|

市場調査レポート

商品コード

1636216

インランドコンテナデポおよびドライポート:市場シェア分析、産業動向、成長予測(2025年~2030年)Inland Container Depot And Dry Port - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インランドコンテナデポおよびドライポート:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

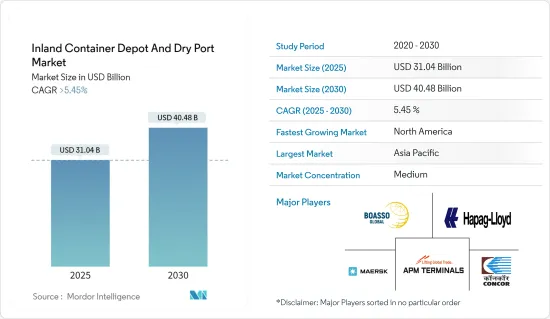

インランドコンテナデポおよびドライポートの市場規模は2025年に310億4,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは5.45%を超え、2030年には404億8,000万米ドルに達すると予測されます。

主なハイライト

- インランドコンテナデポおよびドライポート業界は、港の閉鎖、混雑、燃料価格の高騰により、主にCOVID-19の流行による低迷に直面しました。2020年、世界のコンテナ輸送量は約0.8%減少し、調査対象市場に直接影響を与えました。逆に、紅海危機に起因する最近のコンテナ運賃の高騰は、コンテナ保管とメンテナンスへの投資を大手企業に思いとどまらせた。

- インランドコンテナデポ(ICD)を選択する企業は、自動車や商品から原油や鉱物まで、貨物の性質に応じて選択します。COVID-19の大流行後、世界市場ではICDに対する需要の高まりが見られました。この急増は、国内および国際eコマース市場の拡大、貿易関係の改善、自由貿易協定の普及によって促進されました。特に、国連貿易開発局(UN Trade and Development)の報告によると、世界の商品貿易額は2023年に2兆米ドルに達し、この動向は今後も続くと予想され、市場の成長を後押しします。

- 市場の成長は、主に海上貿易の拡大とコンテナ・ハンドリング・サービスの需要増によってもたらされます。しかし、港湾や保管サービスのコストが高いという課題により、市場の成長は抑制されています。市場は、特に人工知能、自動化、IoT、ロボット工学のような最先端技術の出現により、新たな機会を迎える態勢が整っています。

- アジア太平洋が市場をリードする一方、北米が急成長地域として浮上しています。新規港湾投資の急増を目の当たりにしているアジア太平洋は際立っており、インドだけでも820億米ドル以上を400以上の港湾に投入しています。中国、シンガポール、日本、フィリピンも、港湾開発に積極的に新技術を取り入れています。対照的に、北米は港湾とコンテナ荷役事業体の強固な存在を誇っています。

インランドコンテナデポおよびドライポートの市場動向

マルチモーダルコネクティビティがインランドコンテナデポの需要を押し上げる

- 貨物輸送とロジスティクスにおける持続可能性の推進が、マルチモーダル輸送の台頭を後押ししています。このアプローチは、貨物の剛性を確保し、移動中の損傷を防ぐために、複数の輸送手段(トラック、列車、船舶など)を利用することを重視しています。その結果、頑丈で耐久性のあるコンテナ貨物の需要が急増しました。このようなコンテナ需要の増加は、インランドコンテナデポやドライポートのニーズの高まりに直結しています。

- 鉄道と道路の接続が強化されたことで、インランドコンテナデポ(ICD)はよりアクセスしやすく効率的になり、市場の成長に拍車をかけています。海港と内陸部の架け橋となるこれらの発着所は、複合一貫輸送の要となりつつあり、コンテナ保管とメンテナンス・サービスのニーズを高めています。

- ロジスティクス業界は、鉄道貨物を複合一貫輸送サービスの重要な構成要素としてますます利用するようになっており、各旅程でより効率的な貨物移動を目指しています。このシフトは、コンテナ輸送の需要を直接的に増大させ、その結果、ICDのニーズを急増させています。

- 鉄道貨物量の急増に伴い、ICDの需要もそれに追随する勢いです。特に米国では、2016年から鉄道貨物量が着実に増加し、2023年には2兆1,800億トンキロに達します。この動向は米国に限ったことではなく、世界的に同様のパターンが見られます。

- 道路、鉄道、時には水路輸送を組み合わせた複合一貫輸送が、この急増の中核をなしています。ICDは、これらの輸送手段の中心的なハブとして、シームレスな貨物輸送を促進し、全体的な輸送効率を高め、輸送時間を短縮します。

- この効率性、コスト削減、そして現代の複雑なサプライチェーンに対応する能力により、ICDはますます不可欠な存在となっています。世界貿易の拡大に伴い、より広範な輸送ネットワークにおけるICDの重要性は高まる一方です。

南北アメリカは急成長地域

- 国際貿易は南北アメリカの経済景観を大きく支えています。北米の港湾は、重要な貿易ゲートウェイとして、船舶、列車、トラックによって年間数十億トンの貨物が輸送されています。

- 世界の海上貿易の約7%を占めるラテンアメリカは、主に鉱物、野菜、多様な食品を輸出しています。このような輸出の急増が、より多くのコンテナと内陸コンテナ・ターミナルの必要性に拍車をかけています。この地域の貿易力学は、世界の主要な海上航路、特に欧州、北米、そして最近ではアジア太平洋と複雑にリンクしています。

- ラテンアメリカの上位20の港湾とコンテナ・ターミナルは、業界団体によって強調されているように、この地域の総処理量の80%以上を占めています。2023年には、極東からSAEC(南米東海岸)へのコンテナ貨物の輸入が着実に増加し、最初の8ヵ月で14.5%急増しました。

- これらの貨物のスポット市場はボラティリティを示したが、10月までの運賃は年初から-2%の下落にとどまり、期間中の平均は1FEU当たり2,716米ドルだったが、2,048米ドルから3,286米ドルの間で変動しました。

- このデータは、南北アメリカ全体で海上貨物需要が高まっていることを浮き彫りにし、コンテナ処理量の増加を促し、市場の研究を後押ししています。

インランドコンテナデポおよびドライポート業界の概要

同市場は比較的断片化されており、A.P. Moller-Maersk、Boasso Global、Container Corporation of India(CONCOR)、APM Terminals、Hapag Llyodなど、世界および地域レベルでデポを運営する企業が複数存在します。多くの企業がこの市場に参入しているため、予測期間中に市場は成長すると予想されます。さらに、国際貿易を加速させるため、欧州とアジアのいくつかの国の政府はコンテナデポサービスを提供しており、これは市場をさらに強化すると予想されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- ICDの現在の市場シナリオ

- 世界の海運業界に関する洞察

- 政府の規制と取り組み

- 技術動向と自動化

- バリューチェーン/サプライチェーン分析

- ICDにおけるコンテナハンドリング機器のレビューと解説

- パンデミックと地政学的緊張が市場に与える影響

第5章 市場力学

- 市場促進要因

- 市場抑制要因

- 市場機会

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第6章 市場セグメンテーション

- サービス別

- 保管

- ハンドリング

- 保守・修理

- コンテナタイプ別

- 一般

- 冷蔵(リーファー)

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- その他アジア太平洋地域

- 南米

- ブラジル

- チリ

- 中東

- アラブ首長国連邦

- サウジアラビア

- その他中東

- 北米

第7章 競合情勢

- 市場集中度の概要

- 企業プロファイル

- Boasso Global

- Maersk

- Container Corporation of India(CONCOR)

- APM Terminals

- Hapag Llyod

- Hutchison Ports

- GAC

- DP World

- Abu Dhabi Terminals

- Freightliner Group Ltd*

- その他の企業

第8章 市場の将来

第9章 付録

- マクロ経済指標

- 資本フローの洞察(輸送・貯蔵部門への投資)

- 対外貿易統計

The Inland Container Depot And Dry Port Market size is estimated at USD 31.04 billion in 2025, and is expected to reach USD 40.48 billion by 2030, at a CAGR of greater than 5.45% during the forecast period (2025-2030).

Key Highlights

- The inland container depot and dry port industry faced a downturn due to port closures, congestion, and fuel price hikes, largely due to the COVID-19 pandemic. In 2020, global container transport volumes dipped by approximately 0.8%, directly impacting the market studied. Conversely, a recent surge in container freight rates, attributed to the Red Sea crisis, has dissuaded major players from investing in container storage and maintenance.

- Companies opting for inland container depots (ICDs) tailor their choices based on the nature of the cargo, which can range from cars and merchandise to crude oil and minerals. After the COVID-19 pandemic, the global market witnessed rising demand for ICDs. This surge was fueled by the expanding domestic and international e-commerce markets, improving trade relations, and the proliferation of free-trade agreements. Notably, global goods trade hit USD 2 trillion in 2023, as reported by the UN Trade and Development, a trend expected to persist, propelling market growth.

- The market's growth is primarily driven by escalating maritime trade and the increasing demand for container handling services. However, market growth is restrained due to the challenges of high port and storage service costs. The market is poised for new opportunities, especially with the advent of cutting-edge technologies like artificial intelligence, automation, IoT, and robotics.

- While Asia-Pacific leads the market, North America emerges as the fastest-growing region. Asia-Pacific, witnessing a surge in new port investments, stands out, with India alone injecting over USD 82 billion into 400+ ports. Not to be outdone, China, Singapore, Japan, and the Philippines actively embrace new technologies in their port developments. In contrast, North America boasts a robust presence of port and container handling entities.

Inland Container Depot and Dry Port Market Trends

Multimodal Connectivity Boosts Demand for Inland Container Depots

- The push for sustainability in freight and logistics has propelled the rise of multimodal transportation. This approach emphasizes using multiple modes of transport (trucks, trains, ships, etc.) to ensure cargo rigidity and prevent damage during transitions. Consequently, there has been a surge in demand for containerized cargo, given their solid and durable nature. This uptick in container demand has directly translated into a heightened need for inland container depots and dry ports.

- Enhanced rail and road connections make inland container depots (ICDs) more accessible and efficient, fueling market growth. By bridging seaports and inland areas, these depots are becoming pivotal for intermodal transportation, driving up the need for container storage and maintenance services.

- The logistics industry is increasingly turning to rail freight as a key component of its multimodal services, aiming for more efficient cargo movement in each trip. This shift is directly amplifying the demand for containerized transport, subsequently spiking the need for ICDs.

- With the surge in rail freight volumes, the demand for ICDs is poised to follow suit. Notably, the United States witnessed a steady rise in rail freight volumes from 2016, culminating in 2.18 trillion tonne-km in 2023. This trend is not exclusive to the United States; similar patterns are seen globally.

- Multimodal connectivity, which blends road, rail, and sometimes waterway transport, is at the core of this surge. ICDs, serving as central hubs for these modes, facilitate seamless cargo transfers, enhancing overall transport efficiency and trimming transit times.

- This efficiency, cost savings, and the ability to navigate modern supply chain complexities make ICDs increasingly indispensable. As global trade expands, the significance of ICDs in the broader transport network is only set to grow.

The Americas is the Fastest-growing Region

- International trade significantly bolsters the economic landscapes of the Americas. North America's ports, serving as crucial trade gateways, witness the transit of billions of tons of cargo annually, facilitated by ships, trains, and trucks.

- Latin America, contributing around 7% to global maritime trade, predominantly ships raw minerals, vegetables, and a diverse range of food products. This surge in exports has, in turn, fueled the need for more containers and inland container terminals. The region's trade dynamics are intricately linked to the world's primary maritime routes, notably Europe, North America, and, increasingly, Asia-Pacific.

- The top 20 ports and container terminals in Latin America, as highlighted by an industry association, accounted for over 80% of the region's total throughput. In 2023, imports of containerized goods into SAEC (East Coast South America) from the Far East saw a steady rise, with volumes spiking by 14.5% in the initial eight months, translating to an extra 20,000 TEU monthly.

- While the spot market for these goods exhibited volatility, rates by October had only dipped by -2% from the year's start, averaging at USD 2,716 per FEU over the period but fluctuating between USD 2,048 and USD 3,286.

- This data underscores the mounting sea freight demand across the Americas, propelling increased container throughput and bolstering the market studied.

Inland Container Depot and Dry Port Industry Overview

The market is relatively fragmented, with several players operating depots on global and regional levels like A.P. Moller-Maersk, Boasso Global, Container Corporation of India (CONCOR), APM Terminals, and Hapag Llyod. As many companies are jumping into the market, the market is expected to grow during the forecast period. Additionally, to accelerate international trade, governments of several countries in Europe and Asia are offering container depot services, which is further expected to strengthen the market

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario's of ICDs

- 4.2 Insights on Global Shipping Industry

- 4.3 Government Regulations and Initiatives

- 4.4 Technological Trends and Automation

- 4.5 Value Chain/Supply Chain Analysis

- 4.6 Review and Commentary on Container Handling Equipment in ICDs

- 4.7 Impact of Pandemics and Geopolitical Tensions on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.2 Market Restraints

- 5.3 Market Opportunities

- 5.4 Porter's Five Forces Analysis

- 5.4.1 Threat of New Entrants

- 5.4.2 Bargaining Power of Buyers/Consumers

- 5.4.3 Bargaining Power of Suppliers

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Service

- 6.1.1 Storage

- 6.1.2 Handling

- 6.1.3 Maintenance and Repair

- 6.2 By Type of Container

- 6.2.1 General

- 6.2.2 Refrigerated (Reefer)

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 UK

- 6.3.2.3 France

- 6.3.2.4 Russia

- 6.3.2.5 Spain

- 6.3.2.6 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 India

- 6.3.3.2 China

- 6.3.3.3 Japan

- 6.3.3.4 Rest of Asia-Pacific

- 6.3.4 South America

- 6.3.4.1 Brazil

- 6.3.4.2 Chile

- 6.3.5 Middle East

- 6.3.5.1 United Arab Emirates

- 6.3.5.2 Saudi Arabia

- 6.3.5.3 Rest of Middle East

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 Boasso Global

- 7.2.2 Maersk

- 7.2.3 Container Corporation of India (CONCOR)

- 7.2.4 APM Terminals

- 7.2.5 Hapag Llyod

- 7.2.6 Hutchison Ports

- 7.2.7 GAC

- 7.2.8 DP World

- 7.2.9 Abu Dhabi Terminals

- 7.2.10 Freightliner Group Ltd*

- 7.3 Other Companies

8 FUTURE OF THE MARKET

9 APPENDIX

- 9.1 Macroeconomic Indicators

- 9.2 Insight Into Capital Flows (Investments In Transport and Storage Sector)

- 9.3 External Trade Statistics