|

|

市場調査レポート

商品コード

1630186

透明導電性フィルム:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Transparent Conductive Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 透明導電性フィルム:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

透明導電性フィルム市場の予測期間中のCAGRは8%以下と予測されます。

COVID-19の発生により、世界中で全国的なロックダウン、製造活動やサプライチェーンの混乱、生産停止が発生し、2020年の市場にマイナスの影響を与えました。しかし、2021年には状況が回復し始め、市場の成長軌道が回復しました。

主要ハイライト

- 市場成長を牽引する主要要因としては、民生用電子機器産業からの需要増加や太陽光発電産業の成長拡大が挙げられます。

- その反面、酸化インジウムスズの高コストとCOVID-19の市場全体への影響から生じる不利な状況が、調査対象市場の成長を阻害すると予想されます。

- 透明導電性フィルム生産における技術の進歩は、まもなくメーカーに数多くの機会を提供すると予想されます。

- アジア太平洋が世界市場を独占し、中国、韓国、日本などの国からの需要が大半を占めています。

透明導電フィルム市場動向

ガラス上の酸化インジウムスズ(ITO)が市場を独占する

- インジウムスズ酸化物は、インジウム、スズ、酸素を様々な割合で含む三元組成物であり、酸素の含有量によって合金またはセラミックと表現されます。インジウム錫酸化物の調製には、ほぼ45%のインジウムが使用されます。

- 光学的透明性と電気伝導性により、透明導電性酸化物として広く使用されており、薄膜として成膜することができます。

- ガラス上のインジウムスズ酸化物は透明性が高く、優れた導電性を有します。可視域から近赤外域まで優れた光透過性を示します。

- ガラス上のインジウムスズ酸化物は、微細な粗さが小さく、電気的表面抵抗の均一性に優れ、赤外波長に対する反射率が高く、塗膜の密着性や耐摩耗性に優れ、光透過率の均一性が高いなどの優れた特性を有しており、熱伝導性フィルムに最適です。

- ガラス上の酸化インジウムスズには、LEDやOLEDディスプレイ、微細構造化用途、加熱可能な顕微鏡スライド、医療技術用カバーリップなど様々な用途があります。また、エレクトロニクス用の回路基板、タッチスクリーンやタッチセンシティブ・ディスプレイ技術用の光学と導電性透明コーティング、透明電極用の導電性コーティング、有機太陽電池、赤外線ミラー、反射型赤外線フィルター、除氷ウィンドウ、有機LED(OLED)用アノードとしても応用できます。

- ガラス基板用のITO薄膜は、省エネのためにガラス窓に使用されることが多くなっています。

- しかし、酸化インジウム・コーティングは、酸素または空気雰囲気中で、300°Fまたは150°Cを超える温度にさらされ続けることは推奨されません。ITOは脆く、柔軟性に欠け、製造プロセスには高温と真空が伴う。そのため、比較的時間がかかり、費用対効果も低いため、今後数年間はガラスフィルム上のITOの需要が減少する可能性が高いです。

- さらに、ITO膜の主材料であるインジウムはレアメタルであり、偏在しています。そのため、価格上昇の問題だけでなく、安定供給の面でもリスクがあります。

- 社団法人電子情報技術産業協会(JEITA)によると、世界のエレクトロニクス・IT産業の生産額は、2021年の3兆3,602億米ドルに対し、2022年は3兆4,368億米ドルと推定され、前年比1%の成長率を記録しました。さらに、2023年には前年比3%の成長率で3兆4,368億米ドルに達すると予想されています。

- 世界的に、スマートフォンの需要は著しく増加しています。Telefonaktiebolaget LM Ericssonによると、世界のスマートフォン契約数は2021年の62億5,900万から2027年には76億9,000万に達すると推定されています。この要因は、エレクトロニクスから透明導電性フィルムを使用するための有利な需要を支えると考えられます。

- 金属ナノワイヤグリッド、導電性ポリマー、カーボンナノチューブ、グラフェンなど、高速性能を実現するためにシート抵抗の低い透明導電性酸化物の開発が盛んに行われているが、今後数年間はその特性からITOベースのフィルムに大きな需要があると予測されます。

アジア太平洋市場を独占する中国

- 中国はPPP(購買力平価)ベースで世界最大の経済大国です。しかし、名目GDPで計算すると第2位の経済大国です。同国の成長はここ数年鈍化しており、2019年のGDP成長率は6%を記録したが、これは1990年以降の同国の経済史上最も遅い成長率です。中国経済の成熟化と米国との貿易摩擦をめぐる緊張により、この成長率は緩やかになっています。

- 透明導電性フィルムに対するエレクトロニクス産業からの需要も、射出成形によってエレクトロニクス産業のニーズに合った多様な形態の製品や複雑なモデルを生産できるという利点から、非常に高いです。中国は世界最大のエレクトロニクス生産基地です。中国は、スマートフォン、テレビ、電線、ケーブル、ポータブルコンピューティングデバイス、ゲームシステム、その他のパーソナルデバイスなどのエレクトロニクス製品を積極的に生産しています。

- 継続的な所得増加の結果、国民の1人当たり可処分所得が上昇し、これが中国の電子製品需要に恩恵をもたらすと予想されます。中間所得層と高所得層が拡大することで、電子機器に対する需要が促進されると予想されます。中国国家統計局によると、民生用電子機器・民生用電子機器セグメントの売上高は年間2.04%の成長率を示し、2025年には1,756億7,000万米ドルの市場規模になると予測されています。

- 中国は、広範な需要シナリオから利益を得るため、「メイド・イン・チャイナ2025」計画のような戦略的イニシアティブに着手しました。この計画の下、中国政府は2030年までに生産高3,050億米ドルを達成し、国内需要の80%を満たすという目標を発表しました。

- スマートフォン市場と同様の動向は、ノートパソコン市場でも見られます。生産シフトはスマートフォンほど急激ではないが、多くのノートパソコン・メーカーが生産拠点を中国から移すことを計画しています。HPは、生産能力のほぼ3分の1を中国から他のアジア諸国に移す計画です。

- 中国はまた、電源構成に占める太陽エネルギーの割合を劇的に増やそうとしています。予測期間中、同国では透明導電性フィルムに莫大な需要が見込まれます。

- しかし、COVID-19は中国のエレクトロニクス需要を縮小させ、この動向は予測期間中、パンデミック後も続くと予想されます。このような要因により、この産業の透明導電性フィルムの需要は鈍化すると予想されます。

透明導電性フィルム産業概要

世界の透明導電性フィルム市場はセグメント化されており、複数の世界メーカーと地域メーカーが存在します。市場の主要企業には、Nitto Denko Corporation、OIKE &、Teijin Limited、Sekisui Nano Coat Technology、OFILM Groupなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 民生用電子機器産業からの需要増加

- 太陽光発電産業の成長促進

- 抑制要因

- 酸化インジウムスズの高コスト

- COVID-19の発生による不利な状況

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- 材料タイプ

- ガラス上の酸化インジウムスズ(ITO)

- PET上の酸化インジウムスズ(ITO)

- 銀ナノワイヤ

- カーボンナノチューブ

- 導電性ポリマー

- その他の材料タイプ

- 用途セグメント

- スマートフォン

- タブレット

- ノートパソコン

- LCDとLEDモニターとテレビ

- ウェアラブルデバイス

- OLED照明

- 太陽光発電

- その他

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- その他の北米

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Abrisa Technologies

- C3Nano

- Cambrios Technologies Corp.

- Canatu OY

- Eastman Kodak Company

- FUJIFILM corporation

- Gunze

- Hitachi Chemical Co. Ltd

- MNTech

- Nano-C

- NITTO DENKO CORPORATION

- OFILM GROUP CO., LTD.

- OIKE & Co. Ltd

- SEKISUI CHEMICAL CO.,LTD

- TDK Corporation

- TEIJIN LIMITED

- TORAY ADVANCED FILM CO. LTD

- TOYOBO Co.,LTD.

第7章 市場機会と今後の動向

- 透明導電性フィルム生産における技術進歩

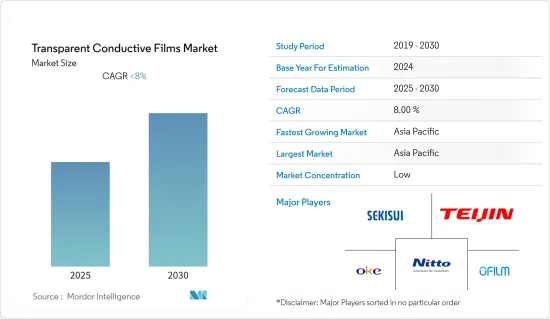

The Transparent Conductive Films Market is expected to register a CAGR of less than 8% during the forecast period.

Due to the COVID-19 outbreak, nationwide lockdowns worldwide, disruption in manufacturing activities and supply chains, and production halts negatively impacted the market in 2020. However, the conditions started recovering in 2021, restoring the market's growth trajectory.

Key Highlights

- The major factors driving the studied market's growth include increasing demand from the consumer electronics industry and augmenting growth in the photovoltaic industry.

- On the flip side, the high cost of indium tin oxide and unfavorable conditions arising from COVID-19's impact on the overall market is expected to hinder the studied market's growth.

- Technological advancements in the transparent conductive film production are expected to offer numerous opportunities for manufacturers shortly.

- Asia-Pacific dominated the global market, with most demand coming from countries such as China, South Korea, and Japan.

Transparent Conductive Films Market Trends

Indium Tin Oxide (ITO) on Glass to Dominate the Market

- Indium tin oxide is a ternary composition of indium, tin, and oxygen in various proportions, and depending upon the oxygen content, it can be described as an alloy or a ceramic. In preparation of indium tin oxide, almost 45% of indium is used.

- It is widely used as transparent conducting oxide owing to its optical transparency and electrical conductivity, and it can be deposited as a thin film.

- Indium tin oxide on glass is highly transparent and possesses excellent electrical conductivity. It offers excellent light transmittance from the visible to the near-infrared range.

- Superior properties of indium tin oxide on glass, such as low micro roughness, excellent homogeneity of the electrical surface resistance, reflection for infrared wavelengths, excellent coating adhesion and abrasion resistance, and high uniformity of optical transmittance, making it ideal for thermal conductive films.

- Indium tin oxide on glass includes various applications such as LED and OLED displays, micro structuring applications, heat-able microscope slides, and coverslips for medical technology. It can also be applied as circuit substrates for electronics, optical and conductive transparent coatings for touch screen and touch-sensitive display technology, conductive coatings for transparent electrodes, organic solar cells, infrared mirrors, reflective infrared filters, de-icing windows and anodes for organic LEDs (OLED).

- ITO thin films for glass substrates are increasingly used in glass windows to conserve energy.

- However, indium oxide coatings are not recommended for continued exposure to temperatures more than 300°F or 150°C in oxygen or air atmospheres, which may result in undesired changes in resistivity. ITO is considered brittle, lacks flexibility, and the fabrication process involves high temperatures and a vacuum. Therefore, it is relatively slow and not cost-effective, likely decreasing the demand for ITO on glass films in the coming years.

- Moreover, indium, the main material of ITO films, is a rare metal and unevenly distributed. Therefore, there is a risk in terms of stable supply, as well as the issue of increasing prices.

- According to the Japan Electronics and Information Technology Industries Association (JEITA), the production by the global electronics and IT industry was estimated at USD 3,436.8 billion in 2022, registering a growth rate of 1% year on year, compared to USD 3,360.2 billion in 2021. Moreover, the industry is expected to reach USD 3,436.8 billion, with a growth rate of 3% year on year, by 2023.

- Globally, the demand for smartphones is increasing at a significant rate. According to the Telefonaktiebolaget LM Ericsson, the number of smartphone subscriptions globally was estimated to reach 7,690 million by 2027 from 6,259 million in 2021. This factor will support the favorable demand for using transparent conductive films from electronics applications.

- While there is significant work on thin metal nanowire grids, conductive polymers, carbon nanotubes, and graphene to develop transparent conducting oxides with lower sheet resistances for higher speed performance, projections still suggest a significant demand for ITO based films owing to its properties in the coming years.

China to Dominate the Asia-Pacific Market

- China is the world's largest economy in terms of PPP (purchasing power parity). However, when calculated in terms of nominal GDP, it is the second-largest economy. The country's growth slowed in the past few years, and it recorded 6% GDP growth in 2019, the slowest rate in the country's economic history since 1990. This growth rate is moderating due to the maturing of China's economy and tensions over the country's trade disputes with the United States.

- The demand for transparent conductive films from the electronics industry is also very high owing to the advantage of producing versatile shape products and complex models using injection molding that fits the electronics industry's needs. China is the largest base for electronics production in the world. China is actively manufacturing electronic products, such as smartphones, TVs, wires, cables, portable computing devices, gaming systems, and other personal devices.

- The continuous income growth resulted in a rise in the population's per capita disposable income, which is expected to benefit the demand for electronic goods in China. The expansion of the middle and high-income populations is expected to propel the demand for electronics. According to the National Bureau of Statistics of China, the revenue in the consumer electronics and household appliances segment is expected to show an annual growth rate of 2.04%, resulting in a projected market volume of USD 175,670 million by 2025.

- China embarked on strategic initiatives like the 'Made in China 2025' plan to benefit from the extensive demand scenario. Under this, the Chinese government announced its goal to reach an output of USD 305 billion by 2030 and meet 80% of its domestic demand.

- A similar trend as that in the smartphone market is also observed in the laptop market. The production shift is less drastic than that of smartphones, but many laptop manufacturers are planning to move their manufacturing bases out of China. HP is planning to move almost one-third of its capacity from China to other Asian countries.

- China is also looking to dramatically increase the proportion of solar energy in its power mix. It is expected to create a huge demand for transparent conductive films in the country during the forecast period.

- However, COVID-19 downsized the demand for electronics in China, and this trend is expected to continue even after the pandemic during the forecast period. Such factors are expected to slow down this industry's demand for transparent conductive films.

Transparent Conductive Films Industry Overview

The global transparent conductive films market is fragmented, with several global and regional manufacturers. Some key players in the market include Nitto Denko Corporation, OIKE & Co., Ltd., Teijin Limited, Sekisui Nano Coat Technology, and OFILM Group Co., Ltd., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from Consumer Electronics Industry

- 4.1.2 Augmenting Growth in Photovoltaic Industry

- 4.2 Restraints

- 4.2.1 High Cost of Indium Tin Oxide

- 4.2.2 Unfavorable Conditions Arising Due to COVID-19 Outbreak

- 4.3 Industry Value-chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Material Type

- 5.1.1 Indium Tin Oxide (ITO) on Glass

- 5.1.2 Indium Tin Oxide (ITO) on PET

- 5.1.3 Silver Nanowire

- 5.1.4 Carbon Nanotubes

- 5.1.5 Conductive Polymers

- 5.1.6 Other Material Types

- 5.2 Application

- 5.2.1 Smartphones

- 5.2.2 Tablets

- 5.2.3 Laptops and Notebooks

- 5.2.4 LCD and LED Monitors and TVs

- 5.2.5 Wearable Devices

- 5.2.6 OLED Lighting

- 5.2.7 Solar Photovoltaic

- 5.2.8 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.2.4 Rest of North America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Abrisa Technologies

- 6.4.2 C3Nano

- 6.4.3 Cambrios Technologies Corp.

- 6.4.4 Canatu OY

- 6.4.5 Eastman Kodak Company

- 6.4.6 FUJIFILM corporation

- 6.4.7 Gunze

- 6.4.8 Hitachi Chemical Co. Ltd

- 6.4.9 MNTech

- 6.4.10 Nano-C

- 6.4.11 NITTO DENKO CORPORATION

- 6.4.12 OFILM GROUP CO., LTD.

- 6.4.13 OIKE & Co. Ltd

- 6.4.14 SEKISUI CHEMICAL CO.,LTD

- 6.4.15 TDK Corporation

- 6.4.16 TEIJIN LIMITED

- 6.4.17 TORAY ADVANCED FILM CO. LTD

- 6.4.18 TOYOBO Co.,LTD.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements in Transparent Conductive Films Production