|

市場調査レポート

商品コード

1636187

米国のエンジニアリング・調達・建設管理(EPCM)-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)US Engineering, Procurement, And Construction Management (EPCM) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国のエンジニアリング・調達・建設管理(EPCM)-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

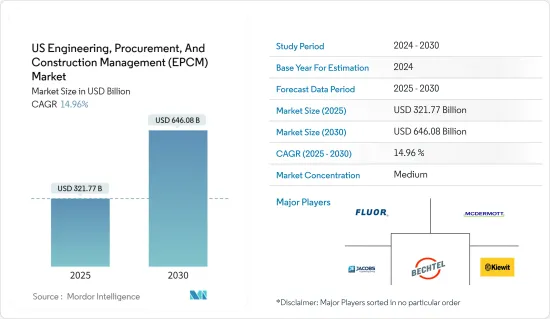

米国のエンジニアリング・調達・建設管理(EPCM)市場規模は2025年に3,217億7,000万米ドルと推定され、2030年には6,460億8,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは14.96%です。

米国のエンジニアリング・調達・建設管理(EPCM)市場は、米国のインフラと産業情勢において極めて重要な役割を果たしています。数十億米ドルの収益と一貫した成長軌道を誇り、主にインフラのアップグレード、再生可能エネルギー事業、産業拡大への多額の投資がその原動力となっています。特筆すべきは、インフラ投資・雇用促進法に代表される政府の取り組みで、交通、公共事業、急成長中のスマートシティ部門に多額の資金が投入されています。さらに、風力、太陽光、エネルギー貯蔵を含む持続可能エネルギーへの国の軸足は、EPC企業のプロジェクト・パイプラインを強化しています。この勢いは、製造工場の近代化が急務であること、医療やデータセンターのインフラに対するニーズが拡大していることで、さらに拍車がかかっています。

有望な展望とは裏腹に、米国EPC市場は成長を阻害しかねない課題に取り組んでいます。規制の複雑さ、労働力不足、資材価格の高騰、インフレ圧力などが顕著な障害となっています。しかし、こうした障害がある一方で、同市場は、特にスマートインフラ、再生可能エネルギー、最先端製造の領域において、さまざまなビジネス機会をもたらしています。Bechtel、Fluor、Jacobs Engineeringといった注目すべき産業参入企業が最前線に立ち、ビルディング・インフォメーション・モデリング(BIM)、IoT、AIといった技術を活用してプロジェクトの効率性と持続可能性を高めています。そのため、米国のEPC市場は、政府の支援、技術の進歩、現代的なインフラに対する意欲の高まりに後押しされ、さらなる拡大が見込まれています。

米国のエンジニアリング・調達・建設管理(EPCM)市場動向

インフラ投資がEPCMセクターを牽引

米国のインフラ投資、特にエンジニアリング・調達・建設管理(EPC)部門への投資は、経済成長と近代化にとって極めて重要です。同国は、人口増加と技術の進歩に対応するため、交通網や公共事業などの重要インフラ強化に多額の資金を投入しています。

2023年、大統領と運輸長官は、バイデン-ハリス政権が新しい国家インフラプロジェクト支援(メガ)裁量助成金プログラムから9つの国家プロジェクトに約12億米ドルを割り当てたことを発表しました。これらのイニシアチブは、経済の活性化、高賃金の雇用創出、サプライチェーンの強化、住民の移動性向上、交通システムの安全性向上を目的としています。

メガ補助金イニシアティブは、バイデン大統領の画期的なインフラ整備法から生まれたもので、規模や複雑さにおいて従来の資金援助プログラムを凌駕するプロジェクトを対象としています。対象となる事業には、高速道路、橋、港湾、公共輸送が含まれます。

2026年までに、このメガ・プログラムは、現在と将来の世代に利益をもたらすことに重点を置き、米国のインフラ刷新に総額50億米ドルを投入することが期待されています。最新の申請では、米国運輸省は2022年の10億米ドルをはるかに上回る総額約300億米ドルの申請を行った。注目すべきプロジェクトは以下の通りです。

ハドソンヤードのコンクリートケース第3工区(ニューヨーク州)に2億9,200万米ドル:この資金により、コンクリートケースの最終セクションが完成し、新しいハドソン・リバー・トンネルの用地が確保され、ゲートウェイプロジェクトの舞台が整う。ハドソン・トンネル構想が実現すれば、通勤時間の改善、北東回廊(NEC)のAmtrakの信頼性向上、米国人口の17%を擁する地域経済の活性化が約束されます。Amtrakは、このプロジェクトにより建設期間中に7万2,000人の雇用が創出されると見込んでおり、職業訓練のための組合との提携に重点を置いています。

ブレント・スペンス橋の改良に2億5,000万米ドル(オハイオ州シンシナティとケンタッキー州コビントン):オハイオ川に架かるこの重要な貨物通路は、年間4,000億米ドルを超える貨物輸送の確認者であり、トラックのボトルネックで悪名高いです。このメガ・グラントは、ブレント・スペンス橋のアップグレードと、既存の橋に隣接する新しい橋の建設を促進するもので、渋滞の緩和と移動時間の信頼性向上を図り、地域経済を強化することを目的としています。

全体として、米国におけるインフラ投資、特にEPC部門における投資は、経済成長と近代化を推進する上で極めて重要です。バイデン-ハリス政権のコミットメントは、国家インフラプロジェクト支援(メガ)裁量助成金プログラムから約12億米ドルが割り当てられたことからも明らかです。ハドソン・リバー・トンネルやブレント・スペンス橋のような注目すべきプロジェクトは、交通網の強化、雇用創出、サプライチェーンの弾力性強化に重点を置く政権の姿勢を浮き彫りにしています。2026年までに50億米ドルを投資するメガ・プログラムにより、国家は、モビリティ、安全性、経済的強靭性の向上を目の当たりにし、現在と将来の世代に恩恵をもたらす態勢が整っています。

需要が急増する電力・公益セクター

2023年、米国の電力・公益事業部門は脱炭素化への取り組みを大幅に進め、太陽光発電とエネルギー貯蔵の導入量を記録しました。この進展は、極めて重要なクリーンエネルギーと気候に関する法律によって後押しされ、2024年まで続きました。このセクターのファンダメンタルズはまちまちであったが、電力数量は、主に暖冬のため、2023年末までに前年比約1.2%減少すると予測されました。サプライチェーンの課題は緩和され始めたが、鉄鋼や変圧器のような主要材料の持続的な不足は操業を混乱させ、コストを押し上げました。

2023年の発電用天然ガスコストが前年比53%減少したことが主因となって、多くの地域で電力卸売価格が下落しました。しかし、すべての電力会社が卸売市場から電力を調達しているわけではなく、燃料費は顧客請求書のコンポーネントに過ぎないため、価格変動との相関関係は直接的でない可能性があります。2023年には、主要な電力・ガス会社が合計で1,710億米ドル近くを送電網の近代化と脱炭素化に費やし、新記録を樹立しました。今後予想される支出や金利上昇と相まって、こうした多額の資本支出は顧客負担の増加につながる可能性があります。

2024年、電力料金は安定的に推移すると予想されるが、売上高は約2%増加すると予測されます。サプライチェーンの混乱は徐々に解消されると予想されます。様々な触媒に支えられたクリーンエネルギーへの取り組みの勢いは、今後も続くと考えられます。米国では、炭素削減目標を前倒しする電力会社が増えており、従来の「2050年までに正味ゼロ」という目標から、2030年までに80%削減することを目指しています。インフレ抑制法(IRA)施行1周年の2023年8月までに、投資家はすでに1,220億米ドル以上をクリーンエネルギー発電に、さらに1,100億米ドルを国内のクリーンエネルギー製造の強化に充当しています。

2023年には、インフラ投資・雇用促進法(IIJA)が、送電網の信頼性向上、バッテリー・サプライチェーン、EVプログラム、エネルギー効率向上のために数十億米ドルを割り当てた。米国エネルギー情報局(EIA)は、実用規模の太陽光発電設備が大幅に急増し、2023年には2倍以上の24ギガワットに達し、2024年にはさらに36ギガワットに達すると予想しました。また、再生可能エネルギーの電力シェアは2023年の22%から2024年には25%近くまで上昇するとの予測もあります。

全体として、米国の電力・公益事業部門は、実質的な法的支援と記録的な投資に支えられ、脱炭素化とクリーンエネルギー導入において大きく前進しました。サプライチェーンの課題や電力数量の落ち込みが予想されるもの、同部門は、野心的な炭素削減目標に向けた勢いを持続させながら、2024年には安定した電力価格と数量の増加に向けて態勢を整えています。

米国のエンジニアリング・調達・建設管理(EPCM)産業概要

米国のEPCM市場は、複数の大手多国籍企業の存在と大規模な合併・買収活動により、中程度の市場集中度を示しています。競合情勢はダイナミックであり、継続的な技術の進歩と政府の施策が市場構造を形成しています。このセグメントで著名な企業には、Fluor Corporation、McDermott International Ltd、Jacobs Engineering Group、Bechtel Corporation、Kiewit Corporationなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- インフラの近代化と開発

- 建設産業における持続可能性重視の高まり

- 市場抑制要因

- 熟練労働力の確保

- 材料費の上昇

- 市場機会

- 風力・太陽エネルギープロジェクトへの投資の増加

- バリューチェーン/サプライチェーン分析

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- PESTLE分析

- 市場における技術革新に関する洞察

第5章 市場セグメンテーション

- サービス別

- エンジニアリング

- 調達

- 建設

- その他サービス

- セクター別

- 住宅産業、インフラ(運輸)、エネルギー・公益事業

- 産業

- インフラ(運輸)

- エネルギー・公益事業

第6章 競合情勢

- Market Concetration Overview

- 企業プロファイル

- Fluor Corporation

- McDermott International Ltd

- Jacobs Engineering Group

- Bechtel Corporation

- Kiewit Corporation

- AECOM

- Black & Veatch

- Burns & McDonnell

- Turner Construction

- The Walsh Group Ltd

第7章 今後の動向

The US Engineering, Procurement, And Construction Management Market size is estimated at USD 321.77 billion in 2025, and is expected to reach USD 646.08 billion by 2030, at a CAGR of 14.96% during the forecast period (2025-2030).

The engineering, procurement, and construction management (EPCM) market in the United States plays a pivotal role in the nation's infrastructure and industrial landscape. It boasts multi-billion dollar revenues and a consistent growth trajectory, primarily fueled by substantial investments in infrastructure upgrades, renewable energy ventures, and industrial expansions. Notably, government initiatives, exemplified by the Infrastructure Investment and Jobs Act, channel significant capital into transportation, utilities, and the burgeoning smart city sector. Furthermore, the nation's pivot toward sustainable energy, encompassing wind, solar, and energy storage, bolsters the project pipeline for EPC firms. This momentum is further fueled by the imperative for modernizing manufacturing plants and the expanding need for healthcare and data center infrastructure.

Despite its promising outlook, the US EPC market grapples with challenges that could impede its growth. Regulatory intricacies, labor scarcities, escalating material prices, and inflationary pressures pose notable hurdles. However, amid these obstacles, the market presents a range of opportunities, especially in the realms of smart infrastructure, renewable energy, and cutting-edge manufacturing. Noteworthy industry players like Bechtel, Fluor, and Jacobs Engineering are at the forefront, harnessing technologies like building information modeling (BIM), IoT, and AI to elevate project efficiency and sustainability. Therefore, the US EPC market is poised for further expansion, buoyed by governmental backing, technological strides, and an escalating appetite for contemporary infrastructure.

US Engineering, Procurement, And Construction Management (EPCM) Market Trends

Investments in Infrastructure are Poised to Propel the EPCM Sector

Infrastructure investment in the United States, especially in the engineering, procurement, and construction (EPC) sector, is pivotal for economic growth and modernization. The country is channeling significant funds into enhancing transportation networks, public utilities, and other crucial infrastructure to keep pace with a growing population and advancing technology.

In 2023, the President and Transportation Secretary unveiled that the Biden-Harris Administration had allocated nearly USD 1.2 billion from the new National Infrastructure Project Assistance (Mega) discretionary grant program to nine national projects. These initiatives aim to bolster the economy, create well-paying jobs, fortify supply chains, enhance resident mobility, and elevate the safety of the transportation systems.

The Mega grant initiative, a product of President Biden's landmark infrastructure legislation, is tailored for projects that outstrip conventional funding programs in scale or complexity. Eligible ventures include highways, bridges, ports, and public transportation.

By 2026, the Mega program is expected to infuse a total of USD 5 billion into revamping the US infrastructure, with a focus on benefiting current and future generations. In the latest application round, the US Department of Transportation fielded requests totaling around USD 30 billion, far surpassing the available USD 1 billion in 2022. Notable projects include:

USD 292 million for Hudson Yards Concrete Casing, Section 3 (New York): This funding will complete the final section of the concrete casing, securing the right-of-way for the new Hudson River Tunnel and setting the stage for the Gateway Project. The Hudson Tunnel initiative, upon fruition, promises improved commute times, enhanced Amtrak reliability on the Northeast Corridor (NEC), and a boost to the regional economy, which houses 17% of the US population. Amtrak anticipates the project will create 72,000 jobs during construction, with a focus on union partnerships for job training.

USD 250 million for Brent Spence Bridge improvements (Cincinnati, OH, and Covington, KY): This vital freight corridor, spanning the Ohio River, witnesses over USD 400 billion in annual freight movement and is notorious for its truck bottlenecks. The Mega grant will facilitate essential upgrades to the Brent Spence Bridge and the construction of a new bridge alongside the existing one, aimed at alleviating congestion and enhancing travel time reliability, thus bolstering the regional economy.

Overall, infrastructure investment in the United States, especially in the EPC sector, is pivotal in driving economic growth and modernization. The Biden-Harris Administration's commitment is evident in allocating nearly USD 1.2 billion from the National Infrastructure Project Assistance (Mega) discretionary grant program. Noteworthy projects like the Hudson River Tunnel and Brent Spence Bridge highlight the administration's focus on bolstering transportation networks, job creation, and supply chain resilience. With the Mega program eyeing a USD 5 billion investment by 2026, the nation is poised to witness enhanced mobility, safety, and economic robustness, benefiting current and future generations.

The Power and Utilities Sector is Experiencing a Surge in Demand

In 2023, the US power and utilities sector significantly advanced its decarbonization efforts, achieving record solar and energy storage installations. This progress, bolstered by pivotal clean energy and climate legislation, continued into 2024. While the sector's fundamentals were a mixed bag, electricity sales were forecasted to dip by approximately 1.2% YoY by the end of 2023, primarily due to a mild winter. Supply chain challenges began to ease, yet persistent shortages of key materials like steel and transformers disrupted operations and drove up costs.

Many regions saw a drop in wholesale electricity prices, largely attributed to a 53% YoY decrease in natural gas costs for power generation in 2023. However, since not all utilities procure electricity from wholesale markets and fuel expenses are just one component of customer bills, the correlation with price movements may not be direct. In 2023, major electric and gas utilities collectively spent nearly USD 171 billion on grid modernization and decarbonization, setting a new record. Coupled with anticipated future spending and rising interest rates, these high capital outlays could translate to increased customer bills.

In 2024, electricity prices are anticipated to hold steady, while sales are projected to increase by around 2%. Supply chain disruptions are expected to resolve gradually. The momentum for clean energy initiatives, supported by various catalysts, is likely to persist. A growing number of US electric firms have accelerated their carbon reduction targets, aiming for an 80% cut by 2030, shifting from the previous "net zero by 2050" goal. By August 2023, on the first anniversary of the Inflation Reduction Act (IRA), investors had already earmarked over USD 122 billion for clean energy generation and an additional USD 110 billion for bolstering domestic clean energy manufacturing.

In 2023, the Infrastructure Investment and Jobs Act (IIJA) allocated billions for enhancing grid reliability, battery supply chains, EV programs, and energy efficiency. The US Energy Information Administration (EIA) expected a significant surge in utility-scale solar installations of more than doubling to 24 gigawatts in 2023, followed by an additional 36 GW in 2024. Its projections also indicated a rise in the renewable electricity share from 22% in 2023 to nearly 25% in 2024.

Overall, the US power and utilities sector made significant strides in decarbonization and clean energy adoption, supported by substantial legislative backing and record investments. Despite facing supply chain challenges and a forecasted dip in electricity sales, the sector is poised for steady electricity prices and increased sales in 2024, with continued momentum toward ambitious carbon reduction goals.

US Engineering, Procurement, And Construction Management (EPCM) Industry Overview

The US EPCM market exhibits moderate market concentration, driven by the presence of several large multinational firms and significant merger and acquisition activities. The competitive landscape is dynamic, with ongoing technological advancements and government policies shaping the market structure. Prominent entities in this sector include Fluor Corporation, McDermott International Ltd, Jacobs Engineering Group, Bechtel Corporation, and Kiewit Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infrastructure Modernization and Development

- 4.2.2 Increase in Emphasis on Sustainability in the Construction Industry

- 4.3 Market Restraints

- 4.3.1 Skilled Workforce Availability

- 4.3.2 Rising Material Costs

- 4.4 Market Opportunities

- 4.4.1 Increasing Investments in Wind and Solar Energy Projects

- 4.5 Value Chain / Supply Chain Analysis

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 PESTLE Analysis

- 4.8 Insights on Technology Innovation in the Market

5 MARKET SEGMENTATION

- 5.1 By Service

- 5.1.1 Engineering

- 5.1.2 Procurement

- 5.1.3 Construction

- 5.1.4 Other Services

- 5.2 By Sector

- 5.2.1 Residential Industrial, Infrastructure (Transportation), and Energy and Utilities

- 5.2.2 Industrial

- 5.2.3 Infrastructure (Transportation)

- 5.2.4 Energy and Utilities

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concetration Overview

- 6.2 Company Profiles

- 6.2.1 Fluor Corporation

- 6.2.2 McDermott International Ltd

- 6.2.3 Jacobs Engineering Group

- 6.2.4 Bechtel Corporation

- 6.2.5 Kiewit Corporation

- 6.2.6 AECOM

- 6.2.7 Black & Veatch

- 6.2.8 Burns & McDonnell

- 6.2.9 Turner Construction

- 6.2.10 The Walsh Group Ltd