|

市場調査レポート

商品コード

1636212

有害廃棄物管理:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Hazardous Waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 有害廃棄物管理:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

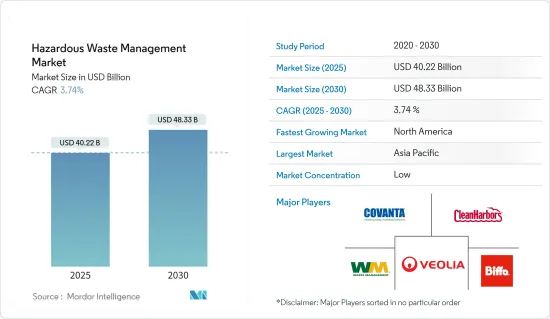

有害廃棄物管理の市場規模は2025年に402億2,000万米ドルと推定され、予測期間中(2025-2030年)のCAGRは3.74%で、2030年には483億3,000万米ドルに達すると予測されます。

主なハイライト

- 有害廃棄物管理には、人の健康や環境を脅かす物質を取り扱い、管理し、処分するための慣行や手順が含まれます。廃棄物の収集、リサイクル、治療、輸送、処分、処分場の監視などが含まれます。主な目的は、リスクを軽減し、健康と環境を守ることです。

- 有害廃棄物管理市場は、いくつかの要因によって牽引されています。世界各国の政府は、汚染や健康リスクに対する懸念から、廃棄物処理への注力を強めています。その結果、廃棄物処理の慣行を管理し、責任ある管理を奨励するために、より厳しい規制が制定されつつあります。

- 技術の進歩は有害廃棄物管理を大幅に強化しました。廃棄物処理と処分における技術革新は、より効率的で環境に優しい方法の到来を告げています。注目すべき技術には、蒸気オートクレーブ処理、化学処理、オゾン処理、熱分解、電子ビーム技術などがあります。例えばペロは、企業が環境への影響を減らし、廃棄物収集をより効率的に管理できるよう開発された新技術です。ペロは、さまざまな方法で企業の目標達成を支援します。まず、ペロ・システムはゴミ箱の満杯レベルを監視し、ゴミ箱の中身と場所に関する情報をリアルタイムで提供します。

- 2023年4月、Recycle Track Systems(RTS)はRecycleSmart Solutionsを買収し、高度な廃棄物転換、有機物回収、リサイクル管理技術を提供するカナダ随一の独立系プロバイダーとしての地位を固めました。この買収は、モノのインターネット(IoT)プラットフォームの不可欠な部分であるRecycle Smartの最先端のPello廃棄物センサー技術を包含しています。

有害廃棄物管理市場の動向

アジア太平洋地域が今後数年間で市場を独占する見込み

- 中国、インド、東南アジア諸国などの急速な工業化により、特に製造業、鉱業、電子機器などの産業で有害廃棄物の生産が急増しています。例えば中国では、1990年代から廃棄物排出量が約3倍に増加しています。この増加には複数の要因があります。過去数十年間、中国の都市化率は着実に上昇してきました。2023年までに、人口の約66.2%が都市部に居住していることが、中国国家統計局のデータから明らかになった。

- 国際通貨基金(IMF)によれば、2023年のGDPが約17兆7,000億米ドルであることからも明らかなように、中国の力強い経済成長は、産業廃棄物の生産をさらに促進しました。鉱滓やフライアッシュのような従来型の産業廃棄物の量は安定しているが、有害廃棄物の生産量は産業の進歩に伴って急増しています。特筆すべきは、これらの有害製品別を安全に処分するためには、より高度な処理が必要だということです。2024年3月、ジェレ・グループが分散型有害廃棄物処理装置「GreenWell」を発表し、大きな節目を迎えました。この革新的なソリューションは、集中型の有害廃棄物処理における課題に対処するために開発されたもので、中間工程の必要性を回避し、現場での処理を可能にします。

- 現場での処理を合理化し、中間工程を省くことで、この最新鋭の装置は処理効率を大幅に高め、廃棄物を削減し、システム内での廃水リサイクルを促進します。印象的なことに、この装置はすでにその有効性を実証しており、坑井現場での油性廃棄物を20%以上削減し、基本油の回収率95%という卓越した結果を達成しています。さらに、その運用枠内で廃水のゼロ排出リサイクルを可能にしています。

- 過去数十年にわたり、アジア太平洋地域は有害廃棄物管理に関する規制枠組みの強化において顕著な進歩を遂げてきました。各国政府は環境規制を強化し、産業界はより強固な廃棄物管理慣行を採用することを余儀なくされています。例えば2021年、インド中央政府は「ゴミのない都市」を構想するスワチ・バーラト・ミッション都市2.0(SBM-U 2.0)を開始しました。このミッションは、都市固形廃棄物の戸別収集、発生源分別、科学的処理を重視し、すべての都市自治体が少なくとも3つ星の認証を確保することを目標としています。

- アジア、特に中国における急速な工業化は、有害廃棄物発生量の顕著な増加をもたらしたが、廃棄物処理技術の進歩や厳しい規制の枠組みは、より効率的で環境に優しい廃棄物管理慣行への転換を促しています。

- 中国やインドのような急速に工業化が進む国々における有害廃棄物発生量の急増は、高度な廃棄物管理ソリューションの必要性を浮き彫りにしています。中国の著しい経済成長と都市化は有害廃棄物の増加に直接寄与しており、GreenWell装置のような革新的な治療技術が必要とされています。この技術は、処理効率を向上させるだけでなく、廃水のリサイクルを通じて環境の持続可能性をサポートします。さらに、アジア太平洋全域で規制の枠組みが強化されていることは、環境課題への取り組みが強まっていることを示しており、産業界はより良い廃棄物管理方法を採用するよう迫られています。こうした動向は、アジア太平洋地域における産業がより持続可能な成長を遂げつつあることを示唆しています。

廃棄物処理タイプ別では、回収が今後さらに牽引力を増す

- 有害廃棄物の収集には、人の健康や環境に重大なリスクをもたらす物質を収集、管理、輸送するための体系的な手順が含まれます。これらの物質は、固有の特性(可燃性、毒性など)や規制機関による特定の指定に基づいて分類されます。正確な識別は、適切な取り扱いと廃棄プロトコルを適用するために非常に重要です。

- 2024年7月、メキシコの環境事務局Sedemaは、XochimilcoとGustavo Maderoにある不法投棄場から5,600本以上のタイヤを処理工場に運ぶことに成功しました。これらのタイヤは、セメント製造の代替燃料として再利用されます。ジオサイクル・メヒコと提携したこの動きは、不適切なタイヤ廃棄による環境課題と闘うセデマの戦略の礎石となるものであり、しばしば公共汚染や山火事リスクの増大につながります。セデマは、レシクラトロン・プログラムを通じてタイヤ回収を強化する計画を発表し、全体的な廃棄物管理へのメキシコのコミットメントと、化石燃料や過剰な鉱物採掘からの脱却を示しました。

- 2024年6月、オタワ市議会は固形廃棄物マスタープランを承認しました。埋立地の更新は6億米ドルを超える可能性があると懸念されています。承認された30年にわたる戦略には、50近くのイニシアチブが含まれています。これらは廃棄物を転換し、埋立地の寿命を2049年まで延ばすことを目的としています。オタワのアプローチは、持続可能な廃棄物管理と長期的な環境スチュワードシップへの献身を強調しています。

- 効果的な有害廃棄物収集には、厳格な規制遵守、適切な人材育成、廃棄物排出事業者、輸送業者、処分施設を含む利害関係者間の協力が必要です。このような協力体制により、安全でコンプライアンスを遵守した有害廃棄物管理が実現します。

- 有害廃棄物収集市場は、規制遵守と革新的な廃棄物管理によって進化しています。メキシコにおけるセデマの取り組みは、廃棄物の再利用、環境リスクの低減、持続可能性の促進に対する積極的な姿勢を示しています。オタワのマスタープランは、廃棄物の削減と資源管理へのコミットメントを反映したもので、当面の埋立地と将来の埋立地の両方の懸念に対処しています。これらの動向は、持続可能性と公衆衛生を優先し、統合的な廃棄物管理を目指す広範な傾向を浮き彫りにしています。

有害廃棄物管理業界の概要

有害廃棄物管理市場は適度に断片化されており、競争も激しいです。Veolia、Biffa、Covanta Holding、Clean Harbors、Suez Groupなどが有害廃棄物管理市場の主要企業です。

さらに、同市場の主要企業は、市場での存在感を高めるため、新たな施設の拡大などの取り組みを行っています。例えば、2022年5月、トリニダード・トバゴ固体廃棄物管理会社(SWMCOL)は、古い携帯電話をリサイクルするための回収サイトを立ち上げました。この新たな立ち上げは、同社のプロジェクト「Helping Electronics Live Longer」の一環であり、リデュース、リユース、リサイクルのための施策です。

同様に、2023年12月、サベスプ社は2024年から28年にかけて97億米ドルを事業に投資する戦略を発表しました。同社が期待する投資の大半は下水道サービスであり、残りは給水範囲の拡大、水損失の抑制、その他の運営業務に費やされます。さらに、プレーヤー各社は、合併、買収、戦略的提携、新規プロジェクトの立ち上げを通じて事業を拡大し、顧客のニーズに応えています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 市場概要

- 市場促進要因

- 世界の環境規制の強化により、コンプライアンスに準拠した有害廃棄物管理・処理ソリューションの需要が増加

- 産業活動の増加と都市化が有害廃棄物排出量を増加させ、廃棄物管理サービスの需要を促進

- 高度なリサイクルや廃棄物エネルギー化プロセスなど、廃棄物治療技術の革新による効率性の向上と環境負荷の軽減

- 市場抑制要因

- 経済的圧力を受けている業界では、コスト効率の高い廃棄物管理とのバランスに苦慮することが多い

- マテリアルハンドリングは人の健康と環境にリスクを与えるため、厳格な安全手順と緊急時対応計画が必要

- 市場機会

- 新興市場における工業化と都市化が有害廃棄物管理サービスの成長を促進

- 廃棄物治療技術の進歩により、効率的で持続可能なソリューションを提供する企業にビジネスチャンスが生まれる

- 戦略的提携により、知識の共有と技術投資が促進される

- バリューチェーン/サプライチェーン分析

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ別

- 固体

- 液体

- 汚泥

- 廃棄物別

- 化学品

- バイオメディカル

- 放射性廃棄物

- その他の廃棄物(腐食性、可燃性など)

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- その他アジア太平洋地域

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- その他中東

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Suez

- Valicor

- Veolia

- Waste Connections

- Waste Management

- Republic Services

- Biffa

- Clean Harbors

- Covanta Holding

- Daiseki

- Hitachi Zosen

- Remondis SE & Co. Kg

- Urbaser

- Biomedical Solutions

- その他の企業

第7章 市場の将来

第8章 付録

- 活動別GDP分布

- 輸入と輸出

The Hazardous Waste Management Market size is estimated at USD 40.22 billion in 2025, and is expected to reach USD 48.33 billion by 2030, at a CAGR of 3.74% during the forecast period (2025-2030).

Key Highlights

- Hazardous waste management involves practices and procedures to handle, control, and dispose of substances that threaten human health or the environment. It includes waste collection, recycling, treatment, transportation, disposal, and monitoring of disposal sites. The primary objective is to mitigate risks and safeguard health and the environment.

- The hazardous waste management market is driven by several factors. Governments worldwide are intensifying their focus on waste disposal due to concerns over pollution and health risks. Consequently, stricter regulations are being enacted to govern waste disposal practices and encourage responsible management.

- Technological advancements have significantly bolstered hazardous waste management. Innovations in waste treatment and disposal have ushered in more efficient and eco-friendly methods. Notable technologies include steam autoclave treatment, chemical treatment, ozone treatment, pyrolysis, and electron beam technology. For instance, Pello is a new technology that has been developed to help businesses reduce their environmental impact and manage their waste collection more efficiently. Pello helps companies achieve these goals in a number of different ways. Firstly, the Pello system monitors the fill level of trash cans and provides real-time information on the dumpsters' contents and location.

- In April 2023, Recycle Track Systems (RTS) acquired RecycleSmart Solutions, solidifying its position as Canada's premier independent provider of advanced waste diversion, organic capture, and recycling management technology. The acquisition encompassed Recycle Smart's cutting-edge Pello waste sensor technology, an integral part of its Internet of Things (IoT) platform.

Hazardous Waste Management Market Trends

Asia-Pacific Expected to Dominate the Market Over the Coming Years

- Rapid industrialization in countries like China, India, and Southeast Asian nations has driven a surge in hazardous waste production, notably in industries such as manufacturing, mining, and electronics. China, for instance, has witnessed a nearly threefold increase in waste output since the 1990s. This rise can be attributed to multiple factors. Over the past few decades, China's urbanization rate has steadily climbed. By 2023, data from the National Bureau of Statistics of China revealed that approximately 66.2% of the population was residing in urban areas.

- China's robust economic growth, evidenced by its 2023 GDP of roughly USD 17.7 trillion, as per the International Monetary Fund (IMF), further bolstered industrial waste production. While the volume of conventional industrial waste, such as tailings and fly ash, has remained stable, hazardous waste production has surged in tandem with industrial progress. Notably, these hazardous by-products necessitate more advanced treatment for safe disposal. A significant milestone was reached in March 2024 when Jereh Group introduced its GreenWell distributed hazardous waste treatment equipment. This innovative solution, tailored to address challenges in centralized hazardous waste disposal, allows for on-site treatment, bypassing the need for intermediary steps.

- By streamlining on-site treatment and eliminating intermediary steps, this state-of-the-art equipment significantly enhances processing efficiency, reduces waste, and facilitates wastewater recycling within the system. Impressively, it has already demonstrated its efficacy, cutting oily waste at well sites by over 20% and achieving an outstanding 95% recovery rate for basic oil. Furthermore, it enables zero-discharge recycling of wastewater within its operational framework.

- Over the past few decades, Asia-Pacific has made notable strides in enhancing its regulatory frameworks for managing hazardous waste. Governments have intensified environmental regulations, compelling industries to adopt more robust waste management practices. For instance, in 2021, the Central Government of India launched the Swachh Bharat Mission Urban 2.0 (SBM-U 2.0), envisioning "Garbage Free Cities." The mission targets all urban local bodies to secure at least a 3-star certification, emphasizing door-to-door collection, source segregation, and scientific processing of municipal solid waste.

- While rapid industrialization in Asia, particularly in China, has led to a notable uptick in hazardous waste generation, advancements in waste treatment technology and stringent regulatory frameworks are heralding a shift toward more efficient and eco-friendly waste management practices.

- The surge in hazardous waste production in rapidly industrializing countries like China and India underscores the critical need for advanced waste management solutions. China's significant economic growth and urbanization have directly contributed to increased hazardous waste, necessitating innovative treatment technologies like the GreenWell equipment. This technology not only improves processing efficiency but also supports environmental sustainability through wastewater recycling. Additionally, the strengthening of regulatory frameworks across the Asia-Pacific indicates a growing commitment to addressing environmental challenges, compelling industries to adopt better waste management practices. These developments suggest a positive trend toward more sustainable industrial growth in the region.

By Disposal Type, Collection Gaining More Traction Over the Coming Years

- Hazardous waste collection involves structured procedures to gather, manage, and transport materials that pose significant risks to human health and the environment. These materials are classified based on inherent traits (flammable, toxic, etc.) or specific designations by regulatory bodies. Accurate identification is crucial for applying proper handling and disposal protocols.

- In July 2024, Sedema, Mexico's Secretariat of the Environment, successfully transported over 5,600 tires from illegal dumps in Xochimilco and Gustavo Madero to a treatment plant. These tires will be repurposed as an alternative fuel in cement production. Partnering with Geocycle Mexico, this move is a cornerstone in Sedema's strategy to combat environmental challenges from improper tire disposal, which often leads to public pollution and heightened wildfire risks. Sedema announced plans to bolster its tire collection via the Reciclatron Program, showcasing Mexico's commitment to holistic waste management and a shift away from fossil fuels and excessive mineral extraction.

- In June 2024, Ottawa's city council greenlit a Solid Waste Master Plan, responding to mounting pressures on the Trail Road Landfill, nearing its 2035 capacity. Concerns arise as replacing it could exceed USD 600 million. The endorsed strategy, spanning three decades, includes nearly 50 initiatives. These aim to divert waste, extending the landfill's life to 2049. Ottawa's approach highlights its dedication to sustainable waste management and long-term environmental stewardship.

- Effective hazardous waste collection demands strict regulatory compliance, proper personnel training, and collaboration among stakeholders, including waste generators, transporters, and disposal facilities. This collaboration ensures safe and compliant hazardous waste management.

- The hazardous waste collection market is evolving, driven by regulatory compliance and innovative waste management. Sedema's initiative in Mexico showcases a proactive stance on repurposing waste, reducing environmental risks, and promoting sustainability. Ottawa's Master Plan mirrors a commitment to waste reduction and resource management, addressing both immediate and future landfill concerns. These cases underscore a broader trend toward integrated waste management, prioritizing sustainability and public health.

Hazardous Waste Management Industry Overview

The hazardous waste management market is moderately fragmented and competitive. Veolia, Biffa, Covanta Holding, Clean Harbors, and Suez Group are among the key players in the hazardous waste management market.

Moreover, key players in the market are taking initiatives such as expanding new facilities to strengthen their market presence. For instance, in May 2022, The Trinidad and Tobago Solid Waste Management Company (SWMCOL) launched collection sites for recycling old mobile phones. The new launch was a part of the company's project, 'Helping Electronics Live Longer,' which is a measure to reduce, reuse, and recycle.

Similarly, in December 2023, Sabesp announced a strategy to invest USD 9.7 billion in its operations over 2024-28. The majority of the company's expected investments will be in sewerage services, while the rest will be spent on expanding water supply coverage, controlling water losses, and other operational tasks. In addition, players are expanding their businesses through mergers, acquisitions, strategic partnerships, and new project launches to meet customer needs.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent Global Environmental Regulations Drive Demand for Compliant Hazardous Waste Management and Disposal Solutions

- 4.2.2 Increased Industrial Activities and Urbanization Driving up Hazardous Waste Production, Fueling Demand for Waste Management Services

- 4.2.3 Innovations in Waste Treatment Technologies, such as Advanced Recycling and Waste-to-Energy Processes, Enhance Efficiency and Reduce Environmental Impact

- 4.3 Market Restraints

- 4.3.1 Industries Under Economic Pressure Often Struggle to Balance Cost-efficient Waste Management

- 4.3.2 Handling Hazardous Materials Risks Human Health and the Environment, Requiring Strict Safety Protocols and Emergency Response Plans

- 4.4 Market Opportunities

- 4.4.1 Industrialization and Urbanization in Emerging Markets are Driving Growth in Hazardous Waste Management Services

- 4.4.2 Advancements in Waste Treatment Technologies Create Opportunities for Companies Offering Efficient and Sustainable Solutions

- 4.4.3 Strategic Collaborations can Enhance Knowledge Sharing and Technology Investments

- 4.5 Value Chain/Supply Chain Analysis

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Solid

- 5.1.2 Liquid

- 5.1.3 Sludge

- 5.2 By Waste

- 5.2.1 Chemicals

- 5.2.2 Biomedical

- 5.2.3 Radioactive

- 5.2.4 Other Waste (Corrosive, Flammable, etc.)

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 United Arab Emirates

- 5.3.4.2 Saudi Arabia

- 5.3.4.3 Rest of Middle East

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Overview (Market Concentration & Major Players)

- 6.2 Company Profiles

- 6.2.1 Suez

- 6.2.2 Valicor

- 6.2.3 Veolia

- 6.2.4 Waste Connections

- 6.2.5 Waste Management

- 6.2.6 Republic Services

- 6.2.7 Biffa

- 6.2.8 Clean Harbors

- 6.2.9 Covanta Holding

- 6.2.10 Daiseki

- 6.2.11 Hitachi Zosen

- 6.2.12 Remondis SE & Co. Kg

- 6.2.13 Urbaser

- 6.2.14 Biomedical Solutions

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX

- 8.1 GDP Distribution by Activity

- 8.2 Imports and Exports