|

市場調査レポート

商品コード

1630294

半導体用電池-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Batteries For Semiconductor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 半導体用電池-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

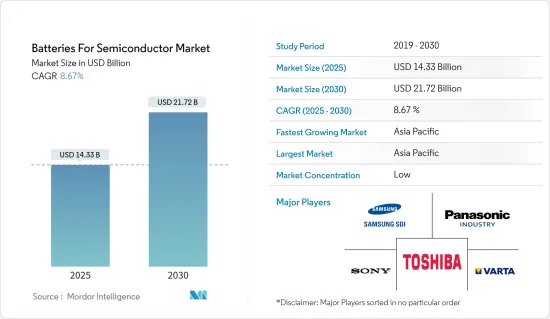

半導体用電池市場規模は2025年に143億3,000万米ドルと推定・予測され、予測期間中(2025~2030年)のCAGRは8.67%で、2030年には217億2,000万米ドルに達すると予測されます。

長期的には、電気自動車の普及と携帯電話需要の増加が予測期間中の市場を牽引するとみられます。

一方、エネルギー密度の低さ、寿命の短さ、充電能力の遅さといった電池の技術的課題は、予測期間中の市場成長を妨げると予想されます。

エネルギー貯蔵システムの採用が増加していることから、半導体用電池市場には大きなビジネス機会が生まれると予想されます。

アジア太平洋には大規模な電池製造インフラが存在するため、消費者用電池市場ではアジア太平洋が支配的な地域になると予想されます。

半導体用電池市場の動向

電気自動車セグメントが大きな需要を獲得する見込み

- 電気自動車(EV)市場セグメントは近年大幅な成長を遂げており、これが半導体市場の電池需要に大きな影響を与えています。EVは、その環境上の利点と技術の進歩により人気を集め続けているため、効率的で信頼性の高い電池の必要性が最も重要になっています。この需要の急増は半導体市場全体に波及効果をもたらし、産業の利害関係者に新たな機会と課題を生み出しています。

- 国際エネルギー機関(IEA)によると、2022年の世界の電気自動車は増加傾向にあり、世界のプラグイン軽電気自動車の累積販売台数は約1,020万台で、2021~2022年にかけて56.9%の成長率を記録し、2018~2022年にかけては5倍に増加しました。

- EV市場セグメントの成長を支える主要要因の1つは、環境問題に対する世界の意識の高まりです。政府と消費者は、よりクリーンでサステイナブル輸送手段を提唱しており、EVは実行可能なソリューションとして浮上しています。このため、電気自動車の採用を促進するさまざまな優遇措置、減税措置、規制が実施されています。その結果、自動車メーカーはEVの生産に重点を移しつつあり、半導体市場における先進的電池技術の需要を高めています。

- 例えば、カナダ政府は2023年1月、国内で販売される自動車の少なくとも20%を2026年から電気自動車にすると発表しました。この発表は、カナダが設定した二酸化炭素排出量目標を達成するため、同国での電気自動車の普及を促進するために行われました。政府はまた、全国で電気自動車用電池を製造する企業に生産奨励金を提供することも発表しています。

- 電気自動車市場セグメントの成長軌道は、半導体産業に連鎖的な影響を及ぼし、市場関係者にさまざまな機会をもたらしています。半導体メーカーは、電気自動車用電池、電池管理システム、パワーエレクトロニクスに必要な最先端の部品やチップを開発・供給する機会を得る。これは、収益の可能性を高め、拡大するEV市場に資本参加する機会につながります。

- 電気自動車の販売台数が増加し、政府の施策も後押ししていることから、半導体用電池の研究開発活動はさらに活発化すると予想されます。

アジア太平洋が大幅な市場成長を占める

- アジア太平洋の半導体用電池市場は、世界の半導体産業に大きな影響を与える極めて重要でダイナミックな地域です。この広大で多様な地域には多くの国が含まれ、それぞれが独自の経済的技術的展望を持っています。アジア太平洋の半導体市場における電池需要は、急速な工業化、民生用電子機器製品の使用増加、急成長する電気自動車市場などの要因によって、着実に増加しています。

- アジア太平洋における半導体用電池需要の重要な原動力の一つは、民生用電子機器製品の急激な成長です。この成長の原動力となっているのは、特に中国やインドなどの国々における可処分所得の増加と中流階級の人口の急増です。これらの消費者は、スマートフォン、ノートパソコン、その他の個人用電子機器をますます採用するようになっており、その結果、これらのガジェットに電力を供給する先進的半導体用電池の必要性が高まっています。民生用電子機器が日常生活の不可欠な一部となるにつれ、アジア太平洋の半導体メーカーは、この成長市場セグメントから利益を得る態勢を整えています。

- さらに、アジア太平洋では電気自動車の導入が大幅に増加しています。環境の持続可能性にますます焦点が当てられ、電気自動車を促進する政府のインセンティブもあり、中国のような国々が電気自動車市場で重要な参入企業となっています。

- 例えば、中国汽車工業協会(AMMA)によると、2023年5月現在、中国は電気自動車(EV)の最大市場であり、プラグイン・ハイブリッド車(PHEV)が79万3,000台、電池電気自動車(BEV)が214万6,000台販売されると推定されています。2022年には、電池電気自動車の販売台数が545万台と、この国が最も多くなります。予測期間中、世界最大の電気自動車市場であり続けると予想されます。

- 電気自動車には、電力と電池の性能を管理するための効率的で信頼性の高い半導体部品が必要であるためです。したがって、電気自動車市場の成長は、アジア太平洋の半導体用電池メーカーに大きな機会を提供しています。

- 結論として、半導体市場における電池のアジア太平洋市場セグメントは、ダイナミックで急速に進化しています。民生用電子機器と電気自動車が牽引するこの地域の半導体用電池需要の拡大は、メーカーに大きなビジネス機会を提供しています。したがって、上記の点から、予測期間中、アジア太平洋が半導体用電池市場を独占することになります。

半導体用電池産業概要

半導体用電池市場は高度にセグメント化され、統合されています。主要企業(順不同)には、SamsungSDI、Sony Corporation、Panasonic Corporation、Varta AG、Toshiba Corporationなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- モバイル機器の需要増加

- 電気自動車の普及

- 抑制要因

- 技術的課題の有無

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 種類

- リチウムイオン

- ニッケル水素

- リチウムイオンポリマー

- ナトリウムイオン電池

- 用途

- 民生用電子機器製品

- 電気自動車

- エネルギー貯蔵システム

- その他のエンドユーザー用途

- 市場分析:地域別(2028年までの市場規模と需要予測)

- 北米

- 米国

- カナダ

- その他の北米

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他の欧州

- 南米

- チリ

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- エジプト

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Samsung SDI Co Ltd.

- Sony Corporation

- Panasonic Corporation

- Varta AG

- Toshiba Corporation

- EnerSys

- GS Yuasa Corporation

- Faradion Limited

- Routejade

- TianJin Lishen Battery Joint-Stock Co. Ltd.

- Market Ranking/Share Analysis

第7章 市場機会と今後の動向

- エネルギー貯蔵システムの革新

The Batteries For Semiconductor Market size is estimated at USD 14.33 billion in 2025, and is expected to reach USD 21.72 billion by 2030, at a CAGR of 8.67% during the forecast period (2025-2030).

Over the long term, the increasing adoption of electric vehicles and demand for mobile phones are expected to drive the market during the forecasted period.

On the other hand, technological challenges of batteries, like low energy density, lower lifespan, and slower charging capacity, are expected to hinder the growth of the market during the forecasted period.

Nevertheless, the increasing adoption of energy storage systems is expected to create huge opportunities for the Batteries for Semiconductor Market.

Asia-Pacific is expected to be a dominant region for the Consumer Battery Market due to the presence of a large battery manufacturing infrastructure in the region.

Semiconductor Battery Market Trends

The Electric Vehicle Segment is Expected to Witness Significant Demand

- The electric vehicle (EV) market segment has witnessed substantial growth in recent years, and this has had a significant impact on the demand for batteries in the semiconductor market. As EVs continue to gain popularity due to their environmental benefits and technological advancements, the need for efficient and reliable batteries has become paramount. This surge in demand has generated a ripple effect throughout the semiconductor market, creating new opportunities and challenges for stakeholders in the industry.

- According to the International Energy Agency, global electric vehicles are on the rise in 2022; the cumulative plug-in light electric vehicle sales globally were around 10.2 million units, recording a growth rate of 56.9% between 2021 and 2022 and a fivefold increase between 2018 and 2022.

- One of the key drivers behind the growth of the EV market segment is the increasing global awareness of environmental concerns. Governments and consumers are advocating for cleaner and more sustainable modes of transportation, and EVs have emerged as a viable solution. This has led to various incentives, tax breaks, and regulations promoting the adoption of electric vehicles. As a result, automakers are shifting their focus towards EV production, thus bolstering the demand for advanced battery technologies within the semiconductor market.

- For instance, in January 2023, the Government of Canada announced that at least 20% of the vehicles sold in the country will be electric vehicles from 2026, and it will gradually increase to 60% in 2030 and reach 100% by the end of 2035. This announcement was made to increase the adoption of electric vehicles in the country to meet the carbon emission targets set by Canada. The government has also announced offering production incentives to companies manufacturing electric vehicle batteries nationwide.

- The electric vehicle market segment's growth trajectory has a cascading effect on the semiconductor industry, creating a range of opportunities for market players. Semiconductor manufacturers have a chance to develop and supply the cutting-edge components and chips required for EV batteries, battery management systems, and power electronics. This translates to increased revenue potential and the chance to capitalize on the expanding EV market.

- With the increasing sales of electric vehicles and the supportive government policies, the segment is expected to increase further, increasing the research and development activities in the battery for semiconductor segment.

Asia-Pacific Account for Significant Market Growth

- The Asia-Pacific market segment for batteries in the semiconductor market is a pivotal and dynamic region with significant implications for the global semiconductor industry. This vast and diverse region encompasses many countries, each with its unique economic and technological landscape. The demand for batteries in the semiconductor market within the Asia Pacific region has been steadily rising, driven by factors that include rapid industrialization, increasing consumer electronics usage, and the burgeoning electric vehicle market.

- One of the critical drivers for the demand for semiconductor batteries in the Asia-Pacific region is the exponential growth in consumer electronics. This growth is driven by rising disposable incomes and a surging middle-class population, especially in countries like China and India. These consumers are increasingly adopting smartphones, laptops, and other personal electronic devices, which, in turn, fuels the need for advanced semiconductor batteries to power these gadgets. As consumer electronics become an integral part of everyday life, semiconductor manufacturers in the Asia-Pacific region are poised to benefit from this growing market segment.

- Additionally, the Asia-Pacific region has witnessed a substantial uptick in electric vehicle adoption. With an increasing focus on environmental sustainability and government incentives to promote electric vehicles, countries like China have become significant players in the electric vehicle market.

- For instance, according to the China Association of Automobile Manufacturers (AMMA), as of May 2023, China is the largest market for electric vehicles (EV), with an estimated 0.793 million plug-in hybrid Electric vehicles (PHEVs) and 2.146 million battery electric vehicles (BEVs) being sold. In 2022, the country recorded the highest sales of battery electric vehicles, with 5.45 million. It is expected to remain the world's largest electric car market during the forecast period.

- This, in turn, has led to soaring demand for advanced batteries in the semiconductor market, as EVs require efficient and reliable semiconductor components to manage power and battery performance. The growth of the electric vehicle market, therefore, offers substantial opportunities for semiconductor battery manufacturers in the Asia-Pacific region.

- In conclusion, the Asia-Pacific market segment for batteries in the semiconductor market is a dynamic and rapidly evolving landscape. The region's growing demand for semiconductor batteries, driven by consumer electronics and electric vehicles, offers significant opportunities for manufacturers. Therefore, per the above points, the Asia-Pacific region will dominate the battery for semiconductor market during the forecasted period.

Semiconductor Battery Industry Overview

The batteries for semiconductor market are highly fragmented and consolidated. The major companies (in no particular order) include Samsung SDI Co Ltd, Sony Corporation, Panasonic Corporation, Varta AG, and Toshiba Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand for Mobile Devices

- 4.5.1.2 Rising Adaption of Electric Vehicles

- 4.5.2 Restraints

- 4.5.2.1 Availability of Technical Challenges

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Lithium-Ion

- 5.1.2 Nickel-Metal Hydride

- 5.1.3 Lithium-Ion Polymer

- 5.1.4 Sodium-Ion Battery

- 5.2 End-User Application

- 5.2.1 Consumer Electronics

- 5.2.2 Electric Vehicles

- 5.2.3 Energy Storage System

- 5.2.4 Other End-User Applications

- 5.3 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Asia-Pacific

- 5.3.2.1 China

- 5.3.2.2 India

- 5.3.2.3 Japan

- 5.3.2.4 South Korea

- 5.3.2.5 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Chile

- 5.3.4.2 Brazil

- 5.3.4.3 Argentina

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Egypt

- 5.3.5.5 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Samsung SDI Co Ltd.

- 6.3.2 Sony Corporation

- 6.3.3 Panasonic Corporation

- 6.3.4 Varta AG

- 6.3.5 Toshiba Corporation

- 6.3.6 EnerSys

- 6.3.7 GS Yuasa Corporation

- 6.3.8 Faradion Limited

- 6.3.9 Routejade

- 6.3.10 TianJin Lishen Battery Joint-Stock Co. Ltd.

- 6.4 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Innovation in Energy Storage System