海底ポンプ:市場シェア分析、産業動向、成長予測(2025~2030年)

Subsea Pump - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日

- 商品コード

- 1629777

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

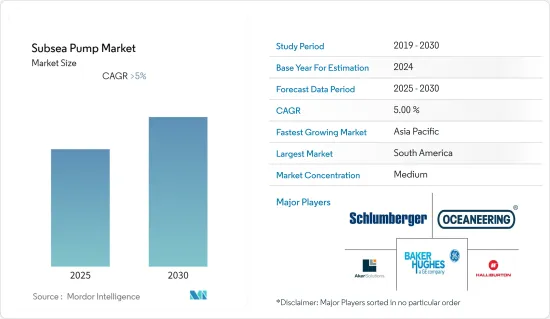

海底ポンプ市場は予測期間中にCAGR 5%超を記録する見込み。

2020年、COVID-19は市場に悪影響を及ぼしました。現在、市場は流行前のレベルに達しています。

主要ハイライト

- 中期的には、成熟期を迎える陸上油田の増加に伴い、探鉱・生産活動はより深い沖合地域へとシフトしていくと予想され、その結果、オフショア深海・超深海プロジェクトが増加すると見込まれます。このことは、予測期間中、市場を牽引すると予想されます。

- 一方、需給ギャップ、地政学、その他いくつかの要因に起因する、近年の非常に不安定な原油価格シナリオは、予測期間中の研究市場の成長を妨げると予想されます。

- 主要企業は、海洋支出全体のコストを削減するために、技術の進歩のための継続的な研究開発プロジェクトに投資しています。海底ポンプは、主に成熟した海洋油田で採用されており、油層への背圧を低減することで回収率を向上させ、生産支出を削減しています。サブシーポンプのコストを削減する能力は、今後の市場を推進する機会となっています。

- 2018年には南米が世界全体の市場を独占し、需要の大部分はブラジルからもたらされました。最も急成長している地域はアジア太平洋、次いで欧州です。

海底ポンプ市場動向

深海部門が市場を独占

- 石油・ガス産業は、既存のブラウンフィールドや新規資産からの収益を最大化するのに役立つ新しい技術や技術を特定し、その生産量を向上させようとする動きを活発化させています。

- 2021年、世界の原油生産量は約42億トンに達しました。さまざまな水深での探鉱・生産活動は、オフショア産業にとって課題となっています。海底開発がさらに沖合や深海に進むにつれて、技術的な難易度は上昇の一途をたどっています。深海開発では、掘削、油田開発、油田操業に関わる全体的なプロセスや機器に関連して、さまざまな海底レイアウトや生産システムが使用されています。

- 近年、成熟しつつある油田の増加に伴い、海洋探査・生産(E&P)活動が拡大しています。例えば、現在原油生産量において最も重要な盆地であるパーミアン・ベースンでは、古い坑井からの生産量が減少し始めており、これらの地域では発見の余地がほとんどないです。その結果、石油・ガス産業は、増大する需要に対応するため、より深い沖合での石油・ガス探査にシフトしつつあります。

- また、オフショアプロジェクトはリードタイムが長く、費用もかかります。事業者は、生産インフラに投資する前に、高額なCAPEXを必要とする他のインフラを建設しました。したがって、すでにFIDが実施され開発が始まっているプロジェクトは、石油・ガス生産収入を通じて投資を回収し続ける可能性が高いです。これらのプロジェクトは、予測期間の前半において重要な推進力になると予想されます。

- 2021年時点で、オフショア石油・ガス産業は世界の原油生産量の約30%を占めています。中東、北海、ブラジル、メキシコ湾、カスピ海が主要なオフショア石油・ガス生産地域です。これに加えて、豊富な資源が利用可能であることに加え、深海や超深海地域からの石油・ガス回収の可能性が高まっていることから、市場調査には大きな機会が期待されます。

- さらに、原油価格が安定した環境下では、原油価格が低いために実行不可能であったプロジェクトが開始され、CAPEXが増加したため、深海と超深海プロジェクトは収益の急増を目の当たりにしました。

- したがって、海洋探査投資の増加と新規開発油田からの石油生産により、深海部門が予測期間中に市場を独占すると予想されます。

著しい成長を遂げる南米

- この地域では、ここ数年、海洋石油・ガス開発が活発に行われています。これは、世界中のオフショア石油・ガスプロジェクトと比較して損益分岐点価格が低く、投資回収期間が競合的であるため、現在の激動の時代により強くなっていることに起因しています。

- 2021年現在、ブラジルは石油・ガス支出に関して南米の主要国です。同国の海上プレソルト油田は、石油総生産量の約50%を汲み上げ、2020年末までに約75%まで増加しました。このように生産量が増加し、オフショア油田・ガス田への依存度が高まっているのは、掘削技術の向上、オフショア石油・ガス産業における専門知識の向上、インフラの整備などにより、生産費用が着実に減少しているためです。

- さらに、アルゼンチンの国営石油会社YPFの2021年の設備投資額は約27億1,000万米ドルで、2020年の値(2020年の設備投資額:15億5,000万米ドル)と比較すると約74%の増加となっています。同社は予測期間中、同国の石油・ガス部門、特に上流部門での設備投資額をさらに増加させる計画です。

- コロンビアは、同国の石油・ガス部門に開発の兆しを見せています。2021年、コロンビアの国営石油会社Ecopetrolは、CAPEX目標を50億米ドルに設定しました。これは、2021年の予想値(35億米ドル)に比べて約30%の増加です。このような増加が予想されるのは、国内外の探鉱・生産プロジェクトが活発化しているためです。深海における最新の投資と今後のプロジェクトは、南米地域における予測期間中の海底ポンプ市場の成長を促進すると考えられます。

- 以上のような点と最近の動向から、南米は予測期間中に海底ポンプ市場で大きな成長を遂げることが予想されます。

海中ポンプ産業概要

海中ポンプ市場は適度にセグメント化されています。同市場の主要企業(順不同)には、Aker Solutions ASA、Baker Hughes A GE Co.、Halliburton Company、Schlumberger Limited、Weatherford International PLC、Oceaneering Internationalなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2028年までの市場規模と需要予測(単位:10億米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 抑制要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 展開別

- 浅水域

- 深海

- 用途別

- ブースティング

- 分離

- インジェクション

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- アジア太平洋

- 中国

- インド

- オーストラリア

- インドネシア

- 欧州

- 英国

- フランス

- ドイツ

- その他の欧州

- 南米

- ブラジル

- コロンビア

- チリ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Aker Solutions ASA

- Baker Hughes Co

- Halliburton Company

- Schlumberger Limited

- Oceaneering International Inc.

- TechnipFMC PLC

- Weatherford International PLC

- Drill-Quip Inc.

- National-Oilwell Varco Inc

- Subsea 7 SA

- Saipem SpA

第7章 市場機会と今後の動向

目次

The Subsea Pump Market is expected to register a CAGR of greater than 5% during the forecast period.

In 2020, COVID-19 had a detrimental effect on the market. Presently, the market has reached pre-pandemic levels.

Key Highlights

- Over the medium term, with the increasing number of onshore fields reaching maturity, exploration and production activity is expected to make a shift toward deeper offshore regions, which is expected to result in an increase in offshore deep-ultra deepwater projects. This, in turn, is expected to drive the market during the forecast period.

- On the other hand, a highly volatile crude oil price scenario in recent years, owing to the supply-demand gap, geopolitics, and several other factors, is expected to hinder the growth of the market studied during the forecast period.

- Nevertheless, the major companies are investing in ongoing R&D projects for the advancement of technology to reduce the overall cost of offshore expenditures. Subsea pumps are employed primarily in mature offshore fields to improve the recovery rate by reducing back-pressure on the reservoir, thereby lowering the production expenditure. The ability to reduce the cost of a subsea pump is providing the opportunity to propel the market in the coming future.

- South America dominated the market across the globe in 2018, with the majority of the demand coming from Brazil. The fastest-growing region is Asia-Pacific, then Europe.

Subsea Pumps Market Trends

Deepwater Sector to Dominate the Market

- The oil and gas industry is engaged in a rising movement to identify new techniques and technologies that can help them maximize revenues from existing brownfields and new assets by enhancing their outputs.

- In 2021, global crude oil production amounted to approximately 4.2 billion metric tons. Exploration and production activities in various water depths have become a challenge for the offshore industry. As the subsea developments have further moved offshore and into deeper waters, the technical difficulty has continuously increased. A wide range of subsea layouts and production systems are used for deepwater developments, associated with the overall process and the equipment involved in drilling, field development, and field operation.

- With the rising number of maturing oilfields in recent years, there has been growth in offshore exploration and production (E&P) activities. For instance, in the Permian Basin, currently the most important basin in terms of crude oil production, the production from old wells has started to decline, and there is little scope for discovery in these areas. As a result, the oil and gas industry is shifting toward deeper offshore regions to search for oil and gas to meet the increasing demand.

- Also, offshore projects have a high lead time and are expensive. Before the operators invested in the production infrastructure, they built other infrastructure that required high CAPEX. Hence, the development of the projects, for which the FIDs have already been taken and development has begun, is likely to continue to recover the investment through oil and gas production revenues. These projects are expected to be significant drivers during the first half of the forecast period.

- As of 2021, the offshore oil and gas industry accounted for about 30% of global crude oil production. The Middle East, North Sea, Brazil, the Gulf of Mexico, and the Caspian Sea are the major offshore oil and gas producing regions. In addition to this, the availability of abundant resources, coupled with increased potential to recover oil and gas from deepwater and ultra-deepwater areas, is expected to provide a great opportunity for the market to be studied.

- Furthermore, during the stable oil price environment, the deepwater and ultra-deepwater projects witnessed a spike in revenue as the projects, which were not viable due to low crude oil prices, got started and increased the CAPEX.

- Therefore, with increasing offshore exploration investment and oil production from newly developed fields, the deepwater sector is expected to dominate the market in the forecast period.

South America to Witness Significant Growth

- The region has witnessed significant offshore oil and gas activity in the last few years. This can be attributed to the lower breakeven prices and competitive payback times compared to offshore oil and gas projects worldwide, making them more resilient in the current turbulent times.

- As of 2021, Brazil was the major country in South America regarding oil and gas spending. The country's offshore pre-salt oil fields pumped around 50% of the total oil output, which increased to approximately 75% by the end of 2020. This increasing production and dependency on offshore oil and gas fields can be attributed to steadily decreasing production expenses due to improved drilling technology, growing expertise in the offshore oil and gas industry, and increased infrastructure.

- Furthermore, Argentina's state-owned oil company YPF's CAPEX in 2021 stood at around USD 2.71 billion, representing an increase of almost 74% when compared to the value in 2020 (CAPEX in 2020: USD 1.55 billion); the company is planning to further increase the CAPEX in the country's oil and gas sector, especially in the upstream activities, during the forecast period.

- Colombia is showing signs of development in the country's oil and gas sector. In 2021, Colombia's state-owned oil company Ecopetrol set a CAPEX target of USD 5 billion, i.e., an increase of about 30% compared to the expected value (USD 3.5 billion) in 2021. This anticipated increase is because exploration and production projects at home and abroad are ramping up. The latest investment and upcoming projects in deepwater are likely to drive the growth of the subsea pump market during the forecast period in the South America region.

- Owing to the above points and recent developments, South America is expected to witness significant growth in the subsea pump market during the forecast period.

Subsea Pumps Industry Overview

The subsea pump market is moderately fragmented. Some of the major players in the market (in no particular order) include Aker Solutions ASA, Baker Hughes A GE Co., Halliburton Company, Schlumberger Limited, Weatherford International PLC, and Oceaneering International.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, in USD billion, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies & Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Deployment

- 5.1.1 Shallow water

- 5.1.2 Deep Water

- 5.2 By Application

- 5.2.1 Boosting

- 5.2.2 Separation

- 5.2.3 Injection

- 5.2.4 Other Applications

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Asia-Pacific

- 5.3.2.1 China

- 5.3.2.2 India

- 5.3.2.3 Australia

- 5.3.2.4 Indonesia

- 5.3.3 Europe

- 5.3.3.1 United Kingdom

- 5.3.3.2 France

- 5.3.3.3 Germany

- 5.3.3.4 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Colombia

- 5.3.4.3 Chile

- 5.3.4.4 Argentina

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Aker Solutions ASA

- 6.3.2 Baker Hughes Co

- 6.3.3 Halliburton Company

- 6.3.4 Schlumberger Limited

- 6.3.5 Oceaneering International Inc.

- 6.3.6 TechnipFMC PLC

- 6.3.7 Weatherford International PLC

- 6.3.8 Drill-Quip Inc.

- 6.3.9 National-Oilwell Varco Inc

- 6.3.10 Subsea 7 SA

- 6.3.11 Saipem SpA

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日