|

市場調査レポート

商品コード

1636180

電気自動車用リチウムイオン電池セパレータの世界市場:市場シェア分析、産業動向、成長予測(2025年~2030年)Global Lithium-ion Battery Separator For Electric Vehicle Application - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 電気自動車用リチウムイオン電池セパレータの世界市場:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

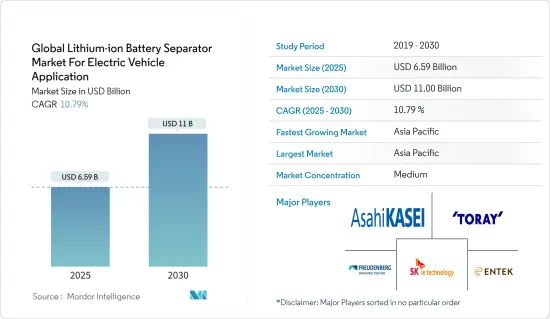

電気自動車用リチウムイオン電池セパレータの世界市場は、2025年の65億9,000万米ドルから2030年には110億米ドルに成長し、予測期間(2025~2030年)のCAGRは10.79%になると予測されます。

主要ハイライト

- 中期的には、電気自動車販売台数の増加やリチウムイオン電池のコスト低下といった要因が、予測期間中の電気自動車向けリチウムイオン電池セパレータ世界市場の最も大きな促進要因の1つになると予想されます。

- その一方で、電池セパレータの製造には複雑なサプライチェーン上の制約があり、予測期間中の電気自動車用途向けリチウムイオン電池セパレータ世界市場の脅威となっています。

- 強化された電池セパレータ材料の開発には継続的な努力が払われています。この要因は、将来的に電気自動車用リチウムイオン電池セパレータの世界市場にいくつかの機会を生み出すと予想されます。

- アジア太平洋は大きな成長が見込まれており、予測期間中に最も高いCAGRで推移する可能性が高いです。これは、同地域に大規模な電池と関連機器・材料の製造産業が存在するためです。

リチウムイオン電池セパレータの世界動向

ポリエチレンが成長を牽引

- ポリエチレン(PE)は、電気自動車用途のリチウムイオン電池セパレータの主要材料として台頭してきました。その主要理由は、優れた化学的安定性、機械的強度、薄い多孔質膜の製造能力です。電気自動車用電池におけるポリエチレン製セパレータの世界市場は、電気自動車産業の急速な拡大と、高性能で安全かつコスト効率の高いエネルギー貯蔵ソリューションに対する需要の高まりにより、近年大幅な成長を遂げています。

- ポリエチレンセパレータ、特に高密度ポリエチレン(HDPE)と超高分子量ポリエチレン(UHMWPE)セパレータは、電気自動車用電池の過酷な環境での使用に適した特性を兼ね備えています。これらの材料は、電池システムの熱暴走を防止するために極めて重要な熱安定性を提供する一方で、リチウムイオン電池で使用される電解液や電極材料に対して優れた耐薬品性を発揮します。

- 世界の電気自動車需要の拡大に伴い、電気自動車用途の電池需要は急増し、その結果、電池セパレータ材料におけるポリエチレンのニーズが高まることになります。このような需要の増加は、効率的で耐久性の高い電池部品を必要とする電気自動車やハイブリッド車の生産台数が増加していることが背景にあります。さらに、電池技術の進歩が、高品質のポリエチレン製セパレータの需要をさらに押し上げています。

- 国際エネルギー機関(IEA)によると、電気自動車の販売台数が近年大幅に急増しているのは、国民の間でサステイナブル輸送ソリューションを採用する意識が高まっていることと、地域政府が脱炭素化目標を達成するためにさまざまな財政的インセンティブを提供しているためです。2023~2022年にかけて、電気自動車の販売台数は30.13%増加し、2019~2023年にかけての年間平均成長率は100%を超えています。

- 最近の動向では、メーカーは最新の製造技術を採用し、新しい材料組成を開発し、他の材料との新しい材料化学反応を開発しています。こうした進歩は、ポリエチレンセパレータの機能特性を向上させただけでなく、製造コストの削減にも貢献しており、生産コストを管理しながら電池性能を最適化したい電気自動車メーカーにとって、ポリエチレンセパレータはますます魅力的な選択肢となっています。

- 例えば2024年1月、Institute of Modern Physics(IMP)と先進エネルギー科学技術広東ラボの科学者は、リチウムイオン電池用の高温耐性ポリエチレンテレフタレート(PET)セパレータを開発しました。リチウムイオン電池の重要部品であるセパレータは、電池の安全性を確保する上で重要な役割を果たします。正極と負極を絶縁してショートを防ぐだけでなく、リチウムイオンの輸送を促進します。

- 従って、上記の点から、ポリエチレン製セパレータ材料は予測期間中に成長が見込まれます。

アジア太平洋が市場を独占する

- アジア太平洋は、電気自動車用リチウムイオン電池セパレータの世界市場で圧倒的な強さを見せており、その影響力は地理的な境界をはるかに超えて広がっています。この優位性は、同地域の強固な製造能力、政府による多大な支援、広範な研究開発イニシアティブ、電気自動車のサプライチェーン全体にわたる主要参入企業の存在など、さまざまな要因に根ざしています。

- 中国、日本、韓国、最近ではインドといった国々が、エレクトロニクス、自動車製造、先端材料といった既存の強みを活かして、電池セパレータ製造のための強力なエコシステムを構築し、急速に発展するこの産業の最前線に位置しています。同地域がこの市場で急成長しているのは、その製造能力の高さによるものだけでなく、電気自動車が世界の交通の将来において極めて重要な役割を果たすことを認識した戦略的先見性によるものでもあります。

- 例えば、国際エネルギー機関(IEA)は近年、電気自動車の販売台数が大幅に伸びていることを目の当たりにしています。2022~2022年にかけて、電気自動車販売台数の伸びは24%以上増加し、2019~2023年にかけては、CAGRが100%に近づいた。これは、電気自動車の牽引力が高まっていることを意味し、その結果、リチウムイオン電池セパレータ市場にとって有利な市場環境が整備されました。

- この認識により、生産能力の拡大、技術革新、電池とセパレータ技術に特化した熟練労働力の開発に多額の投資が行われるようになりました。このようなユニークな要因の組み合わせにより、アジア太平洋は電気自動車用リチウムイオン電池セパレータ生産における現在のリーダーとしての地位を確立しました。アジア太平洋は、他の地域がこの重要な技術セグメントでの能力開発を目指すなかでも、将来にわたってこのリーダー的地位を維持できるような位置にあります。

- 例えば、Asahi Kasei Corporationは2023年10月、ハイポアリチウムイオン電池(LIB)セパレータの生産能力を増強するため、新たな設備投資を行う予定です。同社は、米国、日本、韓国にある現在のLIBセパレータ工場に新たなコーティングラインを設置する計画です。操業は2026年度上期から順次開始する予定。この戦略的な動きにより、旭化成は約170万台の電気自動車の電池ニーズに対応できるようになります。

- Asahi Kasei Corporationの今回の投資は、電池技術を発展させ、増大する電気自動車の需要に応えるというコミットメントを強調するものです。Asahi Kasei Corporationは、生産能力を強化することで、世界のリチウムイオン市場での地位を強化することを目指しています。新しいコーティングラインには、高品質で効率的な生産プロセスを確保するための最新技術が導入されます。この拡大は、サステイナブルエネルギーソリューションへの移行を支援するという旭化成の長期戦略に沿ったものです。

- 従って、前述の通り、予測期間中はアジア太平洋が市場を独占すると予想されます。

世界のリチウムイオン電池セパレータ産業概要

世界の電気自動車用リチウムイオン電池セパレータ市場は、半分断構造になっています。この市場の主要企業(順不同)には、Asahi Kasei Corporation、Toray Battery Separator Film、Freudenberg Performance Materials、SK ie Technology Corporation Ltd、Entek Internationalなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車販売の成長

- リチウムイオン電池の価格低下

- 抑制要因

- サプライチェーンの制約

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- 材料

- ポリエチレン

- ポリプロピレン

- 複合材料

- その他

- 2029年までの市場規模・需要予測(地域別)

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- ノルディック

- ロシア

- トルコ

- その他の欧州

- アジア太平洋

- 中国

- インド

- オーストラリア

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- ナイジェリア

- エジプト

- カタール

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略とSWOT分析

- 企業プロファイル

- Asahi Kasei Corporation

- Toray Battery Separator Film Co. Ltd

- Freudenberg Performance Materials

- SK ie Technology Corporation Ltd

- Entek International

- Sumitomo Chemical Co. Ltd

- Ube Maxell Co. Ltd

- W-Scope Corporation

- Daramic

- Amer SIL

- その他の著名な企業一覧

- 市場ランキング/シェア(%)分析

第7章 市場機会と今後の動向

- 強化型セパレータ材料の開発

The Global Lithium-ion Battery Separator Market For Electric Vehicle Application Industry is expected to grow from USD 6.59 billion in 2025 to USD 11.00 billion by 2030, at a CAGR of 10.79% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as rising growth in electric vehicle sales and declining cost of lithium-ion batteries are expected to be among the most significant drivers for the global lithium-ion battery separator market for electric vehicle applications during the forecast period.

- On the other hand, there are complex supply chain constraints for manufacturing battery separators that pose a threat to the global lithium-ion battery separator market for electric vehicle applications during the forecast period.

- Nevertheless, continued efforts are being made to develop enhanced battery separator materials. This factor is expected to create several opportunities for the global lithium-ion battery separator market for electric vehicle applications in the future.

- The Asia-Pacific region is expected to witness significant growth and is likely to register the highest CAGR during the forecast period. This is due to the presence of a significant battery and associated equipment and materials manufacturing industry in the region.

Global Lithium-ion Battery Separator Market Trends

Polyethylene to Witness Growth

- Polyethylene (PE) has emerged as a dominant material for lithium-ion battery separators in electric vehicle applications. This is mainly due to its excellent chemical stability, mechanical strength, and ability to be manufactured into thin, porous membranes. The global market for Polyethylene separators in electric vehicle batteries has seen substantial growth in recent years, driven by the rapid expansion of the electric vehicle industry and increasing demand for high-performance, safe, and cost-effective energy storage solutions.

- Polyethylene separators, particularly those made from high-density polyethylene (HDPE) and ultra-high molecular weight polyethylene (UHMWPE), offer a compelling combination of properties that make them well-suited for use in the demanding environment of electric vehicle batteries. These materials provide good thermal stability, which is crucial for preventing thermal runaway in battery systems, while also offering excellent chemical resistance to the electrolytes and electrode materials used in lithium-ion cells.

- As global electric vehicle demand escalates, the demand for batteries in electric vehicle applications is set to surge, consequently boosting the need for polyethylene in battery separator materials. This increase is driven by the growing production of electric and hybrid vehicles, which require efficient and durable battery components. Additionally, advancements in battery technology are further propelling the demand for high-quality polyethylene separators.

- According to the International Energy Agency (IEA), electric vehicle sales have witnessed a significant surge in recent years owing to the growing awareness of adopting sustainable transportation solutions amongst the public and various financial incentives offered by regional governments to meet their decarbonization targets. Between 2023 and 2022, electric vehicle sales witnessed an uptick of 30.13%, whereas the annual average growth rate between 2019 and 2023 was over 100%, signifying the growing traction for electric vehicles.

- In recent years, manufacturers have adopted the latest manufacturing techniques, developed new material compositions, and developed new material chemistries with other materials. These advancements have not only improved the functional properties of Polyethylene separators but have also contributed to reducing manufacturing costs, making them an increasingly attractive option for electric vehicle manufacturers looking to optimize battery performance while managing production expenses.

- For instance, in January 2024, Scientists at the Institute of Modern Physics (IMP) of the Chinese Academy of Sciences (CAS) and the Advanced Energy Science and Technology Guangdong Laboratory have developed high-temperature-resistant polyethylene terephthalate (PET) separators for lithium-ion batteries. The separator, a pivotal component of lithium-ion batteries, is instrumental in safeguarding battery safety. It not only insulates the cathode and anode to prevent short-circuiting but also facilitates the transport of lithium ions.

- Therefore, as per the points mentioned above, the polyethylene separator material is expected to witness growth during the forecast period.

Asia Pacific to Dominate the Market

- The Asia-Pacific region has emerged as the dominant force in the global lithium-ion battery separator market for electric vehicle applications, with its influence extending far beyond its geographical boundaries. This dominance is rooted in a variety of factors, including the region's robust manufacturing capabilities, significant government support, extensive research and development initiatives, and the presence of major players across the entire electric vehicle supply chain.

- Countries like China, Japan, South Korea, and, to a growing extent, India have positioned themselves at the forefront of this rapidly evolving industry, leveraging their existing strengths in electronics, automotive manufacturing, and advanced materials to create a formidable ecosystem for battery separator production. The region's rapid growth in this market is not only a result of its manufacturing prowess but also stems from its strategic foresight in recognizing the pivotal role that electric vehicles will play in the future of global transportation.

- For instance, the International Energy Agency has witnessed significant growth in electric vehicle sales in recent years. Between 2022 and 2022, the growth in electric vehicle sales increased by more than 24%, whereas between 2019 and 2023, the annual average growth rate was close to 100%. This signifies the growing traction for electric vehicles, which in turn developed favorable market conditions for the lithium-ion battery separator market.

- This recognition has led to substantial investments in capacity expansion, technological innovation, and the development of a highly skilled workforce specializing in battery and separator technologies. This unique combination of factors has established the Asia-Pacific as the current leader in lithium-ion battery separator production for electric vehicles. Still, it has also positioned itself to maintain this leadership well into the future, even as other regions seek to develop their capabilities in this critical technology sector.

- For instance, in October 2023, Asahi Kasei is set to invest in new equipment to bolster its production capacity for Hipore lithium-ion battery (LIB) separators. The company plans to set up fresh coating lines at its current LIB separator plants in the United States, Japan, and South Korea. Operations are slated to commence in stages, starting in the first half of fiscal year 2026. This strategic move will enable Asahi Kasei to cater to the battery needs of approximately 1.7 million electric vehicles.

- Asahi Kasei's investment underscores its commitment to advancing battery technology and meeting the growing demand for electric vehicles. By enhancing its production capabilities, the company aims to strengthen its position in the global lithium-ion market. The new coating lines will incorporate state-of-the-art technology to ensure high-quality and efficient production processes. This expansion aligns with Asahi Kasei's long-term strategy to support the transition to sustainable energy solutions.

- Therefore, as mentioned above, the Asia-Pacific region is expected to dominate the market during the forecast period.

Global Lithium-ion Battery Separator Industry Overview

The global lithium-ion battery separator market for electric vehicle applications is semi-fragmented. Some of the key players in this market (in no particular order) are Asahi Kasei Corporation, Toray Battery Separator Film Co. Ltd, Freudenberg Performance Materials, SK ie Technology Corporation Ltd, and Entek International.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Electric Vehicle Sales

- 4.5.1.2 Decreasing Lithium-ion Battery Price

- 4.5.2 Restraints

- 4.5.2.1 Supply Chain Constraints

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Material

- 5.1.1 Polyethylene

- 5.1.2 Polypropylene

- 5.1.3 Composite

- 5.1.4 Other Materials

- 5.2 Geography [Market Size and Demand Forecast till 2029 (for regions only)]

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 France

- 5.2.2.3 United Kingdom

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 NORDIC

- 5.2.2.7 Russia

- 5.2.2.8 Turkey

- 5.2.2.9 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Australia

- 5.2.3.4 Japan

- 5.2.3.5 South Korea

- 5.2.3.6 Malaysia

- 5.2.3.7 Thailand

- 5.2.3.8 Indonesia

- 5.2.3.9 Vietnam

- 5.2.3.10 Rest of Asia-Pacific

- 5.2.4 Middle East and Africa

- 5.2.4.1 Saudi Arabia

- 5.2.4.2 United Arab Emirates

- 5.2.4.3 Nigeria

- 5.2.4.4 Egypt

- 5.2.4.5 Qatar

- 5.2.4.6 South Africa

- 5.2.4.7 Rest of Middle East and Africa

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Argentina

- 5.2.5.3 Colombia

- 5.2.5.4 Rest of South America

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted & SWOT Analysis for Leading Players

- 6.3 Company Profiles

- 6.3.1 Asahi Kasei Corporation

- 6.3.2 Toray Battery Separator Film Co. Ltd

- 6.3.3 Freudenberg Performance Materials

- 6.3.4 SK ie Technology Corporation Ltd

- 6.3.5 Entek International

- 6.3.6 Sumitomo Chemical Co. Ltd

- 6.3.7 Ube Maxell Co. Ltd

- 6.3.8 W-Scope Corporation

- 6.3.9 Daramic

- 6.3.10 Amer SIL

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Enhanced Separator Materials