掘削リグ:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Drilling Rig - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636498

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

掘削リグの市場規模は2025年に996億6,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは1.28%で、2030年には1,062億米ドルに達すると予測されます。

主なハイライト

- 中期的には、天然ガス需要の増加とガスインフラの拡張に伴う掘削活動の増加が、調査期間中の市場を促進します。

- その反面、再生可能エネルギー技術への世界のシフトが市場に課題をもたらすと予想されます。

- 一方、水圧破砕技術の進歩は、今後数年間、市場に有望な成長機会をもたらします。

- 地域的には、北米が主導権を握ることになります。具体的には、米国における上流活動の活発化が、調査期間中の北米の支配的地位を強化します。

掘削リグ市場の動向

オフショアセグメントが著しい成長を遂げる

- 高度なツールと機械を備えた掘削リグは、海底から石油・ガスの埋蔵量を抽出する上で極めて重要です。主にオフショアに設置されるこれらのリグは、エンジニアや作業員が海底深くに埋蔵された埋蔵資源にアクセスするための安定したプラットフォームとして機能し、時には水深数キロメートルに達することもあります。

- 石油・ガス需要の世界的急増と陸上埋蔵量の枯渇に牽引され、海洋掘削リグ市場は一貫した成長を遂げてきました。この埋蔵量の枯渇により、より深く離れた海域での探査が必要となった。ブラジル、メキシコ湾、西アフリカのような広大な未開発埋蔵量を誇る地域は、オフショア・プロジェクトへの大規模投資の主要ターゲットとなっています。

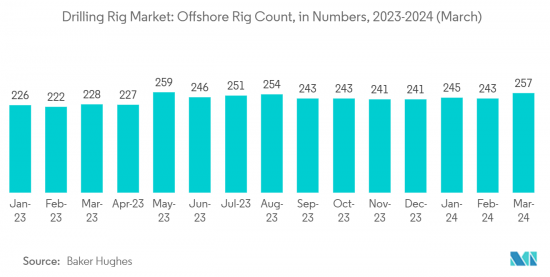

- 2024年3月現在、世界の海洋掘削リグ数は、2023年3月の228基から257基に増加しました。オフショア部門への投資が増加していることから、リグ数は今後も増加基調を維持すると予想されます。

- 2023年3月、ブラジルの鉱山・エネルギー相は「ポテンシアライザ」探鉱・生産プログラムを開始しました。これは、ブラジルを世界第4位の石油生産国に押し上げることを目的としたもので、石油開発投資の拡大を目指します。2029年の予測では、ブラジルの生産量は2021年比80%増の日量540万バレルとなり、その約80%をプレソルト層が占める。このプログラムでは、主要な探鉱鉱区を重視し、成熟鉱区と限界鉱区の両方への投資を提唱することで、掘削リグの需要を増幅させる。

- 2023年8月、SFL Corporation Ltd.は、カナダでEquinor ASAの子会社と半潜水式リグHerculesの掘削契約(推定1億米ドル)を締結しました。この契約は1次坑井1本と2次坑井のオプションで、2024年第2四半期に開始される予定。

- 2024年3月、海洋掘削コントラクターであるドルフィン・ドリリングは、オイル・インディア・リミテッドと半潜水式リグの長期契約を締結しました。インド沖を舞台に、14ヵ月かけて3坑の井戸を掘削するもので、費用は約1億4,500万米ドルを見込んでいます。

- このような投資状況や、陸上埋蔵量の減少に伴う政府のオフショア活動への傾注を考えると、この分野は調査期間中に成長するものと思われます。

市場を独占する北米

- 北米は、世界の石油・ガス市場において支配的な地位を占めているが、その主な理由は、米国が近年、世界有数の原油生産国として台頭してきたからです。

- さらに、米国は石油・ガス産業における資本支出で常に上位にランクされており、この傾向は今後も続くと予想されます。

- 米国は、主にメキシコ湾とアラスカ沖を中心とした堅調な海洋石油・ガス産業を誇っています。掘削深度が進むにつれ、技術的に回収可能な埋蔵量が急増し、この地域に多額の投資が集まっています。

- 2023年3月、バイデン政権は環境問題が議論されるなか、アラスカでの大規模な石油掘削事業を承認しました。コノコフィリップスがアラスカの国家石油保護区で掘削を開始することを許可し、ウィロー・プロジェクトの修正版を承認したのです。コノコフィリップスは、この事業から1日18万バレルの生産量を見込んでいます。

- 大手石油・ガス企業は、2023年以降に向けた設備投資額の平均を上回る増額を発表しました。例えば、シェブロン・コーポレーションは2022年12月、2023年の有機的設備投資予算を連結子会社で140億米ドル、持分法適用関連会社で30億米ドルに追加設定しました。

- 2023年12月、コノコフィリップスは石油生産のための建設を開始し、掘削リグサービスの需要を高めると予想される大きな一歩を踏み出しました。

- 2024年6月、米国エネルギー開発公社(米国エネルギー)は、パーミアン・ベースンにおける野心的な計画を発表し、パーミアン・プロジェクトに重点を置いて、来年度に7億5,000万米ドル以上を計上しました。

- こうした戦略的投資により、北米は当面、石油・ガス市場における優位性を維持する構えです。

掘削リグ産業の概要

掘削リグ市場は断片化されています。同市場で事業を展開する主要企業(順不同)には、Nabors Industries Ltd.、Transocean Ltd.、Saipem SpA、Seadrill Ltd.、Schlumberger NVなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模および需要予測(単位:米ドル)

- 原油生産量(百万バレル/日):2023年まで

- 天然ガス生産量(億立方フィート):2023年まで

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 天然ガス需要の増加とガスインフラの開発

- 掘削活動の増加

- 抑制要因

- よりクリーンな代替燃料の採用

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- 展開場所別

- オンショア

- オフショア

- タイプ別

- ジャッキアップ

- セミサブマーシブル

- ドリルシップ

- その他のタイプ

- 地域別

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- 英国

- ロシア

- ノルウェー

- スペイン

- 北欧諸国

- トルコ

- その他欧州

- アジア太平洋

- 中国

- インド

- オーストラリア

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- エジプト

- ナイジェリア

- カタール

- その他中東とアフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Nabors Industries Ltd.

- Transocean Ltd.

- Noble Corporation PLC

- Saipem SpA

- Arabian Drilling Company

- ADES International Holding PLC

- Shelf Drilling Holdings, Ltd.

- Seadrill Ltd

- Saudi Arabian Oil Company(Saudi Aramco)

- Schlumberger NV

- その他の主要企業一覧

- 市場ランキング/シェア(%)分析

第7章 市場機会と今後の動向

- 水圧破砕プロセスにおける技術の進歩

目次

Product Code: 50003777

The Drilling Rig Market size is estimated at USD 99.66 billion in 2025, and is expected to reach USD 106.20 billion by 2030, at a CAGR of 1.28% during the forecast period (2025-2030).

Key Highlights

- In the medium term, rising drilling activities, coupled with an increasing demand for natural gas and the expansion of gas infrastructure, are poised to propel the market during the study period.

- On the flip side, the global shift towards renewable energy technologies is anticipated to pose challenges to the market.

- Meanwhile, advancements in hydraulic fracturing technology present promising growth opportunities for the market in the coming years.

- Regionally, North America is set to take the lead. Specifically, the uptick in upstream activities in the United States bolsters North America's dominant position during the study period.

Drilling Rig Market Trends

Offshore Segment to Witness Significant Growth

- Drilling rigs, equipped with advanced tools and machinery, are pivotal in extracting oil and gas reserves from the ocean floor. Primarily stationed in offshore locales, these rigs serve as stable platforms, enabling engineers and workers to access reserves buried deep beneath the seabed, sometimes reaching depths of several kilometers.

- Driven by a global surge in oil and gas demand and the depletion of onshore reserves, the offshore drilling rig market has witnessed consistent growth. This depletion has necessitated exploration in deeper, more remote waters. Regions like Brazil, the Gulf of Mexico, and West Africa, boasting vast untapped reserves, have become prime targets for heavy investments in offshore projects.

- As of March 2024, the global offshore drilling rig count rose to 257, up from 228 in March 2023. With increasing investments in the offshore sector, the rig count is expected to continue its upward trajectory in the coming years.

- In March 2023, Brazil's Minister of Mines and Energy launched the "Potencializa" exploration and production program. This initiative, aimed at amplifying oil exploration investments, seeks to elevate Brazil to the status of the world's fourth-largest oil producer. Projections for 2029 forecast Brazil's production at 5.4 million barrels daily, an 80% increase from 2021, with pre-salt areas accounting for roughly 80% of this output. The program will emphasize key exploration zones and advocate for investments in both mature and marginal fields, thereby amplifying the demand for drilling rigs.

- In August 2023, SFL Corporation Ltd. secured a drilling contract in Canada, valued at an estimated USD 100 million, with Equinor ASA's subsidiary for the semi-submersible rig Hercules. The contract encompasses one primary well, with an option for a second, and is slated to commence in Q2 2024.

- In March 2024, Dolphin Drilling, an offshore drilling contractor, clinched a long-term contract with Oil India Limited for its semi-submersible rig. Set off the coast of India, the operations involve drilling three wells over 14 months, with a projected cost of around USD 145 million.

- Given this investment landscape and the government's pivot to offshore activities due to dwindling onshore reserves, the segment is poised for growth during the study period.

North America to Dominate the Market

- North America stands as a dominant player in the global oil and gas market, largely because the United States has emerged as one of the world's leading crude oil producers in recent years.

- Moreover, the United States consistently ranks among the top in capital expenditures within the oil and gas industry, a trend that's expected to persist in the coming years.

- The United States boasts a robust offshore oil and gas industry, primarily centered around the Gulf of Mexico and offshore Alaska. As drilling depths have progressed, the surge in technically recoverable reserves has drawn significant investments to the region.

- In March 2023, the Biden administration, amidst environmental debates, sanctioned a significant oil drilling venture in Alaska. They approved a modified version of the Willow project, permitting ConocoPhillips to initiate drilling in Alaska's National Petroleum Reserve. ConocoPhillips projects a daily output of 180,000 barrels from this venture.

- Major oil and gas corporations have unveiled above-average hikes in their capital expenditures for 2023 and the years to follow. For example, Chevron Corporation, in December 2022, set its 2023 organic capital expenditure budgets at USD 14 billion for its consolidated subsidiaries and an additional USD 3 billion for its equity affiliates.

- In December 2023, ConocoPhillips took a significant step by commencing construction for oil production, a move expected to elevate the demand for drilling rig services.

- In June 2024, US Energy Development Corporation (US Energy) unveiled its ambitious plans in the Permian basin, earmarking over USD 750 million for the upcoming year, with a primary emphasis on Permian projects.

- Given these strategic investments, North America is poised to maintain its dominance in the oil and gas market in the foreseeable future.

Drilling Rig Industry Overview

The drilling rig market is fragmented. Some of the major players operating in the market (in no particular order) include Nabors Industries Ltd., Transocean Ltd., Saipem SpA, Seadrill Ltd, and Schlumberger NV, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Crude Oil Production in Million Barrels Per Day, till 2023

- 4.4 Natural Gas Production in Billion Cubic Feet, till 2023

- 4.5 Recent Trends and Developments

- 4.6 Government Policies and Regulations

- 4.7 Market Dynamics

- 4.7.1 Drivers

- 4.7.1.1 Growing Demand for Natural Gas And Developing Gas Infrastructure

- 4.7.1.2 Increase in Drilling Activities

- 4.7.2 Restraints

- 4.7.2.1 Adoption of Cleaner Alternatives

- 4.7.1 Drivers

- 4.8 Supply Chain Analysis

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Consumers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes Products and Services

- 4.9.5 Intensity of Competitive Rivalry

- 4.10 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Location of Deployment

- 5.1.1 Onshore

- 5.1.2 Offshore

- 5.2 Type

- 5.2.1 Jack-ups

- 5.2.2 Semisubmersible

- 5.2.3 Drill Ships

- 5.2.4 Other Types

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Russia

- 5.3.2.3 Norway

- 5.3.2.4 Spain

- 5.3.2.5 NORDIC Countries

- 5.3.2.6 Turkey

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Australia

- 5.3.3.4 Malaysia

- 5.3.3.5 Thailand

- 5.3.3.6 Indonesia

- 5.3.3.7 Vietnam

- 5.3.3.8 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Egypt

- 5.3.5.4 Nigeria

- 5.3.5.5 Qatar

- 5.3.5.6 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Nabors Industries Ltd.

- 6.3.2 Transocean Ltd.

- 6.3.3 Noble Corporation PLC

- 6.3.4 Saipem SpA

- 6.3.5 Arabian Drilling Company

- 6.3.6 ADES International Holding PLC

- 6.3.7 Shelf Drilling Holdings, Ltd.

- 6.3.8 Seadrill Ltd

- 6.3.9 Saudi Arabian Oil Company (Saudi Aramco)

- 6.3.10 Schlumberger NV

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements in Hydraulic Fracturing Process

掘削リグ:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日