ドイツの速達便:市場シェア分析、産業動向、成長予測(2025年~2030年)

Germany Express Delivery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636139

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

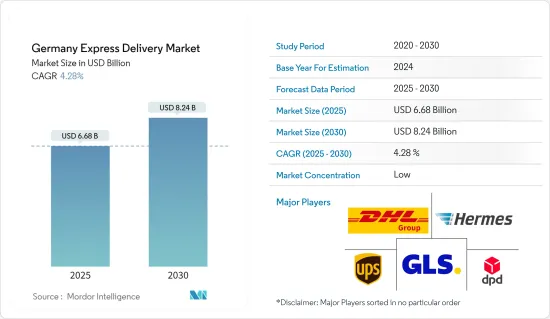

ドイツの速達便市場規模は2025年に66億8,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは4.28%で、2030年には82億4,000万米ドルに達すると予測されます。

主要ハイライト

- ドイツの速達便市場は、主に国際貿易活動の急増と即日配達需要の高まりによって活性化しています。

- 速達便産業の成長を促進する主要要因の1つは、特に新興諸国における国境を越えた/国際的な商業ルートの拡大であり、これにより国際貿易やB2C輸送の受け入れが増加しています。さらに、さまざまなeコマース・ポータルを通じたオンラインショッピングに対する消費者の嗜好の高まりが、市場の成長を後押ししています。国内外の国境を越えて商品を流通させるため、eコマースストアは宅配便業者と連携しています。

- 2019年、オンラインストアは24億米ドルの輸出純売上高を達成し、4億1,800万米ドルに過ぎなかった市場の輸出GMVを大きく上回りました。2023年までに、輸出市場のGMVは11億米ドルに上昇しました。オンラインストアの売上高にはまだ及ばないもの、この157%の成長率は印象的です。

- クラウドソーシングを利用した流通モデルによるデジタル技術の活用など、技術的な向上も市場の好展望に寄与しています。急速な都市化、消費支出能力の上昇、製造業の著しい成長といったその他の要因も、予測期間中に市場をさらに押し上げると予想されます。小売業者の出荷業務全体の効率を向上させるために、自動化された荷物や貨物の出荷ソリューションが提供されています。小売業者は近い将来、通関書類の電子送信などの事務処理を配送パートナーに委託し、迅速な通関手続きを享受することで、関連事務処理にかかる時間と費用を削減できるようになると考えられます。

- さらに、各国政府や貿易圏の間で地域協定や貿易協定の交渉が進むにつれ、中小企業にとって新市場への参入がより魅力的になっています。若い都市人口の増加は、国境を越えたeコマースの急成長に起因しています。

- 即日配達の需要は、オンラインで購入する顧客にとってより一般的な配送オプションになるにつれて高まっています。技術革新は、当日配送サービス産業において支持を集めています。当日配送サービスセグメントの主要な競合企業は、需要の高まりに対応するため、サービスの画期的な技術開発に注力しています。

ドイツの速達便市場動向

市場で大幅な成長を遂げる国際セグメント

- ドイツの国際市場では、輸出ではオンラインストアが市場を上回っています。逆に輸入では、市場からのGMVが店舗からの純売上高を上回っています。ドイツの主要なeコマース輸出パートナーは、もっぱら欧州です。一方、輸入パートナーはスイス、米国、トルコ、インドなど多岐にわたります。ファッションはドイツのeコマースにおける主要な輸入カテゴリーとして圧倒的である一方、輸出はホビー&レジャーが先導し、エレクトロニクスがそれを引き離しています。

- 2019年、オンラインストアは24億米ドルの輸出純売上高を誇り、わずか4億1,800万米ドルの市場輸出GMVを上回りました。2023年になると、輸出市場のGMVは11億米ドルに急増しました。オンラインストアの売上高にはまだ及ばないもの、この157%という成長率は注目に値します。

- 市場は今や輸入を圧倒しており、ドイツでは海外のオンラインストアではなく、国際的な市場がより高いGMVを生み出していることを示しています。これは、海外のオンラインストアが市場を上回っていた2019年からの大きな変化を示しています。

- 2019年、海外オンラインストアは4億1,400万米ドルの輸入純売上高を記録しました。これはその年の輸出売上高のほんの一部ではあったが、それでも市場の輸入によるGMVを上回りました。しかし、2023年までには、国際市場は輸入GMVで10億米ドルの大台を超えただけでなく、オンラインストアの輸入売上高も上回るようになります。ドイツのオンラインストアは、近隣諸国での強固な顧客関係やブランドの信頼に支えられ、輸出に秀でています。

- しかし、輸入のセグメントでは市場が台頭しています。ドイツの消費者が国境を越えて買い物をする機会が増えるにつれ、市場の競合価格と強力な物流サポートに引き寄せられるようになったのです。ドイツで急成長している市場の動向は、世界の市場支配へのシフトを反映しており、国際的なeコマースにおける市場の極めて重要な役割を浮き彫りにしています。

- 2023年には、Ottoが5億7,300万米ドルの越境輸出GMVで首位に立った。しかし、トップの座にありながら、Ottoの輸出GMVは、Amazon.deの輸出売上高(16億米ドル)の3分の1にすぎないです。Ottoの主要取扱商品はファッションで、エレクトロニクスがそれに続きます。国境を越えた取引はオーストリアとオランダに限られており、2023年の総GMVの4%と3.8%に寄与しています。

- 輸入面では、Galaxusがトップランナーに浮上し、ドイツで3億2,700万米ドルの輸入GMVを獲得しました。この数字は、大手オンラインストアのAmazon.comの輸入売上高1億1,800万米ドルの2倍以上です。主にスイスの多国籍市場であるGalaxusは、2023年にはドイツが総GMVの20%近くを占める第2位の市場になると見ています。国際的な売上が急増するにつれて、同市場における速達便の需要も増加します。

2023年、ドイツのeコマースは個人消費の抑制により低迷に直面

- 2023年、ドイツのeコマースは、主に個人消費の減少によって大幅な落ち込みを経験しました。商品総売上高は11.8%急落し、2022年の904億ユーロ(946億9,000万米ドル)を下回る797億ユーロ(834億8,000万米ドル)に落ち着いた。小売総額(食品を除くが薬局の売上を含む)に占めるeコマースのシェアは10.2%に落ち込み、2022年の11.8%から低下しました。

- 旅行予約やコンサートチケット販売などのデジタルサービスは回復を見せたもの、勢いは弱まった。これらのサービスは12.7%増の127億ユーロ(133億米ドル)となり、前年の39.9%増の112億5,000万ユーロ(117億8,000万米ドル)とは対照的でした。その結果、eコマース部門(商品とサービス)の合計売上高は、2020年以来初めて1,000億ユーロ(1,047億4,000万米ドル)の大台を下回りました。2023年のオンライン取引による総売上高は、電話、ファックス、その他の手段によるものを含め、936億ユーロ(980億4,000万米ドル)に達しました。

- 小売企業は、2023年を大きな転換の年として記憶すると考えられます。消費者直接販売(D2C)小売企業は、2022年に11.1%の減収となったもの、より安定した長期的な成長軌道を確立しており、パンデミック前の2019年の値を62%上回る数字を誇っています。市場とオンライン小売業はそれぞれ8.5%と14.7%の減少となったが、どちらもCOVID以前の値を19.0%と7.0%上回っています。マルチチャネル取引は18.1%と最も急な収益減少に直面したが、これは実店舗での顧客の復活が指摘されていることと一致します。

- 2023年には、オンラインショッピングの活動はさらに衰えました。定期的にオンラインショッピングを利用する顧客の割合は34.3%に落ち込み、2019年の平均40%から著しく低下し、4年間の平均を下回りました。eコマースの衰退が続く中、速達便サービスへの需要も微妙に落ち込んでいます。

ドイツの速達便産業概要

ドイツの速達便市場は、多くの市内、地域、世界の参入企業によってセグメント化されています。主要参入企業には、DHL Group、Hermes Europe GmbH、Dynamic Parcel Distribution(DPD)、General Logistics Systems B.V.(GLS)、United Parcel Services(UPS)などがあります。

顧客により良いサービスを提供するため、各社は最先端の技術進歩をサプライチェーンに組み込んでいます。2024年6月、世界有数の国際エクスプレスサービスプロバイダーであるDHL Expressは、AIを活用したプラットフォーム「My Global Trade Services」(MyGTS)をアップグレードし、新たに「トレードレーン比較」機能を導入しました。この追加機能により、企業は規模に関係なく、輸出国と輸入国または地域間の現行の貿易レーン規制や要件にアクセスし、参照することができます。その結果、市場拡大を目指す企業は、十分な情報に基づいた意思決定、効率性の向上、競合の確保にこのツールを活用することができます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 市場概要

- 市場促進要因

- 即日配達需要の急増が市場を牽引

- 可処分所得の増加が市場を牽引

- 市場抑制要因

- 従来の配送方法と比較して高コストであることが市場を阻害している

- 市場に影響を与える規制上の制約

- 市場機会

- 技術的進歩が市場を牽引

- バリューチェーン/サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 政府の規制と取り組み

- 産業の技術動向

- eコマース産業に関する洞察(国内eコマースと越境eコマース)

- 地政学とパンデミックが市場に与える影響

第5章 市場セグメンテーション

- 事業別

- B2B

- B2C

- 目的地別

- 国内

- 海外

- エンドユーザー別

- サービス(BFSI(銀行、金融サービス、保険))

- 卸売・小売(eコマース)

- 製造業、建設業、公益事業

- 第一次産業(農業、その他天然資源)

第6章 競合情勢

- 企業プロファイル

- DHL Group

- Hermes Europe Gmbh

- Dynamic Parcel Distribution(DPD)

- General Logistics Systems B.V.(GLS)

- United Parcel Services(UPS)

- FedEx Express

- DB Schenker

- Go Express

- Atlantic International Express

- Nippon Express*

- その他の企業

第7章 市場の将来

第8章 付録

- マクロ経済指標(GDP分布、活動別、運輸・倉庫部門の経済への寄与度)

- 対外貿易統計-輸出と輸入(製品別)

- 主要輸出先と輸入原産国に関する洞察

目次

The Germany Express Delivery Market size is estimated at USD 6.68 billion in 2025, and is expected to reach USD 8.24 billion by 2030, at a CAGR of 4.28% during the forecast period (2025-2030).

Key Highlights

- German express delivery market is primarily fueled by surging international trade activities and a growing demand for same-day delivery.

- One of the primary drivers driving the growth of the express delivery industry is the expansion of cross-border/international commercial routes, particularly in developing countries, which has increased the acceptance of international trade and B2C shipping. Furthermore, the growing consumer preference for shopping online via various e-commerce portals is boosting market growth. To distribute their products across domestic and international borders, e-commerce stores collaborate with courier service providers.

- In 2019, online stores achieved export net sales of USD 2.4 billion, far surpassing the marketplace export GMV, which was only USD 418 million. By 2023, the export marketplace GMV climbed to USD 1.1 billion. Although it still lags behind online store net sales, this 157% growth rate is impressive.

- Technological improvements, such as the use of digital technology with crowd-sourced distribution models, are also contributing to the market's favourable outlook. Other factors, such as rapid urbanization, rising consumer expenditure capacities, and significant growth in the manufacturing sector, are expected to propel the market even higher during the forecast period. There are automated package and freight shipping solutions available to improve the efficiency of retail merchants' overall shipping operation. Retailers will soon be able to delegate paperwork to shipping partners, such as electronically transmitting customs documentation, and enjoy a fast customs clearing procedure, reducing the time and expense associated with the associated paperwork.

- Furthermore, as more regional and trade agreements are negotiated between governments and trading blocs, it has become more appealing for SMEs to enter new markets. The increase of a young, urban population is attributed to the rapid growth of cross-border e-commerce.

- The demand for same-day delivery is growing as it becomes a more popular shipping option for customers purchasing online. Technological innovations are gaining traction in the industry for same-day delivery services. The major competitors in the same-day delivery services sector are focusing on creating technology breakthroughs in their services to meet the growing demand.

Germany Express Delivery Market Trends

International segment experiencing substantial growth in the market

- In Germany's international landscape, online stores outpace marketplaces in exports. Conversely, for imports, the GMV from marketplaces surpasses the net sales from stores. Germany's primary eCommerce export partners are exclusively European. In contrast, its import partners span a broader spectrum, including Switzerland, the U.S., Turkey, and India. Fashion dominates as the leading imported category in German eCommerce, while exports are spearheaded by hobby & leisure, trailed by electronics.

- In 2019, online stores boasted export net sales of USD 2.4 billion, overshadowing the marketplace export GMV, which stood at a mere USD 418 million. Fast forward to 2023, and the export marketplace GMV surged to USD 1.1 billion. While still trailing behind online store net sales, this growth rate of 157% is noteworthy.

- Marketplaces now dominate imports, indicating that international marketplaces, rather than foreign online stores, are generating a higher GMV in Germany. This marks a significant shift from 2019 when foreign online stores outperformed marketplaces.

- In 2019, foreign online stores recorded import net sales of USD 414 million. While this was a mere fraction of that year's export sales, it still eclipsed the GMV from marketplace imports. By 2023, however, international marketplaces not only crossed the USD 1 billion mark in import GMV but also outpaced the import sales of online stores.German online stores excel in exports, bolstered by robust customer relationships and brand trust in neighboring nations.

- In the realm of imports, however, marketplaces are gaining ground. As German consumers increasingly shop beyond their borders, they are drawn to marketplaces for their competitive pricing and robust logistical support. This burgeoning marketplace trend in Germany mirrors the global shift towards marketplace dominance, underscoring their pivotal role in international eCommerce.

- In 2023, Otto led the pack with a cross-border export GMV of USD 573 million. Yet, despite its top position, Otto's export GMV is only about one-third of Amazon.de's leading export net sales, which stand at a hefty USD 1.6 billion. Otto's primary offerings are fashion, trailed by electronics, and its cross-border dealings are limited to Austria and the Netherlands, contributing 4% and 3.8% to its total GMV in 2023.

- On the import front, Galaxus emerged as the frontrunner, amassing an import GMV of USD 327 million in Germany. This figure more than doubles the import net sales of the leading online store, Amazon.com, which stands at USD 118 million. Galaxus, primarily a Swiss multinational marketplace, sees Germany as its second-largest market, accounting for nearly 20% of its total GMV in 2023. As international sales surge, the demand for express delivery in the market rises in tandem.

German e-commerce grappled with a downturn in 2023, as consumer spending curtailed

- In 2023, German e-commerce experienced a significant downturn, primarily driven by reduced consumer spending. Gross goods turnover plummeted by 11.8%, settling at EUR 79.7 billion (USD 83.48 billion), down from EUR 90.4 billion (USD 94.69 billion) in 2022 The e-commerce share of total retail (excluding food but including pharmacy revenues) dipped to 10.2%, a drop from 11.8% in 2022.

- While digital services like vacation bookings and concert ticket sales saw a recovery, the momentum weakened. These services grew by 12.7% to EUR 12.7 billion (USD 13.30 billion), a stark contrast to the previous year's 39.9% surge to EUR 11.25 billion (USD 11.78 billion). Consequently, the combined turnover for the e-commerce sector (goods and services) fell below the EUR 100 billion (USD 104.74 billion) mark for the first time since 2020. Total revenues from online trade in 2023, including those generated via telephone, fax, or other means, reached EUR 93.6 billion (USD 98.04 billion).

- Retailers will remember 2023 as a year of significant shifts. Direct-to-consumer (D2C) retailers, despite an 11.1% revenue drop in 2022, have established a more stable long-term growth trajectory, boasting figures 62% above their pre-pandemic 2019 values. Marketplaces and online retailers saw declines of 8.5% and 14.7% respectively, yet both stand 19.0% and 7.0% above their pre-COVID values. Multichannel trading faced the steepest revenue drop at 18.1%, coinciding with a noted resurgence of customers at physical points of sale.

- Online shopping activity waned further in 2023. The proportion of regularly active online customers making purchases in the dipped to 34.3%, a notable decline from the 40% average in 2019 and below the four-year average. As the e-commerce landscape continues to wane, demand for express delivery services has seen a subtle dip.

Germany Express Delivery Industry Overview

The German express delivery market is fragmented with a lot of local, regional, and global players. Major players include DHL Group, Hermes Europe Gmbh, Dynamic Parcel Distribution (DPD), General Logistics Systems B.V. (GLS), United Parcel Services (UPS), etc.

To better serve their customers, companies are integrating cutting-edge technological advancements into their supply chains. In June 2024, DHL Express, the world's foremost international express service provider, upgraded its AI-driven platform, "My Global Trade Services" (MyGTS), introducing a new "trade lane comparison" feature. This addition allows businesses, regardless of size, to access and reference current trade lane regulations and requirements between exporting and importing nations or territories. Consequently, firms eyeing market expansion can utilize this tool for informed decision-making, enhancing efficiency and securing a competitive edge.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in demand for same day delivery driving the market

- 4.2.2 Increased disposable income driving the market

- 4.3 Market Restraints

- 4.3.1 High cost compared to traditional delivery methods hindering the market

- 4.3.2 Regulatory constraints affecting the market

- 4.4 Market Opportunities

- 4.4.1 Technological advancements driving the market

- 4.5 Value Chain / Supply Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Government Regulations and Initiatives

- 4.8 Technological Trends in Industry

- 4.9 Insights on the E-commerce Industry (Domestic and Cross-border E-commerce)

- 4.10 Impact of Geopolitics and Pandemic on the Market

5 MARKET SEGMENTATION

- 5.1 By Business

- 5.1.1 B2B (Business-to-Business)

- 5.1.2 B2C (Business-to-Consumer)

- 5.2 By Destination

- 5.2.1 Domestic

- 5.2.2 International

- 5.3 By End User

- 5.3.1 Services (BFSI (Banking, Financial Services and Insurance))

- 5.3.2 Wholesale and Retail Trade (E-commerce)

- 5.3.3 Manufacturing, Construction, and Utilities

- 5.3.4 Primary Industries (Agriculture, and Other Natural Resources)

6 COMPETITIVE LANDSCAPE

- 6.1 Overview (Market Concentration and Major Players)

- 6.2 Company Profiles

- 6.2.1 DHL Group

- 6.2.2 Hermes Europe Gmbh

- 6.2.3 Dynamic Parcel Distribution (DPD)

- 6.2.4 General Logistics Systems B.V. (GLS)

- 6.2.5 United Parcel Services (UPS)

- 6.2.6 FedEx Express

- 6.2.7 DB Schenker

- 6.2.8 Go Express

- 6.2.9 Atlantic International Express

- 6.2.10 Nippon Express *

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX

- 8.1 Macroeconomic Indicators (GDP Distribution, by Activity, Contribution of Transport and Storage Sector to economy)

- 8.2 External Trade Statistics - Exports and Imports, by Product

- 8.3 Insights into Key Export Destinations and Import Origin Countries

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日