|

|

市場調査レポート

商品コード

1630373

受動光ネットワーク(PON)機器- 市場シェア分析、産業動向、成長予測(2025年~2030年)Passive Optical Network (PON) Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 受動光ネットワーク(PON)機器- 市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

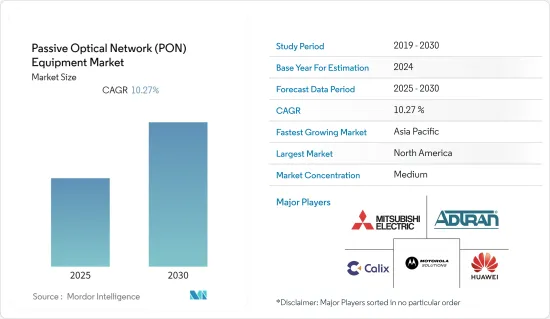

受動光ネットワーク(PON)機器市場は予測期間中にCAGR 10.27%を記録する見込み

主要ハイライト

- さらに、政府は、IoTインフラのスムーズな流れを可能にするために、光ファイバリッチなネットワークでスマートシティプログラムなどのイニシアチブを取っています。光ファイバネットワークは、水、電気、廃水、下水管理、セキュリティ、通信などの公益事業を推進する技術を可能にします。国連によると、2050年までに世界人口の68%以上が都市部に住むと推定されており、世界的にスマートシティプロジェクトが活発化すると考えられます。

- データトラフィックが指数関数的に増加し続ける中、より大容量のネットワークに対する需要が高まっています。受動光ネットワーク(PON)は、長距離にわたって広帯域を提供できるため、この問題に対する有効な解決策となります。帯域幅に対するニーズの高まりが、受動光ネットワーク市場の成長を促す主要要因となっています。消費者は、ビデオストリーミングやその他の帯域幅集約型アプリの普及に伴い、より高速で信頼性の高いネットワークを求めています。PONは、アクティブ・コンポーネントや高価な光ファイバーを使用することなく、かなりの距離にわたってギガビット速度を提供できるため、このような需要に対応するのに適しています。

- COVID-19の流行により、世界各国は予防措置を実施しました。学校は休校となり、地域社会は自宅待機を求められたが、多くの組織では、従業員が自宅で仕事ができるようにする方法を模索していました。電気通信会社は、超高速、超高信頼性、将来性のあるブロードバンドネットワークを提供するため、フルファイバーインフラの構築に積極的に取り組みました。

- 例えば、世界5Gコンベンションで発表されたデータによると、中国の月間平均モバイルユーザーのオンライントラフィックは、5Gに牽引され、過去3年間で7.8GBから14.9GBに増加しました。これにより、リモートワーク、オンライン教育、デジタルライフ、科学研究、COVID-19パンデミック時の疫病予防と制御が容易になりました。これらの要因が予測期間中の市場成長率に大きく寄与しています。

受動光ネットワーク(PON)市場動向

GPON機器が大きく成長する見込み

- 拡大モバイルブロードバンド(eMBB)は、5G NRと4G LTEの遅延改善により、より広いデータ帯域幅を記載しています。eMBBは、モバイルブロードバンドサービスを顧客に直接提供することで、多くの事業者を5Gの新たな使用事例へと導いた。そのため、スペクトル効率や電力が改善され、先進国や発展途上国でスマートフォンのデータ利用が増加していることから、デジタルサービスのための十分な容量を補完しています。

- 最近、テスト、計測、アシュアランスソリューション、先進精密光ソリューションプロバイダのVIAVI Solutions Inc.は、最大10GbEまでのネットワークテスト、ターンアップ、パフォーマンスモニタリング用の小型フォームファクタープラガブル(SFP+)ギガビットイーサネットトランシーバ、Fusion JMEP 10を発表しました。VIAVI NITROライフサイクル・マネジメントプラットフォームの一部であるFusion JMEP 10は、5G xHaul、ビジネスイーサネットサービス、ケーブル向けDAA(Distributed Access Architecture)、ファイバー・アクセス・ネットワーク向けGPON/XGSPON(Gigabit Passive Optical Networks)などの用途で主流となる10GbEのイーサネット帯域幅の出現に対応しています。

- 5Gとファイバーの互換性は、互恵的なパートナーシップをもたらします。家庭へのファイバー接続が困難、高価、時間がかかりすぎる地域では、5G固定無線アクセスがFTTH展開のギャップを埋め、カバレッジを拡大することができます。顧客はセルラーネットワークからWi-Fiに移行し、5GトラフィックをWi-FiとFTTHにオフロードします。これにより、RAN容量と価格の効率的な管理が容易になり、ミッションクリティカルな用途のために5G容量を解放し、家庭での顧客体験を向上させることができます。モバイル機器のユーザーは、5Gによる大幅な高速化と世界のカバレッジを期待しており、そのためには高性能なモバイルトランスポート・ネットワークが必要です。さらに、そのトランスポートを提供するために、すでに存在する受動光ネットワーク(PON)技術ベースのFTTHネットワークが使用されます。

- 世界中でGPONの展開が加速していることから、通信事業者もファイバー展開の次のステップに向けて積極的に動いています。ギガバイト時代は、今後5年間で急速に光アクセスネットワークに到来します。10G PON受動光ネットワーク技術は、その広いカバレッジと広帯域幅が特徴です。高速光アクセス・ネットワークを敷設する際、1つのシステムで30~40世帯にギガバイト・アクセスを提供できるため、世界中の事業者はこの技術を好んでいます。

アジア太平洋が急成長

- 最近、高速インターネットと5Gネットワークへの注目が高まっています。同地域を牽引しているのは、中国、日本、台湾、インド、オーストラリアなどの新興国です。中国には5Gのための確立されたエコシステムがあり、予測期間中にさらに成長すると予想されます。しかし、5G技術は現在のモバイルブロードバンドとのホットスポット技術として機能することが期待されており、成長は緩やかなものになると予想されています。

- 中国は、10G PON技術に代表される新たなギガビット超広帯域ステージに向かって前進しており、光ネットワークの基本的優位性という点で世界をリードしています。主要な通信プロバイダーは、ギガビット光ネットワークの簡潔な開発計画を効果的に打ち出しています。2021年には全国300以上の都市でギガビット・ブロードバンド・アクセス・ネットワークが整備され、8,000万世帯以上にサービスを提供しています。270万人以上の全国ギガビットインターネットアクセス利用者がほとんどの省通信プロバイダーからギガビット商用包装の提供を受けました。新規ユーザー数はわずか5ヶ月で前年の総数を上回った。

- Beijing Mobileは市内に数百のダブルギガビット・ブティック・コミュニティを建設するほか、F5Gの建設を急ぐ。広州電信とHuaweiが発表した初のFTTR白書は、全光住宅ネットワーク技術によってギガビット・ブロードバンドのフルハウスカバレッジを保証します。デジタル経済の強固な基盤を強化するため、杭州移動は「ダブル5G」デジタル都市白書を発表しました。中国のギガビット・ブロードバンドは、多くのデバイスや端末を接続し、家庭、企業、ビジネス、工業製造などのマルチシナリオ用途を実現し、消費者に信頼性の高い高速帯域幅アクセス容量を提供するために、そのカバレッジを拡大し続けると考えられます。

- 中国の通信会社は5Gに594億米ドル以上を投資し、推定1兆2,500億米ドルの経済効果を生み出しています。これは、新しいネットワークインフラが経済成長に大きく貢献していることを示しています。科学技術省副大臣のXiang Libin氏によると、5Gの商業利用は正のフィードバックループに入り、3年以上の開発期間を経て、産業向けの5G用途はゼロから1に増えたと指摘しました。これらの要因が予測期間中の市場成長率に寄与していると分析しています。

受動光ネットワーク(PON)産業概要

受動光ネットワーク機器市場は、少数の企業が市場に存在するため、適度に統合されています。また、これらの企業は顧客に幅広い技術を提供するために大規模な投資を行っています。さらに、これらの企業は市場シェアを拡大するために、戦略的パートナーシップ、買収、製品開拓に継続的に投資しています。各社の現在の進展の一部を以下に示します。

- 2022年5月-オーストリアのウィーンで開催されたFTTH Conference 2022で、モバイルインターネット向けの通信、企業、消費者向け技術ソリューションの重要な世界サプライヤーであるZTE Corporation(0763. HK/000063.SZ)は、50ギガビット対応受動光ネットワーキング(50G PON)とWi-Fi 7技術の両方を提供する産業初の光ネットワークユニット(ONU)のプロトタイプを発表したと宣言しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- 安全で信頼性の高いネットワーク運用への需要

- 従来のネットワークと比較して環境に優しい代替品

- 低い総所有コストと高い投資収益率

- 市場抑制要因

- オペレータ・インターフェースにおけるコンポーネント・コストの高さ

第6章 市場セグメンテーション

- 構造別

- イーサネット受動光ネットワーク(EPON)機器

- ギガビット受動光ネットワーク(GPON)機器

- コンポーネント別

- 波長分割マルチプレクサ/デマルチプレクサ

- 光フィルタ

- 光パワースプリッター

- 光ケーブル

- 光回線終端装置(OLT)

- 光ネットワーク端末(ONT)

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- ADTRAN, Inc.

- Calix, Inc.

- Huawei Technologies Co., Ltd.

- Mitsubishi Electric Corporation

- Motorola Solutions, Inc.

- Nokia Corporation

- Telefonaktiebolaget LM Ericsson

- Tellabs, Inc.

- Verizon Communications, Inc.

- ZTE Corporation

第8章 投資分析

第9章 市場機会と今後の動向

目次

Product Code: 70276

The Passive Optical Network Equipment Market is expected to register a CAGR of 10.27% during the forecast period.

Key Highlights

- Additionally, governments are taking initiatives like smart city programs with fiber optic-rich networks to enable the smooth flow of IoT infrastructure. Fiber optic network allows the technology to drive utilities like water, electricity, wastewater, sewerage management, security, and communication. According to the UN, over 68% of the global population is estimated to live in urban areas by 2050, which will fuel more smart city projects globally.

- The demand for networks with greater capacity is increasing as data traffic keeps growing exponentially. Because they can deliver high bandwidths across great distances, passive optical networks (PONs) present a viable solution to this issue. The rising need for bandwidth is the primary factor driving the passive optical network market growth. Consumers demand faster and more dependable networks as video streaming and other bandwidth-intensive apps proliferate. Due to their ability to deliver gigabit speeds over considerable distances without the use of active components or pricey optical fiber, PONs are uniquely suited to meet this demand.

- Due to the COVID-19 outbreak, countries worldwide implemented preventive measures. While schools were closed and communities were asked to stay at home, many organizations were finding ways to enable employees to work from their homes. Telecom companies actively made efforts to build full-fiber infrastructure to deliver an ultrafast, ultra-reliable, and futureproof broadband network.

- For instance, the average monthly mobile user in China's online traffic increased from 7.8 GB to 14.9 GB over the past three years, driven by 5G, according to data released at the global 5g convention. It facilitated remote work, online education, digital life, scientific research, and epidemic prevention and control during the COVID-19 pandemic. These factors significantly contribute to the market growth rate during the forecast period.

Passive Optical Network (PON) Market Trends

GPON Equipments is Expected to Grow Significantly

- Enhanced mobile broadband (eMBB) provides greater data bandwidth due to latency improvements on 5G NR and 4G LTE. It led most operators towards new use cases for 5G by delivering mobile broadband services directly to customers. It, thus, complements ample capacity for digital services, owing to better spectral efficiency, power, and increasing smartphone data usage in developed & developing countries.

- Recently, VIAVI Solutions Inc., a test, measurement, assurance solutions, and advanced precision optical solutions provider, announced Fusion JMEP 10, a small form-factor pluggable (SFP+) Gigabit Ethernet transceiver for network test, turn-up, and performance monitoring up to 10 GbE. The Fusion JMEP 10, which is part of the VIAVI NITRO lifecycle management platform, addresses10 GbE emergence as the dominant Ethernet bandwidth for applications such as 5G xHaul, Business Ethernet Services, Distributed Access Architecture (DAA) for Cable and Gigabit Passive Optical Networks (GPON/XGSPON) for Fiber Access Networks.

- The compatibility of 5G and fiber results in a reciprocal partnership. In areas where connecting fiber to the home is challenging, expensive, or takes too long, 5G fixed wireless access can fill in the gaps in FTTH deployments and expand coverage. Customers leave the cellular network for Wi-Fi, offloading 5G traffic to Wi-Fi and FTTH. It facilitates managing RAN capacity and prices effectively, freeing up 5G capacity for mission-critical applications and improving the customer experience at home. Users of mobile devices anticipate substantially faster speeds and global coverage from 5G, which requires a high-performance mobile transport network. Further, to offer that transport, a passive optical network (PON) technology-based FTTH networks already in existence are used.

- With the accelerating rollout of GPON worldwide, telecom operators are also actively moving toward the next step in fiber rollouts. The Gigabyte era will rapidly enter optical access networks during the next five years. The 10G PON passive optical network technology is distinguished by its broad coverage and high bandwidth. When installing high-speed optical access networks, operators around the world favor this technology since it can give Gigabyte access to 30-40 households on a single system.

Asia-Pacific Region to Witness the Fastest Growth

- Recently, there is an increased emphasis on high-speed internet and 5G network. The major driving countries in the region for the same are emerging countries, including China, Japan, Taiwan, India, and Australia. China includes an established ecosystem for 5G and is expected to grow further in the forecast period. However, the 5G technology is expected to serve as a hotspot technology with the current mobile broadband; the growth is expected to be gradual.

- China is advancing towards a new Gigabit ultra-wide stage, represented by 10G PON technology, and leading the global in terms of optical networks' fundamental advantages. Primary telecom providers effectively put up concise development plans for a gigabit optical network. Over 300 cities nationwide had a gigabit broadband access network in 2021, serving more than 80 million households. More than 2.7 million National Gigabit internet access consumers have received gigabit commercial packages from most provincial telecommunications providers. The number of new users surpassed the total number from the previous year in just five months.

- In addition to building hundreds of double Gigabyte boutique communities throughout the city, Beijing Mobile will hasten the construction of F5G. The first FTTR White Paper, published by Guangzhou Telecom and Huawei, ensures Gigabit broadband full house coverage through an all-optical residential network technology. To strengthen the firm foundation of the digital economy, Hangzhou Mobile published the "Double 5G" Digital City White Paper. China's Gigabit Broadband will continue to broaden its coverage to connect many devices and terminals, achieve multi-scenario applications such as home, enterprise, business, and industrial manufacturing, and give consumers reliable, high-speed bandwidth access capacity.

- Chinese telecom companies have invested more than USD 59.4 billion in 5G, generating more than USD 59.4 billion in 5G, generating an estimated USD 1.25 trillion in economic output. It shows the significant contribution new network infrastructure makes to economic growth. The commercial use of 5G entered a positive feedback loop, according to Xiang Libin, vice-minister of science and technology, and noted that after more than three years of development, industry-oriented 5G applications have increased from zero to one. These factors are analyzed to contribute to the market growth rate during the forecast period.

Passive Optical Network (PON) Industry Overview

The market for passive optical network equipment is moderately consolidated due to the presence of a few companies in the market. Also, these companies are investing extensively in offering customers a wide range of technologies. Moreover, these companies continuously invest in strategic partnerships, acquisitions, and product development to gain market share. Some of the current advancements by the companies are listed below.

- May 2022 - At the FTTH Conference 2022 in Vienna, Austria, ZTE Corporation (0763. HK / 000063.SZ), a significant global supplier of telecoms, enterprise, and consumer technology solutions for the mobile internet, declared that it had unveiled the prototype of the first Optical Network Unit (ONU) in the industry to offer both 50-Gigabit-Capable Passive Optical Networking (50G PON) and Wi-Fi 7 technologies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment on the Impact of COVID-19 on the market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Demand for secure and reliable network operation

- 5.1.2 Eco-friendly substitute as compared to traditional networks

- 5.1.3 Low total cost of ownership and high return on investment

- 5.2 Market Restraints

- 5.2.1 High component cost at operator interface

6 MARKET SEGMENTATION

- 6.1 By Structure

- 6.1.1 Ethernet Passive Optical Network (EPON) Equipment

- 6.1.2 Gigabit Passive Optical Network (GPON) Equipment

- 6.2 By component

- 6.2.1 Wavelength Division Multiplexer/De-Multiplexer

- 6.2.2 Optical filters

- 6.2.3 Optical power splitters

- 6.2.4 Optical cables

- 6.2.5 Optical Line Terminal (OLT)

- 6.2.6 Optical Network Terminal (ONT)

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ADTRAN, Inc.

- 7.1.2 Calix, Inc.

- 7.1.3 Huawei Technologies Co., Ltd.

- 7.1.4 Mitsubishi Electric Corporation

- 7.1.5 Motorola Solutions, Inc.

- 7.1.6 Nokia Corporation

- 7.1.7 Telefonaktiebolaget LM Ericsson

- 7.1.8 Tellabs, Inc.

- 7.1.9 Verizon Communications, Inc.

- 7.1.10 ZTE Corporation