|

市場調査レポート

商品コード

1851801

ロボットオペレーティングシステム:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Robot Operating System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ロボットオペレーティングシステム:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月06日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

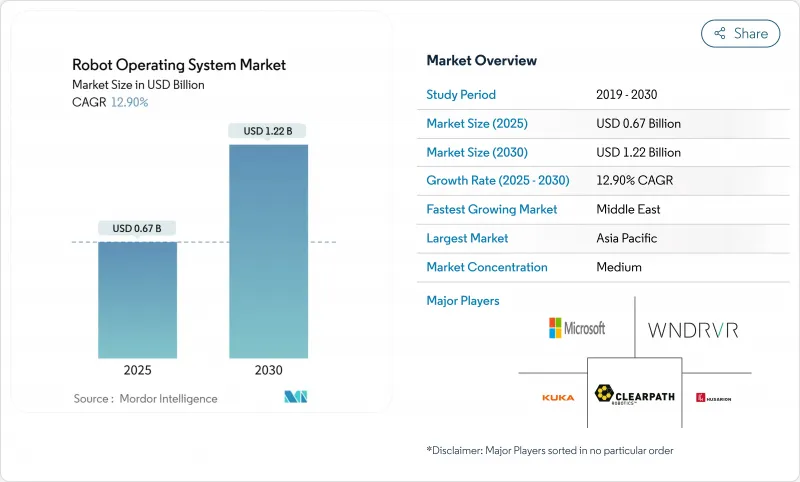

ロボットオペレーティングシステムの市場規模は2025年に6億7,000万米ドルと推定され、2030年には12億2,000万米ドルに達し、CAGR 12.9%で成長すると予測されています。

成長の背景には、産業オートメーション化の進展、相互運用性要件の拡大、大規模なリエンジニアリングなしに変化する現場の状況にロボットを適応させるオープンなモジュール型ソフトウェアへのシフトがあります。エッジコンピューティングと5Gの進歩は、リアルタイム制御をロボットに近づけ、クラウドシミュレーションとRobot-as-a-Serviceモデルは、ロボット工学に新規参入する企業の参入障壁を低くしています。ROS-Industrialライブラリが幅広く利用できるようになったことで、モーション、知覚、安全機能が標準化され、導入時間が短縮されます。自動車、エレクトロニクス、ヘルスケアの各メーカーは、大量生産と柔軟なツーリングへのニーズのバランスが取れているため、主要な採用企業となっています。ROS 1が2025年5月にサポート終了を迎える中、長期サポート、セキュリティ強化、アップデート・オーケストレーションをバンドルするプラットフォーム・ベンダーは、プレミアム・サービスの地位を確立しつつあります。

世界のロボットオペレーティングシステム市場の動向と洞察

自動車組立ラインにおけるROS対応コボットの採用拡大

自動車グループは、タクトタイムの改善と熟練労働者の不足に対処するため、協働ロボットの導入を強化しています。フォルクスワーゲン、ゼネラルモーターズ、テスラは、接着、検査、ネジ締め作業にROSベースのコボットを統合し、ステーションのスループットを向上させ、高いファーストパス歩留まりを維持しています。ステランティスはミラフィオーリ工場で、拡張現実ガイダンスとデジタルツインフィードバックでモバイルマニピュレータを同期させることにより、組立効率が27%向上することを実証しました。ROS 2で構成されたコボットは、単一障害点を取り除き、安全パラメータのライブ更新を可能にするDDSミドルウェアの恩恵を受けています。成長には、センサーコストの低下と、混合モデルラインの統合時間を短縮するプラグアンドプレイツールが引き続き貢献しています。

クラウドベースのシミュレーションプラットフォームの拡大

産業界の開発者は、工場フロアにハードウェアを設置する前に、仮想環境でロボットの全作業負荷を検証することが増えています。FogROS2-FTフレームワークは、計算負荷の高いモーションプランニングクエリを複数のクラウドエンドポイントにオフロードすることで、シミュレーションコストを2.2倍削減し、耐障害性を強化します。AWS RoboMakerや同様のサービスには継続的な統合フックが付属しており、コードのコミットごとに自動回帰テストがトリガーされ、開発スプリントが短縮されます。開発者はこれらのパイプラインを使用して、物理的な生産ラインを停止することなく、知覚と把握アルゴリズムを反復し、新しいSKUのゴーライブタイムラインを加速します。

分散ROSネットワークにおけるサイバーセキュリティの脆弱性

ROS 1のノードは、なりすましやリプレイが可能な暗号化されていないTCPROSトピックに依存しており、セーフティクリティカルなアクチュエータが露出する可能性があります。ROS 2は、DDSを通じて認証とアクセス制御プラグインを組み込んでいますが、フリートが複数のVLANにまたがっている場合、誤設定は依然として一般的です。最近の侵入テストでは、ヘルスケアロボットの導入における証明書管理の脆弱性が明らかになり、オペレータはゼロトラスト・ポリシー、セグメント化されたネットワーク、リアルタイムの異常検知を導入するよう促されました。業界コンソーシアムは現在、ハードニング・ガイドを発行しているが、中小メーカーは推奨されるパッチを適用するサイバーセキュリティ担当者が不足していることが多いです。

セグメント分析

産業用ロボットは、溶接、パレタイジング、CNC作業などでの長年にわたる利用を反映し、2024年の売上高の57%を占めました。ファナックの100万台達成は、その規模とインストールベースの成熟度を裏付けています。このコホートの中で、コボットは自動車への導入の4分の1を占め、混合モデルラインでの人間と機械の協働を推進していることを強調しています。サービスロボット、特にロジスティクスAMRと病院搬送ロボットは、eコマースのフルフィルメントへの圧力と患者ケアの品質への取り組みに後押しされ、2030年までのCAGRが16.8%になると予想されています。

サービス・セグメントの勢いは、棚の補充や自律清掃のためのAIビジョンと組み合わせたナビゲーション対応プラットフォームの導入が増加していることからも明らかです。ベンダーは、ROS 2のリアルタイムサービス品質設定を活用して、大規模な施設全体でSLAMマップの一貫性を維持しています。サブスクリプションの価格設定が施設管理の予算と整合するにつれて、プロフェッショナルな環境にサービスを提供するサービスユニットのロボットオペレーティングシステム市場規模は急速に拡大すると予測されます。産業機器メーカーは、分析ダッシュボードをバンドルし、稼働時間の指標を鮮明にする予測保守オーバーレイを追加する傾向が強まっています。

自動車メーカーは、ROSベースのモーション・プランニングと品質検査パイプラインを使用して、ラインを停止することなく、より高いモデルのバリエーションを管理しています。ヘキサポッド・アライメント・システムは、運転支援機能に必要なヘッドランプ・キャリブレーションと光学センサーの位置決めをサポートします。コネクテッド自動運転車のデモでは、ROS 2によって同期化されたAMRタガーが、ジャスト・イン・タイムで部品ビンに部品を補充し、エンド・オブ・ライン・ステーションのスループットを向上させる様子が紹介されています。

ヘルスケアは15.91%のCAGRを記録し、最も急上昇しました。ROSベースの手術支援装置は、決定論的ループタイミングを採用して多軸ツールパスを調整し、厳しい運動学的精度目標を達成しています。PeTRAのような病院物流プラットフォームは、ROS 2と高度なHRIモジュールを組み合わせ、群衆をナビゲートし、患者のバイタルにリアルタイムで対応します。プロバイダーが手術室をデジタル化するにつれて、ヘルスケアロボットのロボットオペレーティングシステム市場規模は診断とリハビリに拡大すると予想されます。

ロボットオペレーティングシステム市場は、ロボットタイプ別(産業用ロボット、サービスロボット)、エンドユーザー産業別(自動車、その他)、コンポーネント別(ソフトウェアスタック、サービス)、展開形態別(オンプレミス、クラウド)、オペレーティングシステム分布別(ROS 1、その他)、ハードウェアアーキテクチャ対応別(x86、その他)、地域別に分類。市場予測は金額(米ドル)で提供されます。

地域別分析

アジア太平洋地域は、中国、日本、韓国における大規模な自動化投資により、2024年の世界収益の38%を占めました。上海のROSCon Chinaには200社以上が参加し、地域コミュニティの厚みを示しました。政府の資金援助が採用を加速:韓国のTech Valley補助金は、少量生産の電子機器工場向けのAI推論アクセラレータを引き受け、シンガポールのART Cテストベッドは先進的な3Dビジョンライブラリを試験的に導入しています。この地域のロボットオペレーティングシステム市場規模は、国内サプライヤーがASEANの製造コリドーに低コスト武器を拡大するにつれて、ペースを維持すると予測されます。

中東は2030年までのCAGRで最速の17.1%を記録します。サウジアラビアの「ビジョン2030」やUAEの「Operation 3000bn(3,000億作戦)」といった国家計画は、炭化水素からの転換を図るためにロボット工学に傾注しています。政府が支援するドバイの実証ゾーンでは規制遵守が簡素化され、倉庫ロボットや手術用ロボットの迅速な試験運用が可能になります。地域のシステムインテグレーターは欧州の部品メーカーと提携してサプライチェーンを現地化し、自給自足の目標を強化しています。

北米は依然としてイノベーションの核であり、ROSの中核的なメンテナとハイパースケールクラウドプロバイダを擁しています。ROS-Industrial Consortium Americasは、航空宇宙、石油・ガス、食品加工にまたがるメンバーにオープンソースの品質保証パイプラインを紹介しています。大学では、ベンチャーキャピタルを獲得するスピンオフに適応操作の研究を注ぎ込み、豊富な新興企業パイプラインを維持しています。需要は、リショアリング・イニシアチブと先端製造装置に対する税制優遇措置によってさらに後押しされています。

欧州では、産業用ロボットの密度が高く、サイバーセキュアなオートメーションが政府から義務付けられています。ドイツだけでも欧州の設置台数の3分の1があり、Industrie 4.0の枠組みの一部としてROSベースの改修を推進しています。スペインやハンガリーのような国々は、2024年に2桁のロボット在庫増加を記録しました。オーデンセで開催された調査では、デンマークのコボットメーカーとAI研究者を結びつけ、適応型ピックアンドプレース機能を商品化するための共同研究開発が強調されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 自動車組立ラインにおけるROS対応コボットの採用拡大(アジア)

- クラウドベースのシミュレーションプラットフォームの拡大(北米、欧州)

- 政府出資のロボティクス・テストベッドの急増(APACと中東)

- AMRのためのROS 2と5GおよびエッジAIの統合(グローバル)

- オープンソース産業用ライブラリ(ROS-Industrial)の急速な普及

- 長期サポート(LTS)ディストリビューションへのベンダーシフト

- 市場抑制要因

- 分散ROSネットワークにおけるサイバーセキュリティの脆弱性

- OEM間で細分化されたハードウェア抽象化レイヤー

- 新興市場におけるROS認定人材の希少性

- セーフティ・クリティカル・アプリケーションにおけるリアルタイム決定論の課題

- バリュー/サプライチェーン分析

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- ロボットタイプ別

- 産業用ロボット

- アーティキュレーテッド

- スカラ

- パラレル/デルタ

- カーテシアン/リニア

- 協働ロボット(コボット)

- サービスロボット

- プロフェッショナル・サービス・ロボット

- 物流ロボット

- ヘルスケア・医療ロボット

- 防衛・セキュリティロボット

- 農業用ロボット

- パーソナル・家庭用サービスロボット

- 産業用ロボット

- エンドユーザー業界別

- 自動車

- 電気・電子

- ヘルスケアとライフサイエンス

- eコマースと物流

- 航空宇宙および防衛

- 飲食品

- 農業

- 教育および調査

- その他(金属、プラスチックなど)

- コンポーネント別

- ソフトウェア・スタック

- コアROSライブラリ

- ミドルウェア/通信ツール

- シミュレーションと可視化(Gazebo、RViz)

- サービス

- システムインテグレーションとコンサルティング

- サポートとメンテナンス

- トレーニングと認定

- ソフトウェア・スタック

- OSディストリビューション別

- ROS 1

- ROS 2

- その他のバリエーション(ROS-Industrial、micro-ROS)

- 対応ハードウェアアーキテクチャ別

- x86

- ARM

- RISC-V、その他

- 展開モード別

- オンプレミス

- クラウドベース(ROS-aaS)

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- 北欧諸国

- スウェーデン

- ノルウェー

- デンマーク

- フィンランド

- アイスランド

- 中東

- GCC

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- その他アフリカ

- アジア太平洋地域

- 中国

- 日本

- 韓国

- インド

- インドネシア

- その他アジア太平洋地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Microsoft Corporation

- Amazon Web Services Inc.

- Clearpath Robotics Inc.

- KUKA AG

- Bosch Rexroth AG

- ABB Ltd.

- FANUC Corp.

- Yaskawa Electric Corp.

- Universal Robots A/S

- Open Robotics(Intrinsic)

- Wind River Systems Inc.

- Husarion Inc.

- Brain Corporation

- Neobotix GmbH

- PAL Robotics SL

- Locus Robotics Corp.

- Milvus Robotics

- iRobot Corporation

- Omron Corporation

- Siasun Robot & Automation

- Fetch Robotics(Zebra)

- Teradyne Mobility(AGV)