|

市場調査レポート

商品コード

1636490

米国の電気自動車用バッテリー電解液:市場シェア分析、産業動向、成長予測(2025~2030年)United States Electric Vehicle Battery Electrolyte - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の電気自動車用バッテリー電解液:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

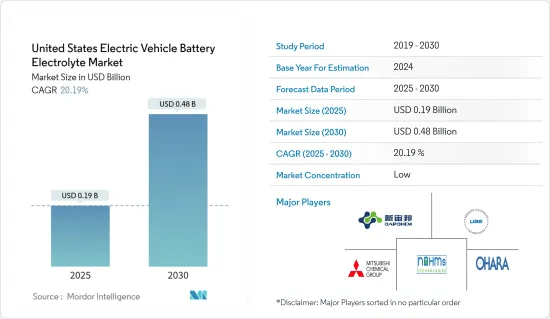

米国の電気自動車用バッテリー電解液市場規模は2025年に1億9,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは20.19%で、2030年には4億8,000万米ドルに達すると予測されます。

主要ハイライト

- 長期的には、米国ではBEV、PHEV、HEVを含む電気自動車の利用が増加しており、電気自動車の利用を促進する政府の施策が市場の成長を促進すると予測されます。

- 一方、中国のような一部の国の独占によって生じるバッテリー材料のサプライチェーン格差が、今後の市場成長を抑制すると予想されます。

- 電解質材料や効率的な電解質の研究と進歩が進んでいることは、市場成長の機会を提供する可能性があります。

米国の電気自動車用バッテリー電解質市場動向

リチウムイオンバッテリーが市場を独占する見込み

- 電気自動車(EV)の動力源として極めて重要なリチウムイオンバッテリーは、電気自動車の寿命を延ばし、バッテリー交換の頻度を最小限に抑えます。リチウムイオンバッテリーは、他のバッテリータイプとは異なり、鉛やカドミウムのような有害物質を含まないため環境に優しく、クリーンで安全な選択肢となっています。さらに、その高出力は、素早い加速と高速走行が要求されるEVには不可欠です。

- サステイナブルエネルギーのための経済人会議(BCSE)によると、2023年時点で米国のリチウムイオンバッテリー製造能力は114GWhを誇る。電気自動車の販売台数が増加しているため、自動車セクターのリチウムイオンバッテリー需要は今後数年で大きく伸びる展望です。例えば、国際エネルギー機関の報告によると、米国とカナダにおける電気自動車の販売台数は2021~2023年にかけて54%以上急増します。このようなリチウムイオンバッテリーの使用量の増加は、正極と負極の間で正リチウムイオンを輸送するのに不可欠な浸透電解質溶液の需要を後押しします。

- 2023年、アメリカの大手化学メーカーであるHuntsman Corporationは、テキサス州で電解質溶媒エチレンカーボネートの生産を増強する計画を発表しました。さらに、Capchemと共同で米国に工場を設立し、同国の電気自動車用バッテリー電解液市場をさらに強化します。

- さらに2023年3月、ホワイトハウスは「National Blueprint for Lithium Batteries」を発表し、2021~2030年までの産業の方向性を示しました。この青写真では、原料調達の強化と国内リチウム加工の強化が強調されており、電気自動車ブームによる米国のリチウムイオンバッテリー需要の急増が予想されることが強調されています。

- 電気自動車へのリチウムイオンバッテリーの採用が増加し、価格も低下していることから、このセグメントは今後数年で大きく成長する見込みです。

電気自動車の普及が市場を牽引する見込み

- 消費者の関心の高まりと政府の支援施策に後押しされ、米国では電気自動車(EV)用バッテリー電解質市場が急拡大しています。

- 特に高ニッケルや電解液の技術進歩が、バッテリーの性能と費用対効果を高めています。同時に米国は、リチウム、ニッケル、コバルトといった重要材料の国内サプライチェーンを強化し、輸入への依存度を下げ、安定性を確保することを目指しています。

- 2024年1月、マサチューセッツ工科大学(MIT)の研究者たちは、電気自動車の電源を一変させる画期的なバッテリー材料を発表しました。このリチウムイオンバッテリーは、革新的な有機材料ベースの正極と電解質溶液を特徴としており、従来のコバルトやニッケル使用からの転換を意味します。このような進歩は、バッテリー電解質材料の国内需要を増幅させることになります。

- 電気自動車の導入が急増する中、米国はバッテリー製造サプライチェーンの強化を優先しています。この勢いは、電解質を含む電気自動車用バッテリー部品の国内生産に拍車をかけると考えられます。

- 2023年6月、中国の研究開発中心企業であるCapchemは、オハイオ州南部に1億2,000万米ドルの電解質工場を建設する計画を発表しました。同時に、Dongwha Electrolyteはテネシー州で7,000万米ドルの施設を開始し、年間7万トン以上の電解液生産を目標としています。さらに、ソウルブレインはインディアナ州に7,500万米ドルの電解液工場を設立しており、近隣のバッテリー工場に対応する戦略的な立地となっています。

- 今後、EVの普及が上昇の一途をたどるなか、米国はエネルギー密度の向上、コスト削減、EV走行距離の延長を目的としたバッテリー技術の研究開発に注力し、バッテリー正極市場を活性化させると考えられます。

- 国際エネルギー機関(IEA)のデータによると、米国のEV車販売台数は大幅に増加し、2022年の99万台から2023年には139万台に急増します。

- 2030年までに2,600万台の電気自動車が普及すると予測されることから、米国では1,290万個の充電ポートが必要になると予想され、電気自動車用バッテリー正極市場が急成長する道を開いています。

- 電気自動車の普及が加速し、技術的な進歩も見られることから、米国は予測期間中、市場をリードしていくものと考えられます。

米国の電気自動車用バッテリー電解質産業概要

米国の電気自動車用バッテリー電解質市場は半分裂状態です。市場に参入している主要企業(順不同)には、Advanced Electrolyte Technologies LLC、Mitsubishi Chemical Holdings、Shenzhen Capchem Technology、Nohms Technologies Inc.、Ohara Corporationなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- BEV、PHEV、HEVを含む電気自動車の利用増加

- 電気自動車の利用を促進する有利な政府施策

- 抑制要因

- バッテリー材料のサプライチェーン格差

- 促進要因

- サプライチェーン分析

- PESTLE分析

- 投資分析

第5章 市場セグメンテーション

- バッテリータイプ

- リチウムイオンバッテリー

- 鉛蓄バッテリー

- その他

- 電解質タイプ

- 液体電解質

- ゲル電解質

- 固体電解質

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Advanced Electrolyte Technologies LLC

- Mitsubishi Chemical Holdings

- Shenzhen Capchem Technology Co., Ltd

- Nohms Technologies Inc

- Ohara Corporation

- BASF SE

- LG Chem Ltd

- Targray Industries Inc.

- 市場ランキング/シェア(%)分析

- その他の著名な企業一覧

第7章 市場機会と今後の動向

- 現在進行中の電解質材料の調査と進歩

The United States Electric Vehicle Battery Electrolyte Market size is estimated at USD 0.19 billion in 2025, and is expected to reach USD 0.48 billion by 2030, at a CAGR of 20.19% during the forecast period (2025-2030).

Key Highlights

- Over the long term, the increasing usage of electric vehicles, including BEVs, PHEVs, and HEVs, and favorable government policies to promote the usage of electric vehicles in the United States are expected to drive the market's growth.

- On the other hand, the supply chain gap in battery materials created by the monopoly of some countries like China is expected to restrain market growth in the future.

- Nevertheless, the ongoing research and advancement in electrolyte material and efficient electrolytes may offer opportunities for market growth.

United States Electric Vehicle Battery Electrolyte Market Trends

Lithium-ion Battery is Expected to Dominate the Market

- Lithium-ion batteries, pivotal for powering electric vehicles (EVs), extend the lifespan of these vehicles, thereby minimizing the frequency of battery replacements. Unlike some other battery types, lithium-ion batteries are deemed environmentally friendly, as they lack toxic materials such as lead or cadmium, making them a cleaner and safer option. Furthermore, their high power output is essential for EVs, which demand swift acceleration and elevated speeds.

- As of 2023, the United States boasts a lithium-ion battery manufacturing capacity of 114 GWh, according to the Business Council for Sustainable Energy (BCSE). With rising electric vehicle sales, the automotive sector's demand for lithium-ion batteries is poised for significant growth in the coming years. For example, the International Energy Agency reports that electric vehicle sales in the United States and Canada surged over 54% from 2021 to 2023. This uptick in lithium-ion battery usage will subsequently boost the demand for penetration electrolyte solutions, vital for transporting positive lithium ions between the cathode and anode.

- In 2023, Huntsman Corporation, a leading American chemical manufacturer, unveiled plans to boost production of the electrolyte solvent ethylene carbonate in Texas. Additionally, in collaboration with Capchem, they are establishing a plant in the United States, further bolstering the country's electric vehicle battery electrolyte solution market.

- Moreover, in March 2023, the White House unveiled the "National Blueprint for Lithium Batteries," charting the industry's course from 2021 to 2030. The blueprint emphasizes enhancing raw material sourcing and bolstering domestic lithium processing, underscoring the anticipated surge in lithium-ion battery demand in the United States driven by the electric vehicle boom.

- Given the rising adoption of lithium-ion batteries in electric vehicles and their declining prices, the segment is set for substantial growth in the coming years.

Increasing Adoption of Electric Vehicles is expected to Drive the Market

- Driven by rising consumer interest and supportive government policies, the United States is witnessing a rapid expansion in its electric vehicle (EV) battery electrolyte market.

- Technological advancements, particularly in high-nickel and electrolyte solutions, are boosting battery performance and cost-effectiveness. Concurrently, the U.S. is bolstering its domestic supply chain for critical materials such as lithium, nickel, and cobalt, aiming to reduce import reliance and ensure stability.

- In January 2024, MIT researchers unveiled a groundbreaking battery material set to transform electric vehicle power sources. This lithium-ion battery, featuring an innovative organic material-based cathode and electrolyte solution, marks a shift from the traditional cobalt or nickel usage. Such advancements are poised to amplify the nation's demand for battery electrolyte materials.

- As electric vehicle adoption surges, the United States is prioritizing the fortification of its battery manufacturing supply chain. This momentum is likely to spur domestic production of electric vehicle battery components, including electrolytes.

- In June 2023, Capchem, a China-based R&D-centric company, unveiled plans for a USD 120 million electrolyte plant in southern Ohio. Simultaneously, Dongwha Electrolyte commenced a USD 70 million facility in Tennessee, targeting an annual production of over 70,000 metric tons of electrolytes. Additionally, Soulbrain is establishing a USD 75 million electrolyte plant in Indiana, strategically located to cater to a nearby battery factory.

- Looking ahead, as EV adoption continues its upward trajectory, the United States's R&D focus on battery technology-aimed at boosting energy density, cutting costs, and extending EV range-will likely invigorate the battery cathode market.

- Data from the International Energy Agency highlights a significant jump in United States EV car sales, soaring to 1.39 million units in 2023 from 0.99 million in 2022.

- With projections of 26 million electric vehicles by 2030, the United States anticipates a need for 12.9 million charging ports, paving the way for a burgeoning electric vehicle battery cathode market.

- Given the accelerating adoption of EVs and technological strides, the United States is poised to lead the market during the forecast period.

United States Electric Vehicle Battery Electrolyte Industry Overview

The United States Electric Vehicle Battery Electrolyte Market is semi-fragmented. Some of the major companies operating in the market (in no particular order) include Advanced Electrolyte Technologies LLC, Mitsubishi Chemical Holdings, Shenzhen Capchem Technology Co., Ltd, Nohms Technologies Inc., and Ohara Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 The Increasing Usage of Electric Vehicles, including BEVs, PHEVs, and HEVs

- 4.5.1.2 Favorable government policies to promote the usage of electric vehicles

- 4.5.2 Restraints

- 4.5.2.1 The Supply chain gap in battery materials

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-Ion Batteries

- 5.1.2 Lead-Acid Batteries

- 5.1.3 Other type of Batteries

- 5.2 Electrolyte Type

- 5.2.1 Liquid Electrolyte

- 5.2.2 Gel Electrolyte

- 5.2.3 Solid Electrolyte

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Advanced Electrolyte Technologies LLC

- 6.3.2 Mitsubishi Chemical Holdings

- 6.3.3 Shenzhen Capchem Technology Co., Ltd

- 6.3.4 Nohms Technologies Inc

- 6.3.5 Ohara Corporation

- 6.3.6 BASF SE

- 6.3.7 LG Chem Ltd

- 6.3.8 Targray Industries Inc.

- 6.4 Market Ranking/Share (%) Analysis

- 6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Ongoing Research and Advancement in Electrolyte Material