パーソナルロボット:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

Personal Robots - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1630347

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

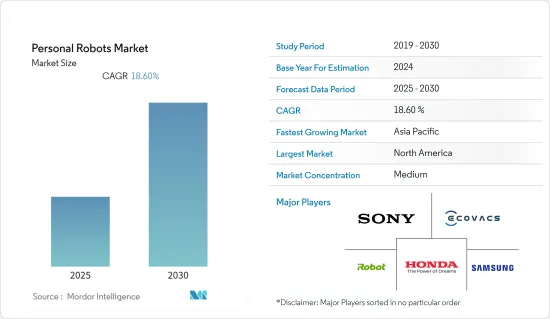

パーソナルロボット市場は予測期間中にCAGR 18.6%を記録する見込みです。

主なハイライト

- 日本や中国のようなアジア太平洋地域の高齢化社会が医療技術分野の成長を牽引しており、その結果、同地域でパーソナル支援ロボットの巨大市場が形成されています。日本統計局によると、日本の65歳以上人口は2021年の3,639万人から2040年には3,921万人に増加すると予測されています。このことは、企業がこの地域の高齢者向け製品に投資することを後押ししています。すでに導入されているそのようなロボットのひとつに、アルツハイマー病などの患者を支援するために設計されたパロ(アザラシの赤ちゃん)があります。

- 認知、インタラクション、操作など、さまざまな分野における技術革新が、パーソナルロボットをより魅力的なものにしています。技術やその他の部品プロバイダーは、ロボットのエコシステムを前進させるのに役立っています。

- 機械学習、コンピューター・ビジョン、自然言語処理、ジェスチャー制御などの人工知能(AI)技術は、家庭や病院でのパーソナルロボットの導入方法を変革しつつあります。パーソナルロボットがよりインテリジェントになれば、周囲の環境を理解し、静的・動的な物体を避け、感情を理解し、コミュニケーションをとることができるようになり、家庭のような混雑した混雑空間で動き回ることができるようになります。

- さらに、マシンビジョンカメラの開発が進む中、企業はAI技術を搭載したこれらの2Dおよび3Dマシンビジョンカメラを使用して、階段のような床の端を効果的にマッピングし、ごみ箱やケーブル、ドアの敷居、敷物のような障害物を認識することで、次世代ロボットへの道を開くと期待されています。

- しかし、パーソナルロボット技術の標準化が進んでいないこと、これらのロボットの操作に伴う技術的な複雑さ、様々な使用事例におけるこれらのシステムの統合の複雑さなどが、パーソナルロボット市場の成長を阻む大きな課題となっています。

- コロナウイルスの大流行は、製造業や技術産業に大混乱をもたらしました。ロボット分野のいくつかの世界的・地域的企業は、深刻な部品・原材料不足を目の当たりにし、それが彼らの製品に直接的な影響を及ぼしました。ほとんどの国で全国的な封鎖が行われたため、世界のサプライ・チェーン・ネットワークが混乱し、製品の売上が減少しました。

- さらに、ロボット技術への関心が高まっているため、ABBやロックウェル・オートメーションなどの企業は、COVID-19の大流行中に株価が上昇しました。2020年には、ForwardXRoboticsが最近、北米市場進出のために1,500万米ドルの資金調達を発表しました。一方、Brain Corpは、数週間前から、特に閉鎖命令を受けている企業の間で、同社の床清掃ロボットに対する需要が増加しています。

- このような動向は、調査対象市場の成長にマイナスの影響を及ぼしているが、特にパンデミックの発生以来、先端技術に対する意識がより多くの人々の間で高まっており、調査対象市場の成長に対する長期的な影響はプラスに働くと予想されます。

パーソナルロボット市場の動向

家事用パーソナルロボットが市場の主要シェアを占める見込み

- ロボットコンパニオン/アシスタント/ヒューマノイド、掃除機がけ、床掃除、芝刈り、プール掃除、窓拭きなどは、パーソナルロボットの家庭用セグメントで人気が高まっているロボットの主な種類です。国際ロボット連盟(IFR)とLoup Venturesが提供したデータによると、ロボット掃除機は2025年までに約2,210万台が出荷され、約49億8,000万米ドルの売上が見込まれています。

- 家庭用ロボットの中でも、自動掃除機とモッパーは各社が最も商品化・開発した製品です。各社は、家庭の狭い場所にも届くよう、よりコンパクトで一体化した掃除機やモップ掛けロボットの開発に継続的に投資しています。各社は、音声認識や床構造をマッピングするレーザーベースの技術などの先進技術を統合しています。例えば、2022年2月、世界有数のハイテク企業であるMidea Groupは、傘下のMidea Robozone Technology製次世代ロボット掃除機S8+自動集塵ロボットの詳細を発表しました。

- iRobot社、Robomow社、Mayfield Robotics社などの企業が、家庭用ロボットを開発しています。人間の行動検出や音声認識のような技術革新は、顧客の信頼を高め、その結果、掃除、洗濯、その他の音声対応IoT活動のような家庭用目的での自動配備を促進しています。

- さらに、マシンビジョンカメラの開発が進む中、企業はAI技術を搭載した2Dおよび3Dマシンビジョンカメラを使用して、階段のような床の端と端を効果的にマッピングし、ケーブル、ごみ箱、ドア枠、敷物などの障害物を認識しています。機械学習、AI、顔認識などの技術を取り入れることで、家庭用ロボットにもイノベーションがもたらされています。例えば、2019年2月、クラウドAIとロボットソリューションの開発・運営会社であるCloudMinds Technologyは、クラウドAIをベースとした、コンプライアンスに優れたサービスロボット「XR-1」を発売しました。

アジア太平洋地域が大きな市場シェアを握る

- 同地域で国内のヘルスケアやアシスタンス用途へのロボット導入が大きく伸びている主な要因は高齢化です。日本政府は、2025年までに38万人の熟練労働者の不足を補うため、高齢者介護ロボットの開発に資金を拠出すると発表しました。このため、高齢者介護ロボットの導入は、近い将来、高齢者の住居でも促進されると予想されます。

- ロボット車椅子もこの地域で注目を集めています。パナソニックのような開発企業は、さまざまな使用事例を満たすことができる革新的な車椅子の開発にますます力を入れています。例えば、2021年2月、全日本空輸(ANA)ジャパンとパナソニック株式会社は、自動運転電動車椅子をテストするためのパートナーシップを締結しました。この協業は、東京成田国際空港におけるモビリティとアクセシビリティの選択肢を増やすための遠大な計画の一環です。

- 中国は最近、ロボット工学の分野で世界のリーダーになるために多大な努力をしているため、個人用ロボット導入の面で主要国になると予想されます。例えば、2021年12月、中国の工業情報化省は、他の14の政府部門と共同で、第14次5カ年計画において、同国のロボット産業を成長させる計画を発表しました。

- インドのような国では5Gの普及が進んでおり、住民が外出先からデータにアクセスできるため、警備・監視ロボットの配備を後押しすることも期待されています。インドのような国々は今後数年で5Gの導入を加速させると予想されており、個人向けロボット市場にとって有利な市場シナリオが生まれると期待されています。

- さらに、APACはほぼすべての主要な用途にヒューマノイドを採用する可能性が高いです。ヒューマノイドは、高齢者人口の増加に伴い、中国や日本などのAPAC諸国において、個人支援や介護の用途で使用されると予想されます。

パーソナルロボット産業の概要

パーソナルロボット市場の競合情勢は、依然として極めてダイナミックです。様々な用途における新たな顧客ニーズに対応するため、複数の新興企業が市場に参入しています。市場に参入している大手企業には、ソニー株式会社、本田技研工業株式会社、iRobot Corporation、Ecovacs Robotics Inc.などがあります。市場の最近の動向は以下の通りです。

- 2022年8月-Amazon.com Inc.は、ロボット掃除機メーカーのiRobot Corp.を現金取引で約17億米ドルで買収すると発表しました。この買収により、同社はパーソナルロボットとスマートホームデバイス市場でのプレゼンス拡大に注力します。

- 2022年5月-コンシューマー向けロボットのリーダーであるiRobot Corp.は、同社のジーニアス・ホーム・インテリジェンス・プラットフォームを進化させたiRobot OSを発表しました。新しいiRobot OSは、ロボットのスマート化を可能にし、すべてのお客様に有益な価値ある新機能を提供します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の業界への影響評価

第5章 市場力学

- 市場促進要因

- 障害者・高齢者向けアシストロボットの需要拡大

- パーソナルロボットの低価格化

- 市場抑制要因

- ロボット操作に伴う技術的複雑さ

第6章 市場セグメンテーション

- タイプ別

- 家庭用

- 娯楽

- 高齢者・障害者支援

- ホームセキュリティと監視

- その他

- 地域別

- 北米

- 欧州

- アジア太平洋

- 世界のその他の地域

第7章 競合情勢

- 企業プロファイル

- Sony Corporation

- Honda Motor Company Ltd

- Ecovacs Robotics Inc.

- iRobot Corporation

- Neato Robotics Inc.(Vorwerk Corporation)

- Samsung Group

- Gecko Systems International Corporation

- Hanool-Robotics Corp.

- Segway Inc.(Ninebot Company)

- F&P Robotics AG

第8章 投資分析

第9章 市場の将来

目次

Product Code: 69565

The Personal Robots Market is expected to register a CAGR of 18.6% during the forecast period.

Key Highlights

- The aging societies of the Asia-Pacific, like Japan and China, are driving growth in the medical technology sector, thus, creating a massive market for personal assistive robots in the region. According to the Statistics Bureau of Japan, the country's population (65 and over) is forecasted to grow from 36.39 million in 2021 to 39.21 million in 2040. This encourages companies to invest in products for the elderly in the region. One such robot that is already deployed is Paro (baby seal), designed to help patients with diseases like Alzheimer's.

- The technological innovations in various fields, such as cognition, interaction, and manipulation, make personal robots much more appealing. The technology and other component providers have been instrumental in driving the robotics ecosystem forward.

- Artificial intelligence (AI) technologies, including machine learning, computer vision, natural language processing, and gesture controls, are transforming how personal robots are deployed in homes and hospitals. As personal robots become more intelligent, they will be capable of comprehending their surroundings, avoiding static and dynamic objects, comprehending emotions, and communicating, allowing them to move around in congested and congested spaces like homes.

- Additionally, with the increasing developments in machine vision cameras, companies are using these 2D and 3D machine vision cameras with AI technologies to effectively map the edges of the floor, such as a staircase, and recognize obstacles, such as dustbins and cables, doorsills, and rugs which are expected to pave the way for next-generation robots.

- However, the lack of personal robot technology standardization, technical complexity associated with operating these robots, along with complications in the integration of these systems across various use cases are some of the major factors challenging the growth of the personal robots market.

- The coronavirus pandemic caused havoc in the manufacturing and technology industries. Several global and regional players in the robotics sector witnessed severe component and raw material shortages, which had a direct impact on their offerings. The worldwide supply chain network got disrupted by the nationwide lockdown in most nations, resulting in a drop in product sales.

- Moreover, due to the growing interest in robotic technologies, companies like ABB and Rockwell Automation have seen their stock values rise during the COVID-19 pandemic. In 2020, ForwardXRobotics recently announced USD 15 million in funding to expand into the North American market, while Brain Corp has experienced increasing demand for its floor-cleaning robots, especially among enterprises under closure orders for the previous few weeks.

- Such trends have had a negative impact on the growth of the studied market; however, with the awareness about advanced technologies growing within a larger section of the audience, especially since the outbreak of the pandemic, the long-term impact on the growth of the studied market is expected to be positive.

Personal Robots Market Trends

Personal Robots for Household Work is Expected to Hold a Major Share of the Market

- Robot companions/assistants/humanoids, vacuuming, floor cleaning, lawn mowing, pool cleaning, and window cleaning, among others, are some of the major types of robots that are increasingly gaining popularity in the household segment of personal robots. According to the data provided by the International Federation of Robotics (IFR) and Loup Ventures, about 22.1 million robotic vacuum cleaners are expected to be shipped by 2025, generating a revenue of approximately USD 4.98 billion.

- Among all the household robots, automated vacuum cleaners and moppers are the companies' most commercialized and developed products. The companies are continuously investing in developing more compact and integrated vacuum cleaners and mopping robots to reach little places at home. The companies are integrating advanced technologies like voice recognition and laser-based technologies to map the floor structure. For instance, in February 2022, Midea Group, a leading global high-technology company, announced details of Midea's S8+ auto-dust-collection robot, its next-gen robot vacuum cleaner, made by Midea Robozone Technology, one of its subsidiaries.

- Companies like iRobot, Robomow, and Mayfield Robotics, are among the prominent players, innovating robots for household space. Innovations, like detecting human behavior and voice recognition, are increasing customer confidence, thus, driving the automated deployment for household purposes, like cleaning, laundry, and other voice-enabled IoT activities.

- Additionally, with the increasing developments in machine vision cameras, companies are also using these 2D and 3D machine vision cameras with AI technologies to map and edges of the floor like staircases effectively and to recognize obstacles such as cables, dustbins, doorsills, and rugs. Incorporating technologies like machine learning, AI, and facial recognition, are also bringing innovations into household robots. For instance, in February 2019, CloudMinds Technology, a developer and operator of cloud AI and robotic solutions, launched its cloud AI-based, highly compliant service robot, the XR-1.

Asia Pacific to Hold Significant Market Share

- The aging population is a primary factor for the significant growth in the deployment of robots in domestic healthcare and assistance applications in the region. The Japanese government has announced funding for the development of eldercare robots to fill the estimated gap of 380,000 skilled workers by 2025. This is expected to drive the adoption of elderly care robots also at their residences in the recent future.

- Robotic wheelchairs are also gaining attraction in the region. Companies like Panasonic are increasingly making efforts to develop innovative wheelchairs that can fulfill different use cases. For instance, in February 2021, All Nippon Airways (ANA) Japan and Panasonic Corporation entered a partnership to test self-driving electric wheelchairs. The collaboration is part of a far-reaching plan to increase mobility and accessibility options at Tokyo Narita International Airport.

- China is expected to become the leading country in terms of personal robot adoption as the country has been making significant efforts lately to become a global leader in the field of robotics. For instance, in December 2021, China's Ministry of Industry and Information Technology, in collaboration with 14 other government departments, unveiled its plans to grow the country's robotics industry in its 14th five-year plan.

- The growing 5G penetration in countries like India is also expected to help push the deployment of security and surveillance robots as the residents can access the data on the go. Countries like India are expected to speed up the deployment of 5G in the coming years, which is expected to create a favorable market scenario for the personal robots market.

- Moreover, APAC is likely to adopt humanoids for almost all major applications. Humanoids are anticipated to be used in personal support and caregiving applications in APAC countries such as China and Japan as the senior population grows.

Personal Robots Industry Overview

The competitive landscape of the personal robotic market remains exceptionally dynamic. Several startups are entering the market to meet emerging customer needs for various applications. Some of the major players operating in the market include Sony Corporation, Honda Motor Company Ltd., iRobot Corporation, Ecovacs Robotics Inc., etc. Some of the recent developments in the market are as follows:-

- August 2022 - Amazon.com Inc announced the acquisition of iRobot Corp, the maker of robot vacuum cleaners, in an all-cash deal for about USD 1.7 billion. Through this acquisition, the company focuses on further expanding its presence in the personal robots and smart home devices market.

- May 2022 - iRobot Corp., a leader in consumer robots, introduced iRobot OS, an evolution of the company's Genius Home Intelligence platform. iRobot OS delivers a new customer experience for a healthier, cleaner, and smarter home. The new iRobot OS enables the robots to get smarter, delivering valuable new features and functionality that benefit all customers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing demand for Assistive Robots for Handicapped and Elderly People

- 5.1.2 Reducing Price of Personal Robots

- 5.2 Market Restraints

- 5.2.1 Technical Complexity Associated with Operating these Robots

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Household Work

- 6.1.2 Entertainment

- 6.1.3 Elderly and Handicap Assistance

- 6.1.4 Home Security and Surveillance

- 6.1.5 Other type

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia-Pacific

- 6.2.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Sony Corporation

- 7.1.2 Honda Motor Company Ltd

- 7.1.3 Ecovacs Robotics Inc.

- 7.1.4 iRobot Corporation

- 7.1.5 Neato Robotics Inc. (Vorwerk Corporation)

- 7.1.6 Samsung Group

- 7.1.7 Gecko Systems International Corporation

- 7.1.8 Hanool-Robotics Corp.

- 7.1.9 Segway Inc. (Ninebot Company)

- 7.1.10 F&P Robotics AG

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

パーソナルロボット:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日