|

市場調査レポート

商品コード

1628740

南米の接着剤・シーラント:市場シェア分析、産業動向、成長予測(2025~2030年)South America Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 南米の接着剤・シーラント:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

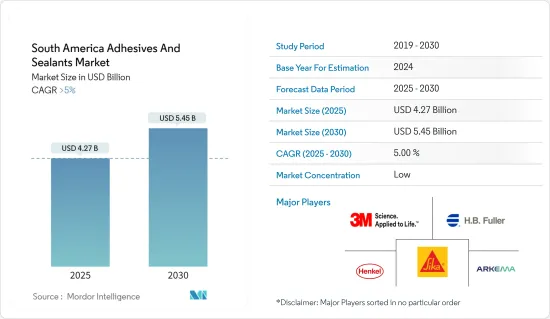

南米の接着剤・シーラント市場規模は2025年に42億7,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは5%を超え、2030年には54億5,000万米ドルに達すると予測されます。

南米の接着剤・シーラント市場はCOVID-19の大流行によって大きな影響を受け、課題と機会の両方をもたらしました。建設業や製造業などの産業では当初、操業停止や混乱によって需要が減少しました。しかし、パンデミックは同時に、医療用品、個人用保護具、衛生用品の製造における接着剤・シーラントの必要性を高めました。当初の後退にもかかわらず、市場は回復し、長期的な成長を示すと予想されています。

接着剤・シーラントの需要は、建設産業からの需要の増加と医療インフラの増加によって大きく牽引されています。

しかし、接着剤・シーラントに関連する厳しいVOC排出規制が市場成長の妨げになる可能性が高いです。

バイオベースの接着剤の技術革新と開発、複合材料の接着へのシフトは、同地域の接着剤・シーラント市場に機会を提供すると考えられます。

ブラジルは、建設、航空宇宙、自動車などのエンドユーザー産業が消費の主要原動力となっているこの地域で、接着剤・シーラントの最大市場となっています。

南米の接着剤・シーラントの市場動向

建築・建設産業が市場を独占

- 接着剤・シーラントは、その特性と物理的特性により、建築・建設産業で広く使用されています。これらの特性には、良好な接着性と弾性、凝集性、高い凝集強度、柔軟性、基材の高い弾性率、熱膨張に対する耐性、紫外線、腐食、塩水、雨、その他の風化条件に対する耐環境性などが含まれます。

- 2022年、南米地域では建設活動が飛躍的に増加します。その理由は、パンデミック(世界的大流行)の年に政府が行った閉鎖や制限の影響からの回復です。

- チリ建設会議所(CChC)によると、建設資材・供給価格指数(IPMIC)は2023年1~3月に前年同期比5.9%上昇しました。

- ブラジルは、この地域の主要かつ最も重要な建設・不動産市場です。しかし、同国の景気後退と脆弱な経済状況は、同地域の建設産業の成長を妨げると予想されます。

- ブラジル政府は、港湾、道路、鉄道、送電線、衛生インフラの開発を目的としたインフラ・コンセッション計画を開始しました。この計画の下、政府は官民パートナーシップ(PPP)モデルを通じて450億BRL(141億米ドル)の投資を目指しています。さらに、Minha Casa Minha Vida(MCMV)、Plano Decenal de Expansao de Energia 2026、National Education Planなどの政府プログラムは、予測期間中の産業の成長をサポートすると予想されます。

- さらに2022年には、ブラジルの産業建設が大幅に増加します。アグリビジネスチェーン企業のBSBiosは、ブラジルで小麦エタノール工場の建設を計画しています。大手投資会社のノルディック・インパクト・コーポレーション(NIC)は、ブラジルで容量18メガワットの太陽光発電所6カ所の建設に投資しています。

- 上記のような薄型ブラジルの要因はすべて、予測期間中、同地域の接着剤・シーラントの需要を増加させると考えられます。

南米地域で需要を独占するブラジル

- ブラジルは南米で接着剤の消費量が最も多い国です。包装、自動車、建設、その他のセクターが接着剤に大きく依存しています。

- ブラジルの成長は、主に住宅と商業建築部門の急速な拡大と同国の経済拡大によって後押しされています。

- ブラジル政府によると、ブラジルの観光都市の状態をアップグレードし、この産業の潜在力を最大限に引き出して、より多くの観光客を呼び込み、より快適な滞在を提供するために、2022年には762のインフラプロジェクトに8億6,600万米ドルが投資されました。

- ブラジルの紙・パルプ部門は、ブラジルで最も成功している農産物輸出のひとつであり、この種の製品を生み出している国の中で上位にランクされています。カートンには、板紙、二つ折り、ホワイトクラフト、再生材、複合材など、さまざまな材料が使われています。Combistyleカートン包装は、SIG社がブラジル最大の牛乳メーカーのひとつであるFrimesaとともに2022年5月に導入しました。これらのカートンパックは、ブラジルのソパウロで開催された南北アメリカ最大のF&B見本市、APAS Show 2022で展示されました。

- ブラジルは南米最大の段ボール市場のひとつです。ブラジル地域統計ラボの推定によると、ブラジルのシート・段ボール包装の生産量は2018年の28億9,000万米ドルから2023年には31億8,000万米ドルに増加すると見込まれています。

- ブラジルのeコマース市場は2021年上半期に31%成長し、2020年にはすでに40%成長しています。競争の激しい今日のFMCG市場において、企業が競合他社に差をつけ、市場におけるブランドイメージを維持するためには、魅力的な包装を使用し、包装にイノベーションをもたらすことが不可避となっています。

- 自動車産業は、国内で接着剤・シーラントを広く使用しているもう一つの主要部門です。OICAによると、2022年の乗用車と商用車を含む自動車総生産台数は236万台で、2021年比で5%の伸びを記録しました。2021年の自動車総生産台数は約224万台と推定されています。

- 同国は、この地域では成熟した医薬品市場です。同国の市場は、国内の大規模なベンダーのおかげで、医薬品包装製品を中心に様々な製品イノベーションを確認しています。

- さらに、ブラジル病院連盟、ブラジル国民健康連盟、ブラジル保健省によると、ブラジルの病院数は2022年に7,191に達しました。このような病院の成長は、配合される医薬品に対するニーズの高まりに対応するため、全国の医薬品包装ベンダーにとっての機会を増大させると考えられます。

- 上記の要因はすべて、同国における接着剤・シーラントの需要に大きな影響を与えています。

南米の接着剤・シーラント産業概要

南米の接着剤・シーラント市場は、その性質上セグメント化されています。主要企業(順不同)には、Henkel AG &Co.KGaA、3M、H.B. Fuller Company、Arkema、Sika AGなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- ブラジルの建設産業からの需要増加

- 包装産業における用途の拡大

- その他の促進要因

- 抑制要因

- VOC排出に関する厳しい環境規制

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- 接着剤樹脂

- ポリウレタン

- エポキシ

- アクリル

- シリコーン

- シアノアクリレート

- VAE・EVA

- その他樹脂(ポリエステル、ゴムなど)

- 接着技術

- 溶剤系

- 反応性

- ホットメルト

- UV硬化型接着剤

- シーラント樹脂

- シリコーン

- ポリウレタン

- アクリル

- エポキシ樹脂

- その他の樹脂(瀝青、ポリサルファイドUV硬化型など)

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- フットウェア・皮革

- 医療

- 包装

- 木工・建具

- その他のエンドユーザー産業(エレクトロニクス、コンシューマー/DIYなど)

- 地域

- アルゼンチン

- ブラジル

- コロンビア

- その他の南米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- 3M

- Arkema Group

- Ashland

- Avery Dennison Corporation

- Beardow Adams

- Dow

- DuPont

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Hexion

- Huntsman International LLC

- ITW Performance Polymers(Illinois Tool Works Inc.)

- Jowat AG

- Mapei Inc.

- Tesa SE(A Beiersdorf Company)

- Pidilite Industries Ltd

- RPM International Inc.

- Sika AG

- Wacker Chemie AG

第7章 市場機会と今後の動向

- バイオベース接着剤の革新と開発

- 複合材料の接着へのシフト

The South America Adhesives And Sealants Market size is estimated at USD 4.27 billion in 2025, and is expected to reach USD 5.45 billion by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

The South American adhesives and sealants market was significantly affected by the COVID-19 pandemic, bringing both challenges and opportunities. Lockdowns and disruptions in industries like construction and manufacturing initially reduced demand. However, the pandemic simultaneously increased the need for adhesives and sealants in manufacturing medical supplies, personal protective equipment, and hygiene products. Despite the initial setbacks, the market is anticipated to recover and exhibit long-term growth.

The demand for adhesives and sealants is extensively driven by the growing demand from the construction industry and increasing healthcare infrastructure.

However, the market growth is likely to be hindered by the stringent VOC emissions regulations related to adhesives and sealants.

The innovation and development of bio-based adhesives and shifting focus toward adhesive bonding for composite materials are likely to offer opportunities for the adhesives and sealants market in the region.

Brazil stands to be the largest market for adhesives and sealants in the region, where the end-user industries, such as construction, aerospace, and automotive, majorly drive consumption.

South America Adhesives and Sealants Market Trends

The Building and Construction Industry to Dominate the Market

- Adhesives and sealants have been extensively used in the building and construction industry owing to their characteristics and physical properties. These properties include good adhesion and elasticity, cohesion, high cohesive strength, flexibility, the high elastic modulus of the substrate, resistance from thermal expansion, and environmental resistance from UV light, corrosion, salt water, rain, and other weathering conditions.

- In 2022, the South American region will see a tremendous increase in construction activities. The reason for this is the rebounding from the impact of lockdowns and restrictions imposed by the government during the pandemic year.

- According to the Chilean Chamber of Construction (CChC), the Construction Materials and Supplies Price Index (IPMIC) rose by 5.9% YoY in the first three months of 2023.

- Brazil is the primary and most significant construction and real estate market in the region. However, the country's recession and weak economic conditions are expected to hamper the growth of the region's construction industry.

- In Brazil, the government launched an infrastructure concessions program with an aim to develop the country's port, road, railway, power transmission lines, and sanitation infrastructure. Under this plan, the government aims to invest BRL 45.0 billion (USD 14.1 billion) through the public-private partnership (PPP) model. Furthermore, government programs such as Minha Casa Minha Vida (MCMV), Plano Decenal de Expansao de Energia 2026, and the National Education Plan are expected to support industry growth over the forecast period.

- Furthermore, in 2022, there will be a tremendous rise in industrial construction in Brazil. BSBios, an agribusiness chain company, is planning to construct a wheat ethanol plant in Brazil. Nordic Impact Cooperation (NIC), a major investment company, has invested in the construction of six solar PV plants with a capacity of 18MW in Brazil.

- All of the above thin Brazil factors are likely to increase the demand for adhesives and sealants in the region during the forecast period.

Brazil to Dominate the Demand in South American Region

- Brazil is the country with the highest consumption of adhesives in South America. Packaging, automotive, construction, and other sectors rely heavily on adhesives.

- Brazil's growth is fueled mainly by rapid expansion in the residential and commercial building sectors and the country's expanding economy.

- According to the Brazilian government, USD 866 million was invested in 762 infrastructure projects in 2022 to upgrade the state of Brazilian tourist cities and maximize the potential of the industry, drawing more tourists and providing them with a more comfortable stay.

- Brazil's paper and pulp sector is one of the country's most successful agricultural exports, ranking high on the list of nations that generate this kind of product. Cartons can be made from various materials such as paperboard, duplex, white kraft, recycled materials, or composite. Combistyle carton packaging was introduced in May 2022 by SIG, along with Frimesa, one of the largest milk producers in Brazil. These carton packs were showcased at APAS Show 2022, the biggest F&B trade show in the Americas, held in So Paulo, Brazil.

- Brazil is one of South America's largest markets for corrugated cardboard. According to estimates from the Brazilian Institute of Geography and Statistics, Brazil's production of sheets and corrugated cardboard packaging is expected to rise from USD 2.89 billion in 2018 to USD 3.18 billion in 2023.

- The Brazil e-commerce market grew by 31% in the first half of 2021, and in 2020, it had already grown by 40%. In today's competitive FMCG market, it has become inevitable for companies to use attractive packaging and bring innovation to their packaging to stand out from their competitors and maintain their brand image in the market.

- The automotive industry is another primary sector that uses adhesives and sealants extensively in the country. According to OICA, the total production of automotive, including passenger cars and commercial vehicles, in 2022 was 2.36 million units, registering a 5% growth in production compared to 2021. In 2021, the total automotive production was estimated to be around 2.24 million units.

- The country is a mature pharmaceutical market in the region. The market in the country witnessed various product innovations, especially pharmaceutical packaging products, owing to significant vendors across the country.

- Furthermore, according to the Brazilian Federation of Hospitals, National Health Confederation (Brazil), and Ministry of Health (Brazil), the number of hospitals in Brazil reached 7,191 in 2022. Such growth in hospitals would increase the opportunities for pharmaceutical packaging vendors nationwide to serve the growing need for prescribed pharmaceuticals.

- All the factors above have a significant impact on the demand for adhesives and sealants in the country.

South America Adhesives and Sealants Industry Overview

The South American adhesives and sealants market is fragmented in nature. The major players (not in any particular order) include Henkel AG & Co. KGaA, 3M, H.B. Fuller Company., Arkema and Sika AG.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Report

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Demand from the Construction Industry in Brazil

- 4.1.2 Growing Usage in the Packaging Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations Regarding VOC Emissions

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Adhesives Resin

- 5.1.1 Polyurethane

- 5.1.2 Epoxy

- 5.1.3 Acrylic

- 5.1.4 Silicone

- 5.1.5 Cyanoacrylate

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins (Polyester, Rubber, etc.)

- 5.2 Adhesives Technology

- 5.2.1 Solvent-borne

- 5.2.2 Reactive

- 5.2.3 Hot Melt

- 5.2.4 UV-Cured Adhesives

- 5.3 Sealant Resin

- 5.3.1 Silicone

- 5.3.2 Polyurethane

- 5.3.3 Acrylic

- 5.3.4 Epoxy

- 5.3.5 Other Resins (Bituminous, Polysulfide UV-Curable, etc.)

- 5.4 End-user Industry

- 5.4.1 Aerospace

- 5.4.2 Automotive

- 5.4.3 Building and Construction

- 5.4.4 Footwear and Leather

- 5.4.5 Healthcare

- 5.4.6 Packaging

- 5.4.7 Woodworking and Joinery

- 5.4.8 Other End-user Industries (Electronics, Consumer/DIY, etc.)

- 5.5 Geography

- 5.5.1 Argentina

- 5.5.2 Brazil

- 5.5.3 Colombia

- 5.5.4 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 Ashland

- 6.4.4 Avery Dennison Corporation

- 6.4.5 Beardow Adams

- 6.4.6 Dow

- 6.4.7 DuPont

- 6.4.8 H.B. Fuller Company

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Hexion

- 6.4.11 Huntsman International LLC

- 6.4.12 ITW Performance Polymers (Illinois Tool Works Inc.)

- 6.4.13 Jowat AG

- 6.4.14 Mapei Inc.

- 6.4.15 Tesa SE (A Beiersdorf Company)

- 6.4.16 Pidilite Industries Ltd

- 6.4.17 RPM International Inc.

- 6.4.18 Sika AG

- 6.4.19 Wacker Chemie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Innovation and Development of Bio-based Adhesives

- 7.2 Shifting Focus Toward Adhesive Bonding for Composite Materials