石油・ガス用静止・回転機器:市場シェア分析、産業動向、成長予測(2025~2030年)

Oil & Gas Static And Rotating Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636229

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

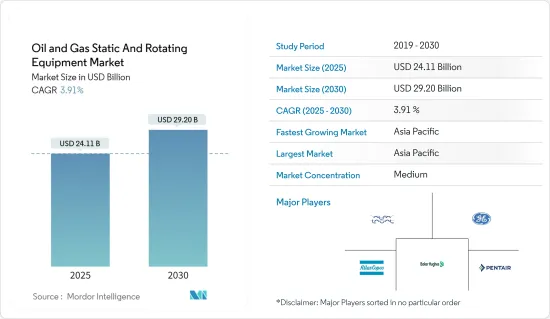

石油・ガス用静止・回転機器市場規模は2025年に241億1,000万米ドルと推定・予測され、予測期間(2025~2030年)のCAGRは3.91%で、2030年には292億米ドルに達すると予測されます。

主要ハイライト

- 石油・ガス用静止・回転機器市場は、世界のエネルギー需要の増加と、海洋探査活動の活発化による静止回転機器へのニーズから、予測期間中に成長すると予想されます。

- 一方で、再生可能でクリーンなエネルギー源の採用が増加していることが、今後の市場成長の妨げになると予想されます。

- しかし、予測期間中に機器の効率を向上させる技術の進歩により、市場が大きく成長する機会があります。

- アジア太平洋は予測期間中、市場の大幅な成長が見込まれます。

石油・ガス用静止・回転機器市場動向

回転機器セグメントは大きな需要が見込まれる

- 石油・ガス産業では、回転機器が重要な役割を果たしています。この装置の回転部品は、エンジン、コンプレッサー、タービン、工業用バルブなどで構成されます。回転機器の多くは、ある場所からによる場所へ物質を輸送するために使用されるか、プロペラを回転させるなどして物質を強制的に回転させるために使用されます。

- 回転機器は、上流、下流、下流などの産業で使用されます。ポンプとコンプレッサーは、石油・ガスの生産と貯蔵においていくつかの用途を持つ回転機器の一例です。

- いくつかの石油・ガスプロジェクトでは、回転機器を設置するために他社と協定や契約が結ばれています。例えば、2024年5月、Larsen & Toubro(L&T)、L&T Energy Hydrocarbon(LTEH)は、ONGCから、ONGCのムンバイ・ハイとタプティ沖合にある新しいプロセスガス・コンプレッサー(PGC)モジュールのエンジニアリング、調達、建設、据付、試運転を受注しました。

- さらに、ガス生産量の増加により、コンプレッサーやポンプのような回転機器への需要が見込まれます。Statistical Review of World Energy Dataによると、2023年の世界のガス生産量は4兆592億立方メートルです。ガス生産量は2010年以降継続的に増加しており、2020年には若干減少します。

- さらに、各企業は研究開発への投資を増やし、回転機器の効率を向上させる努力をしており、それが将来的に回転機器のビジネス機会を生み出すことになります。

- 例えば、2024年5月、回転機器ソリューションとエネルギー転換技術の世界的リーダーであるJohn Craneは、カナダのアルバータ州で5年間の契約を獲得しました。この契約では、大手複合施設向けに工業用シールのサポートサービスを記載しています。この契約の一環として、ジョン・クレーンは現場の重要な資産の寿命を延ばすために、管理信頼性プログラム(MRP)を実施しています。これには、遠心ポンプや工業用シールなどの回転機器が含まれます。このようなプログラムは、回転機器の効率を向上させ、将来の需要を促進すると期待されています。

- このように、石油・ガス産業における回転機器の使用と需要のおかげで、このセグメントは予測期間中に大きな需要を持つことが期待されています。

アジア太平洋は市場の著しい成長が期待される

- アジア太平洋は、世界人口の半分以上を擁しており、世界のエネルギーの将来に大きな影響を与える可能性を秘めています。この地域には、急速な都市化と工業化を経験しているインド、中国、日本などの新興諸国が含まれます。

- そのため、この地域のエネルギー需要は継続的に増加しており、石油・ガス産業における生産・探査活動が求められています。今後の石油・ガスプロジェクトに伴い、同地域では静止・回転機器の需要が拡大すると予想されます。

- 例えば、2022年10月、SENEX Energyは、クイーンズランド州南西部のアトラスプロジェクトに隣接して、新しいガス圧縮施設を建設すると発表しました。このガスプラントは、生産ライセンスPL209を利用して建設されます。石油・ガス生産の増加に伴い、同設備の需要は予測期間中に拡大すると予想されます。

- Statistical Review of World Energy Dataによると、2023年のアジア太平洋のガス総生産量は6,918億立方メートルで、前年比年率0.6%増です。

- さらに、下流プロジェクトの開発が同地域の市場を牽引すると予想されます。石油化学産業では、精製に静止装置と回転装置が使用されます。2023年3月、Indian Oil Corporation Ltdは、オディシャ州パラディップに石油化学コンプレックスを建設するために7億4,200万米ドルを投資すると発表しました。このような新規プロジェクトは装置需要を増加させ、市場を牽引すると予想されます。

- 同地域における天然ガス生産需要の増加は、石油・ガス始動装置や回転装置のニーズを急増させると予想されます。例えば、ガス輸出国フォーラムによると、2050年までに東南アジアの総発電構成の36%を天然ガスが占めると予測されています。まとめると、アジア太平洋の天然ガス需要は大幅に伸びると予想され、2050年には710bcmに達すると予測されています。

- 石油・ガス産業の開発とエネルギー需要の増加により、アジア太平洋は大きく成長すると予想されます。

石油・ガス用静止・回転機器産業概要

石油・ガス用静止・回転機器市場は半分断されています。同市場の主要企業(順不同)には、Alfa Laval AB、Atlas Copco AB、General Electric Co.、Baker Hughes Co.、Pentair PLCなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:10億米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- エネルギー需要の増加

- 海洋探査活動の活発化

- 抑制要因

- 再生可能でクリーンなエネルギー源の採用増加

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- 用途

- 上流

- 中流

- 川下

- タイプ

- 静止型

- 回転式

- 地域

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- ロシア

- ノルディック

- イタリア

- その他の欧州

- アジア太平洋

- 中国

- インド

- オーストラリア

- 日本

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- エジプト

- カタール

- ナイジェリア

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Alfa Laval AB

- Atlas Copco AB

- General Electric Co

- Baker Hughes Co.

- Pentair PLC

- Siemens AG

- Sulzer Limited

- FMC Technologies Inc.

- Flowserve Corporation

- Mitsubishi heavy Industries Ltd

- Doosan Group

- その他の著名な企業一覧

- 市場ランキング分析

第7章 市場機会と今後の動向

- 効率性を高める技術の進歩

目次

Product Code: 50003497

The Oil & Gas Static And Rotating Equipment Market size is estimated at USD 24.11 billion in 2025, and is expected to reach USD 29.20 billion by 2030, at a CAGR of 3.91% during the forecast period (2025-2030).

Key Highlights

- The oil and gas static and rotating equipment market is expected to grow during the forecast period due to increasing global energy demand and the need for static rotating equipment from increased offshore exploration activities.

- On the other hand, the rising adoption of renewable and cleaner energy sources is expected to hamper the market growth in the future.

- However, there is an opportunity for significant market growth through technological advancements to improve equipment efficiency during the forecast period.

- Asia-Pacific is expected to witness significant growth in the market during the forecast period.

Oil & Gas Static And Rotating Equipment Market Trends

The Rotating Equipment Segment is Expected to Have a Significant Demand

- Rotating equipment plays a significant role in the oil and gas industry. The rotating components of this equipment may consist of engines, compressors, turbines, and industrial valves. Most of the rotating equipment is used to transport substances from one area to another, or it may be used to force materials to rotate, such as by making a propeller turn.

- Rotating equipment is used in industries, including upstream, downstream, and downstream. Pumps and compressors are examples of rotating equipment that have several uses in the production and storage of oil and gas.

- In several oil and gas projects, agreements and contracts are made with other companies to install rotating equipment. For example, in May 2024, Larsen & Toubro (L&T), L&T Energy Hydrocarbon (LTEH), got a contract from ONGC for the engineering, procurement, construction, installation, and commissioning of new process gas compressor (PGC) modules at ONGC's Mumbai High and Tapti offshore locations.

- Further, increasing gas production is expected to create demand for rotating equipment like compressors and pumps. According to the Statistical Review of World Energy Data, in 2023, global gas production accounted for 4059.2 billion cubic meters. Gas production has increased continuously since 2010, with a slight drop in 2020.

- Moreover, companies are making efforts to improve the efficiency of rotating equipment by investing more and more in research and development, which, in turn, will create opportunities for these equipment in the future.

- For instance, in May 2024, John Crane, a global leader in rotating equipment solutions and energy transition technologies, secured a five-year contract in Alberta, Canada. The contract involves providing industrial seal support services for a major complex. As part of this agreement, John Crane is implementing a managed reliability program (MRP) to enhance the longevity of critical site assets. This includes rotating equipment like centrifugal pumps and industrial seals. Such programs are expected to improve rotating equipment efficiency, driving future demand.

- Thus, owing to the use and demand for rotating equipment in the oil and gas industry, the segment is expected to have a significant demand during the forecast period.

Asia-Pacific is Expected to Have a Significant Growth in the Market

- Asia-Pacific is home to over half of the world's population, giving it the potential to influence the future of global energy significantly. The region includes developing countries like India, China, and Japan, which are experiencing rapid urbanization and industrialization.

- Thus, the region's energy demand is increasing continuously, which, in turn, demands production and exploration activities in the oil and gas industry. With the upcoming oil and gas projects, the demand for static and rotating equipment is expected to grow in the region.

- For example, in October 2022, SENEX Energy announced the construction of a new gas compression facility adjacent to its Atlas project in southwest Queensland. The gas plant will be constructed using production license PL209. With increasing oil and gas production, demand for this equipment is expected to grow during the forecast period.

- According to Statistical Review of World Energy Data, in 2023, Asia-Pacific total gas production accounted for 691.8 billion cubic meters, an annual growth rate of 0.6% compared to the previous year.

- Further, the development of downstream projects is expected to drive the market in the region. In the petrochemical industry, static and rotating equipment are used in refining. In March 2023, Indian Oil Corporation Ltd announced it would invest USD 742 million in building a petrochemical complex at Paradip in Odisha. Such new projects are expected to increase the demand for equipment, thereby driving the market.

- The increasing demand for natural gas production in the region is expected to surge the need for oil and gas starting and rotating equipment. For instance, according to the Gas Exporting Countries Forum, natural gas is projected to account for 36% of Southeast Asia's total generation mix by 2050. In summary, Asia-Pacific's demand for natural gas is expected to grow significantly, with estimates reaching 710 bcm by 2050.

- Due to the development of the oil and gas industry and the increasing energy demand, Asia-Pacific is expected to grow significantly.

Oil & Gas Static And Rotating Equipment Industry Overview

The oil and gas static and rotating equipment market is semi-fragmented. The key players in the market (in no particular order) include Alfa Laval AB, Atlas Copco AB, General Electric Co, Baker Hughes Co., and Pentair PLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Energy Demand

- 4.5.1.2 More Offshore Exploration Activities

- 4.5.2 Restraints

- 4.5.2.1 Rising Adoption of Renewable and Cleaner Energy Sources

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Upstream

- 5.1.2 Midstream

- 5.1.3 Downstream

- 5.2 Type

- 5.2.1 Static

- 5.2.2 Rotating

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Spain

- 5.3.2.5 Russia

- 5.3.2.6 NORDIC

- 5.3.2.7 Italy

- 5.3.2.8 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Australia

- 5.3.3.4 Japan

- 5.3.3.5 Malaysia

- 5.3.3.6 Thailand

- 5.3.3.7 Indonesia

- 5.3.3.8 Vietnam

- 5.3.3.9 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 Saudi Arabia

- 5.3.4.2 United Arab Emirates

- 5.3.4.3 Egypt

- 5.3.4.4 Qatar

- 5.3.4.5 Nigeria

- 5.3.4.6 South Africa

- 5.3.4.7 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Colombia

- 5.3.5.4 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Alfa Laval AB

- 6.3.2 Atlas Copco AB

- 6.3.3 General Electric Co

- 6.3.4 Baker Hughes Co.

- 6.3.5 Pentair PLC

- 6.3.6 Siemens AG

- 6.3.7 Sulzer Limited

- 6.3.8 FMC Technologies Inc.

- 6.3.9 Flowserve Corporation

- 6.3.10 Mitsubishi heavy Industries Ltd

- 6.3.11 Doosan Group

- 6.4 List of Other Prominent Companies

- 6.5 Market RankingAnalysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancement to Increase the Efficiency

石油・ガス用静止・回転機器:市場シェア分析、産業動向、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日