|

市場調査レポート

商品コード

1630335

欧州の印刷包装:市場シェア分析、産業動向と統計、成長予測(2025~2030年)Europe Printed Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の印刷包装:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

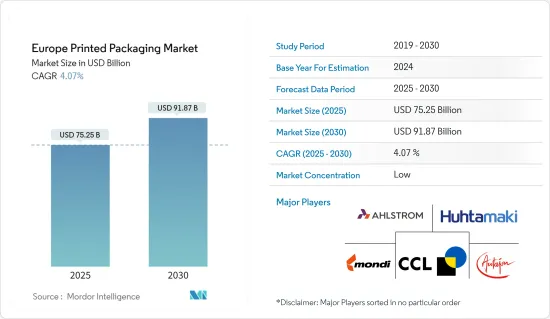

欧州の印刷包装市場規模は2025年に752億5,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは4.07%で、2030年には918億7,000万米ドルに達すると予測されます。

主要ハイライト

- 欧州の印刷包装市場は、いくつかの主要動向と消費者の需要を通じて進化しています。サステイナブル包装へのシフトが主要な促進要因であり、消費者の嗜好と規制要件により、リサイクル可能、生分解性、プラスチックフリーの包装を含む環境に優しいソリューションへの需要が高まっています。このため、特に環境影響への懸念が大きい飲食品産業では、紙ベースや植物ベースの材料の採用が増加しています。

- 印刷技術は、パーソナライズされカスタマイズ型包装ソリューションを可能にすることで、市場に変革をもたらしつつあります。この技術により、メーカーは特定の消費者の要求や限定品に対応するため、可変デザインで小ロット、コスト効率の良い印刷を行うことができます。消費者が個性的な包装体験を求める中、eコマースセグメントは主にこの動向を示しています。

- 例えば、2024年7月、Siegwerkは欧州市場初のUVフレキソ脱墨システムCIRKIT CLEARPRIME UV E02を発表しました。このシステムはUV印刷された感圧ラベル(PSL)を脱墨するソリューションを提供し、包装のリサイクル性を高めています。非食品包装用途に開発されたこのプライマー技術は、ラベル付きプラスチック包装のリサイクル性を向上させる。これにより、非食品包装用途での再利用に適した高品質の再生品を製造することができます。

- eコマースの成長により、包装要件は再構築され、製品の完全性を維持しながら輸送コストを最適化するための、保護的でありながら軽量なソリューションの必要性が強調されています。このため、輸送保護とコスト効率を提供する段ボールや軟包装材への需要が高まっています。eコマース企業もまた、オンライン購入時の開封体験を高めるため、高級感のある包装デザインに投資しています。

- 欧州市場では、メーカーが革新的な機能を統合することで、革新的な包装技術が台頭しています。QRコード、RFIDタグ、AR(拡張現実)コンポーネントは、製品情報を提供し、トレーサビリティを向上させ、インタラクティブな体験を生み出します。こうした技術は消費者の関心を高めると同時に、特に食品・医薬品産業ではサプライチェーン管理と製品認証をサポートします。

- 消費者の健康意識は、規制基準を満たした安全性に適合した包装への需要を強めています。食品や医薬品の包装は、製品の完全性を確保し、汚染を防止し、成分や有効期限情報を明白に表示しなければならないです。また、安全・安心を優先するセグメントでは、開封防止包装や小児用包装の採用が増加しています。こうした新興国市場の開拓は、消費者の嗜好、技術の進歩、規制要件への市場の適応を反映しています。

欧州の印刷包装市場の動向

飲料産業が大きなシェアを占める

- 欧州の飲料産業では、消費者の嗜好の変化、持続可能性の動向、技術の先進性などを背景に、印刷包装の需要が伸び続けています。印刷包装は、競争の激しい市場においてブランドの重要な差別化要因となっています。飲料メーカーが棚での存在感を競う中で、適切な包装はマーケティング戦略にとって不可欠となっています。印刷されたラベルや包装は、特にアルコール飲料のようなプレミアムセグメントにおいて、グラフィック、テクスチャ、仕上げを通じて製品のID確認と品質を伝えます。

- 印刷包装に対する需要の高まりは、持続可能性への関心の高まりに起因しています。欧州の消費者の環境意識は、ブランドに対して環境への影響を削減するよう促しています。その結果、リサイクル可能な材料、生分解性インク、サステイナブル印刷プロセスなど、環境に優しい包装ソリューションが採用されるようになりました。欧州連合(EU)の包装包装廃棄物指令は、飲料部門をサステイナブルプラクティスへと押し上げました。企業は現在、効率的な材料の再利用とリサイクルを確実にするため、循環経済の原則に沿った包装を優先しています。

- 飲料部門では、印刷包装によるパーソナライゼーションとプレミアム化が重視されています。ブランドは、多様な消費者の嗜好に応えるために、ユニークな限定デザインや地域限定のバリエーションを作ることができます。デジタル印刷技術は、生産時間の短縮、費用対効果の高い小ロット生産、デザインの柔軟性によって、このようなカスタマイズを可能にします。このため、消費者が高級包装を製品の品質と結びつけているクラフトビール、ワイン、スピリッツのセグメントで印刷包装需要が高まっている

- 印刷技術の先進は飲料用包装に変革をもたらしました。デジタル印刷は、ガラス、アルミニウム、プラスチックに高品質な印刷を行うことができるため、採用が進んでいます。この技術により、小ロットや季節ごとのリリース用にカスタマイズ型包装の効率的な生産が可能になりました。デジタル印刷は、従来の方法と比較して廃棄物やエネルギー消費を削減し、産業の持続可能性の目標をサポートします。QRコードやAR(拡張現実)を含むインタラクティブな包装機能は、消費者との革新的な関わりを可能にします。

- 規制圧力と消費者行動は、飲料セクターにおける印刷包装の将来を形作る。廃棄物を最小限に抑え、リサイクルを促進するための欧州政府による包装規制の厳格化により、メーカーはサステイナブル材料とプロセスを採用するようになりました。リサイクル情報や持続可能性への取り組みを効果的に伝える包装への需要が高まっています。印刷ラベルは規制遵守を促進し、環境意識の高い消費者にアピールします。欧州飲料の印刷包装市場は、持続可能性の要件、技術革新、ブランディングのニーズを通じて進化し続けています。

- フランスのアルコール飲料市場の印刷包装需要は、2023年7月から2024年6月までの数量と直接相関しています。ビールとライトビールは13億1,244万本で最大のセグメントを占め、製品の差別化のために広範な印刷包装ソリューションを必要としています。サイダーは4,634万本で、個性的な包装デザインが求められます。スピリッツとリキュールは2億7,588万本で、詳細なラベルと高級仕上げの洗練された印刷包装を必要としています。1億5,753万本の食前酒カテゴリーでは、製品の特徴を強調するために印刷包装が利用されています。スパークリングワインとシャンパンは1億9,162万本で、プレミアムな位置づけを伝えるために印刷包装を利用しています。これらのカテゴリー全体の成長は、ブランドの可視性と市場での存在感を高めるための印刷包装ソリューションの需要を引き続き促進しています。

ドイツは著しい成長が見込まれる

- 飲食品、医薬品、化粧品、消費財、eコマースなど、いくつかの主要産業がドイツの印刷包装市場を牽引しています。飲食品セグメントでは、持続可能性を第一に、カートン、ラベル、軟質包装など、ブランディングを目的とした機能的な包装が求められています。製薬産業は、主に印刷された紙器、ラベル、インサートを使用し、高品質で、改ざん防止が可能で、情報が豊富な包装に対する要求を通じて、大きな需要を生み出しています。

- 化粧品とパーソナルケア製品は、機能性と美観のために印刷包装を利用し、チューブ、ラベル、高級紙器が組み込まれ、環境に優しい材料の採用が増加しています。家庭用品、電子機器、アパレルを含む消費財セクターは、製品の差別化、物流、オンライン小売の目的で印刷包装を必要としています。

- ドイツの化粧品市場は、2021~2023年にかけて着実な成長を遂げており、これは市場金額の増加に反映されています。2021年の市場規模は147億4,000万米ドルで、2022年には154億7,000万米ドルに成長し、2023年には172億2,000万米ドルにさらに拡大します。この成長は、スキンケアや美容製品に対する消費者の需要の高まり、プレミアムでサステイナブル化粧品への支出の増加、パーソナライズされた包装に対する消費者の嗜好から生じています。

- 市場成長は持続可能性へのシフトを反映しており、ドイツの消費者は環境に優しく倫理的に生産された化粧品を求めています。この動向は、リサイクル可能な材料や生分解性包装など、包装のイノベーションを推進し、ブランドの差別化要因として欠かせないものとなっています。eコマースは重要な流通チャネルとして台頭し、化粧品のオンラインショッピングは大流行の最中とその後に大幅に増加し、視覚的に魅力的で機能的な印刷包装の需要を生み出しています。

- デジタル印刷技術は、高級と大衆向け化粧品ブランド向けにカスタマイズ型包装オプションを可能にすることで、市場の開拓を強化しました。この先進包装は、主にパーソナライズされた限定品を通じて、包装メーカーが特定の消費者の嗜好に対応する機会を生み出しています。

- eコマースは、オンライン小売企業がブランド化され、丈夫でリサイクル可能な配送資材を求めているため、印刷包装の需要を高めています。このセグメントでは、カスタムボックスとブランドメーラーが主流です。自動車と産業部門は一貫して印刷包装ソリューションを要求しており、主に部品とコンポーネントに段ボール箱とラベルを使用しています。

- 市場は、消費者の嗜好と欧州連合の包装廃棄物規制の影響を受け、すべてのセクターで持続可能性への大幅なシフトを示しています。ドイツ企業は、リサイクル可能、生分解性、再生可能な材料を包装ソリューションに導入しています。デジタル印刷技術は、環境問題やブランディング要件に対応した、カスタマイズ型小ロットの包装生産を可能にします。市場は、持続可能性とイノベーションを基本的な促進要因として、進化を続けています。

欧州の印刷包装産業概要

欧州の印刷包装市場は、Amcor Group、Mondi plc、CCL Industries Inc.などの有力企業が国内外レベルで事業を展開しているため、セグメント化されています。戦略的成長を目的とした合併、買収、関連事業や事業部門の連携は、包装産業において繰り返し見られる市場動向です。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- 印刷産業における技術進歩の拡大

- エンドユーザー向け包装用途の拡大

- 市場抑制要因

- 原料価格の変動と印刷包装コストへの影響

第6章 市場セグメンテーション

- 印刷技術別

- オフセット・リソグラフィー

- グラビア印刷

- フレキソ印刷

- デジタル印刷

- スクリーン印刷

- インキタイプ別

- 溶剤ベースインキ

- UV硬化型インキ

- 水性インキ

- 包装タイプ別

- ラベル

- プラスチック

- ガラス

- 金属

- 紙・板紙

- 用途別

- 化粧品・在宅医療

- 飲食品

- 医薬品

- その他

- 国別

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ポーランド

- オランダ

第7章 競合情勢

- 企業プロファイル

- Mondi plc

- Ahlstrom Oyj

- Autajon Group

- Huhtamaki Oyj

- CCL Industries Inc.

- Clondalkin Group Holdings BV

- Constantia Flexibles Group GmbH

- Amcor Group

- Smurfit Westrock plc

- DS Smith PLC

- International Paper Company

第8章 投資分析

第9章 市場機会と今後の動向

The Europe Printed Packaging Market size is estimated at USD 75.25 billion in 2025, and is expected to reach USD 91.87 billion by 2030, at a CAGR of 4.07% during the forecast period (2025-2030).

Key Highlights

- The Europe printed packaging market is evolving through several key trends and consumer demands. The shift toward sustainable packaging is a primary driver, with consumer preferences and regulatory requirements increasing demand for eco-friendly solutions, including recyclable, biodegradable, and plastic-free packaging. This has increased the adoption of paper-based and plant-based materials, particularly in the food and beverage industry, where environmental impact concerns are significant.

- Printing technologies are transforming the market by enabling personalized and customized packaging solutions. This technology allows manufacturers to produce small-batch, cost-effective print runs with variable designs to meet specific consumer requirements and limited-edition products. The e-commerce sector mainly demonstrates this trend, as consumers seek distinctive packaging experiences.

- For instance, in July 2024, Siegwerk introduced CIRKIT CLEARPRIME UV E02, its first UV flexo deinking system for the European market. The system provides a solution for deinking UV-printed pressure-sensitive labels (PSL) and enhances package recyclability. The primer technology, developed for non-food packaging applications, improves the recyclability of labeled plastic packaging. It enables the production of high-quality recyclates suitable for reuse in non-food packaging applications.

- E-commerce growth has reshaped packaging requirements, emphasizing the need for protective yet lightweight solutions to optimize shipping costs while maintaining product integrity. This has increased demand for corrugated cardboard and flexible packaging materials that provide transit protection and cost efficiency. E-commerce companies also invest in premium packaging designs to enhance the unboxing experience for online purchases.

- Innovative packaging technologies emerge in the European market as manufacturers integrate innovative features. QR codes, RFID tags, and augmented reality components provide product information, improve traceability, and create interactive experiences. These technologies enhance consumer engagement while supporting supply chain management and product authentication, particularly in the food and pharmaceutical industries.

- Consumer health consciousness has intensified the demand for safety-compliant packaging that meets regulatory standards. Food and pharmaceutical packaging must ensure product integrity, prevent contamination, and display evident ingredient and expiration information. The market also shows increased adoption of tamper-evident and child-resistant packaging in sectors prioritizing safety and security. These developments reflect the market's adaptation to consumer preferences, technological progress, and regulatory requirements.

Europe Printed Packaging Market Trends

Beverage Industries to Hold Significant Share

- The demand for printed packaging in the European beverage sector continues to grow, driven by evolving consumer preferences, sustainability trends, and technological advancements. Printed packaging serves as a key differentiator for brands in a competitive market. As beverage companies compete for shelf presence, adequate packaging has become essential to their marketing strategy. Printed labels and packaging communicate product identity and quality through graphics, textures, and finishes, particularly in premium segments like alcoholic beverages.

- The increased demand for printed packaging stems from a heightened focus on sustainability. European consumers' environmental awareness has compelled brands to reduce their environmental impact. This has resulted in adopting eco-friendly packaging solutions, including recyclable materials, biodegradable inks, and sustainable printing processes. The European Union's Packaging and Packaging Waste Directive has pushed the beverage sector toward sustainable practices. Companies now prioritize packaging aligned with circular economy principles to ensure efficient material reuse and recycling.

- The beverage sector emphasizes personalization and premiumization through printed packaging. Brands can create unique, limited-edition designs and region-specific variants to meet diverse consumer preferences. Digital printing technologies enable this customization through faster production times, cost-effective small runs, and design flexibility. This has increased printed packaging demand in craft beer, wine, and spirits segments, where consumers associate premium packaging with product quality.

- Printing technology advances have transformed beverage packaging. Digital printing has gained adoption for its ability to produce high-quality prints on glass, aluminum, and plastic. This technology enables efficient production of customized packaging for small batches and seasonal releases. Digital printing reduces waste and energy consumption compared to traditional methods, supporting industry sustainability goals. Interactive packaging features, including QR codes and augmented reality, enable innovative consumer engagement.

- Regulatory pressures and consumer behavior shape printed packaging's future in the beverage sector. European governments' stricter packaging regulations to minimize waste and promote recycling have led manufacturers to adopt sustainable materials and processes. Demand has increased for packaging that effectively communicates recycling information and sustainability initiatives. Printed labels facilitate regulatory compliance and appeal to environmentally conscious consumers. The printed packaging market in European beverages continues to evolve through sustainability requirements, technological innovation, and branding needs.

- The French alcoholic beverage market's printed packaging demand correlates directly with sales volumes from July 2023 to June 2024. Beer and light beer, with 1,312.44 million units, represent the largest segment, requiring extensive printed packaging solutions for product differentiation. The cider segment, accounting for 46.34 million units, generates demand for distinct packaging designs. Spirits and liqueurs, at 275.88 million units, require sophisticated printed packaging with detailed labels and premium finishes. The aperitifs category, with 157.53 million units, utilizes printed packaging to emphasize product characteristics. Sparkling wine and champagne, representing 191.62 million units, rely on printed packaging to communicate premium positioning. The growth across these categories continues to drive the demand for printed packaging solutions to enhance brand visibility and market presence.

Germany is Expected to Witness Significant Growth

- Several key industries, including food and beverages, pharmaceuticals, cosmetics, consumer goods, and e-commerce, drive the printed packaging market in Germany. The food and beverage sector requires functional packaging for branding purposes, including cartons, labels, and flexible packaging, with sustainability as a primary focus. The pharmaceutical industry generates substantial demand through its requirements for high-quality, tamper-evident, and information-rich packaging, primarily using printed folding cartons, labels, and inserts.

- Cosmetics and personal care products utilize printed packaging for functionality and aesthetic appeal, incorporating tubes, labels, and premium folding cartons, with increasing adoption of eco-friendly materials. The consumer goods sector, encompassing household items, electronics, and apparel, requires printed packaging for product differentiation, logistics, and online retail purposes.

- The cosmetics market in Germany has experienced steady growth from 2021 to 2023, as reflected by the increasing market value. In 2021, the market was valued at USD 14.74 billion, growing to USD 15.47 billion in 2022 and further expanding to USD 17.22 billion in 2023. This growth stems from rising consumer demand for skincare and beauty products, increased spending on premium and sustainable cosmetic products, and consumer preference for personalized packaging.

- The market growth reflects a shift toward sustainability, with German consumers seeking eco-friendly and ethically produced cosmetics. This trend drives packaging innovations, including recyclable materials and biodegradable packaging, which have become essential brand differentiators. E-commerce has emerged as a significant sales channel, with online cosmetics shopping increasing substantially during and after the pandemic, creating demand for visually appealing and functional printed packaging.

- Digital printing technologies have enhanced the market's development by enabling customized packaging options for luxury and mass-market cosmetic brands. This advancement has created opportunities for packaging manufacturers to address specific consumer preferences, mainly through personalized and limited-edition products.

- E-commerce has increased the demand for printed packaging as online retail companies seek branded, sturdy, and recyclable shipping materials. Custom boxes and branded mailers dominate this segment. The automotive and industrial sectors consistently demand printed packaging solutions, primarily using corrugated boxes and labels for parts and components.

- The market demonstrates a substantial shift toward sustainability across all sectors, influenced by consumer preferences and European Union packaging waste regulations. German companies implement recyclable, biodegradable, and renewable materials in their packaging solutions. Digital printing technologies enable customized, short-run packaging production that addresses environmental concerns and branding requirements. The market continues to evolve, with sustainability and innovation as fundamental drivers.

Europe Printed Packaging Industry Overview

Europe's Printed Packaging market is fragmented because many players run their businesses at national and international levels, with significant players like Amcor Group, Mondi plc, CCL Industries Inc.and among others. Mergers, acquisitions, and collaboration of relevant businesses and business units for strategic growth have been recurring market trends in the packaging industry.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Technological Advancement in the Printing Industry

- 5.1.2 Expanding End-user Packaging Applications

- 5.2 Market Restraint

- 5.2.1 Fluctuations in Raw Material Prices and Their Impact on the Cost of Printed Packaging

6 MARKET SEGMENTATION

- 6.1 By Printing Technology

- 6.1.1 Offset Lithography

- 6.1.2 Rotogravure

- 6.1.3 Flexography

- 6.1.4 Digital Printing

- 6.1.5 Screen Printing

- 6.2 By Ink Type

- 6.2.1 Solvent-based Ink

- 6.2.2 UV-curable Ink

- 6.2.3 Aqueous Ink

- 6.3 By Packaging Type

- 6.3.1 Label

- 6.3.2 Plastic

- 6.3.3 Glass

- 6.3.4 Metal

- 6.3.5 Paper and Paperboard

- 6.4 By Application

- 6.4.1 Cosmetic and Homecare

- 6.4.2 Food and Beverage

- 6.4.3 Pharmaceutical

- 6.4.4 Other Applications

- 6.5 By Country

- 6.5.1 United Kingdom

- 6.5.2 Germany

- 6.5.3 France

- 6.5.4 Spain

- 6.5.5 Italy

- 6.5.6 Poland

- 6.5.7 Netherlands

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Mondi plc

- 7.1.2 Ahlstrom Oyj

- 7.1.3 Autajon Group

- 7.1.4 Huhtamaki Oyj

- 7.1.5 CCL Industries Inc.

- 7.1.6 Clondalkin Group Holdings BV

- 7.1.7 Constantia Flexibles Group GmbH

- 7.1.8 Amcor Group

- 7.1.9 Smurfit Westrock plc

- 7.1.10 DS Smith PLC

- 7.1.11 International Paper Company