難燃性コーティング:市場シェア分析、産業動向と統計、成長予測(2025~2030年)

Fire Retardant Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1630198

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

難燃性コーティング市場は予測期間中に5%を超えるCAGRで推移する見込み

COVID-19パンデミックは、閉鎖、社会的距離、貿易制裁が世界サプライチェーンネットワークに大規模な混乱を引き起こしたため、市場の妨げとなりました。建設産業は活動の停止により衰退を目の当たりにしました。しかし、この状況は2021年には回復し、予測期間中は市場に利益をもたらすと予想されます。

主要ハイライト

- 市場調査の主要促進要因は、世界の建設活動の増加と石油・ガス探査活動の成長です。

- しかし、用途によっては低コストの代替品が入手可能であることが市場の成長を妨げています。

- シェールガス生産量の大幅な増加は、中国、インドなどの国での消費が最も多い世界市場にとって好機となる可能性が高いです。

難燃性コーティング市場の動向

建築・建設産業からの需要拡大

- アジア太平洋や北米地域におけるインフラプロジェクトの急増により、建築・建設産業が圧倒的なシェアを占めています。

- 難燃性コーティングは、火災が引き起こす被害の程度を軽減し、火災の発生を未然に防ぐために建設産業で使用されています。防火対策には、火災が人や財産に与える影響を最小限に抑えるための構造的・運用的システムを設置・使用することが含まれます。

- 土木学会によると、2025年までに中国、インド、米国が建設セクターの世界的成長の60%近くを占めると予想されており、難燃性コーティングの市場成長率を高めています。

- 米国は世界でもトップクラスの建設市場です。米国国勢調査局によると、2021年の米国の建設は1兆5,800億米ドルと評価され、同国の総GDPの約4.3%を占めています。

- 米国国勢調査局によると、2021年12月の建築許可による民間住宅総戸数は187万3,000戸で、11月の改定値171万7,000戸を9.1%上回った。2021年の建築許可件数は172万4,700戸と推定され、前年の147万1,100戸を17.2%上回った。

- 噴気性コーティングは主に受動的防火に使用されます。このコーティングは熱を加えると元の厚さの何倍にも膨張し、断熱炭化物を形成して、露出した構造用鋼やシートロックなどの下地を保護します。

- 溶剤系または水性の薄膜コーティングシステムは、30分、60分、90分の耐火性が要求される建物の防火に使用されます。難燃性コーティングの需要は、建設支出に大きく左右されます。

- 米国で現在進行中の最も高額な建設プロジェクトには、デトロイトのハドソンズ開発(10億米ドル)、ニューヨークのワン・ヴァンダービルト(31億4,000万米ドル)、DHSの国境の壁長期戦略(150億米ドル)、地下鉄2番街第3期プロジェクト(MTA-ニューヨーク市交通局)(142億米ドル)、ゲートウェイ・ハドソン・トンネルプロジェクト(127億米ドル)、JFK国際空港の拡大・改修(130億米ドル)などがあります。

- したがって、上記の要因は今後数年間、難燃剤市場に大きな影響を与えると予想されます。

アジア太平洋が最も急成長

- アジア太平洋は、難燃性コーティングの市場として最も急成長しています。難燃性コーティングは建設現場で消費され、市場の成長を牽引しています。

- 難燃性コーティングは、可燃・不燃を問わず、さまざまな製品を火災から守るために必要とされることが多いです。難燃性コーティングは、材料の本質的な性質を変えることなく、あらゆる表面に塗布する最も古く、最も効率的で、最も簡単な方法です。

- 中国、インド、ベトナムなどのアジア太平洋諸国は、建設活動の力強い成長を記録しており、予測期間中にこの地域における炭酸バリウムの消費を促進すると期待されています。

- 米国国際貿易局によると、中国は世界最大の建設市場であり、2030年まで年平均8.6%の成長が予測されています。国家開発改革委員会(NDRC)によると、中国は今後5年間(2025年)の主要建設プロジェクトに1兆4,300億米ドルを投資します。上海の計画には今後3年間で387億米ドルの投資が含まれており、広州は80億9,000万米ドルを投資する16の新規インフラプロジェクトに調印しました。

- インドでは、2021年3月に建設開発部門が260億8,000万米ドル、活動が247億2,000万米ドルとなりました。2022年、インドは、万人向け住宅、スマートシティ計画など、インフラ開発や手頃な価格の住宅における政府の取り組みにより、建設産業に約6,400億米ドルを貢献しました。同国における建設活動の拡大が、予測期間中の難燃性コーティング市場を牽引しています。

- インドネシアでは、国家中期開発計画(RPJMN 2020~2024)の下、政府は国内の交通、産業、エネルギー、住宅インフラプロジェクトの開発に4,120億米ドルを投資する計画であり、これが難燃性コーティング市場を後押しする可能性があります。

- インドネシア統計局(BPS)によると、2021年の同国の建設セクターのGDPは1,770億米ドルでした。さらに、World Cementのデータによると、インドネシアの建設市場は2022年に7.2%の成長を記録しました。

- 日本の財務省によると、日本の建設産業の2021年度の売上高は約1兆2,200億米ドルで、前年同期比2.1%の増加を記録しました。

- したがって、上記の要因は、今後数年間、アジア太平洋における難燃性コーティングの需要を押し上げると予想されます。

難燃性コーティング産業概要

難燃コーティング市場は統合されています。主要参入企業としては、3M、Akzo Nobel N.V.、RPM International Inc、PPG Industries, Inc、The Sherwin-Williams Companyなどが挙げられる(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 世界の建設活動の増加

- 石油・ガス探査活動の成長

- 抑制要因

- 低コストの代替品の入手可能性

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- 樹脂タイプ

- シリコーン

- エポキシ

- アクリル

- ビニール

- その他

- 技術

- 水性

- 溶剤型

- 粉体コーティング

- その他

- コーティングタイプ

- 浸透性コーティング

- セメント系コーティング

- エンドユーザー産業

- 建築・建設

- 電力

- 運輸

- 石油・ガス

- その他

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア分析

- 主要企業の戦略

- 企業プロファイル

- 3M

- Akzo Nobel N.V.

- Albi Protective Coatings

- Benjamin Moore & Co

- Carboline

- Contego International Inc.

- Hempel AS

- Isolatek International

- Jotun

- No-Burn, Inc.

- PPG Industries, Inc.

- RPM International Inc

- The Sherwin-Williams Company

- TREMCO ILLBRUCK

第7章 市場機会と今後の動向

- シェールガス生産の大幅な増加

- その他の機会

目次

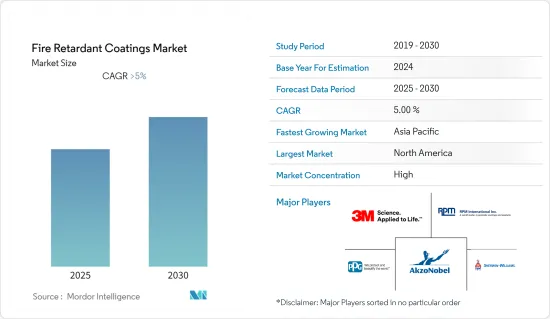

The Fire Retardant Coatings Market is expected to register a CAGR of greater than 5% during the forecast period.

The COVID-19 pandemic hampered the market, as lockdowns, social distances, and trade sanctions triggered massive disruptions to global supply chain networks. The construction industry witnessed a decline due to the halt in activities. However, the condition recovered in 2021 and was expected to benefit the market during the forecast period.

Key Highlights

- Major factors driving the market studied are increasing construction activities globally and growth in oil & gas exploration activities.

- However, the availability of low-cost alternatives for some applications hinders the market's growth.

- The strong rise in shale gas production will likely act as an opportunity for the markeglobal marketed the market across the globe with the largest consumption in a country such as China, India, etc.

Fire Retardant Coatings Market Trends

Growing Demand from Building & Construction Industry

- The building and construction industry is the dominating segment, owing to the escalation in infrastructure projects in Asia-Pacific and North American regions.

- Fire retardant coatings are used in the construction industry to reduce the extent of damage that a fire can cause and help to avert one from breaking out in the first place. Fire protection involves installing and using structural and operational systems to minimize the impact of fire on people and property.

- According to the Institution of Civil Engineers, China, India, and the United States are expected to account for almost 60% of all global growth in the construction sector by 2025, thus increasing the market growth of fire retardant coatings.

- The United States was among the top construction markets globally. Per the United States Census Bureau, in 2021, construction in the United States was valued at USD 1.58 trillion, accounting for around 4.3% of the country's total GDP.

- According to the US Census Bureau, the total privately owned housing units authorized by building permits in December 2021 were 1,873,000, 9.1% more than the revised rate of 1,717,000 in November. In 2021, an estimated 1,724,700 housing units were authorized by building permits, 17.2% more than 1,471,100 in the previous year.

- Intumescent coatings are mostly used in passive fire protection. Intumescent coatings are typically water-based, solvent-based, or epoxy-based paint-like materials, which expand by many times their original thickness when heated to form an insulating char to protect the substrate, such as exposed structural steel or sheetrock, in the event of fire accidents.

- Solvent-based or water-based thin film coating systems are used for fire protection in buildings with a resistance requirement of 30, 60, and 90 minutes. The demand for intumescent coatings is majorly dependent on construction spending.

- Some of the most expensive construction projects in the United States, which are currently underway, are Hudson's Development, Detroit (USD 1 billion), One Vanderbilt, New York (USD 3.14 billion), DHS border wall long-term strategy (USD 15 billion), phase 3 of the second avenue subway project - MTA - New York city transit (USD 14.2 billion), gateway Hudson tunnel project (USD 12.7 billion), and JFK international airport expansion and renovations (USD 13 billion).

- Therefore, the factors above are expected to impact the fire retardant market in the coming years significantly.

Asia-Pacific Region to Exhibit the Fastest Growth

- The Asia-Pacific region stands to be the fastest-growing market for fire retardant coatings. Consumption of these coatings in construction activities drives the market's growth.

- Fire retardant coatings are often required to protect a wide range of products bo,th flammable and nonflammable, against fire. It is the oldest, most efficient, and easiest method to apply any surface without modifying the intrinsic properties of materials.

- Asia-Pacific countries, such as China, India, and Vietnam, have been registering strong growth in construction activities, which is expected to drive the consumption of barium carbonate in the region over the forecast period.

- As per U.S. International Trade Administration, China is the world's largest construction market and is forecasted to grow at an annual average rate of 8.6% till 2030. According to National Development and Reform Commission (NDRC), China is investing USD 1.43 trillion in major construction projects in the next five years, 2025. The Shanghai plan includes an investment of USD 38.7 billion in the next three years, whereas Guangzhou signed 16 new infrastructure projects with an investment of USD 8.09 billion.

- In India, the construction development sector and activities stood at USD 26.08 billion and USD 24.72 billion, respectively, in March 2021. In 2022, India contributed about USD 640 billion to the construction industry due to government initiatives in infrastructure development and affordable housing, such as housing to all, smart city plans, etc. The growing construction activities in the country are driving the fire retardant coatings market over the forecast period.

- In Indonesia, under the National Medium-term Development Plan (RPJMN 2020-2024), the government plans to invest USD 412 billion in the development of transport, industrial, energy, and housing infrastructure projects in the country, which may help boost the fire retardant coatings market.

- As per Statistics Indonesia (BPS), in the year 2021, the GDP of the construction sector in the country was USD 0.177 trillion. Furthermore, as per the data by World Cement, the Indonesian construction market recorded a growth of 7.2% in 2022.

- According to the Ministry of Finance of Japan, the construction industry in Japan generated sales of approximately USD 1.22 trillion in the fiscal year 2021, registering an increase of 2.1% compared to the same period last year.

- Therefore, the factors above are expected to boost the demand for fire retardant coatings in the Asia-Pacific region in the coming years.

Fire Retardant Coatings Industry Overview

The Fire Retardant Coatings Market is consolidated. Some major players include (not in a particular order) 3M, Akzo Nobel N.V., RPM International Inc, PPG Industries, Inc., and The Sherwin-Williams Company, amongst others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Construction Activities Across the Globe

- 4.1.2 Growth in Oil & Gas Exploration Activities

- 4.2 Restraints

- 4.2.1 Availability of Low-Cost Alternatives

- 4.2.2 Other Restraints

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Resin Type

- 5.1.1 Silicone

- 5.1.2 Epoxy

- 5.1.3 Acrylic

- 5.1.4 Vinyl

- 5.1.5 Other Resin Types

- 5.2 Technology

- 5.2.1 Water-borne

- 5.2.2 Solvent-borne

- 5.2.3 Powder Coatings

- 5.2.4 Others

- 5.3 Coating Type

- 5.3.1 Intumescent Coating

- 5.3.2 Cementitious Coating

- 5.4 End-user Industry

- 5.4.1 Building & Construction

- 5.4.2 Power

- 5.4.3 Transportation

- 5.4.4 Oil & Gas

- 5.4.5 Others

- 5.5 Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 Italy

- 5.5.3.4 France

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East & Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East & Africa

- 5.5.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 Albi Protective Coatings

- 6.4.4 Benjamin Moore & Co

- 6.4.5 Carboline

- 6.4.6 Contego International Inc.

- 6.4.7 Hempel AS

- 6.4.8 Isolatek International

- 6.4.9 Jotun

- 6.4.10 No-Burn, Inc.

- 6.4.11 PPG Industries, Inc.,

- 6.4.12 RPM International Inc

- 6.4.13 The Sherwin-Williams Company

- 6.4.14 TREMCO ILLBRUCK

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Strong Rise in Shale Gas Production

- 7.2 Other Opportunities

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日