|

市場調査レポート

商品コード

1850010

米国の圧力センサー:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)US Pressure Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の圧力センサー:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月22日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

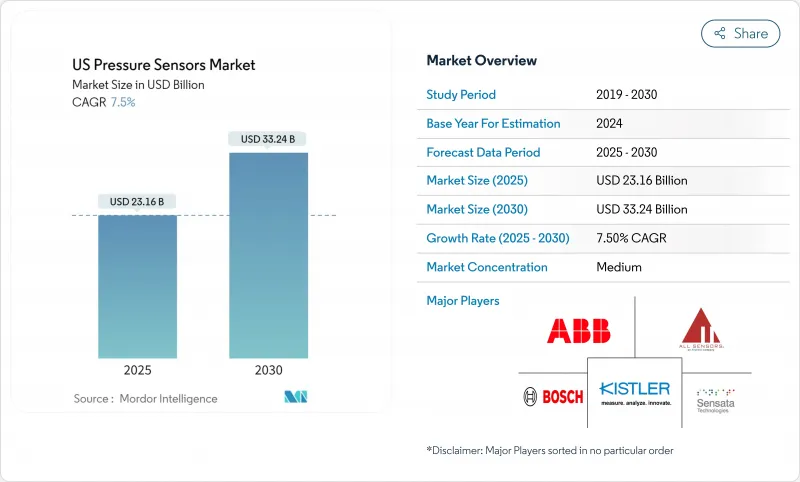

米国の圧力センサー市場は、2025年に231億6,000万米ドルとなり、2030年には332億4,000万米ドルに拡大し、CAGR 7.50%で成長すると予測されています。

半導体工場が真空とガス制御の公差を+-0.05%フルスケール以下に厳しくしているため、半導体メーカーがこの拡大の大きなシェアを牽引しています。自動車、医療、LNGインフラにおける安全規制の強化により、サプライチェーンがストレスに直面しても需要は底堅いです。MEMSとNEMSプラットフォームの融合により、コストカーブが再構築され、ナノスケールデバイスが新たな精度基準を設定する一方、AI対応モジュールへの統合が容易になります。バッテリー駆動のIoTシステムは、低消費電力と温度安定性を兼ね備えた静電容量式設計の採用を後押ししています。地域的には、南部がエネルギーコストの優位性から新工場を誘致し、ヘリウム不足が長期的な気密性を向上させるパッケージング革新を余儀なくしています。

米国の圧力センサー市場動向と洞察

TPMS交換サイクルがアフターマーケット需要を加速

第一世代タイヤ空気圧監視システムの寿命が尽き、センサー・サプライヤーはリピート・ビジネスを生み出しています。2007年のTREAD法以降に製造された車両は第2、第3の交換サイクルに入りつつあり、北東部と中西部では冬の路面塩害がバッテリーの消耗を早めています。Bartec Auto IDの2025 Rite-SensorBlue(R)は、Teslaモデル用に設計されており、Bluetooth診断を追加し、サービス間隔を延長するEVに最適化されたTPMSへのシフトを示しています。これらのユニットに組み込まれた予測アラートは、アフターマーケットを反応的な交換から定期的なメンテナンスへと移行させ、プレミアム価格帯を支えます。

家庭用血圧計のメディケア償還

メディケアとメディケイドの適用範囲が拡大され、現在では自己測定式血圧計の84%に達し、約140万人の高血圧受益者が利用できるようになりました。ミシガン州のプログラムでは、機器1台あたり最高75米ドルが支払われ、全国的な価格設定の基準となっています。このような償還状況は、遠隔医療プラットフォームにデータをストリーミングしながら、コンパクトなアームカフに収まる信頼性の高い低圧センサーへの急速な需要を煽っています。

スマートフォンの気圧計の飽和

現在、中位から上位のほぼすべての携帯電話に気圧センサーが搭載され、家電製品の数量成長に上限が設けられています。メーカーは、ウェアラブル用の超低消費電力型やドローン用の高精度高度計など、差別化された性能に軸足を置き、西海岸のサプライチェーンに集中する成熟した分野でニッチな利益を獲得しています。

セグメント分析

MEMSは2024年の米国の圧力センサー市場シェアの31.05%を占め、主流の自動車および産業用設計を支えています。歩留まりを最適化したシリコンラインは単価を低く抑え、グラフェン膜は感度を66µV/V/kPaまで引き上げ、高度計や医療用ウェアラブル機器の分解能を向上させています。ストレインゲージ・デバイスは、石油上流のような苛酷な環境では依然として好まれており、炭化ケイ素製は600℃でも確実に動作します。光学センサーは、強力な電磁場のある環境において優位に立ちます。

鋳造メーカーが共有金型を導入することで、生産規模はMEMSとのコスト差を縮め、大量生産が可能な医療用ディスポーザブルへの採用が拡大します。そのため、米国の圧力センサー市場では、AIやデータ暗号化を組み込んだミックスド・テクノロジー・モジュールにおいて、マイクロとナノのフォーマットが徐々に融合していくことになります。

ピエゾ抵抗アーキテクチャは、メーカーが成熟したCMOSバックエンドステップを再利用できるため、2024年の売上シェアは46.00%でトップとなりました。最近のシリコンカーバイドの改訂により、ゼロ出力の温度係数が1℃あたり0.08%に低減され、過酷な油田や航空宇宙のニーズに適合するようになりました。ASICに組み込まれた多項式回帰アルゴリズムは、残留誤差を0.008%FSまで削減し、精度をミッションクリティカルな期待に合わせます。

CAGR10.20%で増加すると予測される静電容量式センシングは、バッテリー駆動のIoTノードに不可欠な優れたエネルギー効率を提供します。ES Systemsの2024年リリースは、I2C、SPI、アナログ出力を提供しながら、+-0.25%FSの総合誤差を達成しています。共振技術は、0.1 Paの分解能で半導体チャンバー圧力をガイドする特殊真空ゲージに留まります。OEMがアプリケーション固有のしきい値に合わせて性能を調整できるように、ベンダーは複数の技術を単一パッケージに統合しているため、米国の圧力センサー市場では競合の重複が見られるでしょう。

米国の圧力センサー市場レポートは、センサータイプ別(MEMS、ひずみゲージ、その他)、技術別(ピエゾ抵抗、静電容量、その他)、出力インターフェース別、圧力範囲別、用途別(自動車、医療、産業、家電、その他)、米国地域別(北東部、中西部、その他)に分類されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- TPMSの交換サイクルがアフターマーケットの需要を加速

- 家庭用血圧計のメディケア払い戻し

- OSHA LNG連続ログ義務

- 半導体工場の超高精度化の要求

- 市場抑制要因

- スマートフォンの気圧計の飽和

- ヘリウム不足によりMEMSパッケージングコストが上昇

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- センサータイプ別

- MEMS

- ひずみゲージ

- NEMS

- 光学

- 技術別

- ピエゾ抵抗型

- 静電容量式

- 共鳴型

- その他

- 出力インターフェース別

- アナログ

- デジタル(IC/SPI)

- 圧力範囲別

- 10 kPa未満(低)

- 10 kPa 1 MPa(中圧)

- 1 MPa超(高)

- 用途別

- 自動車

- 医療

- 家電

- 産業

- 航空宇宙および防衛

- 飲食品

- HVAC

- その他

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Honeywell International Inc.

- Sensata Technologies Inc.

- Bosch Sensortec GmbH

- Emerson Electric Co.(Rosemount)

- ABB Ltd.

- Infineon Technologies AG

- STMicroelectronics NV

- Tektronix-Kistler Group

- NXP Semiconductors NV

- Panasonic Industry Co.

- TE Connectivity Ltd.

- Omron Corporation

- Pressure Systems Inc.

- All Sensors Corp.

- Endress+Hauser AG

- Rockwell Automation Inc.

- Yokogawa Electric Corp.

- Siemens AG

- Kulite Semiconductor Products Inc.

- TDK-Invensense Inc.