産業用電気部品-市場シェア分析、産業動向・統計、成長予測(2025~2030年)

Industrial Electrical Component - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636126

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

産業用電気部品市場規模は2025年に594億9,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは4%を超え、2030年には723億8,000万米ドルに達すると予測されます。

産業用電気部品市場は予測期間中にCAGR 4%を記録すると予測されます。

主要ハイライト

- 長期的には、産業からの高い電力需要、大規模な生産施設を設置するための民間投資、経済活動の活発化が産業用電気部品市場を牽引すると予想されます。

- その一方で、部品の複雑なメンテナンスプロセス、環境に影響を与える有毒廃棄物の出現、産業用電気部品の高い交換コストが、市場の成長を妨げる可能性が高いです。

- 仕様の向上、産業の自動化、最適な安全性を実現するための継続的な研究開発は、産業用電気部品市場に成長機会をもたらすと考えられます。アジア太平洋は、各国の産業部門からの需要が増加しているため、市場を独占すると予想されます。

産業用電気部品市場の動向

産業からの高いエネルギー需要が市場を牽引する見込み

- IEAによると、2022年の世界の最終エネルギー総使用量に占める産業部門の割合は35%で、エネルギー消費量は過去10年間から5%増加しているが、これは主に鉄鋼、精錬、アルミニウム、基礎化学品、セメント、紙・パルプ、飲食品など、エネルギー集約型産業サブセクターの生産拡大が後押ししています。

- 世界最大の製造拠点のひとつである中国は、2023年4月の製造業生産が前年比6.50%増となりました。同国の総電力消費量の約40.66%は、ハイテクや機器製造などの産業活動によるものです。IEAによれば、世界の電力消費に占める中国の割合は、工業化の進展により、2025年までに3分の1に達すると予想されています。これは、今後数年間における産業用電気部品市場の成長を示しています。

- さらに、エネルギー情報局(EIA)によれば、2022年の米国における産業部門への電力小売数量は1兆100億kWh、25.8%でした。また、製造業エネルギー消費調査(MECS)によると、米国における電力購入総量は、建設・鉱業部門よりも製造部門の方が78%多かった。これは、米国の産業部門で電気部品が広く利用されていることを表しており、市場のさらなる成長を促進する可能性があります。

- 同様に、EUの産業部門における2021年の最終エネルギー消費量は25.6%でした。同地域では、暖房、冷房、照明といったプロセスと非プロセスの目的により高いエネルギーを消費しています。2021年に欧州連合が使用したエネルギー製品のシェアは、電気が33.2%、天然ガスが32.7%、再生可能エネルギーが9.7%でした。従って、今後の電気部品市場が堅調であることを浮き彫りにしています。

- したがって、上記の要因から、産業用電気部品市場は、予測期間中にエネルギー多消費国による高エネルギー消費の増加により成長すると予想されます。

アジア太平洋が市場を独占する

- インドは世界でも重要な鉄鋼生産・輸出国です。2022会計年度の最初の10ヶ月間の粗鋼生産量は1億320万トンで前年同期比4.2%増でした。同期間の鉄鋼輸出量は533万トンであったが、前年度を下回りました。

- 工業投資の増加は、より多くの工業作業所を建設し、ひいては電気部品の需要を生み出すと予想されます。例えば、2023年、Arcelor Mittalは、Nippon Steelとともに50億米ドルを投じてインドでの鉄鋼生産能力を拡大すると宣言しました。

- 主に工業用消費者から届く電力需要を満たすための発電量の増加が、アジア太平洋の工業用電気部品市場を牽引する可能性が高いです。World Energy Data Statistical Reviewによると、2022年の同地域の発電量は1万4,546.4TWhで、前年比4%増でした。発電量はさらに増加し、電気部品の販売が増加すると予想されます。

- さらに、多くの産業が再生可能エネルギー技術を採用することで、実用規模の発電や屋上太陽光発電プロジェクトを加速させています。政府の施策とクリーンエネルギー発電により、多くの企業が日々のエネルギー需要を満たすため、大規模な太陽エネルギー発電システムの設置を好んでいます。このことは、アジア太平洋における産業用電気部品市場の成長に資する環境を作り出しており、再生可能エネルギー発電の増加とともに、さらに成長することが期待されています。

- したがって、鉄鋼のような商品の生産と輸出の増加、再生可能エネルギー発電の増加、新しい装置製造ユニット、発電量の増加は、この地域の産業用電気部品市場の成長に大きく貢献すると考えられます。

産業用電気部品産業概要

産業用電気部品市場は細分化されています。この市場の主要企業には、SiemensAG、ABB Ltd.、Toshiba Corporation、General Electric、Schneider Electricが含まれる(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義と調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2028年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 産業からの高い電力需要

- 経済活動の活発化

- 抑制要因

- 部品の複雑なメンテナンスプロセスと環境に影響を与える有害廃棄物の出現

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ

- ケーブル

- ワイヤ

- 配電ユニット

- 変圧器

- 開閉装置

- 販売チャネル

- OEM

- アフターマーケット

- 地域

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

- その他の欧州

- アジア太平洋

- インド

- 中国

- 日本

- その他のアジア太平洋

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- 北米

第6章 競争情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Siemens AG

- Toshiba Corporation

- General Electric Company

- Schneider Electric SE

- Eaton Corporation plc

- Mitsubishi Electric Corporation

- OMRON Automotive Electronics Co. Ltd.

- Emerson Electric Co.

- ABB Ltd.

第7章 市場機会と今後の動向

- 仕様の強化、産業の自動化、最適な安全性を実現する研究開発

目次

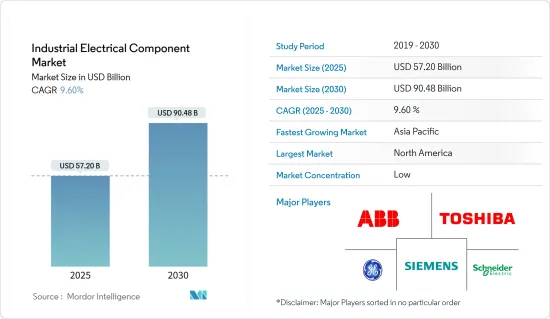

The Industrial Electrical Component Market size is estimated at USD 59.49 billion in 2025, and is expected to reach USD 72.38 billion by 2030, at a CAGR of greater than 4% during the forecast period (2025-2030).

The Industrial Electrical Components market is expected to mark a CAGR of 4% during the forecast period.

Key Highlights

- Over the long term, high electricity demand from industries, private investments to set up extensive production facilities, and enhancement in economic activities are expected to drive the industrial electrical component market.

- On the other hand, the complex maintenance process of components, the emergence of toxic wastes that affect the environment, and the high replacement costs of industrial electrical components will likely obstruct the market's growth.

- Nevertheless, continuous research and development to enhance specifications, industry automation, and optimum safety would likely create growth opportunities for the Industrial Electrical Component market. The Asia-Pacific region is anticipated to dominate the market due to the increasing demand from the industrial sector across the countries.

Industrial Electrical Component Market Trends

High Energy Demand from Industries is Expected to Drive the Market

- As per IEA, there was a 35% share of the industrial sector in total global final energy usage in 2022, a five percent increase in energy consumption from the previous decade is mainly propelled by ramping of production in energy-intensive industry sub-sectors such as iron & steel, refining, aluminum, basic chemicals, cement, paper & pulp, food & beverage, etc.

- China, one of the largest manufacturing hubs worldwide, witnessed an increase in manufacturing production of 6.50% in April 2023 compared to the previous year. About 40.66% of the total electricity consumption in the country came from industrial activities like high technology and equipment manufacturing, etc. As per IEA, China's share in global electricity consumption is touted to reach one-third by 2025, owing to a rise in industrialization. This indicates a growth in the industrial electrical component market in the next few years.

- Further, as per the Energy Information Administration (EIA), the retail sale of electricity to the industrial sector in the United States in 2022 was 1.01 trillion kWh or 25.8%. Also, per the Manufacturing Energy Consumption Survey (MECS), the total electricity purchases in the United States was 78% more in the manufacturing sector than in the construction and mining sectors. This represents the widespread utilization of electrical components in the United States' industrial sector, which might propel further market growth.

- Similarly, the final energy consumption in the European Union's industrial sector in 2021 was 25.6%. The process and non-process purposes such as space heating, cooling, and lighting draw higher energy in the region. Electricity, natural gas, and renewables accounted for 33.2%, 32.7%, and 9.7% of the share of energy products used by the European Union in 2021, which is expected to rise as the industrial output progresses. Hence, it highlights a robust market for the electrical components market in the future.

- Therefore, based on the abovementioned factors, the industrial electrical component market is expected to grow due to the rise in high energy consumption by energy-intensive countries during the forecast period.

Asia-Pacific to Dominate the Market

- India is a significant steel producer and exporter in the world. The crude steel production during the first ten months of the financial year 2022 was 103.2 million tonnes, a 4.2% increase from the previous year for the same period. Steel exports were 5.33 million tonnes in the same duration but were deemed lower than the previous year.

- An increase in industrial investments is expected to construct more industrial working stations, which, in turn, is expected to create demand for electrical components. For instance, in 2023, Arcelor Mittal declared that it would expand its steel production capacities in India with Nippon Steel with an investment of USD 5 billion, which would likely propel the requirement of electrical components by the novel steel industry in the upcoming years.

- The rise in electricity generation to fulfill electricity demand arriving majorly from industrial consumers is likely to drive the industrial electrical component market in the Asia-Pacific region. As per the Statistical Review of World Energy Data, in 2022, the electricity generation in the region was 14546.4 TWh, an increase of 4% from the previous year. The generation is expected to grow more, increasing the sale of electrical components.

- Further, many industries have accelerated utility-scale electricity generation and rooftop solar projects by adopting renewable energy technologies. Due to government policies and clean energy generation, many enterprises prefer installing large-scale solar energy generation systems to meet daily energy requirements. This has created a conducive environment for the growth of the industrial electrical component market in the Asia-Pacific region, which is expected to grow more with the rise in renewable energy generation.

- Hence, the increase in production & export of commodities such as steel, the rise of renewable energy generation, new equipment manufacturing units, and the increase in electricity generation would significantly help in the growth of the Industrial Electrical Component Market in the region.

Industrial Electrical Component Industry Overview

The Industrial Electrical Component Market is fragmented. Some of the key players in this market include (in no particular order) Siemens AG, ABB Ltd., Toshiba, General Electric, and Schneider Electric.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition and Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 High Electricity Demand from Industries

- 4.5.1.2 Enhancement in Economic Activities

- 4.5.2 Restraints

- 4.5.2.1 The Complex Maintenance Process of Components And the Emergence of Toxic Wastes that Affect the Environment

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products/Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Cables

- 5.1.2 Wires

- 5.1.3 Power Distribution units

- 5.1.4 Transformers

- 5.1.5 Switchgears

- 5.2 Sales Channels

- 5.2.1 OEM

- 5.2.2 Aftermarket

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Rest of Asia Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle East & Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Siemens AG

- 6.3.2 Toshiba Corporation

- 6.3.3 General Electric Company

- 6.3.4 Schneider Electric SE

- 6.3.5 Eaton Corporation plc

- 6.3.6 Mitsubishi Electric Corporation

- 6.3.7 OMRON Automotive Electronics Co. Ltd.

- 6.3.8 Emerson Electric Co.

- 6.3.9 ABB Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Research and Development to Enhance Specifications, Industry Automation, and Optimum Safety

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日