|

市場調査レポート

商品コード

1630181

高機能合金-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)High Performance Alloys - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 高機能合金-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

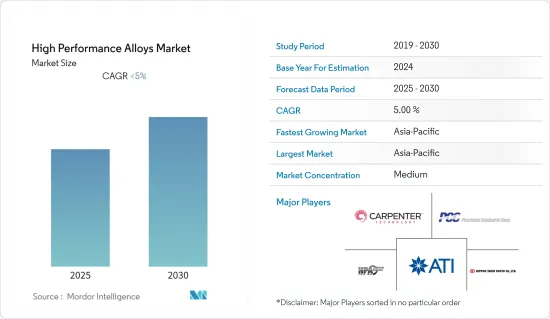

高性能合金市場の予測期間中のCAGRは5%以下と予想されます。

COVID-19期間中、世界各地で政府の閉鎖措置がとられ、エンドユーザーの操業がしばらく停止しました。これは航空宇宙産業、電力産業、石油・ガス産業に大きな影響を及ぼし、高性能合金市場にも同様に影響を及ぼしました。しかし、パンデミック後は産業が回復し、市場は今後数年間も成長軌道を維持すると予想されます。

主要ハイライト

- 航空宇宙産業の合金に対するニーズの高まりが、市場を成長させている主要要因です。

- しかし、原料の価格変動が市場成長の妨げになる可能性が高いです。

- 非鉄金属は他タイプの材料よりも優れているため、その需要の急増は市場にとって好機となりそうです。

- アジア太平洋は市場で最大のシェアを占めており、今後数年間もその傾向が続くと予想されます。

高性能合金市場の動向

航空宇宙産業が市場を独占する

- 高性能合金は、その高い機械的強度、高い表面安定性、耐食性により、航空宇宙、石油・ガス、自動車などの産業で様々な用途に使用されています。しかし、航空宇宙産業における機器の軽量化需要の増加や新世代航空機の需要の急増が、市場を前進させる可能性が高いです。

- 次世代航空機、回転翼機、無人航空機、ミサイルは、軽量化、視覚、熱シグネチャ、高速化、操縦性などの点でより厳しい要件が課されることになります。このような要求から、これらの機能性を取り入れることができる高性能合金の必要性が高まっている

- 国際航空運送協会(IATA)の推定によると、民間航空会社の世界売上高は、2021年の4,720億米ドルから2022年には7,270億米ドルへと、年間ベースでほぼ43%増加しました。2023年までには、7,790億米ドルの収益が見込まれています。

- Boeing Commercial Outlook 2022-2041は、2041年までに、飛行業務、整備・エンジニアリング、地上業務、駅業務、貨物業務などの民間航空サービスの世界市場は3兆6,150億米ドルに達すると予測しています。

- また、Boeing Commercial Outlook 2022-2041は、2041年までに新型航空機の世界総出荷数は41,170機になると推定しています。世界の航空機保有台数は2019年時点で約2万5,900機であり、2041年には47,080機に達する可能性が高いです。

- 経済分析局によると、米国の航空輸送産業は2022年第1~3四半期に約3,520億米ドルを経済に加えました。これは前年同期比で約35%増です。

- 以上の理由から、予測期間中は航空宇宙産業が市場をリードすると予想されます。

アジア太平洋が最も高い需要を見込む

- アジア太平洋は、航空宇宙、自動車、電気・電子、その他多くの製造業の中心地です。これらには、多くの高性能合金が使用され、調査された市場での需要を増加させています。

- アジア太平洋では、中国、東南アジア、南アジアの航空宇宙市場が急成長すると予想され、調査市場の需要をさらに押し上げると考えられます。ボーイング商業展望2022~2041によると、2041年までに中国では8,485機の航空機が新たに納入され、市場サービス額は5,450億米ドルに達します。

- さらに、インドでは2036年までに4億8,000万人の航空機利用者が見込まれ、これは日本(2億2,500万人弱)とドイツ(2億人強)の合計を上回ると予測されており、そのためには2038年までに約2,380機の新しい民間航空機が必要になると、India Brand Equity Foundation(IBEF)は述べています。

- これとは別に、高性能合金は石油・ガス産業でも必要とされています。高性能合金は、高温や機械的応力下でもよく働き、海水や酸にさらされても錆びないからです。

- BP Statistical Review of World Energy 2022によると、中国は2021年にアジア太平洋で最大の石油生産国になります。中国の石油生産量は2億トンに迫り、前年比2.5%増となります。同時に、2021年の天然ガス市場の3分の1を占め、中国も地域最大の天然ガス生産国となります。同期間中、中国全体で約2,100億立方メートルの天然ガスが生産されました。

- 予測期間中、同地域では順調に推移しているため、高機能合金市場の成長が期待されます。

高性能合金産業概要

調査対象の高性能合金市場は、主要企業間で部分的に統合されています。主要企業は以下の通り(順不同):ATI、Precision Castparts Corp.、Nippon Yakin Kogyo、CRS Holdings Inc.、High Performance Alloys, Inc.

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 航空宇宙産業における合金の需要増加

- その他の促進要因

- 抑制要因

- 原料価格の変動

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模(数量ベース))

- 卑金属タイプ

- アルミニウム

- ニッケル

- スチール

- マグネシウム

- チタン

- その他

- 製品タイプ

- 耐熱合金

- 耐食合金

- 耐摩耗合金

- その他

- エンドユーザー産業

- 航空宇宙

- 電力

- 石油・ガス(化学を含む)

- 電気・電子

- 自動車

- その他

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- その他の欧州

- その他

- 南米

- 中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)分析**/ 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- AMG

- ATI

- Corporation VSMPO-AVISMA

- CRS Holdings Inc.

- Fort Wayne Metals Research Products, LLC

- High Performance Alloys, Inc

- Nippon Yakin Kogyo Co., Ltd.

- Precision Castparts Corp

- Stanford Advanced Materials

第7章 市場機会と今後の動向

- 非鉄金属需要の急増

- その他の機会

The High Performance Alloys Market is expected to register a CAGR of less than 5% during the forecast period.

During the COVID-19 period, government lockdowns in many parts of the world caused end-user operations to stop for a while. This had a big effect on the aerospace, power, and oil and gas industries, and so on the high-performance alloys market as well.However, post-pandemic, the industries have recovered, and the market is expected to retain its growth trajectory in the coming years.

Key Highlights

- The aerospace industry's growing need for alloys is the main thing that is making the market studied grow.

- However, fluctuating pricing of raw materials is likely to hinder market growth.

- Nevertheless, the surging demand for non-ferrous metals due to their benefits over other types of materials is likely to act as an opportunity for the market.

- The Asia-Pacific region had the biggest share of the market and is expected to keep doing so during the next few years.

High Performance Alloys Market Trends

Aerospace Industry to Dominate the Market

- High-performance alloys serve various purposes in industries such as aerospace, oil and gas, automotive, and others due to their high mechanical strength, high surface stability, and corrosion resistance. However, the increasing demand for lightweight equipment and the surge in demand for new-generation aircraft in the aerospace industry are likely to drive the market forward.

- Next-generation aircraft, rotorcraft, unmanned aerial vehicles, and missiles will have stricter requirements in terms of lightweight, visual, and thermal signatures, increased speed, and maneuverability. These requirements incite a need for high-performance alloys that can incorporate these functionalities.

- The International Air Transport Association (IATA) estimates that the global revenue for commercial airlines increased by almost 43 percent on an annual basis, from USD 472 billion in 2021 to USD 727 billion in 2022. By 2023, it is anticipated that the revenue will total USD 779 billion.

- Boeing's Commercial Outlook 2022-2041 predicts that by 2041, the global market for commercial aviation services, such as flight operations, maintenance and engineering, ground, station, and cargo operations, will be worth USD 3,615 billion.This is likely to increase demand for the market under consideration in the years to come.

- The Boeing Commercial Outlook 2022-2041 also stated that the total global deliveries of new airplanes are estimated to be 41,170 by 2041. The global airplane fleet amounted to around 25,900 units as of the year 2019, and the fleet number is likely to reach 47,080 units by 2041.

- The Bureau of Economic Analysis said that the air transport industry in the United States added about USD 352 billion to the economy in the first three quarters of 2022. This is about 35% more than the same time period the year before.

- Due to the above reasons, it is expected that the aerospace industry will lead the market during the forecast period.

Asia-Pacific Region to Witness Highest Demand

- The Asia-Pacific region is a center for many types of manufacturing, such as aerospace and automotive, electrical and electronics, and many others.For these things, a lot of high-performance alloys are used, which increases the demand in the studied market.

- In the Asia-Pacific region, the aerospace markets in China, Southeast Asia, and South Asia are expected to grow at a fast rate, which will boost the demand for the studied market even more.By 2041, there will be 8,485 new fleet deliveries in China with a market service value of USD 545 billion, according to the Boeing Commercial Outlook 2022-2041.

- Moreover, India is projected to have 480 million flyers by 2036, which will be more than that of Japan (just under 225 million) and Germany (just over 200 million) combined, and for that to happen, India will need approximately 2,380 new commercial airplanes by 2038, as stated by the Indian Brand Equity Foundation (IBEF).

- Aside from this, high-performance alloys are also needed in the oil and gas industry. They work well at high temperatures and under mechanical stress, and they don't rust when exposed to seawater or acid.

- According to the BP Statistical Review of World Energy 2022, China will be the biggest oil producer in the Asia-Pacific region in 2021. It will produce close to 200 million tons of oil, which is 2.5% more than it did the year before. At the same time, accounting for one-third of the natural gas market in 2021, China was also the region's largest natural gas producer. Around 210 billion cubic meters of natural gas were produced in China overall in that period.

- During the forecast period, the market for high-performance alloys is expected to grow because things are going well in the region.

High Performance Alloys Industry Overview

The high-performance alloys market studied is partially consolidated among the top players. The key players include (in no particular order): ATI, Precision Castparts Corp., Nippon Yakin Kogyo Co., Ltd., CRS Holdings Inc., and High Performance Alloys, Inc., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand of the Alloys in the Aerospace Industry

- 4.1.2 Other Drivers

- 4.2 Restraints

- 4.2.1 Fluctuating Pricing of Raw Materials

- 4.2.2 Other Restraints

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Base Metal Type

- 5.1.1 Aluminum

- 5.1.2 Nickel

- 5.1.3 Steel

- 5.1.4 Magnesium

- 5.1.5 Titanium

- 5.1.6 Other Base Metal Types

- 5.2 Product Type

- 5.2.1 Heat Resistant Alloys

- 5.2.2 Corrosion Resistant Alloys

- 5.2.3 Wear Resistant Alloys

- 5.2.4 Other Product Types

- 5.3 End-user Industry

- 5.3.1 Aerospace

- 5.3.2 Power

- 5.3.3 Oil and Gas (including Chemical)

- 5.3.4 Electrical and Electronics

- 5.3.5 Automotive

- 5.3.6 Other End-user Industries

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 France

- 5.4.3.3 Germany

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 Rest of the World

- 5.4.4.1 South America

- 5.4.4.2 Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis ** / Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AMG

- 6.4.2 ATI

- 6.4.3 Corporation VSMPO-AVISMA

- 6.4.4 CRS Holdings Inc.

- 6.4.5 Fort Wayne Metals Research Products, LLC

- 6.4.6 High Performance Alloys, Inc

- 6.4.7 Nippon Yakin Kogyo Co., Ltd.

- 6.4.8 Precision Castparts Corp

- 6.4.9 Stanford Advanced Materials

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Surging Demand for Non-ferrous Metals

- 7.2 Other Opportunities