|

市場調査レポート

商品コード

1850035

データセンターブレードサーバー:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Data Center Blade Server - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| データセンターブレードサーバー:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月20日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

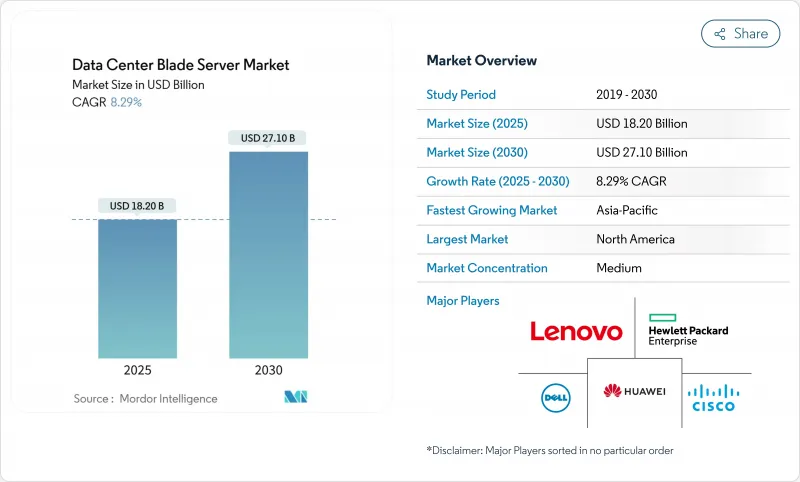

データセンターブレードサーバー市場の2025年の市場規模は182億米ドルで、2030年には271億米ドルに達し、CAGR 8.29%で拡大すると予測されています。

AIや機械学習ワークロードの導入が増加し、コンピュート密度の要件が変化しているため、ベンダーはコンピュート、ストレージ、ネットワーキングのリソースを分離するコンポーザブルな分離型ブレード設計に向かっています。このアーキテクチャの転換により、利用率の向上とワークロードの迅速な再配置が可能になる一方、直接液体冷却、シリコンフォトニクス製バックプレーン、高度なシャーシ管理ソフトウェアが、30kWを超えるようになったラックの電力エンベロープの管理に役立っています。北米は規模のリーダーを維持しているが、アジア太平洋はインド、中国、シンガポールでの大規模なグリーンフィールドの建設により、成長が加速しています。コロケーション施設が最大の顧客グループであることに変わりはないが、ハイパースケーラは、より高いラックレベルの効率を実現する専用AIブレードシステムに移行しており、技術的な課題を設定しています。

世界のデータセンターブレードサーバー市場の動向と洞察

AI/MLワークロードに対応するラックレベルの電力密度の急増

AI推論およびトレーニングクラスタは、現在、ラックのエンベロープを10~15 kWから30~50 kWへと押し上げています。Open Compute ProjectのOSAI仕様は、250kWから1MWのラック・アーキテクチャを目標としており、ブレード・ベンダーは高効率電圧レギュレータと直接液冷を統合することを奨励しています。デルのPowerEdge XE9680Lは、シャーシレベルのエアフロー、コールドプレートループ、AI専用アクセラレータが、サーマルスロットリングなしで共存できることを実証しています。国際エネルギー機関(IEA)は、AIに特化したデータセンターが2030年までに945 TWhを消費する可能性があると予測しており、電力効率の高いブレード設計が事業者戦略の中心に据えられています。

マイクロモジュラーDCの導入を加速するエッジとクラウドの融合

5Gの展開と超低遅延サービスは、コンピュートをネットワークエッジに押しやり、配線済みで冷却済みのマイクロモジュールデータセンターの需要を生み出しています。グーグルのモジュール式エッジ設備に関する特許は、電源と熱交換が統合された安全なマルチテナント型ラックアセンブリの重要性を裏付けています。電気通信事業者は、6,000億米ドルのCAPEX計画のかなりの部分をこのようなエッジサイトに割り当てており、ブレードベンダーに、制約のあるフットプリントに合わせた1/4ハイトのノードを供給する機会を与えています。

シリコンフォトニクスと800GbEバックプレーン移行による設備投資の急増

フォトニック集積回路と800GbEファブリックへの切り替えは、レイテンシと帯域幅の向上を可能にするが、新しいシャーシ、ミッドプレーンコネクタ、リタイマーカードを要求します。国家機関は、効率性の向上は認めているもの、特に中堅企業にとっては、初期導入に多額の資本コストがかかることに注意を促しています。CXL上のメモリ分割に関する調査では、投資回収に数年を要することが示唆されており、事業者はアップグレードの時期をずらすことを余儀なくされています。

セグメント分析

ティア3施設は、N+1冗長プロファイルが主流企業のSLAに合致していることから、2024年のデータセンターブレードサーバー市場の42.21%を占めています。ティア4施設は、数は少ないもの、AIトレーニングクラスターからの耐障害性要求により、CAGR 12.2%で成長すると予測されています。この勢いにより、ティア4は100%液冷シャーシとシリコンフォトニクス相互接続の実証実験場として位置づけられています。

一般的にエッジアグリゲーションやブランチワークロードにサービスを提供するティア1およびティア2施設のオペレータは、自動化を進めながらコスト規律を維持するために標準化されたブレードを採用しています。Infrastructure Masonsのレポートによると、現在の電力増加の90%はAIモデルのトレーニングによるものであり、その負荷は、より高い電力消費とラック密度に対応しなければならない控えめなサイトにまで波及しています。その結果、ベンダーは低階層の部屋に格納通路と後部ドアの熱交換器を後付けするキットをパッケージ化し、より広いデータセンターブレードサーバー市場の勢いを維持しています。

ハーフハイト・ブレードは、デュアルソケットCPU、十分なDIMMスロット、PCIe拡張をサポートし、ほとんどの仮想化とデータベース・タスクに対応します。ハーフハイト・ブレードは、企業のコロケーション・ラックの主力製品であり続けています。フルハイト・モデルは、クアッドソケット、インメモリ分析などのメモリバインド型ワークロードに引き続き対応します。

クォーターハイトおよびマイクロブレードノードは、10Uシェルフあたり16~32台のコンピュートスレッドに対応し、限られたエッジフットプリントに理想的なため、CAGR14.12%で最も急速に成長しているスライスです。ベンダーは現在、これらのコンパクトなスレーズにGPUアクセラレータを統合し、セルタワーサイトでのリアルタイム推論を可能にしています。Open Rack v3仕様との互換性により、同一キャビネット内での混在展開が可能になり、データセンターブレードサーバー市場のエッジ拡張の物語を支えています。

データセンターブレードサーバー市場レポートは、業界をタイプ(ティア1、ティア2、その他)、フォームファクター(ハーフハイトブレード、フルハイトブレード、その他)、エンドユーザー業界別(BFSI、製造、その他)、データセンタータイプ(ハイパースケーラ/クラウドサービスプロバイダ、その他)、地域(アジア太平洋、欧州、その他)に分類しています。市場予測は金額(米ドル)で提供されます。

地域別分析

北米は2024年にデータセンターブレードサーバー市場の42.23%を占め、バージニア北部、テキサス、シリコンバレーのハイパースケールキャンパスがその原動力となりました。ローレンス・バークレー国立研究所は、2023年の米国データセンターの電力使用量を176TWhと算出し、施設のPUEを削減する液冷ブレードの緊急性を高めています。カナダとメキシコは、地域の主権クラウドと災害復興ゾーンを通じて、さらに需要を増やします。

アジア太平洋は、2025~2030年のCAGRが12.54%で最も急成長する地域です。中国では大規模なAIクラウドクラスターが導入され、インドではデジタルエコノミーの目標に追いつくため、2030年までに設置容量を135万kWから5万kWに拡大する必要があります。シンガポールの政策枠組みは、高密度ブレードと熱回収型チラーを含む設計に優先的に容量ライセンスを与えます。日本とオーストラリアは、海底ケーブル陸揚げ局に沿ってエッジフットプリントを拡大し、コンテンツキャッシング用に1/4ハイトのブレードを組み込んでいます。

欧州は、厳しい効率性とデータ主権に関する規則の下で着実な拡大を示しています。Ecodesign 2019/424の改訂により、35℃以上の温水冷却をサポートするブレード・シャーシが奨励され、地域熱ループとの統合が容易になります。中東とアフリカでは、フィンテックやゲーム顧客にサービスを提供するクラウド・オンランプへの投資が集まっています。南米では、ブラジルのインターネット交換ハブを中心に設置が進んでおり、事業者は季節的なトラフィックのピークに対応するためにコンポーザブル・ブレードを導入しています。こうした地域力学が、データセンターブレードサーバー市場のグローバルな関連性を高めています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- ラックレベルの電力密度の急上昇により、AI/MLワークロードに対応

- エッジクラウドの融合によりマイクロモジュールDCの展開を加速

- 高いサーバー統合率により、OPEXと不動産コストが削減されます

- 液冷対応シャーシが規制上の優遇措置を受ける(EU、シンガポール)

- ハイパースケーラーによるコンポーザブル分散型ブレードの好感度が増加

- 市場抑制要因

- シリコンフォトニクスと800 Gb Eバックプレーンの移行による設備投資の急増

- 独自のシャーシエコシステムにおけるサプライヤーの集中

- マルチファブリック、分散アーキテクチャの管理におけるスキルギャップ

- ORAN/5Gの収益化の遅れにより、通信事業者DCのROIが長期化

- サプライチェーン分析

- 規制と持続可能性の情勢

- 技術展望(PCIe 6.0、CXL 3.0、シリコンフォトニクス)

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- ライバル関係の激しさ

- マクロ経済動向が市場に与える影響の評価

第5章 市場規模と成長予測

- データセンター層別

- ティア1とティア2

- ティア3

- ティア4

- フォームファクター別

- ハーフハイトブレード

- フルハイトブレード

- クォーターハイト/ マイクロブレード

- アプリケーション/ワークロード別

- 仮想化とプライベートクラウド

- 高性能コンピューティング(HPC)

- 人工知能/機械学習とデータ分析

- ストレージ中心

- エッジ/IoTゲートウェイ

- データセンターの種類別

- ハイパースケーラー/クラウドサービスプロバイダー

- コロケーション施設

- エンタープライズとエッジ

- 最終用途産業別

- BFSI

- ITおよび通信/CSP

- ヘルスケアとライフサイエンス

- 製造業とインダストリー4.0

- エネルギーと公益事業

- 政府と防衛

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- シンガポール

- オーストラリア

- マレーシア

- その他アジア太平洋地域

- 南米

- ブラジル

- チリ

- アルゼンチン

- その他南米

- 中東

- アラブ首長国連邦

- サウジアラビア

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- Strategic Initiatives

- 市場シェア分析

- 企業プロファイル

- Cisco Systems Inc.

- Dell Technologies

- Hewlett Packard Enterprise

- Huawei Technologies Co. Ltd.

- IBM Corporation

- Fujitsu Ltd.

- Lenovo Group Ltd.

- NEC Corporation

- Oracle Corporation

- Super Micro Computer Inc.

- Inspur Group

- Quanta Cloud Technology

- Gigabyte Technology

- Hitachi Ltd.

- AMD(Pensando)

- Nvidia Corp.(Grace Superchip platforms)

- Marvell Technology(DPU-centric blades)

- Broadcom Inc.(Switch-on-Blade)

- Advantech Co. Ltd.

- Silicom Ltd.

- ZTE Corporation