進させ、より効率的で環境に配慮した電子廃棄物管理への道を切り開いています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場洞察

- 現在の市場シナリオ

- 技術動向

- サプライチェーン/バリューチェーン分析に関する洞察

- 業界の規制に関する洞察

- 業界の技術的進歩に関する洞察

第5章 市場力学

- 市場促進要因

- 急速な技術進歩による電子廃棄物量の増加

- 都市化と工業化

- 市場抑制要因

- リサイクル費用の高さ

- 電子廃棄物の複雑さ

- 市場機会

- リサイクル技術の進歩

- 官民パートナーシップ

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第6章 市場セグメンテーション

- 材料タイプ別

- 金属

- プラスチック

- ガラス

- その他の材料

- 排出源タイプ別

- 民生用電子機器

- 産業用電子機器

- 家電製品

- その他

- 用途別

- 埋立地

- リサイクル

- その他の用途

- 国別

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

第7章 競合情勢

- 市場集中度の概要

- 企業プロファイル

- Veolia Group

- Remondis

- Averda

- Sims Recycling Solutions

- TES-AMM

- Enviro-Hub Holdings Ltd

- Blue Planet Environmental Solutions Pte Ltd

- ECO Recycling Ltd(Ecoreco)

- Attero

- JOMAR Life Research Laboratory

- その他の企業

第8章 市場機会と今後の動向

第9章 付録

目次

The APAC E-Waste Management Market size is estimated at USD 18.74 billion in 2025, and is expected to reach USD 24.78 billion by 2030, at a CAGR of 5.75% during the forecast period (2025-2030).

Asia-Pacific region is experiencing a significant rise in electronic waste due to rapid technological advancements, increased adoption of consumer electronics, and strong economic growth. China, India, and Japan are major contributors.

In August 2023, Japan announced a partnership with ASEAN countries to address e-waste challenges. This collaboration, established during an environment ministers' meeting, focuses on developing regulations for e-waste disposal. Japan will assist in creating registration and certification systems for waste management businesses, funded through its fiscal year 2024 budget.

This initiative aims to improve e-waste handling in Southeast Asia, which has struggled with environmental contamination and health risks due to lax waste import regulations. Japan also seeks to recover valuable metals from e-waste, supporting its electric vehicle industry and mitigating its limited domestic metal resources.

Meanwhile, in May 2024, South Korea's private equity and environmental firms increasingly invested in the landfill sector. Affirma Capital acquired Jentec, a major landfill operator, for KRW 500 billion (USD 368 million). Jentec operates a large landfill in Dangjin, South Chungcheong Province. This growing interest reflects increased confidence in waste management and suggests potential advancements in e-waste treatment technologies.

APAC E-Waste Management Market Trends

India's Upcoming EPR Certificate Platform to Boost E-Waste Recycling Efficiency

In the financial year 2022, India produced over 1.6 million metric tons of e-waste, with 527 thousand metric tons being collected and processed. As of March 2024, the government plans to roll out an online platform for trading Extended Producer Responsibility (EPR) certificates to combat this escalating challenge. EPR mandates hold producers accountable for recycling their products post-disposal, thereby promoting the creation of more recyclable and reusable goods.

The Central Pollution Control Board (CPCB) oversees this platform to boost transparency and efficiency in the EPR certificate market. Companies can fulfill recycling obligations by managing waste internally or procuring EPR certificates from entities surpassing their recycling benchmarks. The CPCB will set the guidelines and pricing for these certificates, pegged to a percentage of the environmental compensation for unmet EPR targets.

Since the inception of EPR directives in the E-Waste (Management) Rules of 2022, the government has processed 5,615 EPR applications, approving 4,865, and has received 285 applications from recyclers, granting 196. Notably, the government has already surpassed its recycling goal of 1.05 billion metric tons for Waste Electrical and Electronic Equipment (WEEE). It is now looking to bolster these efforts with the upcoming platform.

China Highlights E-Waste Innovations and Sustainability Initiatives at Beijing Event

Industry experts note that in 2022, China, the world's largest producer of electronic waste, churned out over 12 million metric tons. Fast-forward to April 2024, when the Qijiayuan Diplomatic Residence Compound (DRC) in Beijing set the stage for an event spotlighting China's waste sorting and recycling strides. The exhibition featured cutting-edge AI-driven waste-sorting machinery and showcased products crafted from recycled materials. Notably, the event included interactive activities for children, emphasizing the importance of recycling.

Hosted by the Beijing Municipal Center for Foreign-related Environment Sanitation Services, the event underscored China's resolve to combat e-waste, leveraging advancements in AI, IoT, big data, and cloud computing. The China International Press Communication Center (CIPCC), under the China Public Diplomacy Association (CPDA), facilitated this visit as part of a media exchange initiative reignited after a pause during the COVID-19 pandemic. The program hosted 100+ journalists from 90+ nations, focusing on media exchange and offering insights into China's ongoing developments.

Through such showcases and initiatives, China is crafting a narrative of being a frontrunner in sustainable e-waste management technology. This strategic move aims to bolster China's global standing, amplifying its soft power and influence in international environmental dialogues.

APAC E-Waste Management Industry Overview

The e-waste management market in Asia-Pacific sees intense competition, with major firms like Veolia Group, Remondis, and Averda, alongside Sims Recycling Solutions and TES-AMM, leading the charge. Veolia Group and Remondis, in particular, stand out for their emphasis on advanced recycling technologies and broadening service portfolios to handle diverse electronic waste streams.

These market leaders prioritize sustainability, forging partnerships with local governments to bolster e-waste collection and recycling infrastructure. Attero, a prominent player in India's e-waste landscape, has a widespread collection network and cutting-edge recycling methods. Collectively, these firms are propelling the APAC e-waste market forward through a strategic focus on technology, regulatory adherence, and sustainable initiatives, paving the way for a more efficient and eco-conscious e-waste management landscape.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Technological Trends

- 4.3 Insights into Supply Chain/Value Chain Analysis

- 4.4 Insights into Governement Regualtions in the Industry

- 4.5 Insights into Technological Advancements in the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rapid Technological Advancements Drive Increasing E-Waste Volumes

- 5.1.2 Urbanization and Industrialization

- 5.2 Market Restraints

- 5.2.1 High Cost of Recycling

- 5.2.2 Complexity of E-Waste

- 5.3 Market Opportunities

- 5.3.1 Advancements in Recycling Technologies

- 5.3.2 Public-Private Partnerships

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Threat of New Entrants

- 5.4.2 Bargaining Power of Buyers/Consumers

- 5.4.3 Bargaining Power of Suppliers

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Metal

- 6.1.2 Plastic

- 6.1.3 Glass

- 6.1.4 Other Materials

- 6.2 By Source Type

- 6.2.1 Consumer Electronics

- 6.2.2 Industrial Electronics

- 6.2.3 Household Appliances

- 6.2.4 Other Sources

- 6.3 By Application

- 6.3.1 Landfill

- 6.3.2 Recycled

- 6.3.3 Other Applications

- 6.4 By Country

- 6.4.1 China

- 6.4.2 Japan

- 6.4.3 India

- 6.4.4 South Korea

- 6.4.5 Rest of Asia-Pacific

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 Veolia Group

- 7.2.2 Remondis

- 7.2.3 Averda

- 7.2.4 Sims Recycling Solutions

- 7.2.5 TES-AMM

- 7.2.6 Enviro-Hub Holdings Ltd

- 7.2.7 Blue Planet Environmental Solutions Pte Ltd

- 7.2.8 ECO Recycling Ltd (Ecoreco)

- 7.2.9 Attero

- 7.2.10 JOMAR Life Research Laboratory*

- 7.3 Other Companies

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 APPENDIX

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日