飲料用キャップとクロージャ:市場シェア分析、産業動向と統計、成長予測(2025~2030年)

Beverage Caps And Closures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1629812

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

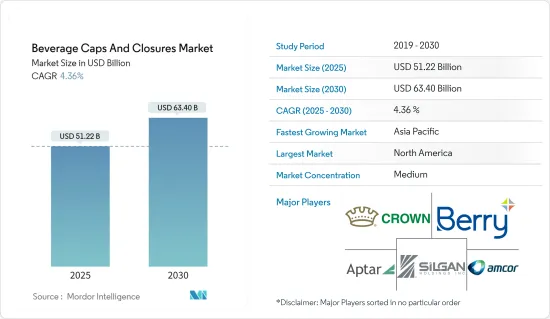

飲料用キャップとクロージャ市場規模は2025年に512億2,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは4.36%で、2030年には634億米ドルに達すると予測されます。

主要ハイライト

- キャップとクロージャは、飲料タイプや包装材にかかわらず、飲料の流出を防ぎ、製品の鮮度を維持する上で極めて重要です。これらの部品は保存期間を延ばし、密封によって微生物汚染から保護します。米国では、プラスチック製キャップとクロージャの需要は、利便性と使いやすさを求める消費者の嗜好が主要要因となっています。プラスチックキャップは製品を汚染物質や微生物から効果的に保護します。さらに、プラスチック製キャップとクロージャは、金属製キャップとクロージャよりもコスト面で有利です。

- キャップとクロージャの世界の需要は、その使いやすさとサステイナブル包装品質により増加しています。PETとPPはその製造に使用される主原料です。これらの部品は、飲料産業でアルコール製品、ノンアルコール製品の両方に広く利用されています。キャップとクロージャは、製品の賞味期限を延ばし、汚染物質や湿気から保護し、包装された商品の酸素濃度を調整するなど、複数の機能を果たします。需要が増加し続けているため、予測期間中に市場はさらなる成長が見込まれます。

- ボトル入り飲料水は、量的に最も急成長している飲料カテゴリーのひとつです。ボトル入り飲料水に対する消費者の需要が増加していることから、予測期間中、開封防止キャップとクロージャのニーズが高まると予想されます。消費者の間で健康とウェルネスに対する意識が高まり、甘い飲料からより健康的な代替品へとシフトしており、ボトル入り飲料水はこの動向の主要受益者です。さらに、一部の地域では水質に対する懸念がボトル入り飲料水の需要をさらに押し上げ、堅牢な包装ソリューションが必要とされています。

- 現代の消費者の「オン・ザ・ゴー」ライフスタイルは、軽量で使い勝手の良い包装ソリューションの需要を押し上げています。カスタムキャップとクロージャのメーカーは、より軽量で効率的なデザインで対応しています。世界市場の成長は、様々な種類の飲料に対する需要の増加によってさらに促進されています。こうした動向は、リサイクル可能な材料やeコマースのニーズに対応したデザインなど、包装の革新につながっています。カスタムキャップ&クロージャ市場は進化を続け、消費者の嗜好や多様な産業の製品要件に対応しています。

- さらに、ライフスタイルパターンの変化と一人当たりの消費量の増加が、ボトル入り飲料水市場の拡大に拍車をかけています。都市化、多忙なライフスタイル、ボトル入り飲料水の利便性がその人気に貢献しています。消費者が外出先での水分補給を選ぶようになっているため、メーカーは製品の安全性と使いやすさを確保するために、さまざまなサイズのボトルや革新的なクロージャデザインを提供することで対応しています。この動向は今後も続くとみられ、ボトル入り飲料水用包装の不正開封防止キャップとクロージャ市場のさらなる成長を促すと考えられます。

- プラスチック包装の技術的進歩は、産業内の製品開発における大きな革新につながっています。多くの企業がユニークでコスト効率の高い製品を生み出すために研究開発活動に多額の投資を行っており、その結果、市場の革新が進んでいます。しかし、気候変動に対する懸念の高まりから、包装用プラスチック使用に対する政府の規制が厳しくなっています。これらの規制は、予測期間中の飲料用キャップとクロージャ市場の成長に対する主要な制約になると予想されます。

飲料用キャップとクロージャ市場の動向

ボトル入り飲料水セグメントが大きな市場シェアを占める

- ボトル入り飲料水市場は、米国のような先進国市場やインド、インドネシアのような新興国市場において、主要飲料タイプの中で最も大幅な成長を記録すると予想されます。この成長の原動力となっているのは、健康意識の高まり、利便性、一部の地域における水道水の水質に対する懸念です。2023会計年度には、Indian Railways Catering &Tourism Corporation Ltd.(IRCTC)が35以上の飲料を生産しました。(IRCTC)は3億5,700万本以上のボトル入り飲料水を生産し、2022年の1億9,860万本からほぼ倍増しました。この大幅な増加は、インドにおけるボトル入り飲料水市場の急拡大を反映しています。

- ボトル入り飲料水市場の拡大は、特に拡大するボトル入り飲料水セグメントにおいて、プラスチック製キャップとクロージャの需要増加を生み出しています。キャップとクロージャは、ボトル入り飲料水の品質と安全性を維持し、汚染を防ぎ、鮮度を確保する上で重要な役割を果たしています。ボトル入り飲料水の消費量が世界的に増加し続けているため、プラスチック製キャップとクロージャのメーカーは持続的な成長機会に恵まれる可能性が高いです。この動向は、製品の安全性と消費者の信頼を高めるタンパーエビデント機能や改良されたシーリング技術など、キャップ設計の革新によってさらに後押しされています。

- 飲料市場では、ガラス容器からプラスチック容器への移行が進んでおり、プラスチック製キャップとクロージャの需要を押し上げると予想されます。この移行は、軽量であること、破損による製品ロスを減らすことができることなど、プラスチックの利点によって推進されます。より広範な市場では、金属製キャップが、特にビール瓶に好まれるクロージャとして、引き続き優位を占めると考えられます。ワイン産業では、主に1回分のワインボトルの人気が高まっているため、金属製ロールオン・スクリュー・キャップの使用が増加すると考えられます。

- さらに、ボトル入り飲料水は、世界的に数量が最も急成長している飲料カテゴリーの一つです。ボトル入り飲料水に対する消費者の需要が増加し、予測期間中に開封防止キャップとクロージャのニーズが高まると考えられます。ボトル入り飲料水市場の成長は、ライフスタイルの変化と一人当たりの消費量によって促進されます。ボトル入り飲料水市場における競争企業間の敵対関係は、Coca-Cola、Danone、Nestle、PepsiCo、Nongfu Springといった国際的な競合企業の存在感の高まりによって激化しています。

- プラスチック包装の技術先進は、飲料産業の製品開発に革新をもたらしました。多くの企業が、ユニークで費用対効果の高い製品を開発するために研究開発活動に多額の投資を行っており、このセグメントにおける技術革新は著しく増加しています。

- AmcorやBallなど、他の多くの大手企業も同様の戦略をとり、新しく革新的な最終製品を提供しています。産業の技術革新に伴い、製品に対する需要も伸びているため、世界中の飲料産業におけるキャップとクロージャの成長を牽引しています。

大きな成長を記録するアジア太平洋

- アジア太平洋のキャップとクロージャ市場は中国が支配的で、インドと日本が僅差で続いています。いくつかの重要な要因がこの主導的地位を後押ししています。第一に、飲料産業によるボトル入り飲料水とパック入り飲料の需要の増加が市場を大きく押し上げています。第二に、キャップとクロージャの製造に高性能材料を採用することで、製品の品質と機能性が向上しています。第三に、この市場は幅広い材料組成の恩恵を受けており、包装ソリューションの多様性を可能にしています。

- 中国の経済成長は、市場情勢の形成に重要な役割を果たしています。同国の経済が急拡大を続けるなか、中流家庭の可処分所得が大幅に増加しています。この購買力の上昇により、飲料を中心とした包装商品の消費が増加し、キャップとクロージャの需要を牽引しています。この動向は今後も続くと予想され、アジア地域の市場リーダーとしての中国の地位はさらに確固たるものになると考えられます。

- アジア太平洋のキャップとクロージャ市場は、主に飲料消費の増加と人口増加によって拡大しつつあります。同地域の飲料産業は、可処分所得の増加に起因して、過去10年間で巨大な成長を遂げました。この動向は、消費者の嗜好の変化、特にエネルギー飲料や栄養飲料への需要の高まりの影響を受け、予測期間を通じて継続すると予想されます。

- この地域のプラスチック製キャップとクロージャ市場は、急速な都市化、人口増加、アルコール需要の増加によって牽引されています。さらに、この地域では、プラスチックのリサイクルと持続可能性を重視する産業が増加しているため、キャップとクロージャにリサイクル可能なプラスチック材料の採用が増加すると予想されます。2023会計年度には、インドの各種蒸留酒の中でウイスキーの数量が最も多く、2億5,000万ケースを超えます。対照的にブランデーの数量は約8,200万ケースでした。同国の蒸留酒市場全体の数量は4億ケースに近づいています。このような動向は、様々なアルコール飲料にキャップやクロージャの需要を生み出しています。

- ベリカップの最近の調査によると、中国の拡大する中産階級は、特にキャップやクロージャのようなプラスチック部品を必要とする包装産業において、より洗練された製品を求めています。その結果、中国のプラスチック産業は、技術や環境に優しいコンセプトに焦点を当てた、包括的な変革期を迎えています。市場の動向は、魅力的な色彩や印刷へと向かっています。製品の色、形、質感、グラフィック、印刷がブランドID確認を伝え、店頭で競合他社と差別化するため、企業は人目を引く包装の生産をますます重視するようになっています。

飲料用キャップとクロージャ産業概要

飲料用キャップとクロージャ市場は細分化されており、各社は競合価格と最先端の製品を提供することで顧客を獲得しています。Crown Holdings Inc.、Berry Global Inc.、Aptar Group Inc.、Evergreen Packaging Inc.、Global Closure Systemsなどが市場の大手企業です。研究開発投資、新市場への取り組み、世界的プレゼンス、生産拠点や施設、生産能力、製品発売などにより、市場は競争状態にあります。

- 2024年6月、BERICAPは、アフリカ、南米、東南アジアに新たな生産施設を設立し、国際的な足跡を広げました。同社は、ケニアのナイロビとベトナムのホーチミン市で新工場を立ち上げ、ペルーのリマと南アフリカのダーバンで設立された生産ユニットも買収しました。これらの戦略的移転により、ベリカップの生産拠点は25カ国に30カ所となり、顧客は現地に根ざしたプロジェクトサポート、ロジスティクス、サービスの恩恵を受けられるようになりました。

- 2024年3月、ワインと蒸留酒用のクロージャとカプセルの世界的リーダーであるAmcor Capsulesは、STELVINアルミニウム・スクリュー・キャップ・シリーズの発売60周年を迎えました。1964年にフランスのシャロン=シュル=ソーヌで発売されたSTELVINキャップは、ワイン産業における極めて重要な進化の先駆けとなりました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業のサプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- 新興経済諸国における飲料消費の増加

- 技術の進歩と革新的包装ソリューション

- 市場抑制要因

- プラスチック製キャップとクロージャの使用に関する厳しい規制

第6章 市場セグメンテーション

- 材料別

- 金属

- プラスチック

- その他の材料(ゴム、コルク)

- 用途別

- ビール

- ワイン

- ボトル入り飲料水

- 炭酸飲料

- 乳製品

- 調味料・ソース

- その他

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア・ニュージーランド

- ラテンアメリカ

- ブラジル

- メキシコ

- コロンビア

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Crown Holdings Inc.

- Berry Global Inc.

- Aptar Group Inc.

- Global Closure Systems

- Silgan Holdings Inc.

- Bericap GmbH & Co. KG

- Guala Closures Group

- Ball Corporation

- Amcor Group

- Pact Group

- Albea Group

- Tetra Laval International

第8章 投資分析

第9章 市場機会と今後の動向

目次

The Beverage Caps And Closures Market size is estimated at USD 51.22 billion in 2025, and is expected to reach USD 63.40 billion by 2030, at a CAGR of 4.36% during the forecast period (2025-2030).

Key Highlights

- Caps and closures are crucial in preventing beverage spillage and maintaining product freshness, regardless of the beverage type or packaging material. These components extend shelf life and protect against microbial contamination through tight seals. In the United States, the demand for plastic caps and closures is primarily driven by consumer preferences for convenience and ease of use. Plastic caps effectively shield products from contaminants and microorganisms. Additionally, plastic caps and closures offer a cost advantage over their metal counterparts.

- The global demand for caps and closures is increasing due to their ease of use and sustainable packaging qualities. PET and PP are the primary raw materials used in their manufacture. These components are extensively utilized in the beverage industry for both alcoholic and non-alcoholic products. Caps and closures serve multiple functions: they extend product shelf life, protect against contaminants and moisture, and regulate oxygen levels in packaged goods. As demand continues to rise, the market is expected to experience further growth during the forecast period.

- Bottled water is one of the fastest-growing beverage categories in terms of volume. This increasing consumer demand for bottled water is expected to drive the need for tamper-proof caps and closures during the forecast period. The growing awareness of health and wellness among consumers has shifted from sugary drinks to healthier alternatives, with bottled water being a primary beneficiary of this trend. Additionally, concerns about water quality in some regions have further boosted the demand for bottled water, necessitating robust packaging solutions.

- The modern consumer's "on-the-go" lifestyle has driven demand for lightweight, user-friendly packaging solutions. Custom caps and closures manufacturers are responding with lighter and more efficient designs. The global market growth is further propelled by increasing demand for various beverage types. These trends have led to packaging innovations, including recyclable materials and designs catering to e-commerce needs. The custom caps and closures market continues evolving, meeting consumer preferences and product requirements across diverse industries.

- Moreover, changes in lifestyle patterns and increased per capita consumption fuel the expansion of the bottled water market. Urbanization, busy lifestyles, and the convenience of bottled water have contributed to its popularity. As consumers increasingly opt for on-the-go hydration, manufacturers are responding by offering a variety of bottle sizes and innovative closure designs that ensure product safety and ease of use. This trend will likely continue, driving further growth in the tamper-proof caps and closures market for bottled water packaging.

- Technological advancements in plastic packaging have led to significant innovations in product development within the industry. Many companies invest heavily in research and development activities to create unique and cost-effective products, resulting in increased market innovations. However, the growing concern over climate change has led to stringent government regulations on plastic usage for packaging. These regulations are expected to be the primary constraint on the growth of the beverage caps and closures market during the forecast period.

Beverage Caps And Closures Market Trends

Bottled Water Segment Holds a Significant Market Share

- The bottled water market is expected to register the most substantial gains among major beverage types in developed markets like the United States and developing areas such as India and Indonesia. This growth is driven by increasing health consciousness, convenience, and concerns about tap water quality in some regions. In the financial year 2023, Indian Railways Catering & Tourism Corporation Ltd. (IRCTC) produced over 357 million units of bottled water, nearly doubling their production from 198.60 million units in 2022. This significant increase reflects the rapidly expanding bottled water market in India.

- The growing market for bottled water is creating increased demand for plastic caps and closures, particularly within the expanding bottled water segment. Caps and closures play a crucial role in maintaining the quality and safety of bottled water, preventing contamination, and ensuring freshness. As bottled water consumption continues to rise globally, manufacturers of plastic caps and closures are likely to see sustained growth opportunities. This trend is further supported by innovations in cap design, such as tamper-evident features and improved sealing technologies, which enhance product safety and consumer confidence.

- The ongoing transition from glass to plastic containers is expected to boost demand for plastic caps and closures in the beverage market. This shift is driven by plastic's advantages, including its lightweight nature and ability to reduce product loss through breakage. In the broader market, metal caps will continue to dominate, particularly as the preferred closure for beer bottles. The wine industry is likely to see an increase in metal roll-on screw cap usage, primarily due to the growing popularity of single-serve wine bottles.

- Moreover, bottled water is one of the beverage categories with the fastest growth in terms of volume globally. There would be a rise in the consumer demand for bottled water, raising the need for tamper-evident caps and closures in the forecast period. The bottled water market's growth is fueled by changes in lifestyle and per capita consumption. The competitive rivalry in the market for bottled water is intensified by the increasing presence of international competitors like Coca-Cola, Danone, Nestle, PepsiCo, and Nongfu Spring.

- Technology advancements in plastic packaging have resulted in innovations in product development in the beverage industry. Many companies are investing significantly in R&D activities to develop unique and cost-effective products, and innovation in this space is increasing significantly.

- Many other major companies, such as Amcor and Ball Corp., follow similar strategies and offer new and innovative final products. With innovations in the industry, the demand for products is also growing, thus driving the growth of caps and closures in the beverages industry around the globe.

Asia-Pacific to Register Major Growth

- The Asia-Pacific caps and closures market is dominated by China, with India and Japan following closely behind. Several key factors drive this leadership position. First, the beverage industry's increasing demand for bottled water and packaged drinks has significantly boosted the market. Second, adopting high-performance materials in cap and closure manufacturing has enhanced product quality and functionality. Third, the market benefits from a wide range of material compositions, allowing for versatility in packaging solutions.

- China's economic growth has played a crucial role in shaping the market landscape. As the country's economy continues to expand rapidly, middle-class families are experiencing a substantial increase in their disposable incomes. This rise in purchasing power has led to higher consumption of packaged goods, particularly beverages, driving the demand for caps and closures. The trend is expected to continue, further solidifying China's position as the market leader in the Asia region.

- The Asia-Pacific caps and closures market is experiencing expansion, primarily driven by increasing beverage consumption and population growth. The region's beverage industry has grown enormously over the past decade, attributed to rising disposable incomes. This trend is expected to continue throughout the forecast period, influenced by evolving consumer preferences, particularly the growing demand for energy and nutritional drinks.

- The plastic caps and closures market in this region has been driven by rapid urbanization, population growth, and increasing alcohol demand. Additionally, the region's adoption of recyclable plastic materials for caps and closures is expected to rise as industries increasingly emphasize plastic recycling and sustainability. In the financial year 2023, whiskey had the highest sales volume among various spirits in India, exceeding 250 million cases. Brandy, in contrast, had a sales volume of approximately 82 million cases. The country's overall spirits market sales approached 400 million cases. This growing trend creates demand for caps and closures for various alcoholic beverages.

- A recent survey by Bericap indicates that China's expanding middle class is demanding more sophisticated products, particularly in the packaging industry, which requires plastic components like caps and closures. Consequently, China's plastic industry is undergoing a comprehensive transformation, focusing on technology and environmentally friendly concepts. The market is experiencing a trend toward attractive colors and printing. Companies are increasingly emphasizing the production of eye-catching packages, as the color, shape, texture, graphics, and printing of products communicate brand identity and differentiate them from competitors on store shelves.

Beverage Caps And Closures Industry Overview

The beverage caps and closures market is fragmented, with firms varying for customers by offering competitive prices and cutting-edge products. Crown Holdings Inc., Berry Global Inc., Aptar Group Inc., Evergreen Packaging Inc., and Global Closure Systems are a few of the market's biggest companies. Due to R&D investments, new market efforts, global presence, production sites and facilities, production capabilities, and product launches, the market is competitive.

- June 2024: BERICAP broadened its international footprint by setting up new production facilities in Africa, South America, and Southeast Asia. The company launched new plants in Nairobi, Kenya, and Ho Chi Minh City, Vietnam, and also acquired established production units in Lima, Peru, and Durban, South Africa. These strategic moves brought BERICAP's total to 30 production sites in 25 countries, ensuring customers benefit from localized project support, logistics, and services.

- March 2024: Amcor Capsules, a worldwide leader in crafting closures and capsules for wine and spirits, marked the 60th anniversary of its STELVIN aluminum screw cap range. Launched in 1964 in Chalon-sur-Saone, France, the STELVIN cap heralded a pivotal evolution in the wine industry.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Supply Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Beverage Consumption in Developing Economies

- 5.1.2 Technological Advancements and Innovative Packaging Solutions

- 5.2 Market Restraints

- 5.2.1 Stringent Regulations on the Usage of Plastic caps and closures

6 MARKET SEGMENTATION

- 6.1 By Material

- 6.1.1 Metal

- 6.1.2 Plastic

- 6.1.3 Other Materials (Rubber, Cork)

- 6.2 By Application

- 6.2.1 Beer

- 6.2.2 Wine

- 6.2.3 Bottled water

- 6.2.4 Carbonated soft drinks

- 6.2.5 Dairy products

- 6.2.6 Condiments and sauces

- 6.2.7 Other Applications

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 United Kingdom

- 6.3.2.3 France

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.5.1 Brazil

- 6.3.5.2 Mexico

- 6.3.5.3 Colombia

- 6.3.6 Middle East and Africa

- 6.3.6.1 United Arab Emirates

- 6.3.6.2 Saudi Arabia

- 6.3.6.3 South Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Crown Holdings Inc.

- 7.1.2 Berry Global Inc.

- 7.1.3 Aptar Group Inc.

- 7.1.4 Global Closure Systems

- 7.1.5 Silgan Holdings Inc.

- 7.1.6 Bericap GmbH & Co. KG

- 7.1.7 Guala Closures Group

- 7.1.8 Ball Corporation

- 7.1.9 Amcor Group

- 7.1.10 Pact Group

- 7.1.11 Albea Group

- 7.1.12 Tetra Laval International

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日