|

市場調査レポート

商品コード

1630214

固形/乾式潤滑油:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Solid/Dry Lubricants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 固形/乾式潤滑油:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

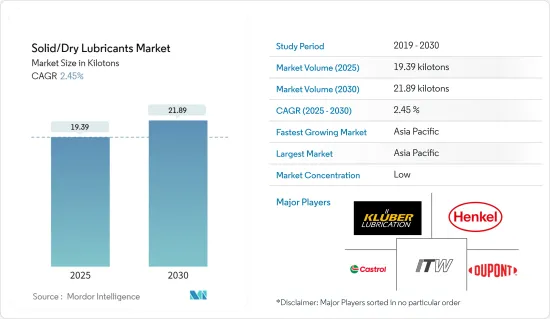

固形/乾式潤滑油市場規模は2025年に19.39キロトンと推定され、予測期間(2025~2030年)のCAGRは2.45%で、2030年には21.89キロトンに達すると予測されます。

COVID-19危機は世界の自動車供給産業に大きな影響を与え、ほとんどの地域で自動車の生産と販売の両方が突然停止しました。こうした作業停止により、世界中で数百万台の自動車生産が失われました。自動車産業は潤滑油市場に直接的な影響を及ぼします。しかし、市場の成長は着実に回復しています。2021年後半に規制が解除され、自動車やその他の建設活動が活発化したためです。

主要ハイライト

- 中期的には、アジア太平洋の製造業の成長と乾式潤滑剤におけるスプレー用途の需要拡大が、調査対象市場の成長を促進する重要な要因です。

- 一方、市場の成長を制限する要因としては、原料に関する政府の厳しい規制や、電気自動車(EV)の将来的な影響が控えめであることなどが挙げられます。これらは乾式潤滑油の需要に悪影響を及ぼすと予想されます。

- 技術の絶え間ない進歩と環境意識の高まりは、世界市場に有利な成長機会を間もなく生み出す可能性が高いです。

- アジア太平洋が市場を独占し、予測期間中に最も高いCAGRで推移する可能性が高いです。

固体潤滑剤の市場動向

自動車産業からの最大の消費

- 自動車産業は、コーティング剤にとって急成長しているセグメントのひとつです。自動車産業では、ユーザーエクスペリエンス向上のために先進的表面処理を行う傾向が強まっており、これが自動車産業における固体(乾式)潤滑剤の需要を押し上げています。

- 乾式潤滑剤は、ブレーキキャリパー、フルードデリバリーチューブ、ファスナー、タイロッドエンド、防振部品、ショックロッドに使用されています。また、ピストンリング、エンジンバルブ、自動車のドアハンドル、エンブレム、フロントグリル、メッキアルミホイール、燃料噴射ハウジングなどにも使用され、自動車に求められる耐摩耗性、耐摩擦性、耐腐食性を実現しています。

- Organisation Internationale des Constructeurs d'Automobiles(OICA)によると、世界の自動車生産台数は2022年に8,501万6,728台に達しました。前年のデータと比較すると、生産台数は5.9%増加しました。また、2021年と2022年の自動車生産台数の前年比成長率は6%でした。

- 同様に、OICAによると、2022年の商用車生産台数は5,749万台に達し、2021年の5,644万台と比較して成長を記録しました。

- 一方、米国商務省経済分析局によると、2022年の小型車小売販売台数は1,375万4,300台に達しました。2021年の1,494万6,900台と比較すると、最低生産台数を記録しました。

- さらに、Verband der Automobilindustrieによると、ドイツの自動車生産台数は2022年に340万台に達し、2021年の310万台と比較して9.6%の伸びを記録しました。

- 上記のような自動車の動向は、予測期間中に固形/乾式潤滑剤の需要を増加させる可能性が高いです。

アジア太平洋が市場を独占

- アジア太平洋が世界市場シェアを独占。アジア太平洋では、中国が最大の経済大国である、

- 自動車産業は、中国における固体(乾式)潤滑剤の主要な促進要因です。しかし、その成長はすべての市場で異なっています。乗用車市場は、施策的な債務超過と高基準が自動車市場低成長の主因となり、落ち込んでいます。

- 新興諸国では、中間所得層の増加、技術の進歩、自動車メーカーによる販売促進などにより、乗用車の需要が大幅に伸びています。

- Organisation Internationale des Constructeurs d'Automobiles(OICA)によると、近年、アジア太平洋が世界の自動車生産をリードしています。中国は国内最大の自動車生産国です。2022年、中国は2,384万台以上の乗用車を生産し首位を維持、次いで657万台の日本が続いた。

- China Association of Automobile Manufacturers(CAAM)によると、2022年、中国では乗用車が約2,356万台、商用車が約330万台販売されました。

- さらに、経済産業省の発表によると、日本の自動車産業では、2022年の自動車生産額が増加し、前年の約17兆6,500億円(12兆2,600億米ドル)に対し、19兆2,900億円(13兆3,900億米ドル)に達します。

- 上記の要因により、予測期間中に調査対象市場の需要が増加すると予想されます。

固形/乾式潤滑油産業概要

固形/乾式潤滑油市場は、その性質上、部分的にセグメント化されています。同市場の主要企業(順不同)には、Illinois Tool Works Inc.、Henkel AG &Co.KGaA、DuPont、CASTROL LIMITED、Kluber Lubricationなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- アジア太平洋における製造業の成長

- 乾式潤滑剤におけるスプレー用途の需要拡大

- その他の促進要因

- 抑制要因

- 原料に関する政府の厳しい規制

- 将来における電気自動車(EV)の影響はわずか

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模(数量ベース))

- タイプ

- 二硫化モリブデン(MoS2)

- PTFE

- 黒鉛

- ソフトメタル

- その他

- 最終用途

- 自動車

- 繊維

- 一般工業

- その他

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- その他の北米地域

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- ロシア

- その他の欧州

- その他

- 南米

- 中東

- アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Anti-Seize Technology

- CASTROL LIMITED

- Curtiss-Wright Surface Technologies(CWST)

- DuPont

- ENDURA PLATING TECHNOLOGY

- Henkel AG & Co. KGaA

- Illinois Tool Works Inc.

- Kluber Lubrication

- Lubrication Engineers

- Metal Coatings

- Sandstrom Products Company

- SCCS Industries LLC.(DYNACRON)

- SKF

- Slickote Coatings

- Sun Coating Company

- The B'laster Corporation

- WEICON GmbH & Co. KG

第7章 市場機会と今後の動向

- 技術の絶え間ない進歩環境意識の高まり

- その他の機会

The Solid/Dry Lubricants Market size is estimated at 19.39 kilotons in 2025, and is expected to reach 21.89 kilotons by 2030, at a CAGR of 2.45% during the forecast period (2025-2030).

The COVID-19 crisis heavily impacted the global automotive supply industry, as both the production and sales of motor vehicles came to a sudden halt in most regions. These work stoppages led to a loss in the production of millions of vehicles across the world. The automobile industry comes with a direct effect on the lubricants market. However, the market growth picked up steadily. It is owing to increased automotive and other construction activities after the lifting of restrictions in the second half of 2021.

Key Highlights

- Over the medium term, the growing manufacturing industry in Asia-Pacific and growing demand for spray application in dry lubricants are significant factors driving the growth of the market studied.

- On the other hand, factors limiting the growth of the market include stringent government regulations on raw materials and the modest impact of electric vehicles (EVs) in the future. These are expected to come with a negative influence on the demand for dry lubricants.

- Nevertheless, the continuous advancements in technology and increasing environmental consciousness are likely to create lucrative growth opportunities for the global market soon.

- Asia-Pacific region is expected to dominate the market and is also likely to witness the highest CAGR during the forecast period.

Solid Dry Lubricants Market Trends

Largest consumption from Automotive Industry

- The automotive segment is one of the rapidly growing segments for these coatings. The growing trend of advanced surface engineering in the automotive industry for better user experience is boosting the demand for solid (dry) lubricants in the automotive industry.

- Dry lubricants are used in brake calipers, fluid delivery tubes, fasteners, tie rod-ends, anti-vibration components, and shock rods. It is also used in piston rings, engine valves, car door handles, emblems, front grills, plated aluminum wheels, and fuel injection housing, among others, to achieve the desired wear, friction, and corrosion resistance in vehicles.

- According to the International Organization of Motor Vehicle Manufacturers (OICA), global motor vehicle production reached 85,016,728 units in 2022. The production increased by 5.9% when compared to the previous year's data. Also, motor vehicle production growth year-on-year between 2021 and 2022 markets was at 6%.

- Similarly, as per OICA, commercial vehicle production reached 57.49 million units in 2022 and registered growth when compared to 56.44 in 2021.

- Meanwhile, as per the Bureau of Economic Analysis of the United States Department of Commerce, light vehicle retail sales reached 13,754.3 thousand units. It registered the lowest production when compared to 14,946.9 thousand units in 2021.

- Further, according to the German Association of the Automotive Industry (Verband der Automobilindustrie), automobile production in Germany reached 3.4 million in 2022 and registered a growth of 9.6% when compared to 3.1 million in 2021.

- The trends mentioned above in automotive are likely to increase the demand for solid/dry lubricants in the market during the forecast period.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region dominated the global market share. In Asia-Pacific, China is the largest economy,

- The automotive industry is the major driving factor for solid (dry) lubricants in China. However, the growth is different for all markets. The passenger car market is down due to policy overdrafts and high base, which became the main factors for the low growth of the automobile market.

- In developing countries, the demand for passenger cars is significantly increasing due to the growth in middle-class incomes, technology, and sales promotions provided to people by automobile manufacturers.

- According to the Organisation Internationale des Constructeurs d'Automobiles (OICA), Asia-Pacific has led global automobile production in recent years. China is the largest producer of automobiles in the country. In 2022, china produced over 23.84 million units of passenger cars and remained at the top, followed by Japan with 6.57 million units.

- According to the China Association of Automobile Manufacturers(CAAM), in 2022, approximately 23.56 million passenger cars and 3.3 million commercial vehicles were sold in China.

- Additionally, as per the Ministry of Economy, Trade and Industry (METI), the Japanese automotive industry saw a rise in the production value of motor vehicles in 2022, reaching JPY 19.29 trillion (USD 13.39 trillion), compared to approximately JPY 17.65 trillion (USD 12.26 trillion) in the preceding year.

- The factors above are expected to increase the demand for the market studied during the forecast period.

Solid Dry Lubricants Industry Overview

The solid/dry lubricants market is partially fragmented in nature. Some of the major players in the market (not in any particular order) include Illinois Tool Works Inc., Henkel AG & Co. KGaA, DuPont, CASTROL LIMITED, and Kluber Lubrication, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Manufacturing Industry in Asia-Pacific

- 4.1.2 Growing Demand for Spray Application in Dry Lubricants

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Government Regulations on Raw Materials

- 4.2.2 Modest Impact of Electric Vehicles (EVs) in the Future

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Molybdenum Disulfide (MoS2)

- 5.1.2 PTFE

- 5.1.3 Graphite

- 5.1.4 Soft Metals

- 5.1.5 Other Types

- 5.2 End-use

- 5.2.1 Automotive

- 5.2.2 Textile

- 5.2.3 General Industrial Manufacturing

- 5.2.4 Others

- 5.3 Geography

- 5.3.1 Asia Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Rest of North America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle East

- 5.3.4.3 Africa

- 5.3.1 Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Anti-Seize Technology

- 6.4.2 CASTROL LIMITED

- 6.4.3 Curtiss-Wright Surface Technologies (CWST)

- 6.4.4 DuPont

- 6.4.5 ENDURA PLATING TECHNOLOGY

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 Illinois Tool Works Inc.

- 6.4.8 Kluber Lubrication

- 6.4.9 Lubrication Engineers

- 6.4.10 Metal Coatings

- 6.4.11 Sandstrom Products Company

- 6.4.12 SCCS Industries LLC.(DYNACRON)

- 6.4.13 SKF

- 6.4.14 Slickote Coatings

- 6.4.15 Sun Coating Company

- 6.4.16 The B'laster Corporation

- 6.4.17 WEICON GmbH & Co. KG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Continuous Advancements in Technology Increasing Environmental Consciousness

- 7.2 Other Opportunities